“The hardest thing in the world is to understand Income Tax”- -Albert Einstein

When it comes to income tax there is a whole lot of fuss among individual tax payers. They more often understand a very little and get confused. Let me tell you what made me write this article before you think why I am I late to the Budget 2020 party. I was talking to a friend of mine last day. His tax liability under new regime will be Rs. 1,25,000 for AY 21-22 and he was asking me very genuinely if he can reduce his tax burden to Rs. 50,000 by investing Rs. 75,000 in LIC. He not only mixed up the benefit of old regime with the new regime but also got the calculation completely wrong by deducting the allowable deductions from total tax liability instead of deducting from Gross Total Income.

Budget 2020 introduced a new personal income tax regime for individual tax payers with more tax slabs and lower tax rates but it came with a catch of removal of all available deductions and exemptions. To add to the confusion, the Finance Minister gave tax payers a choice to choose between new regime and old regime. This in fact made the whole process more complex instead of making it simpler. We will try to understand the current tax system first and then compare it with the new regime.

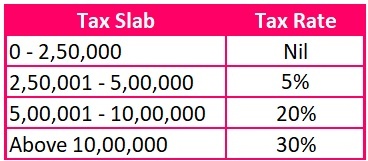

Current tax system – High tax rates with lot of scope for tax planning

Though tax rates are high here there is a lot of scope to pay reduced tax with proper tax planning. The existing rates are as below:

The income tax law allows the individuals to claim various exemptions and deductions. HRA exemption, Leave travel allowance, standard deduction of Rs. 50,000, Health insurance premium, Interest portion of housing loan, Savings account interest, various deductions under 80C like LIC, PF, ELSS, Principal portion of housing loan etc. being few among them. The tax is calculated on the income after claiming all the available exemptions and deductions.

The taxable income can be reduced in lakhs if he is willing to invest. This scheme encourages the tax payers to make investments and save tax to a great extent.

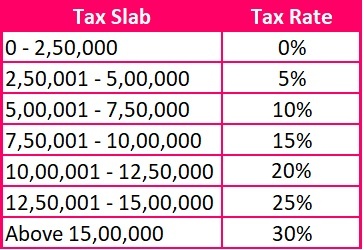

New Regime – Lower Tax Rates with no deductions

Under new regime, the government has introduced more slabs and low tax rates up to Rs. 15,00,000. This is very simple and plain to calculate as the tax payer can’t claim any deduction from his total income. The tax rates under this regime is as below:

As most of the exemptions and deductions are not applicable, this will benefit the sect who don’t usually claim any deduction or very little deduction. People who opt this model don’t save money and end up spending a lot. This is in fact a bad phenomenon in the long run both for the individual and the investment companies.

New Regime vs Old Regime – A comparative case study

Let’s deep dive into the topic and try to understand this from a practical point of view.

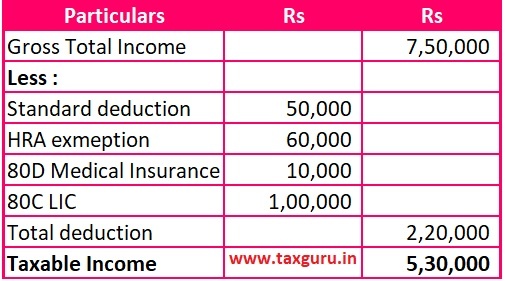

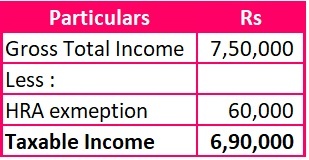

Mr. Smart earns Rs.7,50,000 per annum including HRA of 60,000. He invests Rs. 1,00,000 in LIC (80C). He pays medical insurance premium of Rs. 10,000 per year.

Tax liability of Mr. Smart under new regime will be:

Now, let’s calculate the tax liability under Old regime:

Since Mr. Smart has some allowable deductions. The first step is to calculate his taxable income.

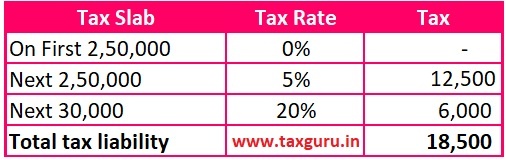

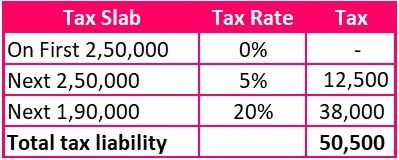

Now it’s the time to calculate the tax liability of Mr. Smart under old regime.

Note: It’s assumed that whole HRA received by the tax payer is allowable under income tax laws.

*Cess is not taken into account while calculating the final tax liability

Now, there is one very interesting point. Say if Mr. Smart is willing to invest 30,000 more in LIC, then his tax liability will be ZERO. This is on account of relief under section 87A. This section gives a tax relief of up to Rs. 12,500 for small tax payers.

It’s crystal clear that Mr. Smart should opt for old regime from the above study.

What if Mr. Smart doesn’t invest in LIC and pay medical insurance?

The tax computation under new regime will remain same as there is no change in his income.

However, the tax computation under old regime will change drastically.

Calculation of Taxable Income

Calculation of Tax Liability:

In this scenario, Mr. Smart should act smart and opt for new regime as its beneficial by Rs. 13,000.

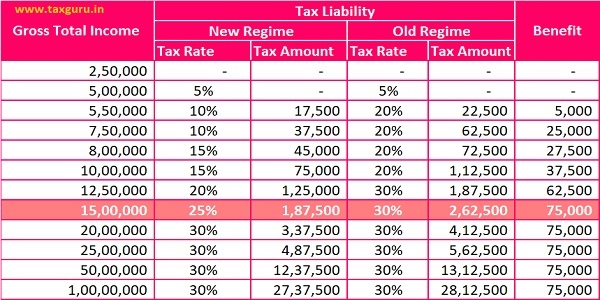

One can save up to Rs. 75,000 (excluding surcharge & cess) opting new regime. A comparative study is as below:

Notes:

-Its assumed that the individual has no applicable deductions/exemptions as per old regime including loss on self-occupied house property.

-Tax liability is calculated excluding cess and surcharge (if any).

-87A relief is applicable for individuals earning up to Rs.5,00,000 and hence no tax.

-Basic exemption income slab in case of a senior citizen and super senior citizen remain at the same 3 lakhs and 5 lakhs respectively.

Conclusion

It’s very clear that the changes introduced doesn’t make things easier for tax payers. One shall choose the regime which is most beneficial for him. New regime will do good to someone who is not intending to invest any money in any tax savings plan.

If you are looking to fulfill your financial obligation, namely- wealth creation through investments in tax saving instruments, paying premium to address your life/health insurance needs, EMI on educational loan, buying a house with home loan etc. the older regime still works in the interest of your financial wellbeing.

Download tax planner in Excel Format

I hope you have found the information in the article useful. If you would like to discuss any of the points raised, please contact me at rahulrnambiar91@gmail.com

Thanks for clarifying the confusion regarding old and new regime. Being a pensioner with deposits, now it is clear that I should opt old. Keep guiding fogged souls like me..thx

Sir. Quite knowledgeable. Kindly send me the full article to my above email. Thank you for helping us as it was quite confusing. I am a pensioner drawing less than five lakhs per annum (more than four lakhs. ) I have a SCSS account and a few FDs For me I feel old tax regime is more appropriate.

Awesomely elaborated Rahul sir, nice.

Thanks for letting me understand this n solving some criticalities from my knowledge base.

Very benefiting knowledge. Kindly send me this full article to my above given Email address i.e. kendivan@yahoo.com

I shaal be grateful.

Confusion free narration n calculation examples.

Even though u r young, u got old world virtues in u. I am happy to go through this article. U have very vividly explained the situation. I am in this line since 1922Act, and continuing by the grace of God. Keep it up. All success to u… With best wishes Kunde

Very helpful artice…