Case Law Details

Sanjay Jain Vs Enforcement Directorate (Delhi High Court)

In the case of Sanjay Jain vs. Enforcement Directorate (Delhi High Court), the court considered various factors before granting bail to the petitioner. The ruling took into account precedents, the completion of investigation, absence of incriminating evidence, and the petitioner’s background.

Non-Arrest of Co-Accused: Relevant Factor for Bail: The court emphasized that the non-arrest of co-accused is a relevant factor in bail considerations. Citing judgments from previous cases, including Dr. Bindu Rana vs. Serious Fraud Investigation Office and Ramesh Manglani vs. ED, the court highlighted the significance of this factor in the bail decision-making process.

Completion of Investigation and Lack of Incriminating Evidence: The court noted that the investigation against the petitioner was complete, and no incriminating material was recovered from him. Despite searches conducted by multiple agencies, no evidence supporting the respondent’s claims was found. Additionally, the petitioner had cooperated with the investigation on multiple occasions.

Conditions for Bail: After considering the petitioner’s background, travel history, and criminal record, the court granted regular bail. Various conditions were imposed, including restrictions on leaving the country, appearing before the court, joining the investigation when directed, and refraining from criminal activities or tampering with evidence.

Conclusion: The Delhi High Court’s ruling in the Sanjay Jain bail case underscores the importance of considering multiple factors in bail decisions. Precedents and legal principles regarding the non-arrest of co-accused, completion of investigation, and absence of incriminating evidence played a crucial role in the court’s decision-making process.

FULL TEXT OF THE JUDGMENT/ORDER OF DELHI HIGH COURT

1. The present petition has been filed under Section 45 of the Prevention of Money Laundering Act, 2002 read with Section 439 of the Code of Criminal Procedure, 1973 seeking regular bail in connection with ECIR No. DLZO-I/43/2021 dated 20.05.2021 registered by the respondent/ED.

FACTS

2. The Enforcement Case Information Report (hereinafter referred to as ‘ECIR’) was registered against the petitioner and others on the basis of FIR No. RC221/2021/E0009 dated 17.05.2021 registered by the CBI under Sections 120B read with 420 IPC and Sections 13(2) read with 13(1)(d) of the PC Act, 1988.

3. The summary of the allegations contained in the FIR registered by the CBI are as follows: –

a. Two complaints were forwarded to the CBI against the MD, Indian Farmers Fertilizer Cooperative Limited (hereinafter referred to as ‘IFFCO’) relating to subsidy fraud in IFFCO by opening Kisan International Trading, exchange of illegal commissions in import of raw materials and fertilizers, manipulation of sales data of fertilizers for claiming higher subsidy etc.

b. During scrutiny and verification of the complaints by the CBI, specific inputs were received from reliable sources alleging serious irregularities committed by the MD, IFFCO and other board members of IFFCO as well as MD, Indian Potash Limited (hereinafter referred to as „IPL‟) and others resulting in huge losses to both the entities and undue pecuniary gain to them and their family members.

c. It is alleged that the accused persons including the petitioner entered into a criminal conspiracy amongst themselves and during the period from 2007-2014 cheated and defrauded IFFCO, IPL, the general shareholders of these entities, as well as, the Government of India by fraudulently importing fertilizers and other materials at inflated prices and claimed higher subsidy thereby causing loss to the public exchequer. It is alleged that the commission from the supplies was siphoned off and the same was done through a complex web of fake commercial transactions through multiple companies which were owned by the accused persons to camouflage the fraudulent transactions as genuine.

d. It is the case of the respondent that IFFCO set up its 100% subsidiary namely, M/s Kisan International Trading FZE in Jebel Ali, Free Zonal Dubai for importing fertilizers and other raw materials from foreign companies/firms. It is alleged that the modus operandi adopted by the accused persons was that original bills were raised by the foreign manufacturers/suppliers (M/s Uralkali Trading Ltd.) at inflated prices to cover the bribe money which was to be paid to the Managing Directors of IFFCO and IPL. It is further alleged that incentives were paid through intermediaries/hawala

e. The commission was received by the sons of the Managing Directors of IFFCO and IPL, respectively through an individual, namely Rajeev Saxena, who in order to justify the receipt of commission from M/s Urakali Trading Ltd. (hereinafter also referred to as “Uralkali”) would execute consultancy agreements without rendering any consultancy services. Subsequently, the commission so received by Rajeev Saxena was transferred by him to the sons of the Managing Directors of IFFCO and IPL as per the instructions of the middleman Pankaj Jain by again executing consultancy agreements with the companies of the sons of the Managing Directors of IFFCO and IPL, respectively without rendering any consultancy services.

f. The specific allegation against the petitioner is that he along with the co-accused acted as intermediaries who channelized the ill-gotten money through various firms and companies registered either in their names or in the names of the sons of the Managing Directors of IFFCO and IPL. It is further alleged that the petitioner along with other co-accused are the owners/key persons of Rare Earth Group and M/s Jyoti Trading Corporation, Dubai which imports fertilizer products on a very large scale.

g. It was further revealed that out of the total illegal commission, an amount of USD 80.18 million (Rs. 481 Crores approx.) was channelized through Rare Earth Group and the remaining amount of USD 34.40 million (Rs. 204 Crores approx.) has been received by the sons of the Managing Directors of IFFCO and IPL either in the accounts of the firms/companies owned by them or in cash.

h. It also transpired that Rare Earth Group Commodities, DMCC (beneficially owned by Pankaj Jain) supplied a large quantity of Rock Phosphate to IFFCO during the period 2007-11 directly or through Kisan Trading It was further revealed that the company of Pankaj Jain namely, Ferttrade DMCC also supplied fertilizers to IFFCO from 2012 onwards. Trans Globe DMCC, a company of Pankaj Jain also supplied fertilizers to IFFCO. Rare Earth Commodities DMCC and Trans Globe DMCC also supplied fertilizers to IPL.

4. In a nutshell, as per the case of the respondent, the petitioner herein has received the proceeds of crime through two routes which are as follows:

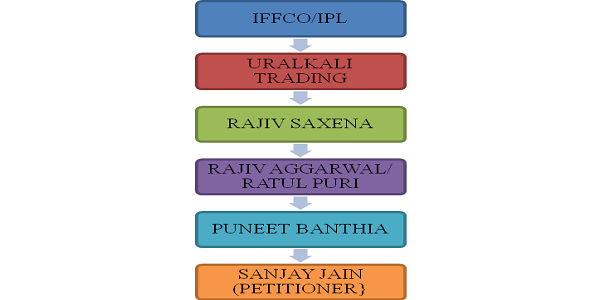

Direct Route/Ratul Puri Route – Under this route, Rajeev Saxena would receive proceeds of crime from Uralkali, then he would pay cash to the petitioner through one Rajiv Aggarwal (an associate of Mr. Ratul Puri). One Punit Banthia used to pick up cash from Rajiv Aggarwal on behalf of the Petitioner. The Direct Route could be depicted by the following flow chart:

Indirect Route/Rayon Trading Route – Under this route, Rajeev Saxena after receiving the proceeds of crime would send money through an entity called Rayon Trading to the Alankit group of companies. Alankit group of companies (owned by Alok Aggarwal and Ankit Aggarwal) in turn made payments to the petitioner. The money used to be handled by Sunil Kumar Gupta and Mahesh Upadhyay and given to various persons on behalf of the petitioner.

SUBMISSIONS ON BEHALF OF THE PETITIONER

5. Mr. Dayan Krishnan, learned Senior Counsel appearing for the petitioner at the outset submits that in order to initiate an investigation and subsequent prosecution under the Prevention of Money Laundering Act, 2002 [in short “the PMLA”] there should be a commission of a scheduled offence and there should be generation of proceeds of crime from such scheduled offence. The person sought to be prosecuted should be directly or indirectly involved in any process or activity connected with the said proceeds of crime and the money trail shall remain unbroken for curtailing the personal liberty of the accused.

6. Krishnan further submits that the predicate offence under the Act should also hold good i.e. hold authority under the law, which is based on cogent material that would lead to a reasonable inference that the accused would be convicted of the predicate offence. If the predicate offence is weak, the same shall enure in favor of the petitioner.

CBI LACKS THE REQUISITE JURISDICTION TO REGISTER THE FIR UNDER THE PROVISIONS OF PREVENTION OF CORRUPTION ACT, 1988

7. The learned Senior Counsel has drawn the attention of the Court to Annexure P-2, the RC221/2021/E0009 dated 17.05.2021 registered by the CBI under Sections 120B r/w 420 IPC and Sections 13(2) r/w 13(1)(d) of the PC Act, 1988, to submit that although the RC was registered by the CBI under the provisions of the Prevention of Corruption Act, but at the relevant time i.e. at the time of import from 2007-2014, neither IFFCO nor IPL was a public company, rather they have been private companies/entities since the year 2000. In this regard, the learned Senior Counsel referred to letters dated 21.08.2017 and 05.09.2018 of the CBI (annexed as Annexure P-13 to the paper book) wherein the CBI has already taken a categorical stand that CBI has no jurisdiction over Indian Potash Limited since it is not a public authority. The letter dated 21.08.2017 reads as under:

No. 179/CO AC 1 2016 A 0009

O/o Supdt. of Police

Central Bureau of Investigation

Anti Corruption –I

B-5 CBI Hqrs., 8th Floor

CGO Complex, Lodhi Road

New Delhi 110003

Tele-fax:-011-24360361

Dated:21.8.2017

To

Sh.Kulwant Rana,

Under Secretary to the Govt. of India,

Ministry of Chemicals & Fertilizers,

Department of Frtilizers,

Shastri Bhawan, New Delhi.

Sub: Irregularities in import of fertilizers –regarding

Sir,

Kindly, refer your office letter F.No.16/4/14-Vig (L.S) dated 12.07.2017 on caption mentioned above.

In this regard, it is informed that the competent authority of CBI has closed this complaint because CBI has no jurisdiction over Indian Potash Limited which at present is not a public authority.

For information please.

Sd/-(Rajiv Ranjan) Supdt. of Police CBI/AC-I/New Delhi.

8. To the same effect is the letter dated 05.09.2018 written by the CBI to the Member of Parliament, which reads as under:

No. 274/CO AC 1 2016 A 0009

O/o Supdt. of Police

Central Bureau of Investigation

Anti Corruption –I B-5 CBI Hqrs., 8th Floor

CGO Complex, Lodhi Road

New Delhi 110003

Tele-fax:-011-24360361

Dated:5.9.2018

To

Dr. Arun Kumar,

Hon‘ble Member of Parliament,

(Lok Sabha),

171-172, South Avenue,

New Delhi.

Sub: Legal Notice for Filing Public Interest Litigation Against Scam in import of Fertilizers By Indian Potash Limited on Government Account-regarding.

Sir,

Kindly refer to your letter dated 08.08.2018.

It is to inform that allegations/complaint mentioned in your letter was already analyzed by the CBI. It is found that CBI has no jurisdiction over Indian Potash Limited since it is not a public authority.

Hence, complaint was closed by the CBI after taking approval from the competent authority.

Thanking You

Supdt. of Police

CBI/AC-I/New Delhi.

9. Further referring to the RC, the learned Senior Counsel submits that the said RC was registered on the basis of two complaints dated 14.06.2016 and 05.09.2016, whereas, on the other hand, the CBI in the year 2017 as well as in 2018 had already taken a stand that it does not possess jurisdiction over IPL. According to the learned Senior Counsel, this contradiction, as well as, the delay in registration of FIR makes it highly improbable that the petitioner would be convicted in the predicate offence.

10. In addition to the aforesaid, Mr Krishnan submits that the co-accused in the present matter i.e. the Managing Directors of IPL and IFFCO have approached this Court by filing WP(C) 1051/2021 and WP(C) 1052/2021, respectively, challenging the registration of RC by the CBI and vide common order dated 31.05.2021 this Court has been pleased to direct that no coercive steps shall be taken against them. The relevant paragraph of the order dated 31.05.2021 reads as under:

“7. Till further orders, no coercive steps shall be taken against the petitioners, however, they shall join investigation as and when called by SHO/IO.“

ANOMALIES IN THE CASE OF THE RESPONDENT IN THE INDIRECT ROUTE/COMMISSION THROUGH RAYON TRADING

11. The submission of the learned Senior Counsel in respect of the indirect route is that in the said route the chain remains inconclusive and suffers from various material irregularities at each leg of this route / money trail, which are enumerated below:

a. IFFCO and IPL have paid Uralkali for fertilizers at inflated prices to cover the commission amount which was subsequently received by the accused persons –

i. It is the submission of the learned Senior Counsel that the respondent has failed to produce any evidence showing payment of inflated prices by IFFCO and IPL. For this purpose, the attention of the Court was drawn to Annexure P-10, the Office Memorandum dated 23.07.2012 issued by the Ministry of Chemicals and Fertilizers in response to a letter written by the Directorate of Enforcement dated 24.02.2012, to submit that the Ministry of Chemicals and Fertilizers has in unequivocal terms dismissed allegations of any wrongdoing on part of IFFCO.

ii. He submits that the said memorandum states that up till the year 2010, the subsidy which an entity was entitled to claim was subject to the weighted average price of the entire industry or based on the price of import by an entity, whichever was lower.

iii. He submits that after 01.04.2010 the subsidy which was payable on imports was directly linked to the percentage of the chemical component in the fertilizer and not the import price thereof. This makes the case of the prosecution doubtful as the subsidy payable was not dependent upon the price of the import or the industry average.

b. Once the money for commission was received by Uralkali Trading, the money was transferred to Rajeev Saxena which was done by creating forged and fabricated consultancy agreements

i. Mr Siddharth Aggarwal, the learned Senior Counsel, who also appeared on behalf of the petitioner, submits that the sole incriminating material collected by the respondent in this regard are the statements of Rajeev Saxena, which are unreliable given the inherent contradictions. He submits that Rajeev Saxena is not reliable as a witness, inasmuch as, it is the respondent’s own case that Rajeev Saxena is guilty of withholding, providing partial documents, as well as, forging documents. To buttress his contention, the attention of the Court is invited to an application under Section 306 CrPC filed by the respondent/ED seeking revocation of tender of pardon granted to Rajeev Saxena in another case titled “The Directorate of Enforcement v. Gautam Khaitan and Ors.”.

ii. He submits that with respect to the statement of Rajeev Saxena, no person from Uralkali has been examined by the respondent/ED to the effect that the money which has been received by Rajeev Saxena was against those very shipments which were imported by IPL/IFFCO. Further, Rajeev Saxena has taken different stands before different investigating agencies, in respect of the above transaction.

iii. It is also contended that Rajeev Saxena is also a co-accused in the present matter and the statement of the co-accused being a weak piece of evidence cannot be used by the prosecution to deny the benefit of bail to the petitioner.

iv. He further submits that the respondent has failed to establish a link between the petitioner and Rajeev Saxena, in as much as there is no record to show any communication between them. Further, the prosecution complaints are based entirely on the unsubstantiated false statements and internal records of Rajeev Saxena (co-accused), thus, the veracity of the allegations against the petitioner is doubtful.

c. Thereafter, the money was transferred to Rayon Trading by Rajeev Saxena –

i. Mr Aggarwal submits that no proof of payment of money in the form of bank account statements has been placed on record by the ED to show any transaction between the entities of Rajeev Saxena and Rayon Trading. He submits that reliance in this regard has been placed by the respondent solely on plain paper (excel sheet) entries and the said document is not a contemporaneous record and has been prepared for investigating agencies. Further, the said document submitted by Rajeev Saxena is not a ledger maintained during the course of business and cannot pass the test of Section 34 of the Indian Evidence Act, 1872.

d. Once the money was received by Rayon Trading, the same was transferred to Alankit Group/ Alok Aggarwal –

i. Mr. Aggarwal submits that the purpose of payment between Rayon Trading and Alankit Group/Alok Agarwal has not been established as the transactions between the two entities have been explained by Alok Agarwal as genuine in his statement dated 28.11.2022 under Section 50 of the PMLA. The relevant part of the said statement reads as under:

”Q.5 Please explain the transactions figuring in the Ledger account of Rayon General Trading LLC in the books of M/s Alankit Global Resources DMCC as submitted by Sh. Ankit Agarwal vide his statement dated 24.11.2022?

Ans 5. These transactions pertain to the consultancy services provided by Alankit Global Resources DMCC to Rayon General Trading LLC. I do not remember the details thereof, however, I undertake to provide the same along with supporting documents by 30.11.2022.

Premised on the above statement the learned Senior Counsel submits that the statement of Alok Agarwal under Section 50 PMLA has to be read in favor of the petitioner.

e. Thereafter, the proceeds of crime have been transferred by Alankit Group to the petitioner

i. Mr Aggarwal submits that to prove the transfer of money by Alankit Group to the petitioner, the respondent/ED has relied entirely on the personal ledgers of Sunil Kumar Gupta and contrary to law, Section 22 of the PMLA has been invoked to read this ledger against the petitioner. Further, it is submitted that Sunil Kumar Gupta has admitted that he has no knowledge of whether these payments were actually made and has admitted to merely noting the entries on the directions of Alok Agarwal and Ankit Agarwal and thus his statement is at best hearsay.

ii. In respect of the cash transactions, it is submitted that each of the persons who have alleged to have received cash from Alankit Group on the petitioner‟s behalf, has denied this fact in their statements under Section 50 of the PMLA and thus must be read in favour of the petitioner. Reference in this regard is made to the statements of Rakesh Jain, Sanjeev Jain, Rahul Mittal, Manish Jain and Sharad Jain.

iii. In respect of the RTGS/Cheque transactions in the personal ledger of Sunil Kumar Gupta, it is submitted that the said transactions are legitimate and have been fully disclosed in accordance with law, on which applicable tax has been paid.

ANOMALIES IN THE CASE OF THE RESPONDENT IN THE DIRECT ROUTE

12. It may be noticed that the first two steps i.e. steps at sub paras (a) and (b) in para 11 above, insofar as payment from IFFCO/IPL to Uralkali and then from Uralkali to Rajeev Saxena, are concerned, the same are common in both the routes, therefore, the submissions apropos the said two steps in the indirect route are same in the direct route, therefore, they are not being repeated for the sake of brevity.

13. The submission of the learned senior counsel in respect of the direct route is that even in the said route there are numerous breaks in the money trail, and such breaks at each step are enumerated below:

a. the proceeds of crime from Rajeev Saxena came to the hands of Ratul Puri and his employee, Rajiv Agarwal

i. The learned Senior Counsel for the petitioner submits that neither Ratul Puri nor his employee Rajeev Aggarwal have supported the case of the prosecution. Reliance in this regard is placed on the statement of Ratul Puri recorded on 20.10.2022 under Section 50 of the PMLA, the relevant part of the statement reads as under:

”Q1. Was any cash delivered to you by Sh. Sanjay Jain through Sh. Rajeev Agarwal?

Ans.1. No, I do not who Sh. Sanjay Jain is.

Q2. Did Sh. Rajeev Saxena give any corresponding credit entries to you or your companies abroad in lieu of cash delivered by you to Sh. Sanjay Jain though Sh. Rajeev Agarwal?

Ans. 2. No.

Q3 You are being shown statement dated 11.06.2021 of Sh. Rajeev Saxena running into 74 pages. Please go through it and comment as far as it pertains to you?

Ans.3. l have seen and read statement dated 11.06.2021 of Sh. Rajeev Saxena running into 74 pages. l have put my dated signatures on all the 74 pages as a token of having read the same. I state that I strongly deny the statemenT made by Sh. Rajiv Saxena. I have no such account with him which he has enumerated in excel spreadsheets. My company’s business dealings were limited to sourcing of Solar panels.

Q.4 Please refer to Question number 15 of statement dated 03.07.2019 tendered before Income Tax Authorities and accepted vide his statement dated 11.06.2021 under section 50 of PMLA, 2002 of Sh. Rajeev Saxena, wherein he has referred to payment of Rs. 5 crores and 1 crores to Sh. Pankaj Jain on 15.01.2014 and 19.08.2013 respectively through you. Do you know Sh. Pankaj Jain and comment on the nature of these transactions?

Ans. 4. I do not know Sh. Pankaj Jain and no such transactions were undertaken. I strongly deny the statement made by Sh. Rajiv Saxena.

Q5 Please refer to Question number 28 of statement dated 03.07.2019 tendered before Income Tax Authorities and accepted vide his statement dated 11.06.2021 under section 50 of PMLA, 2002 of Sh. Rajeev Saxena, wherein he has referred to payments of various amounts through you as detailed under:

a. Rs. I crores to Sh. Sanjay Jain on 16.01.2011

b. Rs. 3 crores to Mr. Amarendra Dhari Singh on 20.07.2011

c. Rs. 2 crores to Mr. Reddy on 14.12.2011

d. Rs. 1.5 crores to Sh. Sanjay Jain on 14.12.2011

e. Rs. 0.75 crores to Sh. Sanjay Jain on 20.12.2011

f. Rs. 1 crore to Sh. Sanjay Jain on 08.02.2016

g. Rs. 1 crore to Sh. Sandeep Khanna on 07.08.2016

Please explain the source of money given by you to these persons.

Ans. 5. No money was given by me to these persons and I strongly deny the statement made by Sh. Rajiv Saxena.

I request that my further statement may be recorded on 21.l 0.2022.

I undertake to appear on 28.10.2022 at 1500 hours.

The above statement of mine running into two pages has been tendered voluntarily on my own without any fear, pressure, force, coercion, threat or inducement and the same is true and correct to the best of my knowledge and belief. It has been typed on a computer at my request.‖

ii. Mr Aggarwal contends that to a similar effect is the statement of Rajiv Aggarwal recorded under Section 50 of the PMLA on 14.10.2022, the relevant part of which reads as under:

”Q.1 Have you ever interacted with Rajiv Saxena in relation to payment of cash in India to Sanjay Jain brother of Pankaj Jain of Dubai?

Ans.1 No.

Q.2 Have you ever interacted with Pankaj Jain or Sanjay Jain in any matter?

Ans.2 No, I do not know these persons at all. I have never met them or interacted with them in any matter at all.

Q.3 Have you ever had any telephone conversations with these two persons?

Ans.3 No.

Q4. Were you having phone numbers of these two persons?

Ans.4 No. I was not having phone numbers of these two persons.

Q.5 Have you ever interacted with Puneet Banthia or Puneet in India for payment of cash in India?

Ans.5 No.

Q.6 Have you ever interacted with Puneet Banthia or Puneet in India for any other matter?

Ans. No.

Q.7 Have you ever had telephonic conversation with Puneet Banthia or Puneet?

Ans. No.

Q.8 Were you having phone numbers of Puneet Banthia or Puneet?

Ans.8 It was there in my telephone diary but I never interacted with him.

Q.9 Who gave you his phone number?

Ans.9 I do not remember.

Q.10 In what connection were you having his phone number?

Ans.10 I do not remember.

Q.11 How do you know him?

Ans. I do not know him.

Q.12 If you do not know him why were you having the phone number of a complete stranger in your telephone diary?

Ans.12 I do not remember in what context anybody has given his number to me. But as per my memory, I have never met him or interacted with him in any manner.

I request that my further statement may be recorded on 18.10.2022. I undertake to present myself at 1530 hours on 18.10.2022 to continue my further statement.

The above statement of mine running into two pages has been tendered voluntarily on my own without any fear, pressure, force, coercion, threat or inducement and the same is true and correct to the best of my knowledge and belief.

iii. He further submits that the statement of Rajeev Saxena would not be admissible as the same is hearsay as he has admitted that he did not coordinate the delivery of cash, which has been allegedly received by the petitioner. For this purpose, the learned Senior Counsel relied upon the statement of Rajiv Saxena recorded under Section 132(4) of the Income Tax Act, 1961, the relevant part of which reads as under:

“Q.19. How did you coordinate the transfer of cash without having any contact person in Delhi/India?

Ans. I was not coordinating the cash. The coordination was done by Rajeev Agarwal with the representative of Mr. Sanjay Jain i.e., Mr. Puneet.‖…

iv. Elaborating further, the learned Senior Counsel submits that according to Rajeev Saxena, it was Shahnawaz Khan, his employee, who was handling cash on his behalf. However, it stated by Shahnawaz Khan that he had no knowledge of the parties on whose behalf cash transfers were being carried out. The relevant part of Shahnawaz‟s statement dated 18.10.2021 under Section 50 of the PMLA reads as under:

“Q.15 Give the normal day to day work handled by you while you were working for Mr. Rajiv Saxena.

Ans. …. On being asked I stated that the party on whose behalf these transfer were being carried out was not know to me…‖

v. It is fairly submitted by Mr Aggarwal, learned Senior Counsel that only one person namely, Puneet Banthia in his statements recorded on 24.09.2021 and 10.10.2022 has supported the case of the prosecution to the effect that he (Puneet Banthia) carried cash from Ratul Puri to the petitioner. He, however, adds that the statement of Puneet Banthia is contradictory to his earlier statement given to Income Tax Authorities in 2019. Further, no figure/amount has been disclosed by Puneet Banthia and that the said transaction (of carrying cash) is of the year 2016, whereas, the ledgers recovered from Rajeev Saxena are only up till the year 2014. This according to Mr. Aggarwal shows that if any cash was carried by Puneet Banthia to the petitioner, the same has no connection with the transactions with Uralkali.

BAIL ON THE GROUND OF PARITY

14. Mr Aggarwal, the learned Senior Counsel for the petitioner submits that the petitioner is also entitled to be enlarged on bail in view of the fact that all the accused persons named in the first complaint dated 30.07.2021 and summoned by the Ld. Special Judge have already been enlarged on bail. The details of the said accused are as follows:

| S. No. | Name of Co-accused | Date and details of the bail order |

| 1. | Amarendra Dhari Singh | Released on regular bail vide order dated 05.08.2021 passed by this Court in BAIL APPLN No. 2293/2021 |

| 2. | Alok Kumar Aggarwal | Released on regular bail vide order dated 16.08.2021 passed by this Court. |

| 3. | Ankit Aggarwal | Granted Anticipatory bail vide order dated 26.10.2021 passed by this Court in BAIL APPLN No. 3619/2021 |

| 04. | Chandra Shekhar Jha | Released on regular bail vide order dated 21.09.2021 passed by the Trial Court. |

THE PETITIONER IS NOT LIKELY TO COMMIT ANY OFFENCE IN CASE HE IS ENLARGED ON BAIL

15. Mr Aggarwal submits that the petitioner had joined the investigation as and when directed by the Investigating Officer/Enforcement Directorate as well as other investigating agencies, who are investigating the same allegations against the petitioner.

16. He submits that the petitioner in the present case had joined the investigation on at least 10 occasions up to 06.10.2022 when the petitioner was arrested. Prior to his arrest, the petitioner had cooperated with all investigating officers, and it is not prudent to keep him in custody.

17. He submits that the investigation qua the petitioner is complete, in as much as the prosecution complaint has been filed on 05.12.2022. Further, all relevant documents and all digital devices including computers, mobile phones, laptops, hard disks etc., were either seized or duplicated.

18. He further submits that between 14.06.2016, the date of receipt of the complaint by the CBI, and 20.05.2021, the date of registration of the subject ECIR, the petitioner has travelled overseas approximately 26 times and he is not likely to flee from the administration of justice.

19. He contends that the antecedents of the petitioner are clean and no criminal case is pending against him except the predicate offence, ED‟s present complaint and Income Tax proceedings for the same allegations.

20. This according to the learned Senior Counsel establishes that the petitioner is not likely to commit any further offence in case he is enlarged on bail and prays for the petitioner to be enlarged on bail.

SUBMISSIONS ON BEHALF OF THE LEARNED SPECIAL COUNSEL FOR THE ED/RESPONDENT

THE PRESENT CASE IS NOT A CASE ONLY UNDER THE PREVENTION OF CORRUPTION ACT BUT ALSO UNDER SECTIONS 420/120B IPC

21. Per Contra, Mr. Zoheb Hossain, learned Special Counsel appearing for the respondent at the outset submits that even if for the sake of argument it is assumed that IFFCO and IPL are private companies and the provisions of the Prevention of Corruption Act are not applicable to the office bearers of IFFCO and IPL, the RC has also been registered under Sections 120B r/w 420 IPC, which are also scheduled offences under the PMLA and bare reading of the RC manifests that the offence of cheating against the accused persons is made out.

22. Elaborating further, he submits that the present case is not a simplictor case of subsidy fraud but the accused persons have also committed the offence of cheating as a result of which both IFFCO and IPL have suffered wrongful loss, and wrongful gain has been derived by the accused persons. It is also the contention of Mr Hossain that the shareholders of the above companies have also been cheated and defrauded as the price at which fertilizers were imported was inflated. He also urged that had the present offence not been committed by the accused persons, the price of import of fertilizers would have been substantially lower than the actual price at which fertilizers were imported.

23. In sum and substance, it is the contention of Mr Hossain that the present case is not a case of only subsidy fraud but has three different layers viz., (i) cheating at the level of the IFFCO/IPL (ii) cheating at the level of their respective shareholders and (iii) cheating at the level of the government by claiming higher subsidy.

VALIDITY OF THE PROCEEDINGS BY THE CBI CAN NOT BE QUESTIONED AT THE STAGE OF BAIL

24. Hossain also submits that the scheme of the PMLA makes it obligatory for the Court to assume that the scheduled offence exists and no doubt can be raised against the existence of the scheduled offence. It is also the contention of the learned counsel that the argument of the petitioner that the scheduled offence is under a cloud cannot be sustained in a bail application, all the more when the CBI, who had registered the scheduled offence, is not a party before this Court. Reliance in this regard was placed on the judgment of a co-ordinate bench of this Court in Satender Kumar Jain vs. Directorate of Enforcement, BAIL APPLN 3590/2022, the relevant paragraph of which reads as under:

“75. The simple fact is that CBI has filed the case of disproportionate assets against public servant Satender Kumar Jain and other persons including the other two petitioners, the cognizance of which has already been taken. Thus, the competent court is seized of the matter regarding the disproportionate assets and the present court cannot go into the question of validity of institution of such proceedings.”

25. Further, reliance was placed by Mr Hossain on the judgment of the Supreme Court in Vijay Madanlal Choudhary vs. Union of India, 2022 SCC OnLine SC 929, more particularly paragraph 253 thereof, to contend that the offence of money laundering will cease only when the accused is finally absolved in the scheduled offence. He submits that even if it is assumed that the allegations contained in the RC registered by the CBI does not make out the scheduled offence, the failure of the petitioner to array the CBI as a party before this Court leaves this Court unequipped to consider the validity of the RC or the material collected by the CBI during its investigation.

OFFICE MEMORANDUM OF THE DEPARTMENT OF FERTILIZERS DOES NOT ABSOLVE THE PETITIONER OF HIS GUILT

26. He invites the attention of the Court to the OM dated 23.07.2012, on page no. 483 of the bail application, to contend that the said office memorandum has itself used the words “even if that could happen” and “If the allegation of import of inputs at higher price is true for one company, it will be true for all”, which means that the office memorandum does not rule out that prices could not have been manipulated, under any circumstance.

27. He submits that at best, the office memorandum discounts the possibility of IFFCO having benefited due to the manipulation of import prices, but it nowhere negates the possibility of loss caused by the manipulative prices which included the commission paid to the sons of U.S. Awasthi and P.S. Gahlaut. He further submits that IFFCO and IPL are major players in the fertilizer industry and the price at which they imported the fertilizers affected the entire industry average. He refers to the OM to illustrate that for the month of April, the price at which fertilizer was imported by IFFCO was USD 69.60 and the industry average was USD 67.80, the industry price being lower was adopted for the said month. Had IFFCO paid its actual price after discounting the commission which is inbuilt into the import price say, USD 63, it would have resulted in a reduction of subsidy payable not only to IFFCO but also to various other importers.

28. To substantiate his submission that IFFCO and IPL are the major players in the fertilizer industry, he contends that during the year 2013-2014, the above two entities were paid Rs 5661.70 Crore of subsidy on imported P&K fertilizers out of a total of Rs. 13926.86 Crore paid to 33 entities which is roughly 40% of the total subsidy payouts. Similarly, for the year 2014-2015, it was Rs. 4003 Crore out of Rs. 8667.30 Crore being 46% of the total subsidy paid, which shows that the manipulation of prices by these two entities alone caused loss to the exchequer to a great extent.

CREDIBILITY OF MR. RAJEEV SAXENA CAN NOT BE QUESTIONED BY THE PETITIONER

29. Hossain submits that considerable emphasis has been laid that Rajeev Saxena who has stated as regards the complicity of the petitioner is not a credible witness. At the outset, Mr Hossain clarified that the revocation application seeking cancellation of approvership of Rajeev Saxena has not been filed in the present case but it has been filed in a separate ECIR bearing number 15/DLZO/2014. Additionally, he submits that the statement of Rajeev Saxena cannot be discarded, especially when the same has been corroborated by the independent material.

30. According to Mr Hossain, the allegation against Rajeev Saxena is with regard to the non-supply of documents and the allegations of fudging also relate to providing incomplete data and not false data. The file titled RP Consolidated USD.xls on which emphasis has been laid by the petitioner is indeed the correct data and the same is evident from the revocation application itself, therefore, what is being relied upon in the present case is the correct file which was subsequently discovered by the respondent in the laptop of Saxena.

31. He submits that the statements of Rajeev Saxena have been recorded under Section 50 of the PMLA, thus, the same are admissible in evidence. The credibility and reliability of the statements of Rajeev Saxena cannot be considered by this Court at this stage as the same will be evaluated by the learned Trial Court at the time of Trial. For this purpose reliance was placed on the judgment of the Supreme Court in Satish Jaggi v. State of Chattisgarh, (2007) 11 SCC 195, the relevant paragraph of which reads as under:-

“At the stage of granting of bail, the Court can only go into the question of the prima facie case established for granting bail. It cannot go into the question of credibility and reliability of the witnesses put up by the prosecution. The question of credibility and reliability of prosecution witnesses can only be tested during the trial.”

UNBROKEN MONEY TRAIL (THROUGH RAYON TRADING/INDIRECT ROUTE)

32. Mr Hossain submits that the money trail i.e. flow of proceeds of crime is unbroken and his submissions in this regard are as under:

a. Payment of money for fertilizers at inflated prices by IFFCO/IPL to Uralkali –

i. According to Mr. Hossain the business dealings between IPL and Urakali are established from bank statements and financial transactions between the parties. The attention of the Court is invited to the debit note dated 09.05.2014 amounting to USD 1,000,000.00 raised by IPL on Uralkali as well as the declaration dated 05.09.2014 under Section 10(5) of the Foreign Exchange Management Act, 1999, whereby IPL has stated that it was expecting a sum of USD 1,000,000.00 from M/s Uralkali Trading (Gibraltar) Ltd on account of “REBATES”.

b. Flow of Proceeds of crime from Uralkali to Rajeev Saxena/Entities controlled by Rajeev Saxena

i. Hossain contends that once money was paid to Uralkali by IFFCO/IPL, the commission amount was thereafter paid to Mr. Rajeev Saxena through companies which were owned by him. For this purpose, the attention of the Court was drawn to the bank statements of Mr. Rajeev Saxena, which were produced by him under Section 50(2) of the PMLA. Referring to the said bank statements, it is contended that on various occasions, Uralkali Trading (Gibraltar) Ltd. had made payments in foreign currency to Pacific International FZC and Midas Metals International LLC and it is not in dispute that the said two companies belong to Mr. Rajeev Saxena.

ii. In respect of the above financial transactions, Mr. Hossain draws the attention of the Court to the statement dated 05.06.2021 of Mr. Rajeev Saxena recorded under Section 50 of the PMLA, to contend that the above-named companies of Rajeev Saxena received funds from Uralkali General Trading, Gibraltar; Gulf Maine DMCC, Dubai on behalf of the petitioner (Sanjay Jain), Pankaj Jain and A.D. Singh and that these payments were actually received as commission. It is also the contention of the learned counsel that there was no agreement between the companies of Rajeev Saxena and Uralkali General Trading, Gibraltar. The relevant part of the statement of Mr. Rajeev Saxena reads as under: –

“Ques. No.2. From the above mentioned statements it is seen that Midas Metal International LLC and Pacific international FZC have received huge amounts from Uralkali General Trading, Gibraltar ; Gulf Marine DMCC, Dubai. Please explain these payments and logic behind these.

Ans. No.2. I have already stated in my above mentioned statements in answer no 1 which were recorded under section 37 of FEMA, 1999. However, I re-state that the my above mentioned group companies i.e. Midas Metal International LLC and Pacific international FZC were receiving funds from Uralkali General Trading, Gibraltar ; Gulf Marine DMCC, Dubai on behalf of Sh. Pankaj Jain, Sanjay Jain and A.D. Singh. The said payments were received as commission for which invoices were raised on the instructions of all these three viz Sh. Pankaj Jain, Sanjay Jain and A.D. Singh. Further, I also state that there is no agreement from these entities with Midas Metal International LLC and Pacific international FZC for the said work. Upon being asked about the structure and ownership of Midas Metal International LLC and Pacific international FZC, I once again state that it is already mentioned in my above mentioned statements.

Ques No. 3 Please refer to your statement dated 24.12.2019 recorded u/s 37 of FEMA, 1999 wherein you have submitted a copy of the agreement between Uralkali Trading (Gibraltar) Limited and your company M/s Midas Metals International LLC and also refer to answer to question no 2 above. Please explain the same.

Ans No.3. 1 have already clarified this in detail in my above mentioned statements. However, I once again submit that the copy of agreement submitted in my statement dated 24.12.2019 is just a draft agreement which was never signed and executed by any of the parties mentioned in the agreement. Further, there was no agreement handed over to me or my company by Rare Earth group. I once again confirm and state that no signed agreement was ever given to us. Upon being asked to explain about the ownership of Rare Earth Group, I once state that Rare Earth Group is beneficially owned, controlled and managed by A.D.Singh, Pankaj Jain and Sanjay Jain. The detail of entities in Rare Earth Group is already submitted in my above mentioned statements recorded u/s 37 of FEMA, 1999.

Ques No.4. As stated in your above mentioned statements you have received funds for Rare Earth group from Uralkali and Gulf Marine in your entities. Please explain the payments made out of these funds.

Ans No.4. The details regarding payments received and made have already been submitted along with the documents in my above mentioned statements. However, I once again state that payments were received from Uralkali and Gulf Marine and made to Amol Awasthi, Anupam Awasthi, Vivek Gahlot, A.D. Singh and Pankaj Jain/Sanjay Jain or entities under their control or ownership. Instructions for these payments were given by A.D. Singh, Sanjay Jain and Pankaj Jain. Since, these payments were although received in Midas Metal International LLC and Pacific international FZC but were belonging to A.D. Singh, Sanjay Jain and Pankaj Jain.

Ques No.5. Who used to give instructions regarding receiving of funds from Uralkali and Gulf Marine and Payments from these funds.

Ans No 5. As I have already stated in my above mentioned statements, I re-state that all three i.e. A.D. Singh, Pankaj Jain and Sanjay Jain visited my office in Dubai for decision making w.r.t. receiving and utilization of the funds received from Uralkali and Gulf Marine. On being further asked, I state that at this stage I am not able to recollect when they came for the first time. However, they were visiting my office regularly 3-4 times in a year since the incorporation of Rare Earth Group. As I was already having business relation with them in one of the meeting all three gave me this proposal that they will be receiving commission from Uralkali and Gulf Marine but they cannot receive directly. Further, they also said that commission received has to be paid to Amol Awasthi, Anupam Awasthi, Vivek Gahlot, A.D. Singh and Pankaj Jain/Sanjay Jain. Accordingly, it was decided that this commission will be received in my entities acting as paymaster for them and will be paid according to their directions. My role was to provide them entities for receiving payments as paymaster and making payments out of these funds as per their directions. Since Pankaj Jain who is brother of Sanjay Jain, is Dubai based used to pass on instructions on behalf of A.D. Singh and Sanjay Jain in case of any modification. Further, I want to state that Sh. Sushil Kumar Pachisia use to interact on behalf of Pankaj Jain with my office on regular basis. He is the key person managing the affairs of the Rare Earth Group. A.D. Singh and Sanjay Jain used to visit my office regularly to have an update of the affairs pertaining to transaction from Uralkali and Gulf Marine. On being further asked to explain the role and function of ‘Paymaster’, 1 state that the role of Paymaster is to receive and disburse payment on the instructions of the client against service charges.‖

c. Proceeds of crime from Rajeev Saxena to Rayon Trading

i. Mr Hossain submits that the money so received in the entities of Rajeev Saxena was thereafter transferred to the account of Rayon General Trading and other entities controlled by Pankaj Jain (co-accused/brother of the petitioner). In support of his contention, he invites the attention of the Court to the statement of Rajeev Saxena dated 10.06.2021 recorded under Section 50 of the PMLA, wherein Rajeev Saxena furnished the consolidated statement showing transactions with Pankaj Jain, Sanjay Jain and A.D. Singh. The relevant part of the statement reads as under:

“On being asked I am submitting consolidated statement of transaction of Pankaj Jain, Sanjay Jain and AD Singh running into pages 1 to 11 under my dated initials as prepared by my accountant Sh. Shahnawaz Khan.

Further I am submitting a statement consisting 71 entries (7 pages) with corresponding bank account statements of transactions of Pankaj Jain, Sanjay Jain and AD Singh under my dated initials.”

ii. Referring to the memorandum of account submitted by Rajeev Saxena, Mr Hossain submits that the said memorandum of account clearly shows the flow of proceeds of crime from Rajeev Saxena to Rayon Group and other entities. The relevant part of the memorandum of account (Excel sheets) is annexed at pages 63 and 64 of the compilation handed over by Mr Hossain.

iii. He further submits that the statement of Rajeev Saxena was corroborated by three (03) e-mails which have been sent by Ajeit Saxena to Shahnawaz Khan dated 18.05.2014, 11.06.2014 and 14.08.2013, wherein Ajeit Saxena can be seen following up on behalf of co-accused Pankaj Jain for due payments to Rayon General Trading.

d. Thereafter, the money/proceeds of crime were transferred by Rayon General Trading to M/s Alankit Global Resources DMCC, controlled by one Alok Kumar Aggarwal

i. Mr. Hossain submits that Alok Kumar Aggarwal in his statement dated 28.11.2022 under Section 50 of the PMLA has admitted that M/s Alankit Global Resources DMCC received money from Rayon General Trading.

ii. Referring to the statement of account submitted by Alok Kumar Aggarwal, Mr Hossain contends that a sum of AED 660,229.33 was credited on 31.05.2014 to the account M/s Alankit Global Resources DMCC from M/s Rayon General Trading LLC. Similarly, the account of Ms Alankit Global was credited with a sum of AED 733,699.70, AED 73,106.40, AED 513,565.12 and AED 219,869.70 on 07.06.2014, 17.06.2014, 19.06.2014 and 09.07.2014, respectively.

e. Proceeds of crime from Alankit Global to the petitioner –

i. To substantiate the last leg of the money trail in the indirect route, Mr Hossain invites the attention of the Court to the statement of one individual namely, Sunil Kumar Gupta, who was an employee of Alok & Company LLP (a CA firm belonging to Alok Kumar Agarwal). He submits that Sunil Kumar Gupta was responsible for maintaining the record of all cash as well as non-cash transactions for Alok Kumar Agarwal and Ankit Agarwal and the same was also recorded in his statement under Section 50 of the PMLA. He further submits that the cash transactions were recorded on a laptop in an Excel sheet as well as in a tally document and the said statements were checked and reconciled by Alok Kumar Agarwal and Ankit Agarwal. It was also explained by Sunil Kumar Gupta that his laptop had been seized by Income Tax Authorities on 18.10.2019.

ii. Mr Hossain submits that Sunil Kumar Gupta took a printout of the said Excel sheet and explained on the basis of diaries/excel sheets/ledgers maintained by him that payments amounting to Rs. 35,04,09,900/- have been made to the petitioner in the form of cash, RTGS transfers, FDRs etc. He further explained that M/s Atoll Vyapaar Private Limited and M/s Rasraj Marketing Private Limited are companies of the petitioner and he held 100% shares of both these companies and the directors of the said companies are dummy directors acting at the behest of the petitioner.

iii. Mr Hossain submits that Sunil Kumar Gupta was maintaining an account titled JPS on his laptop which belonged to the petitioner and on being shown the printout of this account, Sunil Kumar Gupta explained various credit and debit entries contained therein, as under:

a. for instance, on 22.05.2014, the account of the petitioner was credited with Rs. 1,17,32,000 in respect of the transfer of USD 2 lacs to one of many parties related to Alok Kumar Agarwal. For this credit entry, Alok Agarwal charged his commission @ 3% and paid cash in multiple tranches to various parties linked to Sanjay Jain. It was submitted that that this modus operandi is consistent with the statement of Sushil Kumar Pachisia before income tax authorities wherein he explained about generation of cash in Dubai which was sent to Sanjay Jain in India through non-banking channels. In this case, cash generated in Dubai was paid to any of the contacts of Alok Kumar Agarwal/Ankit Agarwal in Dubai in foreign currency (USD/AED) and Alok Kumar Agarwal/Ankit Agarwal would make payment in equivalent Indian currency in India to the petitioner/AD Singh. Alok Kumar Agarwal/Ankit Agarwal would charge a commission from Sanjay Jain/AD Singh for the said transactions. The cash would be paid in India from the cash amount received from the contacts to whom payment was made in foreign currency in Dubai.

b. Another instance which has been pointed out is that on 21.07.2014, the account of the petitioner was credited with Rs.1,20,40,000 in respect of the transfer of USD 2 lacs to one of many parties related to Alok Kumar Agarwal. For this credit entry, Alok Agarwal charged his commission @ 3% and bought shares worth Rs. 97,40,750 of M/s Euro Finmart Ltd. (owned by Alok Agarwal/Ankit Agarwal) in the names of friends and family members of Sanjay Jain. The remaining amount of Rs.19,38,050 was squared off by way of payment in cash to the petitioner on 06.08.2014.

33. According to Mr Hossain, the above trail is established from the fact that the petitioner admitted to having known Sunil Kumar Gupta from Alok & Co. Further, many other persons including Rakesh Kumar Jain, Mukesh Chandra Aggarwal and Mahesh Uphadhyaya etc. have testified to this fact.

34. Mr. Hossain, thus, submits that the funds which were transferred by entities controlled by Pankaj Jain from Dubai, using the vehicle provided by Alankit Group entities under the control of Alok Kumar Agarwal, to the petitioner/Sanjay Jain are also part of the proceeds of crime, which had been transferred by Rare Earth Group entities, and which have been projected as consultancy income by Alok Kumar Agarwal in the entities under his control.

UNBROKEN MONEY TRAIL (THROUGH RATUL PURI/DIRECT ROUTE)

35. Mr. Hossain submits that the flow of money from IFFCO/IPL to Rajeev Saxena through Uralkali is common to both routes, therefore, he made submissions on the subsequent legs of the direct route, which are as under:

a. Flow of Proceeds of Crime from Rajeev Saxena to Ratul Puri or his employee Rajeev Aggarwal

i. Mr. Hossain submits that once the proceeds of crime were in the hands of Rajeev Saxena, they were then transferred to the petitioner through an individual namely, Ratul Puri. Reliance in this regard is placed on the statement dated 11.06.2021 of Rajeev Saxena recorded under Section 50 of the PMLA to contend that on the said day, Rajeev Saxena was confronted with his statement dated 02/03.07.2019 tendered before the Income Tax Authorities and he admitted the same to be true and correct. In the said statement Rajeev Saxena had stated that payment to the tune of Rs. 43.89 Crores (USD 6.98 million) was made to the brother of the petitioner namely, Pankaj Jain. The attention of the Court was also drawn to Tables VII and VIII of the 1st Supplementary RC which shows the details of amount paid by Rajeev Saxena to Sanjay Jain in India through RatuI Puri against illicit commission received from Uralkali Trading Gibraltar against MoP (Muriate of Potassium) imported in India by IFFCO/IPL. He submits that Rajeev Saxena further stated that these payments have been made through Ratul Puri, son of Deepak Puri, owner of the Moser Baer group of companies. He also states that these payments have been made by Rajiv Agarwal, an employee of Ratul Puri mostly through one Punit Banthia who works for Sanjay Jain.

b. Proceeds of Crime from Ratul Puri/Rajiv Agarwal to Puneet Banthia (Employee of the Petitioner)

i. For this purpose, Mr Hossain referred to the statement of Punit Banthia recorded under Section 50 of the Act to contend that Punit Banthia had admitted having picked up cash from the Moser Baer office of Ratul Puri and having delivered the same to the office of Sanjay Jain.

ii. He contends that the statement of Puneet Banthia has been corroborated independently by the statement of Sh. Rajiv Agarwal recorded on 10.10.2022 under Section 50 of the PMLA wherein he admitted the presence of Punit Banthia’s phone number in his phone which was saved as „DUBAI PUNEET RAJIV’.

NON-ARREST OF CO-ACCUSED PERSONS CAN NOT BE A GROUND FOR BAIL

36. Mr Hossain submits that the petitioner’s contention that since he is not the main accused in the matter and other co-accused have either not been arrested or have already been enlarged on bail, he too is entitled to the concession of regular bail, is not tenable in law. For this purpose, reliance was placed on the judgment of the Supreme Court in Central Bureau of Investigation v. V. Vijay Sai Reddy1, the relevant paragraph of which reads as under:

“30. As pointed out by the learned Senior Counsel for CBI in para 25 of the impugned judgment [V. Vijay Sai Reddy v. CBI, Criminal Petition No. 4387 of 2012, decided on 13-6-2012 (AP)], the High Court did not agree with the observation of the Special Judge that the investigation has reached to a conclusion. In fact, the High Court has concluded that the above finding is incorrect. In para 26 also, the High Court appreciated and accepted the stand of CBI that it has been making investigation with regard to other distinct offences that are alleged in the FIR. Interestingly, the High Court has also not accepted the another reasoning of the Special Court for granting bail, namely, that the main accused, A-1 and other beneficiaries have not been arrested by the investigating agency. In other words, the High Court has rightly concluded that the circumstance of not arresting the other accused itself cannot be a ground to grant bail…..

(Emphasis Supplied)

PETITIONER IS NOT ENTITLED TO GRANT OF BAIL ON THE GROUND OF PARITY

37. Hossain submits that it is the case of the petitioner that out of the accused persons who have been arrested, the petitioner is the only one who is in custody. He submits that the petitioner is not entitled to grant of bail on the ground of parity, in as much as, the other accused were granted bail disregarding the twin conditions as contained under Section 45 of the PMLA, based upon the judgment of Nikesh Tarachand Shah v. UOI2, wherein Section 45(1) of the PMLA, insofar as it imposes twin conditions for release on bail, was declared to be unconstitutional, whereas the Supreme Court in Vijay Madanlal Chaudhary (supra) has now upheld the twin conditions under Section 45(1) of the PMLA.

38. He further submits that a co-accused namely, Amarendra Dhari Singh, has been granted bail on medical grounds vide order dated 05.08.2021 in BAIL APPLN. 2293/2021 and the same cannot be a ground to claim parity. To buttress his submission, reliance was placed on the judgment of the Chhattisgarh High Court in Sunny v. State of Chattisgarh3, the relevant paragraph of which reads as under:-

“6. The bail order of Mohan Lalwani and the documents filed along with these bail application would show that Mohan Lalwani being aged about 60 years and because of ailment and further he was shown to be physically disabled as per Annexure A-12, was enlarged on bail. Therefore, the present applicants cannot claim parity of order on basis of medical documents submitted. Neither the degree of ailment or age is at par with the other co-accused. ….‖

39. Similarly, the Gauhati High Court in Laishram Noren Singh vs. Lalsawmillen Kungte4, has held as under:-

“9. As the co-accused was granted bail on medical ground, his case cannot be compared with the case of the present petitioner‘s son i.e., accused as that case is not standing on the same footing. Mere granting of bail to the co-accused does not ipso facto create any right to the accused for bail. If an accused wants to get the benefit like the co-accused, then he has to make out a similar case. In the instant case, no such case is made out…”

40. In view of the above submissions, it is urged by Mr Hossain that as the petitioner does not satisfy the twin conditions under Section 45 of the PMLA, he cannot be enlarged on bail.

SUBMISSIONS OF LEARNED SENIOR COUNSEL IN REJOINDER

41. In rejoinder, Mr Dayan Krishnan learned Senior Counsel made submissions for the petitioner. He submits that considerable reliance has been placed by the respondent on the statements which have been recorded under Section 50 of the PMLA and it has been contended that this Court should not examine the correctness of the statements and must take them at face value. For this purpose, reliance has been placed by the respondent on the decision of this Court in Satyender Jain (supra). He, on the other hand, contends that the statements recorded under Section 50 of the PMLA cannot be seen at this stage at all and can only be seen at the stage of trial and this view has been endorsed by this Court in P. Khandelwal v. Directorate of Enforcement,5 Preeti Chandra v. Directorate of Enforcement 6 and Vijay Aggarwal v. Directorate of Enforcement.7 Thus, he submits that the decision of this Court in Satender Jain (supra) is an exception and ought not to be followed by this Court.

42. Without prejudice to the above, he submits that even if this Court were to examine the statements recorded under Section 50 of the PMLA, the same has to be done holistically having regard to all the attending circumstances. He submits that admissibility is not the same as the weight of evidence and no substantial weight can be attached to the statement of co-accused namely, Rajeev Saxena as it is trite that the statements of co-accused are not a substantive piece of evidence. He places reliance on the decision of Hon‟ble Supreme Court in Dipakbhai Patel v. State, (2019) 16 SCC 547. He further submits that the respondent cannot elevate the weight of the evidence merely because the same is recorded under Section 50 of the PMLA.

43. He submits that the statements of Rajeev Saxena are inherently unreliable, in as much, it is the own case of the respondent that Rajeev Saxena is guilty of “fudging” important documents and now the same is being sought to be relied upon by the respondent. The statements of Rajeev Saxena have not been corroborated by any independent material/documents.

44. Krishnan contends that the predicate offence being weak in nature is a relevant consideration, which shall enure to the benefit of the petitioner. Elaborating further, he submits that where the accused has demonstrated that the predicate offence is weak in nature or that no scheduled offence exists, it has to be taken that the accused has ipso facto shown that he shall be acquitted in the proceedings initiated under the PMLA. This approach according to the learned Senior Counsel has been adopted by this Court in Sanjay Pandey v. Directorate of Enforcement 8 and Chitra Ramkrishna v. Directorate of Enforcement.9

45. Mr Krishnan also repelled the contention on behalf of the respondent/ED that non-arrest of co-accused is not a ground for grant of bail. He submits that the judgment of the Supreme Court in Vijay Sai Reddy (supra) as relied upon by the respondent, lays down that non-arrest of co-accused „by itself‟ cannot be a ground for bail, but the same is a relevant factor which has to be taken into account at the time of considering a bail application. For this proposition, reliance was also placed on the judgments of this Court in Ram Pratap Verma @ Ram Pratap Verma v. The State through Directorate of Enforcement,10 C.P. Khandelwal (supra), Ashish Mittal v. SFIO11 and Rajesh Jain v. State.12

46. In respect of the two money trails, Mr. Krishnan submits that the respondent has relied upon Section 50 statements of an admittedly tainted witness (Rajeev Saxena); a witness whose statement is at the highest hearsay (Sunil Kumar Gupta) and a witness who repeatedly records contradictory statements (Puneet Banthia), whereas, there are several statements under Section 50 of the PMLA which completely exonerate the petitioner and would ultimately lead to the acquittal of the petitioner. According to Mr. Krishnan, the gist of the statements of such witnesses can be summarized as under:

|

1. |

Rakesh Kumar Jain |

|

Each of the individuals has denied participating in any cash transaction. |

| 2. | Sanjeev Jain |

|

|

| 3. | Rahul Mittal |

|

|

| 4. | Manish Jain |

|

|

| 5. | Rajiv Agarwal |

|

The witness has denied knowing the petitioner or delivering cash to him |

ANALYSIS

47. I have heard the learned Senior Counsel for the petitioner, as well as, the learned SPP for the respondent/ED and have given my thoughtful consideration to the material on record.

48. Before adverting to the rival contentions of the parties, it is imperative to bear in mind the threshold that the petitioner is required to meet under Section 45 of the PMLA before he is enlarged on bail. Reference may advantageously be had to the observations of the Supreme Court in Vijay Madanlal Choudhary (supra), the relevant paragraphs of which read as under:-

“388. There is no challenge to the provision on the ground of legislative competence. The question, therefore, is : whether such classification of offenders involved in the offence of money-laundering is reasonable? Considering the concern expressed by the international community regarding the money-laundering activities world over and the transnational impact thereof, coupled with the fact that the presumption that the Parliament understands and reacts to the needs of its own people as per the exigency and experience gained in the implementation of the law, the same must stand the test of fairness, reasonableness and having nexus with the purposes and objects sought to be achieved by the 2002 Act. Notably, there are several other legislations where such twin conditions have been provided for. Such twin conditions in the concerned provisions have been tested from time to time and have stood the challenge of the constitutional validity thereof. The successive decisions of this Court dealing with analogous provision have stated that the Court at the stage of considering the application for grant of bail, is expected to consider the question from the angle as to whether the accused was possessed of the requisite mens rea. The Court is not required to record a positive finding that the accused had not committed an offence under the Act. The Court ought to maintain a delicate balance between a judgment of acquittal and conviction and an order granting bail much before commencement of trial. The duty of the Court at this stage is not to weigh the evidence meticulously but to arrive at a finding on the basis of broad probabilities. Further, the Court is required to record a finding as to the possibility of the accused committing a crime which is an offence under the Act after grant of bail.“

xxxx xxxx xxxx xxxx

400. It is important to note that the twin conditions provided under Section 45 of the 2002 Act, though restrict the right of the accused to grant of bail, but it cannot be said that the conditions provided under Section 45 impose absolute restraint on the grant of bail. The discretion vests in the Court which is not arbitrary or irrational but judicial, guided by the principles of law as provided under Section 45 of the 2002 Act. While dealing with a similar provision prescribing twin conditions in MCOCA, this Court in Ranjitsing Brahmajeetsing Sharma , held as under:

“44. The wording of Section 21(4), in our opinion, does not lead to the conclusion that the court must arrive at a positive finding that the applicant for bail has not committed an offence under the Act. If such a construction is placed, the court intending to grant bail must arrive at a finding that the applicant has not committed such an offence. In such an event, it will be impossible for the prosecution to obtain a judgment of conviction of the applicant. Such cannot be the intention of the legislature. Section 21(4) of MCOCA, therefore, must be construed reasonably. It must be so construed that the court is able to maintain a delicate balance between a judgment of acquittal and conviction and an order granting bail much before commencement of trial. Similarly, the Court will be required to record a finding as to the possibility of his committing a crime after grant of bail. However, such an offence in futuro must be an offence under the Act and not any other offence. Since it is difficult to predict the future conduct of an accused, the court must necessarily consider this aspect of the matter having regard to the antecedents of the accused, his propensities and the nature and manner in which he is alleged to have committed the offence.

45. It is, furthermore, trite that for the purpose of considering an application for grant of bail, although detailed reasons are not necessary to be assigned, the order granting bail must demonstrate application of mind at least in serious cases as to why the applicant has been granted or denied the privilege of bail.

46. The duty of the court at this stage is not to weigh the evidence meticulously but to arrive at a finding on the basis of broad probabilities. However, while dealing with a special statute like MCOCA having regard to the provisions contained in sub-section (4) of Section 21 of the Act, the court may have to probe into the matter deeper so as to enable it to arrive at a finding that the materials collected against the accused during the investigation may not justify a judgment of conviction. The findings recorded by the court while granting or refusing bail undoubtedly would be tentative in nature, which may not have any bearing on the merit of the case and the trial court would, thus, be free to decide the case on the basis of evidence adduced at the trial, without in any manner being prejudiced thereby”

(emphasis supplied)

401. We are in agreement with the observation made by the Court in Ranjitsing Brahmajeet sing Sharma. The Court while dealing with the application for grant of bail need not delve deep into the merits of the case and only a view of the Court based on available material on record is required. The Court will not weigh the evidence to find the guilt of the accused which is, of course, the work of Trial Court. The Court is only required to place its view based on probability on the basis of reasonable material collected during investigation and the said view will not be taken into consideration by the Trial Court in recording its finding of the guilt or acquittal during trial which is based on the evidence adduced during the trial. As explained by this Court in Nimmagadda Prasad, the words used in Section 45 of the 2002 Act are “reasonable grounds for believing” which means the Court has to see only if there is a genuine case against the accused and the prosecution is not required to prove the charge beyond reasonable doubt.”

49. It thus, emerges that at the stage of considering a bail application under the PMLA, the Court has to bear in mind the following aspects:

i. Whether the accused possessed the requisite mens rea.

ii. The words used in Section 45 of the 2002 Act are “reasonable grounds for believing” which means the Court has to see only if there is a genuine case against the accused and the prosecution is not required to prove the charge beyond reasonable doubt.

iii. A positive finding that the accused had not committed an offence under the Act is not required to be recorded. A delicate balance between a judgment of acquittal/conviction and an order granting bail much before commencement of the trial is to be maintained.

iv. The evidence is not to be weighed meticulously but a finding is to be arrived at on the basis of broad probabilities with reference to the material collected during investigation. The weighing of evidence to find the guilt of the accused is the work of Trial Court.

v. A finding is also required to be recorded as to the possibility of the bail applicant committing a crime after grant of bail. This aspect has to be considered having regard to the antecedents of the accused, his propensities and the nature and manner in which he is alleged to have committed the offence.

50. The rival contentions of the parties, therefore, will have to be appreciated bearing in mind the aforementioned principles.

CBI’S JURISDICTION TO REGISTER THE RC

51. The first submission of the learned Senior Counsel for the petitioner is that since IFFCO and IPL are no longer government entities and it is not yet clear whether the co-accused namely, P.S. Gahlaut and U.S. Awasthi are “public servants”, hence, no offence under the provisions of the Prevention of Corruption Act is made out. It was further elaborated that even an inquiry by CBI in respect of IPL was closed stating that it has no jurisdiction over IPL since it is not a public authority. The said submission cannot be gone into at this stage as a co-ordinate Bench of this Court is stated to be seized of the specific issue with regard to the jurisdiction of the CBI to register the RC, in the writ petitions filed by the co-accused. However, suffice it to note that the predicate offence has also been registered under Sections 420 and 120B of the Indian Penal Code, apart from the provisions of the Prevention of Corruption Act. Both offences under Section 120-B and Section 420 IPC find mention in Schedule-A of the PMLA, therefore, such offences by themselves can be a predicate offence to trigger the offence of money laundering under the PMLA.

TO WHAT EXTENT RELIANCE COULD BE PLACED ON THE STATEMENT UNDER SECTION 50 OF THE PMLA AT THE STAGE OF CONSIDERING BAIL APPLICATION

52. As considerable reliance has been placed by the respondent on the statements of the witnesses recorded under Section 50 of the PMLA and both sides have argued on the extent to which the statements under Section 50 of the PMLA can be looked into at the stage of considering a bail application, therefore, apt would it be to examine the said question before proceeding further.

53. A Coordinate Bench of this Court in Chandra Prakash Khandelwal vs. Directorate of Enforcement: 2023 SCC OnLine Del 1094 held that the question of weightage to be given to the statements under Section 50 of PMLA will be tested at the end of the trial and not at the stage of bail. The relevant paragraph of the said judgment read as under:

“34. …… What weigh the statements under Section 50 of PMLA would carry at the end of trial cannot be tested at the stage of bail, more importantly when the intermediary companies were never made an accused in the present ECIR. The ultimate effect of their non-inclusion would be seen at the conclusion of trial…‖

(emphasis supplied)

54. In Preeti Chandra vs. Enforcement Directorate: 2023 SCC OnLine Del 3622 yet another Coordinate Bench of this Court held that the statements recorded under Section 50 can only be analyzed once the parties enter the witness box. However, the Court noted the inconsistency in the statements under Section 50 of the PMLA and observed that prima facie not much reliance could be placed on the said statements. The relevant extract of the judgment has been reproduced as under:

“68. The above statements can only be analysed once the parties enter the witness box.

xxxx xxxx xxxx xxxx

71. A Coordinate Bench of this Court in Chandra Prakash Khandelwal case [Chandra Prakash Khandelwal v. Enforcement Directorate, 2023 SCC OnLine Del 1094] has held that weightage given to Section 50 statement is to be analysed at the final stage and not at the stage of grant of bail. Hence, prima facie not much reliance can be placed on Section 50 statements in view of inconsistency in the statements of Indrajit Zaveri, Anuj Malik and Pranav Kumar.‖

(emphasis supplied)

55. In Manish Sisodia vs. Directorate of Enforcement: 2023 SCC OnLine Del 3770 this Court held that though the statements recorded under Section 50 of the PMLA are admissible in evidence but their evidentiary value has to be weighed at the time of trial. The Court did not look into the contradictions in the testimony of the witnesses observing that the Court cannot appreciate the evidence meticulously but at the same time observed that the Court cannot take the statements under Section 50 of the PMLA as gospel truth and only broad probabilities have to be seen. Accordingly, the Court did not make any comment on such contradictions observing that the trial is yet to take place. The relevant part of the decision reads thus:

“55. This Court is fully conscious of the fact that personal liberty is a sacrosanct right and pre-trial detention cannot be taken as a punitive measure. However, the court has to strike a balance between the interest of an individual and the interest of the society at large. This Court is also conscious of the fact that though the statements recorded under Section 50 of the PMLA are admissible in evidence but their evidentiary value has to be weighed at the time of trial…

xxxx xxxx xxxx xxxx

57. Learned Senior Counsels have invited the attention of this Court towards the contradictions in the testimony of the witnesses. However, this Court is fully conscious of the fact that at the stage of bail, the court cannot appreciate the evidence meticulously. This Court at this stage, would restrain itself to make any comment further on this as the trial is yet to take place. The option before this Court is either to go into the meticulous examinations of the witnesses as being argued by the learned defence counsels or to take into account the statements recorded under Section 50 of the PMLA by the ED. It is correct that the case of ED is based on the statements under Section 50 of the PMLA cannot be taken as gospel truth but at the same, the court has to take into account the probabilities and the legislative intent behind enacting Section 50 of the PMLA. The statements under Section 50 of the PMLA are not akin to Section 161CrPC. The bare perusal of Section 50 makes it clear that these are deemed to be judicial proceedings. There are consequences for making a false statement or not complying to the summons under Section 50 of the PMLA as provided under Section 63 of the PMLA.

58. This Court at this stage cannot go into the probative value of the witnesses nor can it meticulously examine those facts. The involvement of the third parties in the formulating and drafting of the policy certainly points at mens rea. The jurisdiction of bail is a discretionary jurisdiction. But this discretion has to be exercised on the settled principles in a judicial manner. The court has to bring in its judicial experience to arrive at a conclusion, which should be rational and logical. It is pertinent to mention that the accused and complainant/prosecution are entitled to know the reasons on the basis of which their bail application has been decided, but at the same time such reason should not be detailed in such a manner that it may prejudice the trial.”

(emphasis supplied)

56. The principle that emerges from Vijay Madanlal Choudhary (supra), as well as the above decisions as regards the statement recorded under Section 50 of the Act is that such statements are recorded in a proceeding which is deemed to be a judicial proceeding within the meaning of Section 193 and Section 228 of the Indian Penal Code and is admissible in evidence. The said statements are to be meticulously appreciated only by the Trial Court during the course of the trial and there cannot be a mini-trial at the stage of bail. However, when the statements recorded under Section 50 of PMLA are part of the material collected during investigation, such statements can certainly be looked into at the stage of considering bail application albeit for the limited purpose of ascertaining whether there are broad probabilities, or reasons to believe, that the bail applicant is not guilty. Meaning thereby, the statements under Section 50 of the PMLA have to be taken at their face value, but in case any such statement is patently self-contradictory or two separate statements of the same witness are inconsistent with each other on material aspects, then such contradictions and inconsistencies will be one of the factors that will enure to the benefit of the bail applicant whilst ascertaining the broad probabilities, though undoubtedly the probative value of the statement(s) of the witnesses and their credibility or reliability, will be analyzed by the trial court only at the stage of trial for arriving at a conclusive finding apropos the guilt of the applicant.

WHETHER THE CONFESSIONAL STATEMENT OF CO-ACCUSED UNDER SECTION 50 PMLA CAN BE USED AGAINST OTHER ACCUSED