Currently, businesses having turnover of more than one crore rupees are required to get their books of accounts audited by an accountant. In order to reduce the compliance burden on small retailers, traders, shopkeepers who comprise the MSME sector, the Finance Act 2020 has raised the limit of audit by five times the turnover threshold for audit from the existing Rs. 1 crore to Rs. 5 crores. It is also to be noted that this amendment is applicable for F.Y. 2019-20 i.e for the A.Y. 2020-21

Further, in order to boost less cash economy, it has been provided that the increased limit for mandatory tax audit shall apply only to those businesses which carry out less than 5% of their business transactions in cash. But in this connection, following points are to be noted

1. This threshold limit for the applicability of mandatory tax audits is applicable to business entity only and limit for a professional assessee shall continue to be at Rs. 50 lacs even if he receives entire consideration in non-cash mode.

2. It is not provided that who will certify the margin of transactions in cash mode of 5 It appears that the assessee is himself requiring declaring the percentage of receipt in cash mode and non-cash mode.

3. The provision to increase the turnover limit for a mandatory tax audit is amended to benefit the MSME sector.

4. The amendment is carried out only in section 44AB. No amendment is made in section 44AD and thus the turnover limit of Rs. 2 crores shall continue. Suppose an assessee is having a turnover of 180 lacs for the financial year 2020-21 and all the transactions of business are by non-cash modes. The net profit of the assessee is Rs.7 lacs which is less than 6% of turnover of the assessee. Now as per the provisions of sec 44AD, the assessee is required to maintain books of account and get them audited u/s 44AB of the Act.

5. The term ‘aggregate of all receipts and aggregate of all payments‘ is very wide and covers not only the receipts and payments on account of turnover or sales but all other business transactions. Capital introduction, receipt and repayment of a loan, etc., partners‘ drawings, payment of freights, etc. Even payment of taxes made in cash will come within the purview of cash transactions.

It can be better understood with the help of following table

| Turnover | Cash

Payments ≤ |

Cash Receipts

≤ 5% |

Net Profit | Audit u/s 44AB |

| 6 crores | Yes | Yes | 6% | Yes |

| 4.5 crores | Yes | Yes | 7% | No |

| 3 crores | Yes | No | 5% | Yes |

| 1.8 crores | Yes | Yes | 6% | Yes |

| 1.5 crores | Yes | Yes | 5% | Yes |

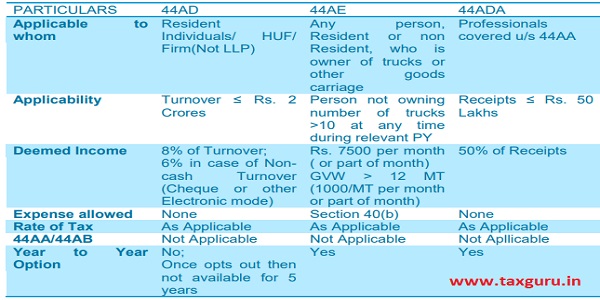

Comparative Study of Section 44AD, 44AE and 44AD

Author Bio

If turnover 1.80 crore and cash transactions below 5% and profit below 6% then according to me no Tax Audit.

A person falling under section 44AD is covered for Tax audit u/s 44AB only if he falls under Subsec (4), which means he has earlier adopted presumptive taxation for any earlier year and then he opts out of it. Only in such case he is liable for Tax audit under subsec (5). Sec 44AB(e) also refers to persons falling under subsec(4) of Sec 44AD.

If turnover between 1.80 to 1.90 crore and cash transaction below 5% and profit below 6% then no Tax audit required and department also confirmed this by not taking any actions. Because we are not going with presumptive scheme.