A Brief Discussion about the Residential Status of an individual and taxability of income according to their residential status in India

Taxability

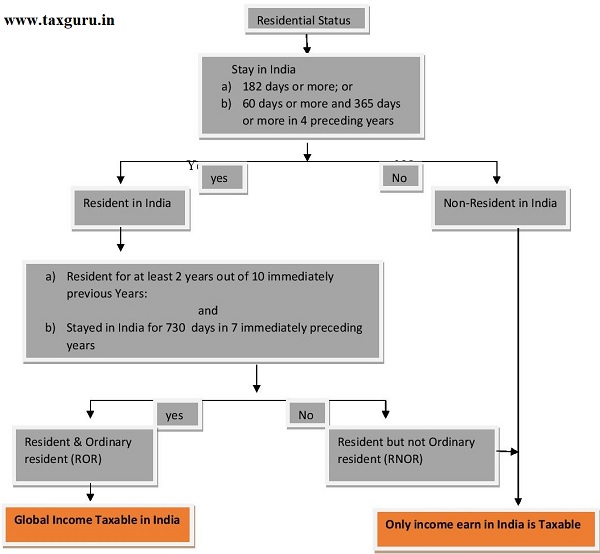

In India, income is taxable is based on their residential status, so it is very important to know about residential status of any individual to check the taxability of income. Let’s know:

| Status | Taxability |

| Resident & Ordinary resident (ROR) | Global Income will be Taxable in India |

| Resident but not ordinary resident | Income earn in India will be Taxable in India |

| Non Resident | Income earn in India will be Taxable in India |

So, to know whether global income is taxable or income earn in India is taxable, you know first about the residential status with the help of following steps:

Step I – Residential Status

In order to know the residential status of an individual we have to check that whether he/she is resident or not in the following manner:

1. He/she is stay in India for a period of 182 days or more in that financial year.

OR

2. He/she is stay in India for 60 days or more in that financial year and has been stay in India for 365 days or more in 4 previous years immediately that relevant financial year.

If any one of the above the condition is satisfied, then the said individual is resident for that financial year.

Provided that condition b) is not applied to check the residential status of an individual who is a citizen of India, leaves India in any financial year for the purpose of employment outside India. In other words, I can say that an individual, leaving India for employment then such individual deems to be resident only if he/she is stay in India for a period of 182 days. (however, from the financial year 2020-21 such period reduced to 120 days).

From the financial year 2020-21 there is another significant amendment that an individual who is a citizen of India & not liable to tax in any other country will be deemed to be resident in India. And such condition applies only if total income (other than foreign sources) exceeds Rs. 15 lakh and nil tax liability in other countries or territories by reason of his domicile or residence or any other criteria of similar nature.

Step – II – Ordinary Residence (ROR) or Not Ordinary Residence (RNOR)

After satisfying with the first step we will further check that he/she is an Ordinary residence or Not Ordinary residence in the following manner:

He/she will be ROR in case of satisfying both the following conditions:

a) Has been a resident of India in at least 2 out of 10 years immediately previous year; and

b) Has stayed in India for at least 730 days in 7 immediately preceding years

Hence if any individual does not satisfy either one or both of the above condition that he/she is a resident but not ordinary resident (RNOR) in India.

Step – III – Non-Residence (NR)

If an Individual does not satisfy the conditions as mentioned in step-I, then he/she is a non-residence in India

You can also understand the residential status of an individual by a graph:

Author Bio