Application for Unbarring of GST Returns – Legal Position, GSTN Advisory and Portal-Based Relief Explained

Introduction

Timely filing of GST returns is a fundamental compliance requirement under the CGST Act 2017. Prolonged non-filing of returns not only attracts late fees and interest but also results in system-driven barring of return filing on the GST portal. In order to address genuine hardship cases and legacy non-compliance, the GST portal provides a facility for Application for Unbarring of Returns, allowing taxpayers to seek administrative approval for filing blocked returns.

This article explains the statutory framework, the GSTN advisory on the three-year limitation, and the practical impact of the unbarring mechanism, read together.

Statutory Framework – Section 39 and Three-Year Limitation

The proviso to Section 39 of the CGST Act, inserted by the Finance Act, 2023, prescribes that a registered person shall not be allowed to furnish GST returns after the expiry of three years from the due date of such return. Similar time restrictions apply to returns under Sections 37, 44 and 52. The said amendment was operationalised vide Notification No. 28/2023 – Central Tax dated 31 July 2023, empowering the GST portal to enforce time-based barring of returns.

GSTN Advisory on Barring of Returns after Three Years

In furtherance of the above statutory amendment, GSTN issued an advisory dated 29 October 2025 titled “Advisory to file pending returns before expiry of three years”, clarifying the manner of implementation of the three-year restriction on the GST portal.

As per the advisory, GST returns such as GSTR-1, GSTR-1A, GSTR-3B, GSTR-4, GSTR-5, GSTR-6, GSTR-7, GSTR-8, GSTR-9 and GSTR-9C, falling under Sections 37, 39, 44 and 52, shall stand barred on the GST portal after completion of three years from their respective due dates. The advisory further specifies the returns that would be barred from 1 December 2025.

Accordingly, as a general rule, returns beyond the prescribed three-year period are not permitted to be filed online.

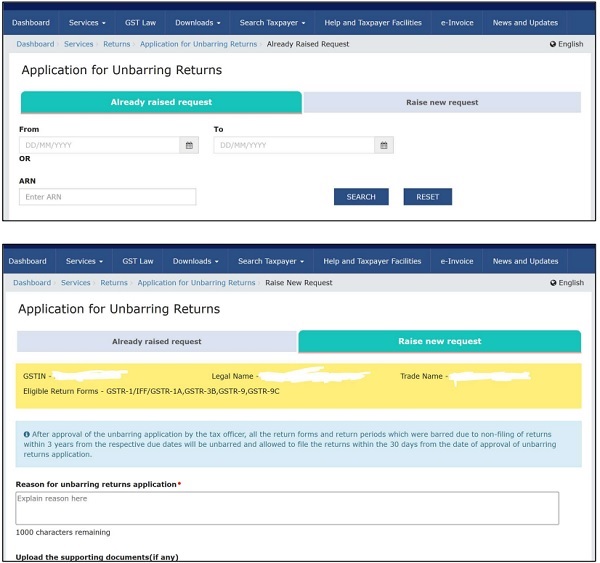

Application for Unbarring Returns – Portal Mechanism

Notwithstanding the above statutory and system-based restrictions, the GST portal provides a separate facility titled “Application for Unbarring Returns”, enabling taxpayers to seek approval from the jurisdictional proper officer for unblocking of return filing access.

Navigation Path

Login → Services → Returns → Application for Unbarring Returns → Raise New Request

The taxpayer is required to specify the blocked return periods and provide reasons for non-filing. Upon submission, an ARN is generated, and the application is routed to the proper officer.

Portal Position – Returns Beyond Three Years

The system-generated disclosure on the GST portal clearly states that upon approval of the unbarring application, all return forms and periods which were barred due to non-filing—including those crossing the three-year threshold—shall be unbarred and enabled for filing.

Further, such returns are required to be filed within 30 days from the date of approval of the unbarring application, failing which the returns may again stand barred.

This portal functionality indicates that the three-year restriction, though statutorily prescribed and reiterated through the GSTN advisory, is subject to an administrative override, exercisable only with the approval of the proper officer.

Harmonious Reading of Law, Advisory and Portal Functionality

The GSTN advisory establishes the general rule of barring returns after three years, while the unbarring module provides a controlled, approval-based exception. The two must therefore be read harmoniously:

- The statutory bar and advisory govern the default position

- The unbarring facility operates as a discretionary administrative relief

- No automatic right accrues to the taxpayer

- Officer approval and post-approval compliance are mandatory

Thus, filing of returns beyond three years is not a matter of entitlement but a conditional compliance opportunity.

Role of the Proper Officer

The proper officer may examine:

- Duration and reasons for non-filing

- Revenue impact and tax liability

- Past compliance behaviour

- Pendency of proceedings, if any

Only upon satisfaction will the officer approve the unbarring request electronically.

Post-Approval Compliance – Critical Time Limit

Once unbarring is approved:

- Barred returns are enabled on the portal

- Returns must be filed within 30 days from approval

- Delay beyond this window may result in re-barring

Taxpayers must therefore be fully prepared with reconciliations, tax payments, and data before applying.

Practical Guidance for Taxpayers and Professionals

1. GSTN advisory remains binding as the general rule

2. Unbarring is an exception, not a relaxation of law

3. Returns beyond three years can be filed only after approval

4. The opportunity is time-bound and case-specific

5. Applications should be reasoned, factual and supported by readiness to comply

Conclusion

The Application for Unbarring of GST Returns represents a significant compliance facilitation tool under GST. While the statutory framework and GSTN advisory impose a three-year filing restriction, the portal-enabled unbarring mechanism allows taxpayers to regularise legacy non-compliance through an approval-based process. Taxpayers and professionals must approach this mechanism with diligence, preparation and a clear understanding that it operates as a conditional administrative relief within the GST framework.

******

Author’s Note: The views expressed are based on the current GST portal functionality and system disclosures. Field-level implementation may vary depending on jurisdictional officer discretion. For any query related to above article, or if you face any issue in Income Tax, GST, SEZ, STPI, MCA compliances etc., especially in cases involving legal proceedings, notices, litigation, or demand matters. Please feel free to contact us at the details mentioned below:

Contact: +91-7842796315; Email: cakrupanand@gmail.com

Author Bio