Case Law Details

In re PES Engineers Pvt Ltd (GST AAR Telangana)

In a recent ruling by AAR Telangana in the case of M/s. PES Engineers Pvt. Ltd. [TSAAR Order No. 09/2023 dated April 13, 2023], held that when parties enter into separate agreements for goods and works contract services, they are treated as distinct supplies and not composite supply. Accordingly, if any advance is received for supply of goods, that will be taxed as per Section 12(2)(a) of the Central Goods and Services Tax Act, 2017

Facts:

M/s. PES Engineers Pvt. Ltd. (“the Applicant”) is engaged in the business of construction and maintenance of various types of power projects.

The Applicant is awarded with a contract by M/s. Singarenni Collieries Company Ltd. (“SCCL”) vide bid notifications dated December 28, 2021.

Accordingly, the Applicant entered into 2 agreements with SCCL. The first agreement is related to supply of goods i.e the Flue Gas Desulphurization (FGD) system, Limestone and gypsum handling system, items related to chimney and the spares related to above parts etc. The second agreement is related to services of transportation, insurance, unloading at site, storage, erection, civil works, safety aspect to safety rules, testing, commission and conducting guarantee tests of the goods supplied under the first agreement.

The Applicant stated that it has received advance of 5% and 7.5% which is specifically for supply of goods under the first agreement and since the activities of both agreements are properly demarcated thus, each agreement has to be independently assessed for the purpose of GST and accordingly, he is liable to pay GST on goods at the time of supply which is, the date of issue of invoice and not on the date on which the Applicant received advance payments for goods under the first agreement.

Issue:

Whether the Applicant is exempt from payment of tax on advances received under the first agreement, as per Notification No. 66/2017-Central Tax dated November 15, 2017?

Held:

The AAR, Telangana in TSAAR Order No. 09/2023 held as under:

- Observed that, the scope of supply undertaken under the individual agreements are entirely independent and specific to that agreement and are not associated with other agreement.

- Further observed that, contract agreement document had put a condition that there are two separate agreements that need to be entered into i.e. one for sale of goods and the other for supply of service. Therefore, both the agreements are separate and cannot be clubbed together.

- Noted that, the supply undertaken under the first agreement terminates at the moment when the Applicant raises tax invoice for supply of goods and endorse the documents.

- Further noted that, since the transfer of property in the goods supplied under first agreement is not taking place during the execution of the works contract under second agreement, the value of goods cannot be included in the works contract services.

- Stated that, the mere fact that different tasks, i.e. two agreements for which separate invoices were issued by the Applicant to SCCL, have been assigned to the Applicant through a single contract would not make it a ‘composite supply’ in terms of Section 2(30) of the CGST Act.

- Ruled that, the applicant is eligible for the benefit of Notification No. 66/2017-Central Tax dated November 15, 2017 and accordingly, the tax liability on sale of goods will arise as per Section 12(2)(a) of the CGST Act.

Relevant Provisions:

Section 12(2) of the CGST Act

“Time of supply of goods

The time of supply of goods shall be the earlier of the following dates, namely:-

(a) the date of issue of invoice by the supplier or the last date on which he is required, under section 31, to issue the invoice with respect to the supply;”

FULL TEXT OF THE ORDER OF AUTHORITY FOR ADVANCE RULING, TELANGANA

[ORDER UNDER SECTION 98(4) OF THE CENTRAL GOODS AND SERVICES TAX ACT, 2017 AND UNDER SECTION 98(4) OF THE TELANGANA GOODS AND SERVICES TAX ACT, 2017.]

******

1. M/s. PES Engineers Private Limited Hyderabad, 1st floor, Pancom chambers, 6-3-1090/1/A, Somajiguda, Hyderabad-500082, Telangana (36AABCP4220B1Z3) has filed an application in FORM GST ARA-01 under Section 97(1) of TGST Act, 2017 read with Rule 104 of CGST/TGST Rules.

2. At the outset, it is made clear that the provisions of both the CGST Act and the TGST Act are the same except for certain provisions. Therefore, unless a mention is specifically made to any dissimilar provisions, a reference to the CGST Act would also mean a reference to the same provision under the TGST Act. Further, for the purposes of this Advance Ruling, the expression ‘GST Act’ would be a common reference to both CGST Act and TGST Act.

3. It is observed that the queries raised by the applicant fall within the ambit of Section 97 of the GST ACT as it involves determination of the liability to pay tax on goods or services and classification of goods or services. The Applicant enclosed copies of challans as proof of payment of Rs. 5,000/-under SGST and Rs. 5,000/- under CGST towards the fee for Advance Ruling. The Applicant has declared that the questions raised in the application have neither been decided nor are pending before any authority under any provisions of the CGST/TGST Act’2017. The application is, therefore, admitted after examining it and the records called for and after hearing the applicant as per section 98(2) of TGST Act’2017.

4. BRIEF FACTS OF THE CASE:

4.1 The applicant M/s. PES Engineers Private Limited Hyderabad are engaged in the construction of various types of Power Projects. They have entered into agreements with Singarenni Collieries Company Limited (SCCL) for “Design, Manufacture, Test, Deliver, Install, Complete & Commission and to conduct guarantee test of certain facilities viz., Fuel Gas de-sulphurisation (FGD) system package for Singareni TPS, stage-1 (2X600MW)” at their Thermal Power Project.

4.2 The applicant entered into two separate contracts for executing this work. The Notification of Award of First Contract was issued by M/s. SCCL vide Ref.No.CRP/MP/01/E0119O0413/FGD/5576, dated: 28/12/2021 and the Notification of Award of Second Contract was issued by M/s. SCCL vide Ref.No. CRP/MP/01/E0119O0413/FGD/5577, dated: 28/12/2021. The scope of First Contract is sale of goods ex-manufacture / ex-works. According to the applicant, it is a contract for pure sale of goods.

4.3 The scope of work under the Second Contract is “Inland Transportation of the main equipment, inland transit insurance, unloading at site, storage, erection, civil works, Safety aspects / Compliance to Safety Rules and other services insurance covers other than inland transit insurance, testing, commission and conducting guarantee tests”. According to the applicant, the supply under Second Contract is Works Contract Service as defined under Sec.2(119) falling under SAC 9954.

The scope of both the contracts and consideration is given by the applicant as follows:

First Contract:

|

Scope of work |

Amount in Rs. |

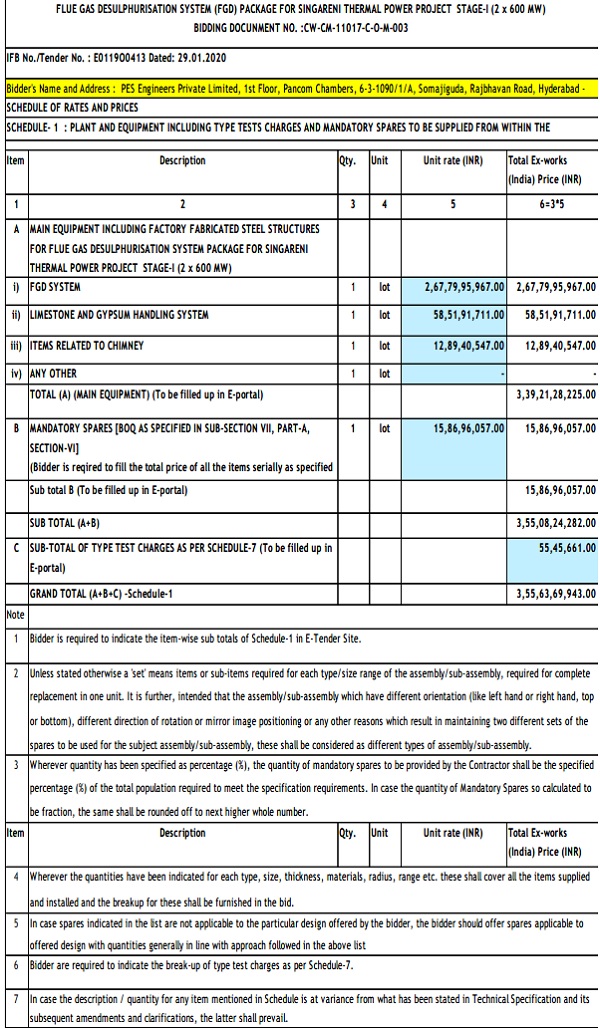

| 1. Ex-Manufacturing Works / Place of Dispatch Price (both in India) for Main Equipment. | 339,21,28,225/- |

| 2. Ex-Manufacturing Works / Place of Dispatch Price (both in India) for Mandatory spares. | 15,86,96,057/- |

| 3. Type Test Charges | 55,45,661/- |

| 355,63,69,943/- |

Second Contract:

|

Scope of work |

Amount in Rs. |

| 1. Inland transportation and inland transit insurance charges for Main Equipment |

3,64,50,501/- |

| 2. Inland transportation and inland transit insurance charges for Mandatory Spares |

19,83,701/- |

| 3. Unloading and handling at site, storage, erection, civil works, SafetyAspects / Compliance to Safety Rules and other services insurance covers other than inland transit insurance, testing, commission and conducting guarantee tests |

230,77,38,228/- |

| 234,61,72,430/- |

4.4 The applicant further brought to the notice of AAR the terms of the payment. As per the payment terms, in respect of Plant and Equipment (Excluding Mandatory spares and type test charges) supplied from within the Employer’s country the following payment schedule is mentioned.

|

Initial Advance on goods |

5% |

| Interim Advance on goods | 7.5% |

| Upon dispatch | 52.5% |

| Upon receipt | 20% |

| On Achievement of intermediate milestone | 5% |

| On successful completion | 10% |

| Total: | 100% |

The advance of 5% plus 7.5% is computed on Rs.339,21,28,225/- is recovered progressively from tax invoices issued for supply of goods under the contract.

4.5 The applicant avers that as can be seen from both the contracts there is a clear cut demarcation of activities of supply of goods and supply of services. Hence, according to the applicant each contract has to be independently assessed for the purpose of GST. According to the applicant since, the Advance of 5% and 7.5% is specifically given against supply of goods under the First Contract, the Applicant is entitled for the benefit of Notification No.66/2017 Central Tax, dated: 15th November, 2017. Hence, this application.

5. The applicant has submitted Statement of relevant facts having a bearing on the question(s) raised as detailed below:

1. The Applicant, M/s PES Engineers Pvt.Ltd., having principal place of business at 1st Floor, Pancom Chambers, 6-3-1090/1/A, Somajiguda, Rajbhavan Road, Hyderabad – 500082, Telangana are engaged in construction and maintenance of various types of Power Projects. They are registered with the GST Department vide GSTN 36AABCP4220B1Z3.M/s Singareni Collieries Company Limited, engaged in mining of coal and generation of thermal power, floated Tender for “Design, manufacture, test, deliver, instal, complete and commission and conduct guarantee test of certain Facilities, viz, Flue Gas Desulphurisation (FGD) System Package for Singareni TPS, Stage-I (2X600 MW)” at their thermal power project. The Applicant participated in the Tender and has been awarded the work. Consequently, the Applicant entered into agreements with SCCL to “Design, manufacture, test, deliver, instal, complete and commission and conduct guarantee test of certain Facilities, viz, Flue Gas Desulphurisation (FGD) System Package for Singareni TPS, Stage-I (2X600 MW)” under Bidding Document No.CW-CM-11017-C-O-M-003. The details of the contracts are as under:

First Contract:

|

Scope of work |

Amount in Rs. |

| 1.Ex-manufacturing Works /Place of Dispatch Price (both in India) for Main Equipment | 339,21,28,225/- |

| 2.Ex-manufacturing Works /Place of Dispatch Price (both in India) for Mandatory spares | 15,86,96,057/- |

| 3. Type Test Charges | 55,45,661/- |

| Total | 355,63,69,943/- |

Second Contract:

|

Scope of work |

Amount in Rs. |

| 1.Inland transportation and inland transit insurance charges for Main Equipment | 3,64,50,501/- |

| 2.Inland transportation and inland transit insurance charges for Mandatory Spares | 19,83,701/- |

| 3. Unloading and handling at site, storage, erection, civil works, Safety Aspects/Compliance to Safety Rules and other services insurance covers other than inland transit insurance, testing, commissioning and conducting guarantee tests | 230,77,38,228/- |

| Total | 234,61,72,430/- |

WET LIMESTONE BASED FLUE GAS DESULPHURISATION (FGD) PROCESS DESCRIPTION:

The subject FGD system shall be based on Wet Limestone Forced Oxidation process. Each unit shall be provided with an independent absorber.

Gas from terminal point on ID fan discharge duct shall be taken directly to the absorber through Booster Fans. In the absorber, SO2 in flue gas shall be removed by a spray of recirculating slurry, pumped by slurry recirculation pumps. Alternatively, the gas shall be bubbled through the absorber slurry to remove the SO2 from flue gas. Only proven system supplied earlier by the FGD vendor shall be supplied by the contractor.

Compressed oxidation air shall be blown through the slurry in the oxidation tank, to oxidize the Calcium sulfite to gypsum. The oxidation system may be either grid sparge type or lance jet type or Jet Air Sprayer or any other proven system as per the practice of the FGD vendor.

Clean gas from the absorber shall be taken to the Wet Chimney, to be provided by the Contractor, through three stage mist eliminators. Provision shall be made for facilitating operation of unit with FGD bypass through existing stack. All modifications required including providing bypass damper is included in the scope of the Contractor.

Limestone to the absorbers of the units shall be supplied by a wet limestone grinding system, common for both the units. Limestone shall be fed to the Limestone day silos which in turn will feed the Limestone to wet ball mill through a gravimetric feeder. The classified limestone slurry from the mills shall be stored in two (2 no)

limestone slurry storage tanks to be provided by the contractor, from where the slurry shall be pumped to the individual absorbers by dedicated limestone slurry pumps.

The gypsum from the absorber(s) shall be pumped by dedicated gypsum bleed pumps to a common Gypsum Dewatering system for both the units consisting of two streams (2×100%) of primary and secondary hydrocyclone and vacuum belt filters for gypsum dewatering. The water removed from the absorber shall be recycled to the absorbers. The waste water from the system shall be collected and neutralized using lime and neutralized effluent shall be pumped at required pressure to waste water terminal point as indicated in Sub-section IV, Part A of the Technical Specification. Contractor shall provide complete automated waste water neutralization system along with automated lime feeding and dosing system to ensure required pH of waste water is ensured before being discharged at the terminal point. Washed and dewatered gypsum from the dewatering system shall be fed to a belt conveyor. The contractor shall discharge the gypsum cake above the Gypsum handling belt conveyor to be provided by the Contractor.

A common auxiliary absorbent tank shall be provided for storage of absorber slurry of one absorber (maximum capacity) for both the units along with slurry pumps for pumping the slurry back to any of the absorber.

PRIMARY COMPONENTS OF THE WET LIMESTONE FGD PLANT ARE DESCRIBED BELOW:

i. Ducting system : The ducts, made of carbon steel, are used for transferring flue gas from existing chimney to the absorber. Further, to maintain the flue gas pressure, booster fans are installed to develop the required pressure for transferring flue gas.

ii. Absorber : Absorber is the main equipment where the Sulphur is removed from flue gas. It is a 46.0 m height shell of 18.0 m diameter, made up of carbon steel, approximate weight of 480 tons. The Limestone slurry is sprayed inside the absorber through headers and nozzles which comes in contact with the flue gas passing through it and removes the Sulphur in it.

iii. Wet ball mills system : The wet ball mills is used for grinding/crushing of limestone up to particle size of 44 micron and for preparation of limestone slurry. The ball mill shall be driven by a motor through a peripheral gear. An auxiliary motor shall also be provided for inching of mills after trip and during maintenance.

iv. Limestone Slurry handling system: The limestone slurry of required fineness available from the wet ball system shall be stored in limestone slurry tanks. From limestone slurry tank, the limestone slurry shall be pumped to individual absorber by means of dedicated limestone slurry transfer pumps.

v. Gypsum handling system : In the de-sulphurisation process, a byproduct Gypsum is generated in liquid form. The liquid form of Gypsum generated in the Absorber is pumped into the gypsum handling system to transform it into crystal form. The main equipment includes for Gypsum Handling System is gypsum hydro cyclones, vacuum belt filters, vacuum pumps, filter water system etc.,

vi. Wastewater treatment and disposal System : The FGD system produce a small amount of wastewater. The main task of the wastewater treatment plant is to adjust the pH and to remove the heavy metals and suspended solids. The waste water collected in the waste water tank of FGD system shall be provided with adequate treatment with lime as reagent and then disposed to existing ash handling system.

vii. Chimney : Reinforced Cement Concrete (RCC) Chimney will be of cylindrical in shape with 18.0 m diameter and 150 m height. Treated flue gas from the absorber will flow through chimney and finally released into the atmosphere.

viii. Electrical & instrumentation : Electricity is required to run slurry pumps, limestone ball mills, conveyor belts, wastewater treatment and recycling pumps, lighting of the plant etc., SCADA system will be provided to run FGD plant with automation.

1. The Price Break up for the supply of goods under First Contract is as under:

The price break up for the Second contract involving supply of services is as under:

The above prices are without GST and applicable GST is payable extra by the employer as under:

As per the payment terms, in respect of Plant and Equipment (Excluding Mandatory spares and type test charges)supplied from within the Employer’s country the following payment schedule is mentioned:

| Initial Advance on goods | 5% |

| Interim Advance on goods | 7.5% |

| Upon dispatch | 52.5% |

| Upon receipt | 20% |

| On Achievement of intermediate milestones | 5% |

| On successful completion | 10% |

| Total | 100% |

The advance of 5% plus 7.5% is computed on Rs.339,21,28,225/- is recovered progressively from tax invoices issued for supply of goods under the contract.

2. The detailed terms of payment for First Contract are as follows:

TERMS OF PAYMENT

A. Schedule No.1: Plant and Equipment (excluding Mandatory Spares and Type Test Charges) quoted on Ex-works (India) basis:

In respect of Plant and Equipment (excluding Mandatory Spares and Type Test charges) supplied from within the Employer’s country the following payment shall be made:

A1. For Ex-works Price Component of Plant and Equipment (excluding Mandatory Spares and Type Test Charges):

(I)(a)Five percent (5%) of the total Ex-works price component as Initial Advance Payment on :

(i) Acceptance of Notification of Award(s) and Signing of the Contract Agreement(s).

(ii) Submission of an unconditional Bank Guarantee covering the advance amount, which shall be initially kept valid upto (ninety) 90days beyond the schedule date for successful Completion of the Facilities under the Package. However, in case of delay in completion of facilities, the validity of this Bank Guarantee shall be extended by the period of such delay. Proforma of Bank Guarantee is enclosed in Section- VII – Bank Guarantee Form for Advance Payment.

(iii) Submission by the Main Contractor of an unconditional Bank Guarantee(s) towards Performance Security(s) in respect of all Contracts all initially valid upto ninety (90) days after the end of Defects Liability Period of all equipment covered under Contract. However, in case of delay in Defect Liability Period, the validity of this Bank Guarantee shall be extended by the period of such delay. The proforma of Bank Guarantee is enclosed in Section- VII-Form of Performance Security.

(iv) In case Deed of Joint Undertaking by the Contractor alongwith his Associate/Collaborator forms part of the Contract then submission of an unconditional Bank guarantee from such Associate/Collaborator towards faithful performance of the Deed of Joint Undertaking for an amount specified in the deed and initially valid upto ninety (90) days after the end of Defect Liability Period of all equipment covered under the Contract. However, in case of delay in Defect Liability Period, the validity of this Bank Guarantee shall be extended by the period of such delay. The proforma of Bank Guarantee(s) shall be as enclosed in Section-VII.

(iv) Submission of a detailed PERT Network based on the work schedule stipulated in Appendix-4 to Form of the Contract Agreement and its approval by the Employer.

(v) Finalization of Master Drawing List (MDL).

(I)(b) Seven and Half percent (7.5%) of the total Ex-works price component as Interim Advance Payment on :

(i) Fulfilment of conditions mentioned at A1(I)(a)(i) to (vi) above.

(ii) Submission of an unconditional Bank Guarantee covering the advance amount,which shall be initially kept valid upto (ninety) 90 days beyond the schedule date for successful Completion of the Facilities under the Package. However, in case of delay in completion of facilities, the validity of this Bank Guarantee shall be extended by the period of such delay. Proforma of Bank Guarantee is enclosed in Section-VII – Bank Guarantee Form for Advance Payment.

(iii) Submission of copy of purchase order(s) placed by Contractor and duly accepted by Sub-Contractor(s) for Booster Fan, Absorber Clad plate/Ceramic Liner, wet ball mill, Chimney Liner material as applicable for each project.

Note : (i) The interim advance amount shall be divided equally among various subsystems mentioned at (I) (b) (iii) above and the amount shall be released progressively on completion of ordering of each system.

(ii)Some of the sub systems as mentioned at (I) (b) (iii) above may not be applicable for some of the projects. Accordingly the interim advance amount may be divided equally among the remaining subsystems.

(II) Fifty Two and Half Percent (52.5%) of Ex-Works Price component of the Contract price for each identified equipment upon despatch of equipment on pro-rata basis on production of invoices and satisfactory evidence of shipment which shall be original Good Receipt/Rail Receipt including Material Despatch Clearance Certificate (MDCC)issued by the Employer.

(III) Twenty Percent (20%) of Ex-works price component of the Contract Price for each identified equipment on receipt of equipment at site on pro-rata basis and physical verification and certification by the Project Manager of the equipment received and stored at site.

(IV) Five Percent (5%) of Ex-works Price Component of the Contract Price shall be released on achievement of intermediate milestone events as mentioned hereunder:

1. One Percent (1%) of Ex-works price component of the Contract Price shall be released on Completion of erection of Absorber system.

2. One Percent (1%) of Ex-works price component of the Contract Price shall be released on Completion of erection of Fan and Ducting System.

3. One Percent (1%) of Ex-works price component of the Contract Price shall be released on Completion of erection of Limestone Handling and Crushing System.

4. One Percent (1%) of Ex-works price component of the Contract Price shall be released on Completion of erection of Gypsum Handling system.

5. One Percent (1%) of Ex-works price component of the Contract Price shall be released on Completion of Chimney.

(V) Ten Percent (10%) of Ex-works Price Component of the contract price on Successful Completion of Initial Operation including all associated auxiliaries and ancillary works of entire Flue Gas Desulphurization System and issue of Completion Certificate by the Project Manager and successful completion of Guarantee Tests of entire Flue Gas Desulphurization System and issuance of Operational Acceptance Certificate by the Project Manager. In case of more than one units in a Project, the payment shall be made on pro-rata basis for each unit.

However, in case the contractor has successfully completed Initial Operation including all associated auxiliaries and ancillary works of entire Flue Gas Desulphurization system and successfully completed guarantee test for “Guarantees Under Category-I (as per technical specification)” and is not able to conduct Guarantee test for “Guarantees Under Category-II (as per technical specification)”, for reasons attributable to the Employer or due to the requirements of the technical specifications, 50% of the payment towards initial operation and guarantee test shall be released to the contractor. Further the balance 50% of the payment towards initial operation and guarantee test shall be released on pro-rata basis after successful completion of guarantee test for “Guarantees Under Category-II.” However, in such case the payments shall not exceed 90% of the amount due on “Completion of Initial Operation along with Guarantee Test”.

Note: (i) If any of the intermediate milestone activities as mentioned

at Sl. No.

(IV) above are not applicable for any project, the corresponding intermediate milestone payment shall be clubbed with last intermediate milestone activity to be achieved.

(ii) The basis for the pro-rata payment at (II) and (III) above shall be the Billing Break-up (BBU) to be finalised subsequently after award of contract.

(iii) In case Installation Price (excluding Civil/Structural works price) is less than 15% of the Ex-works Price of Main Equipment, the amount by which it is lower shall be retained proportionately from the Ex-works component of Contract price while releasing payments due on receipt of equipment, and no interest shall be payable on the retained amount. The aforesaid retained amount shall be paid on pro-rata basis upon completion of installation of the respective equipment and its certification by the Project Manager.

(iv) In case the Civil Works Price (including Site Fabricated Structural works price) is less than 49% of the Ex-works Price of Main Equipment, the amount by which it is lower shall be retained proportionately from the Ex-Works component of Contract price while releasing payments due on dispatch of equipment, and no interest shall be payable on the retained amount. The aforesaid retained amount shall be paid on pro-rata basis upon completion of Civil Works including Structural works (if any) corresponding to the respective equipment and its certification by the Project Manager.

(v) Wherever intermediate milestone events at (IV) above are applicable unit wise, the payment shall be made on pro-rata basis for each unit.

3. The terms for payment of Mandatory Spares and Recommended Spares are mentioned in para B of the Appendix. Payment for Local Transportation is mentioned at para No C of the Appendix and the terms of payment for Installation Services are mentioned in para No D of the Appendix. The terms of payment for Civil Works are mentioned in Para No E. Terms of payment for Structural Work portion, including the cost of materials, Fabrication & Erection are mentioned in Para F. Amount linked to Safety Aspects and compliance to Safety Rules are mentioned in Para G. For the purpose of the application, terms of payment in Para A are only relevant.

6 QUESTION RAISED:

1) Whether the applicant is required to pay GST on “initial advance” of 5% and “interim” advance of 7.5% on Ex works value of goods supplied under “First Contract Agreement” dated 9th February, 2022 with M/s. Singareni Collieries Company Limited.

7. PERSONAL HEARING:

The Authorized representatives of the unit namely Sri R. Raghavendra Rao, Advocate & N Suresh, SGM Taxation attended the personal hearing held on 25.08.2022. The authorized representatives reiterated their averments in the application submitted to dispose the case on merit basis. They were advised by the AAR to submit the complete contract documents of both the contract.

8. DISCUSSIONS & FINDINGS:

8.1 The applicant M/s. PES Engineer Private Limited has entered into two separate agreements with Singareni Collieries Company Limited on the same day i.e., 09.02.2022. The objective of the contract as expressed in the title of both the agreements is as follows:

“Whereas the Employer desires to engage the Contractor to design, manufacture, test, deliver, install, complete and commission and conduct guarantee tests of certain Facilities, viz., Fuel Gas Desulphurisation (FGD) System Package for Singareni TPS, Stage-1 (2 X 600 MW) under Bidding Document No.CW-CM-11017-C-O-M-003 (“the Facilities”) and the Contractor have agreed to such engagement upon and subject to the terms and conditions hereinafter appearing.”

The above narration is given in both the contracts indicating that this is a turnkey contract for construction of a single immovable property. However, the applicant contends that there are two different and severable or divisible contracts within the same contract agreement.

8.2 The applicant contended that since the first contract, of the single contract agreement, involves supply of goods, he is entitled for the benefit of Notification No.66/2017 Central Tax, dated 15th November, 2017 which notified that those registered persons who did not opt for the composition levy under section 10 of the CGST Act’2017 as the class of persons who shall pay the central tax on the outward supply of goods at the time of supply as specified in clause (a) of sub-section (2) of section 12 of the said Act including in the situations attracting the provisions of section 14 of the said Act, and shall accordingly furnish the details and returns as mentioned in Chapter IX of the said Act and the rules made there under and the period prescribed for the payment of tax by such class of registered persons shall be such as specified in the said Act.

“supply” under Section 7 of the CGST Act includes supply of goods or services made or agreed to be made for a consideration. Thus the factum of supply would be initiated once the agreement is entered into between the supplier and recipient and such agreement is for consideration.

Section 12(2)(a) of CGST Act’2017 states that the liability to pay tax on goods shall arise at the time of supply, which is the date of issue of invoice by the supplier or the last date on which he is required, under section 31, to issue the invoice with respect to the supply;

The applicant contended that he is liable to pay tax on goods at the time of supply, which is the date of issue of invoice and not on the date on which he receives advance payments for those goods.

8.3 The issue to be decided in this case is whether the entire supply which involves two separate contracts however a single bidding document, has to be treated as a composite supply of which the principal supply is the second contract which is a ‘works contract’ or both the contracts have to be treated as separate transactions for which the ‘time of supply’ and ‘rate of tax’ to be levied would differ as per the provisions of the CGST Act’2017.

8.4 As stated by applicant that his responsibility under the first contract completes with making goods (ex-works) available and loading them on to the mode of transport. That the moment he raises tax invoice for the supply of goods, endorse and dispatch the documents, the title of the goods passes on to SCCL. This makes the first contract under category of supply of goods to the recipient as the recipient holds the title of goods before they reach his premises as stated by the applicant. It is supply of goods under First contract if the recipient holds the title of goods before the Second contract is initiated which involves inland transportation for delivery at site, inland transit insurance, unloading, storage, handling at site, installation, insurance covers other than inland transit insurance, testing and commissioning including carrying out guarantee tests in respect of all the plants and equipment supplied under the ‘First Contract’. If there is no transfer of title until completion of Second contract then the entire scope of supply would come under category of ‘works contract’.

8.5 It is observed that the Notification of Award of First Contract was issued by M/s SCCL vide Ref.No. CRP/MP/01/E0119O0413/FGD/5576 dated 28/12/2021. The scope of First Contract is sale of goods ex-manufacture / ex-works. It is a contract for pure sale of goods. As per Clause 31 of the General Conditions of the said Contract,

“31. Transfer of Ownership

31.1 Ownership of the Plant and Equipment

Ownership of the Plant and Equipment (including spare parts) procured in the country where the Site is located shall be transferred to the Employer when the Plant and Equipment are loaded on to the mode of transport to be used to convey the Plant and Equipment from the works to the site and upon endorsement of the despatch documents in favour of the Employer.”

From the above clause, it is clear that the responsibility of the Applicant under the first contract completes with making goods available ex-works and loading them on to the mode of transport. The moment the Applicant raises tax invoice for the supply of goods and endorse the despatch documents, the title of the goods passes on to SCCL. As per Appendix 3 of the Contract ( Insurance Requirements), in respect of Main equipment, the Applicant is required to obtain insurance for 110% of the value of the goods and SCCL has to be named as co-insured. The first contract thus involves supply of Goods as defined under Section 2(52) of CGST Act’2017 which states goods as every kind of movable property with some exceptions. The supply of Plant and Equipment (including Type Test Charges) and Mandatory Spares are still not installed or fixed to become a permanent structure before they are brought to the applicant premises and hence they’re movable which makes them to be classified under the category of Goods. The Applicant will issue tax invoices for supply of goods under the First Contract by mentioning respective HSN codes applicable for individual items and will pay GST by applying the rate of GST specified for these items as and when they are supplied and as per time of supply in terms of provisions of Sec 12 of the CGST / TSGST Act, 2017.

8.6 The Notification of Award of Second Contract was issued by M/s SCCL vide Ref.No. CRP/MP/01/E0119O0413/FGD/5577 dated 28/12/2021.The scope of work under the Second Contract is “Inland Transportation of the main equipment, inland transit insurance, unloading at site, storage, erection, civil works, Safety aspects/Compliance to Safety Rules and other services insurance covers other than inland transit insurance, testing, commission and conducting guarantee tests”. Thus, the supply under Second Contract is Works Contract Service as defined under Sec 2(119) falling under SAC 9954 as it involves activities among construction, fabrication, completion, erection, installation and fitting out etc. The definition of works contract is abstracted as under:

Section 2(119) “ ‘works contract’ means a contract for building, construction, fabrication, completion, erection, installation, fitting out, improvement, modification, repair, maintenance, renovation, alteration or commissioning of any immovable property wherein transfer of property in goods (whether as goods or in some other form) is involved in the execution of such contract.”

8.7 In this context, an insight is provided by CBIC Circular No 47/21/2018-GST dated 8-6-2018 relating to how servicing of cars involving both supply of goods (spare parts) and services (labour), where the value of goods and services are shown separately, is to be treated under GST. This dispute was going on since long as to whether the service provided by authorized service stations will be termed as composite supply and it will be taxed accordingly. But most of the service providers, bill separately for material as well as for labor charges. In the said Circular, it is clarified that, “the taxability of supply would have to be determined on a case to case basis looking at the facts and circumstances of each case. Where a supply involves supply of both goods and services and the value of such goods and services supplied are shown separately, the goods and services would be liable to tax at the rates as applicable to such goods and services separately.”

Thus, it is clear that a decision on taxability is to be arrived at on a case to case to case basis. The context of supply, intent of supply provider and recipient, nature of agreements, method of invoicing, nature of payment terms are the few factors which can help to ascertain the taxability of the supply. This implies that multiple supplies can be made within the same contract, when the parties intend to treat them as different supplies and thus intention of the parties is a factor to be reckoned with to decide the nature of supply.

8.8 Thus in the instant case, there is no doubt that there are multiple supplies of both goods and services being undertaken as part of two separate contracts. While the supply emanating from First Contract is a supply of goods i.e the Flue Gas Desulphurization (FGD) system, Limestone and gypsum handling system, items related to chimney and the spares related to above parts etc. The supply under second contract is primarily a service of Transportation, Insurance, Unloading At Site, Storage, Erection, Civil Works, Safety Aspects/Compliance To Safety Rules, Testing, Commission and Conducting Guarantee Tests of the items/goods supplied under First Contract. We find that there is no dispute on the nature of supply by each of the above-mentioned Contracts. The bone of contention is whether the supplies are to be termed as a composite supply or not. For a supply to be consider as a composite supply, its constituent supplies should be so integrated with each other that one cannot be supplied in the ordinary course of business without or independent of the other.

Section 2(30) of the CGST Act, 2017 defines “composite supply” as follows:-

“composite supply ” means a supply made by a taxable person to a recipient consisting of two or more taxable supplies of goods or services or both, or any combination thereof which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply;

Illustration. – Where goods are packed and transported with insurance, the supply of goods, packing materials, transport and insurance is a composite supply and supply of goods is a principal supply;

From the above definition, it is evident that the primary elements of the composite supply under Section 2(30) of the CGST Act, 2017 are:

a) There should be two or more taxable supplies,

b) The taxable supplies should be naturally bundled,

c) They should be supplied in conjunction with each other in ordinary course of business.

d) One of the supplies should be a principal supply.

For a supply to be consider as a composite supply, its constituent supplies should be so integrated with each other that one cannot be supplied in the ordinary course of business without or independent of the other. In other words, they should be naturally bundled. The term ‘naturally bundled’ has not been defined in the GST Act. The concept of the “Naturally Bundled”, as used in Section 2(30) of the CGST Act, 2017, lays emphasis on the fact that the different elements in a composite supply are integral to the overall supply and if one of the elements is removed the nature of supply will be affected.

8.9 Thus the concept of ‘naturally bundled’ is not visible in this contract agreement where the two contracts can be executed independently. The recipient can also award the two contracts to different suppliers and get his work done. This makes it pertinent to note that both the contracts are not naturally bundled together. The second contract can be executed either by the applicant himself or by third party if the recipient agrees to award the second contract of the contract agreement to a third party. This is because the second contract can be executed independently as it is not naturally bundled to the first contract. In this case, although there is only one contract agreement, separate invoices were issued for different activities done at various periods, as specified in the contract agreement, as the both contracts can be executed independently.

8.10 Further as per the definition of the Works Contract under Section 2(119), one of the conditions is that the property in goods used in execution of works contract must be transferred during the execution of contract. In the present case the appellant under the first contract supplies goods available ex-works and loads them on to the mode of transport. The moment the Applicant raises tax invoice for the supply of goods and endorse the despatch documents, the title of the goods passes on to SCCL. Thus the property in the said goods does not remain with the respondent but the same is transferred to supply recipient and while execution of the works contract vide the second contract the property in the said goods was with the recipient. Since the transfer of property in the said goods is not taking place during the execution of the Works Contract Service the value thereof cannot be included in the Works Contract. Further at the same time the applicant will use certain accessories and parts for execution of Works Contract under second contract and value thereof is admittedly included for the reasons that the property in the said good was transferred only during execution of works contract service. Therefore, there is a clear distinction between goods property of which is transferred prior to execution of Works Contract Service and the property in the goods transferred during the execution of Works Contract under second contract.

8.11 In this context we want to rely upon Hon’ble CESTAT in case of C.C.E. & S.T., AHMEDABAD-III Versus KALPATARU POWER TRANSMISSION LTD., 2021 (48) G.S.T.L. 354 (Tri. – Ahmd.),wherein this identical issue was discussed at length. It is noteworthy here that though the judgment is of service tax period, the definition of Works Contract in earlier regime and present GST regime both emphasize on “transfer of property in goods (whether as goods or in some other form) is involved in the execution of such contract.”

6.6 We find that there is a clear terms and conditions between the respondent and the service recipient i.e. EDAs that separate contract has to be entered into, one for manufacture and sale of goods and other is works contract service of erection, installation and commissioning of transmission line. All the service recipient i.e. EDAs are government organization and it cannot be imagined that the government organization will enter into this malpractices to evade service tax by bifurcating the one composite contract into two. It is a fact on records that as regard the supply contract mainly it is a transmission tower which is admittedly manufactured by the respondent in their factory and cleared there- from. These goods were sold at factory gate of respondent therefore, the property in the said goods stands transferred the moment it is cleared from the gate of the respondent. Therefore, it cannot be said that the appellant have provided the Works Contract Service along with the goods manufactured and supplied by them. In this transaction the appellant executed the Works Contract Service with the labour and certain other material used in erection, installation and commissioning. As regard the goods manufactured and supplied by the respondent the same belongs to service recipient i.e. EDAs therefore, the value of the said goods cannot be included in the gross value of Works Contract Service.

6.7 This is not a case where the service provider i.e. appellant and the service recipient i.e. EDAs have colluded and with intention to evade service tax entered into two contract one for supply of goods and other for providing service of erection, installation and commissioning of transmission line. In the bid document itself which was offered by the service recipient put a clear condition that two separate contracts need to be entered into i.e. one for supply of service and other for supply/sale of goods therefore, both the contracts are separate contract and cannot be clubbed together.

6.8 As per the definition of the Works Contract Service one of the condition is that the property in goods used in execution of works contract must be transferred during the execution of contract. In the present case the appellant while clearing the transmission towers from their factory issued the sale invoices accordingly, the property in the said goods does not remain with the respondent but the same was transferred to service recipient and while execution of the works contract service the property in the said goods was with the recipient. Since the transfer of property in the said goods is not taking place during the execution of the Works Contract Service the value thereof cannot be included in the Works Contract Service. At the same time the respondent have used certain accessories and parts for execution of Works Contract Service and value thereof was admittedly included for the reasons that the property in the said good was transferred only during execution of works contract service. Therefore, there is a clear distinction between goods property of which is transferred prior to execution of Works Contract Service and the property in the goods transferred during the execution of Works Contract Service. In view of the clear provision under Works Contract (Composition Scheme for Payment of Service Tax) Rules, 2007 as amended by Notification No. 23/2009-S.T., dated 7-7-2009 the value of the goods, property of which belongs to service recipient before execution of Works Contract Service, shall not be included in the gross amount of Works Contract Service.

6.9 The revenue’s contention is that appellant being common for supply of goods and provider of Works Contract Service cannot enter into separate contract and in such case the one composite contract is not divisible. On this issue much water was flown. In the various courts have given judgments on this issue some of the judgment cited :

- Bhagwandas Goverdhandas Kedia v. Girdharilal Parshottamdas & Co., AIR 1966 SC 543

- Tata Cellular v. Union of India, (1994) 6 SCC 651.

6.10 From the above judgments it can be seen that reliance on the tender or invitation to bid to decide the nature of the contract or the right and obligation flowing under a contract entered pursuant thereto is wholly misplaced, which would be governed only by the contracts entered into two between the parties. In the present case even though there is single bid that contain the condition of separate contract for supply of goods and supply of service. The two separate contracts are correct and legal and the same cannot be clubbed and held that it is a composite contract. The bid/tender is only a offering to the prospective contracts however, the contract is an agreement between two parties and which is recognized as a legal document therefore, when two separate contract are entered into between two separate parties, revenue cannot insist that there should be one composite contract. Therefore, we are of the clear view that even though there is single bid/tender, the two separate contracts are legal and correct and no question can be raised. In the following judgments the issue in question was considered :

- State of Madras v. Gannon Dunkerley & Co. (Madras) Ltd. – (1958) 9 STC 353 = 2015 (330) E.L.T. 11 (S.C.)

- Hindustan Aeronautics Ltd. v. State of Karnataka, (1984) 1 SCC 706

- Builders’ Assn. of India v. Union of India, (1989) 2 SCC 645

- State of Karnataka v. Trans Global Power Limited – (2015) 77 VST 509

- Reliance Infrastructure Ltd. v. Deputy Commissioner – 2015 VIL 60 CAL

- Ishikawajma-Harima Heavy Industries Ltd. v. Director of Income-tax, (2007) 3 SCC 481 = 2007 (6) S.T.R. 3 (S.C.).

6.11 In the above judgments one common issue has been considered that there can be two separate contracts, that is one for sale and another for Works Contract Service as in the present case the value of goods sold, property of which in goods has already been passed on, cannot form part of the value of the second contract i.e. Works Contract.

6.12 The Contention of the revenue is that it is necessary to enter a single indivisible contract is contrary to the principle that there are more than one way for performing an act. It is for parties concerned to choose the method and manner. In this regard the Hon’ble Supreme Court in CIT v. Motors and General Stores (P) Ltd., (1967) AIR 1968 SC 200 reads as under :

‘6. In a later case – Commissioners of Inland Revenue v. Wesleyan and General Assurance Society [30 TC II ] – Viscount Simon expressed the principle as follows :

“……………..

Secondly, a transaction which, on its true construction, is of a kind that would escape tax, is not taxable on the ground that the same result could be brought about by a transaction in another from which would attract tax..”’

6.13 From the above judgment it is clear that even if it is contented that due to two separate contracts there is a shortfall in payment of tax that itself cannot be a reason to reject the concept of two separate contract legally entered into between two parties. Therefore the revenue’s contention related to this is also not sustainable.

8.12 Further there are number of judgments wherein Hon’ble Supreme Court has observed that there can be two separate contracts, that is one for sale and another for Works Contract as in the present case the value of goods sold, property of which in goods has already been passed on, cannot form part of the value of the second contract i.e. Works Contract. Some of them are cited below:-

8.13 In the case of State of Madras Vs. Gannon Dunkerley & Company (Madras) Ltd., [1958] 9 STC353(SC); The Apex Court held that,

“•it is possible that the parties might enter into distinct and separate contracts, one for transfer of materials for money consideration and other for payment of remuneration for services and work done. In these cases, there is two separate agreements, even though there is a single instrument embodying them and the power of the State to separate the agreement to sell, from the agreement to do work and render service and to impose a tax thereon cannot be questioned, and will stand untouched by the present judgment.” [Para 57].

8.14 State of Karnataka Vs. Pro. Lab, 2015(321)EIT 366(SC); the Apex Court held that ,

“….by legal fiction under Article 366(29A) (b) of the Constitution of India there is a deemed sale of goods involved in execution of works contract-Such deemed sale has all incidents of sale of goods involved in execution of works contract , where contract is divisible into one for sale of goods and other for supply of labour and services- Such contract in on par with contract with two separate agreements and State have now power to levy sales tax on value of materials in execution of works contract.”[Para 101(viii)].

8.15 Commissioner Vs. Essar Projects (India) Ltd., 2014(36) STRJ 153(SC); the Apex Court held that,

“….The Appellate tribunal in its impugned order has held that a contract has to be interpreted in a manner from the apparent tenor of the agreement and apparently it has to be accepted as the real state of affairs. The Tribunal further held that both the contract dated 24-08-2007 for supply of equipment’s and construction of works has to be treated as distinct and separate contracts and value of supply contract cannot be added to the value of construction contract for the purpose of Service Tax Liability.”

8.16 In view of above discussion, we summarize as follows:-

- The scope of works/supply undertaken under the individual contracts are entirely independent and specific to that contract and are not associated with other contract.

- Contract agreement document itself, in this case, had put a condition that there are two separate contracts that need to be entered into i.e. one for supply of service and other for supply/sale of goods. Therefore, both the contracts are separate and cannot be clubbed together.

- The supply undertaken under the first contact terminates with making goods available ex-works and loading them on to the mode of transport. The moment the Applicant raises tax invoice for the supply of goods and endorse the despatch documents, the title of the goods passes on to M/s SCCL.

- The supply under the second contact commences with service of transportation of the said goods supplied under first contract. Since the transfer of property in the goods supplied under first contract is not taking place during the execution of the Works Contract under second contract, the value thereof cannot be included in the Works Contract. Thus the supply/ service under second contract commences commences only on completion of all the milestone activities of first contract. Therefore, it is evident that each Contract is independent and every milestone supply made from the individual contract is, an independent transaction.

- The mere fact that different tasks, i.e. two contracts for which separate invoices were issued by him to his recipient, have been entrusted to the applicant through a single contract agreement would not make it a ‘composite supply’ in terms of Section 2(30) of the CGST Act, 2017 for the reasons discussed supra.

- When both the contracts are viewed as separate contracts, not withstanding that both were mentioned in the single Conditions of Contract, then the taxpayer is eligible for the benefit of Notification No. 66/2017-Central Tax dated November 15, 2017 for the outward supply of goods. Accordingly the tax liability on supply of goods, as per First Contract, will arise as specified in clause (a) of sub-section (2) of section 12 of the said Act i.e. at the time of supply, which is the date of issue of invoice by the taxpayer or the last date on which he is required, under section 31, to issue the invoice with respect to the supply and not on the date on which he receives advance payments for those goods.

9. In view of the foregoing, we rule as follows:

In view of the above discussion, the question raised by the applicant is clarified as per the below rulings:

|

Questions |

Ruling |

| Whether the applicant is required to pay GST on “initial advance” of 5% and “interim” advance of 7.5% on Ex works value of goods supplied under “First Contract Agreement” dated 9th February, 2022 with M/s. Singareni Collieries Company Limited | The applicant is eligible for the benefit of Notification No. 66/2017-Central Tax dated November 15, 2017 as discussed supra and accordingly the tax liability on sale of goods, as per First Contract, will arise as specified in clause (a) of sub-section (2) of section 12 of the said Act i.e. at the time of supply, which is the date of issue of invoice by the taxpayer or the last date on which he is required, under section 31, to issue the invoice with respect to the supply. |

[Under Section 100(1) of the CGST/TGST Act, 2017, any person aggrieved by this order can prefer an appeal before the Telangana State Appellate Authority for Advance Ruling, Hyderabad, within 30 days from the date of receipt of this Order]

Author Bio