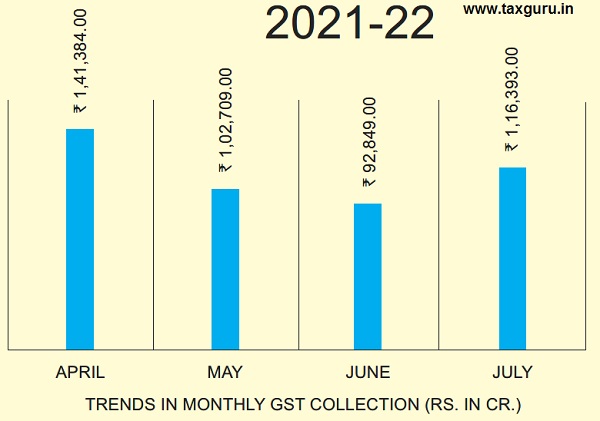

GST Revenue for July 2021

> ₹ 1,16,393 crores gross GST revenue collected in July

The gross GST revenue collected in the month of July 2021 is Rs. 1,16,393 crores of which CGST is Rs. 22,197 crores, SGST is Rs. 28,541 crores, IGST is Rs. 57,864 crores (including Rs. 27,900 crores collected on import of goods) and Cess is Rs. 7,790 crores (including ` 815 crores collected on import of goods). The above figure includes GST collection received from GSTR-3B returns filed between 1st July, 2021 to 31 , July 2021 as well as IGST and cess collected from imports for the same period.

The GST collection for the returns filed between 1st July to 5th July,2021 of Rs. 4,937 crores had also been included in the GST collection in the press note for the month of June, 2021 since taxpayers were given various relief measures in the form of waiver/reduction in interest on delayed return filing for 15 days for the return filing month June 21 for the taxpayers with the aggregate turnover upto Rs. 5 crores in the wake of COVID-19 pandemic second wave.

The government has settled Rs. 28,087 crores to CGST and Rs. 24100 crores to SGST from IGST as regular settlement. The total revenue of Centre and the States after regular settlement in the month of July, 2021 is Rs. 50284 crores for CGST and Rs. 52641 crores for the SGST.

The revenues for the month of July 2021 are 33% higher than the GST revenues in the same month last year. During the month, revenues from import of goods was 36% higher and the revenues from domestic transaction (including import of services) are 32% higher than the revenues from these sources during the same month last year.

GST collection, after posting above Rs. 1 lakh crores mark for eight months in a row, dropped below Rs. 1 lakh crores in June, 2021 as the collections during the month of June 2021 predominantly related to the month of May 2021 and during May 2021, most of the States/UTs were under either complete or partial lock down due to COVID-19. With the easing out of COVID-19 restrictions, GST collection for July,2021 has again crossed Rs. 1 lakh crores, which clearly indicates that the economy is recovering at a fast pace. The robust GST revenues are likely to continue in the coming months too. Source: PIB Press Release dated 01.08.2021

GST Compensation shortfalls released to States

> Rs. 75,000 crores released to States and UTs with Legislature as GST Compensation shortfall which is almost 50 % of the total shortfall for the entire year released in a single instalment

The Government on 15.07.2021 has released Rs. 75,000 crores to the States and UTs with Legislature under the back-to-back loan facility in lieu of GST Compensation. This release is in addition to normal GST compensation being released every 2 months out of actual cess collection.

Subsequent to the 43rd GST Council Meeting held on 28.05.2021, it was decided that the Central Government would borrow Rs. 1.59 lakh crores and release it to States and UTs with Legislature on a back-to-back basis to meet the resource gap due to the short release of Compensation on account of inadequate amount in the Compensation Fund. This amount is as per the principles adopted for a similar facility in FY 2020-21, where an amount of ₹1.10 lakh crores was released to States under a similar arrangement. This amount of Rs. 1.59 lakh crores would be over and above the compensation in excess of Rs. 1 lakh crores (based on cess collection) that is estimated to be released to States/UTs with Legislature during this financial year. The sum total of Rs. 2.59 lakh crores is expected to exceed the amount of GST compensation accruing in FY 2021-22.

All eligible States and UTs (with Legislature) have agreed to the arrangements of funding of the compensation shortfall under the back-to-back loan facility. For effective response and management of COVID-19 pandemic and a step-up in capital expenditure, all States and UTs have a very important role to play. For assisting the States/UTs in their endeavor, Ministry of Finance has front loaded the release of assistance under the back-to-back loan facility during FY 2021-22 and Rs. 75, 000 crores (almost 50 % of the total shortfall for the entire year) has been released in a single instalment. The balance amount will be released in the second half of 2021-22 in steady instalments.

The release of Rs. 75,000 crores being made now is funded from borrowings of GoI in 5-year securities, totaling Rs. 68,500 crores and 2-year securities for Rs. 6,500 crores issued in the current financial year, at a Weighted Average Yield of 5.60 and 4.25 percent per annum respectively.

It is expected that this release will help the States/UTs in planning their public expenditure among other things, for improving, health infrastructure and taking up infrastructure projects.

State/ UTs wise amount released as “Back to Back Loan in lieu of GST Compensation Shortfall” on 15.07.2021

| Sl. No. |

Name of the State/ UTs | GST Compensation shortfall released | ||

| 5-year tenor | 2-year tenor | Total | ||

| 1. | Andhra Pradesh | 1409.67 | 133.76 | 1543.43 |

| 2. | Assam | 764.29 | 72.52 | 836.81 |

| 3. | Bihar | 2936.53 | 278.65 | 3215.18 |

| 4. | Chhattisgarh | 2139.06 | 202.98 | 2342.04 |

| 5. | Goa | 364.91 | 34.63 | 399.54 |

| 6. | Gujarat | 5618.00 | 533.10 | 6151.10 |

| 7. | Haryana | 3185.55 | 302.28 | 3487.83 |

| 8. | Himachal Pradesh | 1161.08 | 110.18 | 1271.26 |

| 9. | Jharkhand | 1070.18 | 101.55 | 1171.73 |

| 0. | Karnataka | 7801.86 | 740.31 | 8542.17 |

| 1. | Kerala | 3765.01 | 357.26 | 4122.27 |

| 2. | Madhya Pradesh | 3020.54 | 286.62 | 3307.16 |

| 3. | Maharashtra | 5937.68 | 563.43 | 6501.11 |

| 4. | Meghalaya | 60.75 | 5.76 | 66.51 |

| 5. | Odisha | 2770.23 | 262.87 | 3033.10 |

| 6. | Punjab | 5226.81 | 495.97 | 5722.78 |

| 7. | Rajasthan | 3131.26 | 297.13 | 3428.39 |

| 8. | Tamil Nadu | 3487.56 | 330.94 | 3818.50 |

| 9. | Telangana | 1968.46 | 186.79 | 2155.25 |

| 10. | Tripura | 172.76 | 16.39 | 189.15 |

| 11. | Uttar Pradesh | 3506.94 | 332.78 | 3839.72 |

| 12. | Uttarakhand | 1435.95 | 136.26 | 1572.21 |

| 13. | West Bengal | 2768.07 | 262.66 | 3030.73 |

| 14. | UT of Delhi | 2668.12 | 253.18 | 2921.30 |

| 15. | UT of Jammu & Kashmir | 1656.54 | 157.19 | 1813.73 |

| 16. | UT of Puducherry | 472.19 | 44.81 | 517.00 |

| Total: | 68500.00 | 6500.00 | 75000.00 | |

Source: PIB Press Release dated 15.07.2021

Finance Minister Smt. Nirmala Sitharaman appreciates CBIC

> Finance Minister Smt. Nirmala Sitharaman appreciates CBIC efforts in fighting COVID-19 pandemic; says enhanced revenue collection in recent months should now be the “New Normal”

The fourth anniversary of introduction of GST, the GST Day, 2021, was marked by Central Board of Indirect Taxes and Customs (CBIC) and all its field offices across India on 01.07.2021. The national level programme was organised by CBIC through virtual mode on the digital platform which was attended by all field formations. GST with enhanced revenue collections for last eight months has been instrumental in building an ‘Aatma Nirbhar’ Bharat. The year marked enhanced taxpayer facilitation with COVID-19 relief packages being announced to ease the burden of compliance. As part of the programme 31 officers were awarded with the GST Day commendation certificate across all zones and one officer was awarded posthumously.

\In a message on GST Day 2021, Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman said that it is a matter of great satisfaction that we have overcome most challenges, including two waves of unprecedented COVID-19 pandemic, in providing stability to this new tax regime. The Finance Minister was happy to note the buoyant tax collections which crossed ` 1 lakh crores for eight months in a row with record GST collection of ` 1.41 lakh crores in April, 2021. The enhanced revenue collection in recent months should now be the “new normal”, She added. Smt. Sitharaman appreciated CBIC effort in recognising more than 54,000 GST taxpayers for their contribution to nation building on the eve of four years of implementation of GST. Taxpayers facilitation during pandemic involved two COVID-19 relief packages covering late fee waiver, interest rate reduction, relaxation of timelines and conducting refund drives to enhance liquidity in the hands of taxpayer. Further, GST rates on vaccines, essential medicines and products/services used for prevention and treatment of COVID-19 were also reduced.

The Finance Minister condoled the loss of 189 personnel and remembered their contribution to the national effort and noted the effort of CBIC in releasing a book “Shraddhanjali” to pay homage to these departed souls. Smt. Sitharaman also congratulated all awardees of ‘Commendation Certificate’ for their exceptional contribution in GST administration.

In his message, Minister of State for Finance & Corporate Affairs Shri Anurag Singh Thakur expressed gratitude to trade and industry, specially MSMEs, whose continuous support and feedback has helped the Government in steadily improving GST laws, procedures and systems over last four years. Shri Thakur condoled the loss of many precious lives from the GST family to COVID-19 pandemic. Shri Thakur congratulated all officers selected for commendation certificate for their dedication, hard work and the spirit of serving the nation.

In his virtual message played during the programme, Shri Bibek Debroy, Chairman, Prime Minister Economic Advisory Council, highlighted that GST is a work in progress which is improving by each passing day. GST has cut down on large number of indirect taxes, brought down litigations and removed inter-state restrictions. During the programme, video messages of eminent personalities from various fields were also played.

Chairman CBIC Shri M. Ajit Kumar lauded the efforts of CBIC officers in facilitating taxpayers during the pandemic and use of technology to ensure minimum physical interaction. He appreciated the taxpayers for coming back strong post COVID-19 and ensuring V-shaped recovery of economy. CBIC effort in recognising more than 54,000 GST taxpayers for their contribution to nation building is a testimony to the fact that their support to GST is imminent. CBIC Members highlighted the automation done over the years in GST processes and exhorted the officers to enhance the use of technology. Sh. Vivek Johri, Member GST appreciated the DGARM reports and MIS generated which is used by field formations to increase revenue collections.

Source: PIB Press Release dated 01.07.2021

Notifications & Circulars

> Clarification regarding extension of limitation under GST Law in terms of Hon’ble Supreme Court’s Order dated 27.04.2021.

The Government has issued notifications under Section 168A of the CGST Act, 2017, wherein the time limit for completion of various actions, by any authority or by any person, under the CGST Act, which falls during the specified period, has been extended up to a specific date, subject to some exceptions as specified in the said notifications. In this context, various representations have been received seeking clarification regarding the cognizance for extension of limitation in terms of Hon’ble Supreme Court Order dated 27.04.2021 in Miscellaneous Application No. 665/2021 in SMW(C) No. 3/2020 under the GST law. The issues have been examined and to ensure uniformity in the implementation of the provisions of law across the field formations, the Board, in exercise of its powers conferred by section 168 (1) of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as “CGST Act”), the Government vide Circular No. 157/13/2021-GST has issued clarification pertaining to the extension of limitation under GST Law in terms of the Supreme Court’s Order dated 27.04.2021.

Circular No. 157/13/2021-GST dated 20.07.21

> Notification with respect to section 110 and 111 of the Finance Act, 2021 w.e.f. 01.08.2021.

The Government has notified that the provisions of Section 110 & 111 of the Finance Act, 2021 shall come into force w.e.f. 01.08.2021.

Notification No. 29/2021-Central Tax dated 30.07.2021

> Notification regarding amendment of Rule 80 of the CGST Rules, 2017 and notification of Form GSTR 9 and 9C for FY 2020-21. Rule 80 provides for exemption from GSTR-9C to taxpayers having AATO up to Rs. 5 crores.

The Government with said notification has amended Rule 80 related to Annual GST Return, the notification also amended Instructions related to GSTR 9 and also amended Form GSTR 9C.

Notification No. 30/2021-Central Tax dated 30.07.2021

> Notification exempting taxpayers having AATO up to Rs. 2 crores from the requirement of furnishing annual return for FY 2020-21.

The Government has exempted the registered person whose aggregate turnover in the financial year 2020-21 is up to 2 crores rupees, from filing annual GST return for the said financial year. This would ease compliance requirement of furnishing reconciliation statement in FORM GSTR-9C, as taxpayers would now be able to self-certify reconciliation statement, instead of getting it certified by a chartered accountant.

Notification No. 31/2021-Central Tax dated 30.07.2021

GST Portal Updates

> Important changes related to QRMP Scheme implemented on the GST Portal for the taxpayers

A. Few important changes related to QRMP Scheme implemented on the GST Portal for the taxpayers are as given below Auto population of GSTR-3B liability from IFF and Form GSTR 1: A taxpayer under QRMP Scheme can declare their liability through optional IFF for Month 1 and Month 2 of a quarter & Form GSTR-1 for Month 3 of that quarter. Declaration of liability in these forms would now be auto-populated in their Form GSTR-3B (Quarterly) for that quarter, based on their filed Form GSTR-1 and IFF. These fields are editable and in case their values are revised upwards or downwards, the edited field(s) would be highlighted in red color and a warning message will be displayed to the taxpayer. However, the system would not prevent taxpayer from filing of Form GSTR-3B with edited values.

B. Nil filing of Form GSTR-1 (Quarterly) through SMS: Nil filing of Form GSTR-1 (Qtrly.) through SMS has been enabled for taxpayers under QRMP Scheme. They can now file it by sending a message in specified format to 14409. The format of the message is < NIL > space < Return Type (R1) > space< GSTIN > space < Return Period (mmyyyy) >.

Example: NIL R1 07XXXXX1234H8Z6 062020 (where return period must be last month of the quarter)

However, NIL filing through SMS can’t be done in following scenarios:

- If IFF for Month 1 or 2 of a quarter is in Submitted stage, but not Filed.

- If invoices are Saved in IFF for Month 1 or 2 of a quarter, which was not submitted or filed by due date.

C. Impact of cancellation of registration on liability to file Form GSTR-1: In case registration of a taxpayer under QRMP Scheme is cancelled, with effective date of cancellation being any date after 1st day of Month 1 of a quarter, they would be required to file Form GSTR-1 for the complete quarter, as the last applicable return. For example, if the taxpayer’s registration is cancelled w.e.f. 1st of April, he/she is not required to file Form GSTR-1 for Apr-June quarter and Form GSTR-1 for Jan-Mar Quarter shall become the last applicable return. However, if the registration is cancelled on a later date during the quarter, the taxpayer would be required to file Form GSTR-1 for Apr-June quarter. In such cases the filing will become open on 1st of month following the month with cancellation date i.e. if cancellation has taken place on 20th May, Form GSTR-1 for Quarter Apr-June can be filed anytime on or after 1st of June.

D. For more details, please click on

1) https://tutorial.gst.gov.in/userguide/returns/index.htm#t=htm

2) https://tutorial.gst.gov.in/userguide/returns/index.htm#t=htm

3) https://tutorial.gst.gov.in/userguide/returns/index.htm#t= Creation_of_Outward_Supplies_Return_in_GSTR-1.htm

4) https://tutorial.gst.gov.in/userguide/returns/index.htm#t=Create_and_Submit_GSTR3B.htm

The above is for your information and necessary action please.

Portal updated on 06.07.2021

- Upcoming functionalities to be deployed on GST Portal for the Taxpayers in the month of July, 2021

As part of constant endeavor to provide a smooth and hassle-free experience to the taxpayers and simplify the process of meeting GST compliances, following changes were recently deployed/ would be deployed shortly, on the GST portal:

| Sl. No | Module | Form/ Functionality | Functionality released/ to be released for Taxpayers |

Current status of deployment |

| 1 | Registration | Timelines for filing of Application for Revocation of Cancellation of Registration in Form GST REG-21 |

In view of the spread of pandemic COVID-19 across many parts of India, vide Notification No 14/2021-CT, dated 1st May, 2021, read with vide Notification No 24/2021-CT, dated 1st June, 2021, the Government had extended the date for filing of various applications falling during the period from the 15th April, 2021 to 29th June, 2021, till 30th June, 2021. In addition to this, timeline for filing of Application for Revocation of Cancellation of Registration, which were due on 15th of April 2021, had also been extended till 30th June 2021 on the GST Portal.

Accordingly, these extensions have now ceased to be effective w.e.f. 1st July, 2021, and timelines for filing of application for revocation of cancellation is now changed to 90 days (as was earlier) on the GST Portal, from date of Order of Cancellation of Registration in Form GST REG-19. |

Deployed on 1st July, 2021 |

| 2 | Returns | Information regarding late fee payable provided in Form GSTR-10 |

Taxpayers whose registration is cancelled, at the time of filing of last return in Form GSTR-10, will now be provided with details of late fee payable by them, for the delayed filing of any of the previous returns/ statements in a table, for their assistance in filing of said return by them. This information can be viewed by clicking on a hyperlink provided under the column “Late Fee Payable” in the online Form GSTR- 10. | |

| The UIN holders file details of their inward supplies in Form GSTR-11 on a quarterly basis. They can subsequently file for refund (if required) in Form GST RFD- 10, for the quarter, in which summary of the documents is auto-populated from their Form GSTR-11, in an editable mode | ||||

| 3 | Returns | Auto-population of data in Form GSTR-11 on basis of Forms GSTR-1 / 5 filed by their suppliers | Form GSTR-11 of the UIN holder would be generated with details of their inward supplies, on basis of Forms GSTR-1 / 5 filed by their suppliers, which will subsequently help them in filing their refund claims | — |

Portal updated on 09.07.2021

> Module wise new functionalities deployed on the GST Portal for taxpayers

Various new functionalities are implemented on the GST Portal, from time to time, for GST stakeholders. These functionalities pertain to different modules such as Registration, Returns, Advance Ruling, Payment, Refund and other miscellaneous topics. Various webinars are also conducted as well informational videos prepared on these functionalities and posted on GSTNs dedicated YouTube channel for the benefit of the stakeholders. To view module wise functionalities deployed on the GST Portal and webinars conducted/ Videos posted on our YouTube channel, refer to table below:

Sl. No. |

Tax-payer functionalities deployed on the GST Portal during |

Click link below |

1 |

June, 2021 |

https://tutorial.gst.gov.in/downloads/news/newfunctionalitiescompilation_jun2021.pdf |

2 |

May, 2021 |

https://tutorial.gst.gov.in/downloads/news/newfunctionalitiescompilation_may%202021.pdf |

3 |

April, 2021 |

https://tutorial.gst.gov.in/downloads/news/newfunctionalitiescompilation_april%202021.pdf |

4 |

January-March, 2021 |

https://tutorial.gst.gov.in/downloads/news/newfunctionalitiescompilation_janmar2021.pdf |

5 |

October-December, 2020 |

https://tutorial.gst.gov.in/downloads/news/functionalities_released_octtodec2020.pdf |

6 |

Compilation of GSTN You-Tube Videos posted from January-December, 2020 |

https://tutorial.gst.gov.in/downloads/news/gstn_youtube_videos_posted_2020.pdf |

Portal updated on 09.07.2021

> Webinars on recent functionalities related to Returns, Ledgers and Payments deployed on GST Portal.

GSTN has recently implemented certain new functionalities on the GST Portal related to Returns, Ledgers and Payments. For creating awareness amongst all the stakeholders, GSTN held webinars, as per details given below:

Webinar Topic |

New functionalities related to Returns, Ledgers and Payments deployed on GST Portal |

||

Lan-guage of webinar |

Tamil |

English |

Marathi |

Date |

16.07.2021

|

20.07.2021

|

28.07.2021

|

Time |

1600 Hrs. to 1630 Hrs. |

1600 Hrs. to 1630 Hrs. |

1200 Hrs. to 1230 Hrs. |

Speaker You tube link to join |

Sh. Rafi Ahmed Kidwai, Manager, GSTN https://youtu.be/c3vInoyv8Js |

Sh. Sanjay Kumar Sharma,SM, GSTN https://youtu.be/QDtX-cnYi04 |

Sh. Bhagwan Patil, VP, GSTN https://youtu.be/Mx01B2KQ0cY |

Portal updated on 16.07.2021

> Filing of Annual returns by composition taxpayers. – Negative Liability in GSTR-4

Filing of Annual returns by composition taxpayers. – Negative Liability in GSTR-4 Instances have come to notice where taxpayers are reporting negative liability appearing in their GSTR-4

Background: Since FY 2019-20, composition taxpayers has to pay the liability through Form GST CMP-08 on quarterly basis while GSTR-4 Return is required to be filed on annual basis after end of a financial year. Reason of Negative Liability in GSTR4: The liability of the complete year is required to be declared in GSTR-4 under applicable tax rates. Taxpayers should fill up table 6 of GSTR-4 mandatorily. In case, there is no liability, the said table may be filled up with ‘0’ value. If no liability is declared in table 6, it is presumed that no liability is required to be paid, even though, taxpayer may have paid the liability through Form GST CMP-08. In such cases, liability paid through GST CMP-08 becomes excess tax paid and moves to Negative Liability Statement for utilization of same for subsequent tax period’s liability.

What the taxpayer did wrongly: Liability paid through Form GST CMP-08 is auto-populated in table 5 of the GSTR-4 for convenience of the taxpayers. Taxpayers who do not fill up table 6 of GSTR-4 i.e. no liability is declared, even though, taxpayer may have paid the liability through Form GST CMP-08; since the ‘Tax payable’ in GSTR-4 is computed after reducing the liability declared in GST CMP-08 and then auto-populated in table 5. Thus, if nothing is declared in table 6, then the negative liability entry appears in GSTR-4.

How to proceed in case of negative liability: If table 6 of GSTR-4 has not been filled due to oversight, a ticket may be raised to nullify the amount available in negative liability statement. If there is no liability to be paid during the year, the liability paid through Form GST CMP-08 shall move to negative liability statement and the same excess amount can be utilised to pay the liability of future tax periods.

Portal updated on 22.07.2021

> New functionality on Annual Aggregate Turnover (AATO) deployed on GST Portal for taxpayers.

GSTN has implemented a new functionality on taxpayers’ dashboards with the following features:

♦ The taxpayers can now see the exact Annual Aggregate Turnover (AATO) for the previous FY, instead of just the two slabs of above or upto Rs. 5 Cr.

♦ The taxpayers can also see the Aggregate Turnover of the current FY based on the returns filed till date.

♦ The taxpayers have also now been provided with the facility of turnover update in case taxpayers feel that the system calculated turnover displayed on their dashboard varies from the turnover as per their records.

♦ This facility of turnover update shall be provided to all the GSTINs registered on a common PAN. All the changes by any of the GSTINs in their turnover shall be summed up for computation of Annual Aggregate Turnover for each of the GSTINs

♦ The taxpayer can amend the turnover twice within a period of one month from the date of roll out of this functionality. Thereafter, the figures will be sent for review of the Jurisdictional Tax Officer who then can amend the values furnished by the taxpayer.

Note: For details, the taxpayers may check out the ‘Advisory’ section of the aforementioned functionality on their respective dashboards. Portal updated on 27.07.2021

> Functionality to check and update bank account details.

How to add bank account in GST registration details?

A functionality to check status of bank account details update for the taxpayers who have taken new registration at GST Portal but have not yet furnished the same, has been introduced, in view of Rule 10A of the CGST Rules 2017. Such taxpayers are required to update their Bank Account Details within 45 days of the first login henceforth.

The taxpayers may login and update Bank Account details through Non-core amendment in the manner as specified in the below table. In case the taxpayers who had not updated bank account after registration and are also failed to update within 45 days of their first login henceforth, the system will prompt and force them to comply with the requirements.

♦ Login to the taxpayer portal

♦ Go to ‘Services’

♦ Click on ‘Registration’

♦ Click on the tab ‘Amendment of Registration Non-Core Fields’

♦ Select tab ‘Bank Accounts’

♦ Add details of Bank Account (Account No., IFSC, Address, Bank Account type)

♦ Click on the verification tab, select authorized signatory, enter a place

♦ Sign application using DSC, E-sign or EVC

Note:

After completion of Bank Account update, a success message will appear on the screen, and the acknowledgment will be sent at the registered email and mobile phone.

Portal updated on 29.07.2021

*****

DISCLAIMER: This newsletter is in-house efforts of the GST Council Secretariat. The contents of this newsletter do not represent the views of GST Council and are for reference purpose only.

Printed & Published by – GST COUNCIL SECRETARIAT | 5th Floor, Tower-II, Jeevan Bharati Building, Connaught Place, |New Delhi 110 001, Ph: 011-23762656, www.gstcouncil.gov.in