Now a day banks are asking its customers having CC /OD facility to close current accounts. This is as per the RBI Circular Dated 06.08.2020. As per this circular no bank shall open current accounts for customers who have availed credit facilities in the form of cash credit (CC)/ overdraft (OD) from the banking system and all transactions shall be routed through the CC/OD account. If the customer does not have any CC/ OD facility then current account can be opened subject to certain guidelines depending upon his other borrowings (Like Term Loan etc.) of customer. Borrowings include both fund based as well as non-fund based borrowings.

The revised guidelines For Opening Current Accounts in banks in brief are as under: –

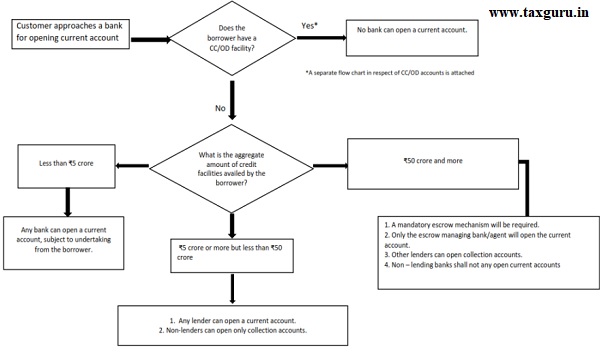

1. For a borrower with existing CC or OD facility: – The bank cannot open a current account for the borrower and all transactions have to be routed through the cash credit or overdraft account.

2. For a borrower with no existing CC or OD facility: – Banks can open a current account if the total exposure to the borrower is less than Rs 5 crore. But when the exposure exceeds Rs 5 crore, the borrower has to inform the bank and then rules would be different.

3. For a borrower having credit facilities (other than CC/OD) of Rs 5 Crore to Rs 50 Crore: – Any lender bank can open a current account, while non-lending banks can only open a collection account.

4. For a borrower having credit facilities (other than CC/OD) of more than Rs 50 Crore: – Banks shall be required to put in place an escrow mechanism. Accordingly, current accounts of such borrowers can only be opened / maintained by the escrow managing bank. However, there is no restriction on opening of ‘collection accounts’ by lending banks. While there is no prohibition on amount or number of credits in ‘collection accounts’, debits in these accounts shall be limited to the purpose of remitting the proceeds to the said escrow account. Non-lending banks shall not open any current account for such borrowers.

The revised guidelines For availing CC / OD facilities in banks in brief are as under: –

1. Where a bank has a share of less than 10 per cent in the total exposure of the banking system to the borrower: – The borrower can avail CC and OD facility form bank with exposure less than 10% but it can only be used for credit transactions.

Any debit transaction can only be to remit funds to the borrower’s CC or OD account held with a bank which has an exposure of 10% or more of the banking system’s total exposure to the borrower.

2. Where a bank has a share of 10 per cent or more in the total exposure of the banking system to the borrower: – Such Bank can provide CC/OD facility.

The detailed flow charts explaining all the above mentioned conditions for opening a current or CC / OD are as under: –

Flow Chart for opening of current accounts

Flow Chart for availing CC/OD facility

All the above mentioned guidelines laid down by RBI in detail as per the circular dated 06.08.2020 are as under:

i. No bank shall open current accounts for customers who have availed credit facilities in the form of cash credit (CC)/ overdraft (OD) from the banking system and all transactions shall be routed through the CC/OD account.

ii. Where a bank’s exposure to a borrower is less than 10 per cent of the exposure of the banking system to that borrower, while credits are freely permitted, debits to the CC/OD account can only be for credit to the CC/OD account of that borrower with a bank that has 10 per cent or more of the exposure of the banking system to that borrower. Funds will be remitted from these accounts to the said transferee CC/OD account at the frequency agreed between the bank and the borrower. Further, the credit balances in such accounts shall not be used as margin for availing any non-fund based credit facilities. In case there is more than one bank having 10 per cent or more of the exposure of the banking system to that borrower, the bank to which the funds are to be remitted may be decided mutually between the borrower and the banks. It may be noted that banks with exposure to the borrower of less than 10 per cent of the exposure of the banking system can offer working capital demand loan (WCDL) / working capital term loan (WCTL) facility to the borrower.

iii. Where a bank has a share of 10 per cent or more in the total exposure of the banking system to the borrower, it can provide CC/OD facility as hitherto.

iv. In case of borrowers covered under guidelines on loan system for delivery of bank credit issued vide circular DBR.BP.BC.No.12/21.04.048/2018-19 dated December 5, 2018, bifurcation of working capital facility into loan component and cash credit component shall henceforth be maintained at individual bank level in all cases, including consortium lending.

v. In case of customers who have not availed CC/OD facility from any bank, banks may open current accounts as under:

a. In case of borrowers where exposure of the banking system is ₹50 crore or more, banks shall be required to put in place an escrow mechanism. Accordingly, current accounts of such borrowers can only be opened / maintained by the escrow managing bank. However, there is no restriction on opening of ‘collection accounts’ by lending banks subject to the condition that funds will be remitted from these accounts to the said escrow account at the frequency agreed between the bank and the borrower. Further, the balances in such accounts shall not be used as margin for availing any non-fund based credit facilities. While there is no prohibition on amount or number of credits in ‘collection accounts’, debits in these accounts shall be limited to the purpose of remitting the proceeds to the said escrow account. Non-lending banks shall not open any current account for such borrowers.

b. In case of borrowers where exposure of the banking system is ₹5 crore or more but less than ₹50 crore, there is no restriction on opening of current accounts by the lending banks. However, non-lending banks may open only collection accounts as defined at (v) (a) above.

c. In case of borrowers where exposure of the banking system is less than ₹5 crore, banks may open current accounts subject to obtaining an undertaking from such customers to the effect that customers shall inform the bank(s), if and when the credit facilities availed by them from the banking system becomes ₹5 crore or more. The current account of such customers, as and when the exposure of the banking system becomes ₹5 crore or more and ₹50 crore or more, will be governed by the provisions of para (v) (b) and (v) (a) respectively.

d. Banks are free to open current accounts of prospective customers who have not availed any credit facilities from the banking system, subject to necessary due diligence as per their Board approved policies.

2. Banks shall monitor all current accounts and CC/ODs regularly, at least on a quarterly basis, specifically with respect to the exposure of the banking system to the borrower, to ensure compliance with these instructions.

3. Banks should not route drawls from term loans through current accounts. Since term loans are meant for specific purposes, the funds should be remitted directly to the supplier of goods and services. Expenses incurred by the borrower for day to day operations should be routed through CC/OD account, if the borrower has a CC/OD account, else through a current account.

All these guidelines are brought with the intention to bring discipline to the opening and operations in current accounts.

After this the RBI has come with further guidelines regarding allowing opening of specific purpose current accounts in addition to CC / OD vide its circular dated 14.12.2020. It has come with an indicative list of such specific purposes. The list is given below:

i. Accounts for real estate projects mandated under Section 4 (2) l (D) of the Real Estate (Regulation and Development) Act, 2016 for the purpose of maintaining 70% of advance payments collected from the home buyers.

ii. Nodal or escrow accounts of payment aggregators/prepaid payment instrument issuers for specific activities as permitted by Department of Payments and Settlement Systems (DPSS), Reserve Bank of India under Payment and Settlement Systems Act, 2007.

iii. Accounts for settlement of dues related to debit card/ATM card/credit card issuers/acquirers.

iv. Accounts permitted under FEMA, 1999.

v. Accounts for the purpose of IPO / NFO /FPO/ share buyback /dividend payment / issuance of commercial papers/allotment of debentures/gratuity, etc. which are mandated by respective statutes or regulators and are meant for specific/limited transactions only.

vi. Accounts for payment of taxes, duties, statutory dues, etc. opened with banks authorized to collect the same, for borrowers of such banks which are not authorized to collect such taxes, duties, statutory dues, etc.

vii. Accounts of White Label ATM Operators and their agents for sourcing of currency.

The above list provided by RBI being indicative and not inclusive so it can be inferred that no current account other than the above mentioned specific purpose current accounts can be opened in case the customer have CC / OD facility from bank.

Now it may be noted that for the purpose of computing aggregate exposure of the banking system, the exposure of non-banking financial companies (NBFCs) and other financial institutions like National Housing Bank (NHB) shall not be included. The instructions are applicable to Scheduled Commercial Banks and Payments Banks. Accordingly, the aggregate exposure for the purpose shall include exposures of these banks only. Further all fund based and non-fund based credit facilities sanctioned by the banks and carried in their Indian books shall be included for the purpose of aggregate exposure.

Moreover Banks are not allowed to open current accounts for borrowers who have availed agricultural/personal ODs or ODs against deposits. It may also be noted that In respect of proprietorship firms, credit facilities availed by the proprietor in his/her personal capacity like home loan, loan against property, etc shall also be included in the aggregate exposure of the banking system for the purpose of this circular.

Author Bio