Every country believes in keeping foreign reserves on a higher side to balance the economy. For that purpose, every economy tends to encourage the exports and motivate the indigenous production. To encourage the exporter every country provides a lot of benefits in terms of Duty Drawback etc. India is not behind compared to any other country to promote their exports and to reward the exporters.

However, there are a lot of benefits and facilities are mentioned in the FTP which are available for the exporters, some of such rewards which are being provided in the India’s Foreign Trade Policies (FTP) and direct benefits are mentioned below

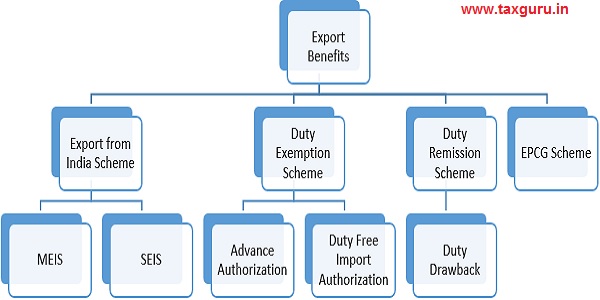

Export from India Scheme

Under this scheme, Duty Credit Scrips shall be granted as a reward under MEIS and SEIS. These scrips are freely transferable and can be used for the purposes of payment of Basic Custom Duty and Additional Custom Duty for import of goods including capital goods subject to some exceptions.

There shall be following two schemes for exports of Merchandise and Services respectively:

(i) Merchandise Exports from India Scheme (MEIS).

(ii) Service Exports from India Scheme (SEIS).

| Description | MEIS | SEIS |

| Objectives | To promote the manufacture and export of notified goods | To encourage and maximize export of notified services |

| Eligibility | Only notified goods are eligible which has to be exported to notified market. Appendix 3B of FTP mentions the notified goods and market | Service providers shall be located in India and only notified services are eligible. Appendix 3D mentions the notified services |

| Entitlement | 3% to 7% on realised FOB value of exports in free foreign exchange, or on FOB value of exports as given in the Shipping Bills in freely convertible foreign currencies, whichever is less, unless otherwise specified. Appendix 3B mentions the rate of entitlement for each class of goods and market | 3% to 7% on net foreign exchange earned from the notified services. Appendix 3D mentions the rate for each notified services |

| Other conditions | The total reward which may be granted to an IEC holder shall not exceed ₹ 2 Crore per IEC on exports made in the period 01.09.2020 to 31.12.2020 | Service provider should have minimum net free foreign exchange earnings of US$15,000 in year of rendering service. For Individual Service Providers and sole proprietorship, such minimum net free foreign exchange earnings criteria would be US$10,000 in year of rendering service |

Note that benefits under MEIS shall not be available for exports made with effect from 01.01.2021. There will be a new scheme introduced by the Department of Commerce, Ministry of Finance called Remission of Duties and Taxes on Exported Products (RoDTEP) Scheme which will be notified soon and will be applicable for all export goods with effect from 01.01.2021. For the services rendered w.e.f. 1st April, 2020, decision on continuation of the SEIS scheme will be taken subsequently and notified.

Duty Exemption Scheme

This scheme enables duty free import of inputs for export production and consist of following,

- Advance Authorization (AA)

- Duty Free Import Authorization (DFIA)

| Description | Advance Authorization | Duty Free Import Authorization |

| Objective | Issued to allow duty free import of input which is physically used in the export goods | Issued to allow only Basic Custom Duty free authorization for import of inputs |

| Basis |

|

Only as per SION |

| Eligibility |

|

|

| Minimum Value Addition requirement | 15% to be achieved | 20% to be achieved |

| Actual user conditions | Yes | No |

| Duties covered | Basic Customs Duty, Additional Customs Duty, Education Cess, Anti-dumping Duty, Countervailing Duty, Safeguard Duty, Transition Product Specific Safeguard Duty, Excise Duty, IGST | Only Basic Custom Duty |

Duty Remission Scheme- Duty Drawback Scheme (DBK)

Duty drawback scheme is administered by Department of Revenue (DoR) and is governed by Customs and Central Excise Duties Drawback Rules, 2017 and various notification issued time to time.

As per the Notification No. 07/2020-CUSTOMS (N.T.) dated 28th January, 2020, the Central Government determines the rates of drawback as per the schedule given along with the notification subject to the conditions as mentioned therein. The rate of Duty Drawback varies depending upon the items as mentioned in the Custom Tariff Act.

EPCG Scheme

EPCG scheme is to facilitate the import of Capital Goods like Machinery etc. for production of quality products.

| Description | EPCG Scheme |

| Objective | It allows the import of Capital Goods at zero custom duty for pre-production, production and post production and capital goods imported for physical export are also exempt from IGST [till 30.09.2021] |

| Goods Covered |

Import of Capital goods for Project imports |

| Export obligation | 6 times of duties, taxes and cess saved on capital goods, to be fulfilled in 6 years from the date of issue of authorisation. For indigenous resourcing it will 25% less than this |

| Validity | Authorization shall be valid for import for 18 months |

| Eligible persons |

|

| Actual user condition | Yes |

*****

A bout the Author : Author is Ruchika Bhagat, FCA working as Manager Taxation in Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India. She is also the Managing Director of Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm established in the year 1997 with its head office at New Delhi. She specializes in Business Advisory, Tax, Regulatory and Risk Advisory. She is a strategic adviser in setting up businesses in India for foreign companies and taking care of its compliances.

bout the Author : Author is Ruchika Bhagat, FCA working as Manager Taxation in Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India. She is also the Managing Director of Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm established in the year 1997 with its head office at New Delhi. She specializes in Business Advisory, Tax, Regulatory and Risk Advisory. She is a strategic adviser in setting up businesses in India for foreign companies and taking care of its compliances.