Important Aspects from RTI reply received from CBIC- Rs 900 Crores collected as GST Late Fees

GST was launched on 1st July 2017 and termed as biggest tax reform in India after independence. Certain initial hiccups were expected in the implementation considering the mammoth data integration as GST has subsumed within itself 16 different taxes. The Migration of existing taxpayers registered under Central Excise and Service Tax was started from 7th January 2017 on GSTN. Thus effectively the common portal of GST is in use for nearly 16 months now.

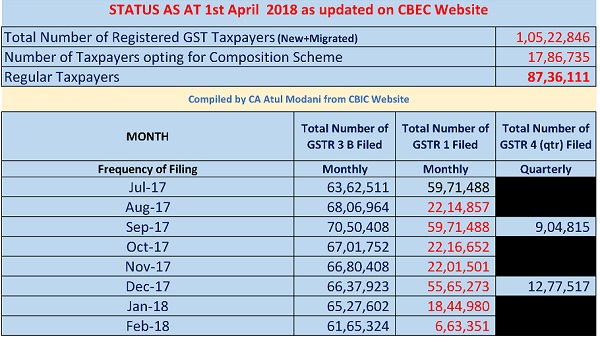

Following is the analysis of Return filing of GSTR 3 B, 1 and 4 available on CBIC website under the head GST – Concept & Status (01-04-2018).

The above analysis is self-explanatory. Even Govt have sounded alert on low compliance ratios consistently. There were many occasions when the Portal was crashed and thrown glitches. Even High Courts have accepted the fact of glitches in many cases.

The basic features of the return mechanism in GST includes electronic filing of returns, uploading of invoice level information, auto-population of information relating to input tax credit from returns of supplier to that of recipient, invoice level information matching and auto-reversal of input tax credit in case of mismatch. The returns mechanism is designed to assist the taxpayer to file returns and avail ITC.

Under GST, a regular taxpayer needs to furnish monthly returns and one annual return. The GST Council has however recommended to ease the compliance requirements for small tax payers by allowing taxpayers with annual aggregate turnover up to Rs. 1.5 Crore to file details of outward supplies in FORM GSTR-1 on a quarterly basis and on monthly basis by taxpayers with annual aggregate turnover greater than Rs. 1.5 Crore. Further, GST Council has recommended to postpone the date of filing of Forms GSTR-2 and GSTR-3 for all normal tax payers, irrespective of turnover, till further announcements are made in this regard.

Revision of Returns: The mechanism of filing of revised returns for any correction of errors/ omissions has been done away with under GST. The rectification of errors/omissions is allowed in the return for subsequent period (s). The continuous change in mechanism of return filing by GSTN also ensured that in case of errors in data punching, the taxpayer will get stuck up and will not be able to file the return for current as well as subsequent period because unless the earlier return is filed portal did not allow to file subsequent month’s return. Further unless and until tax and late fees is paid, the return does not get uploaded and thus got the cycle of return filing to a standstill. The clarifications regarding stuck up of Return filing and consequent Amendment / corrections / rectification of errors were also made by CBEC (Now CBIC) vide Circular No. 26/26/2017-GST dated 29th December 2017.

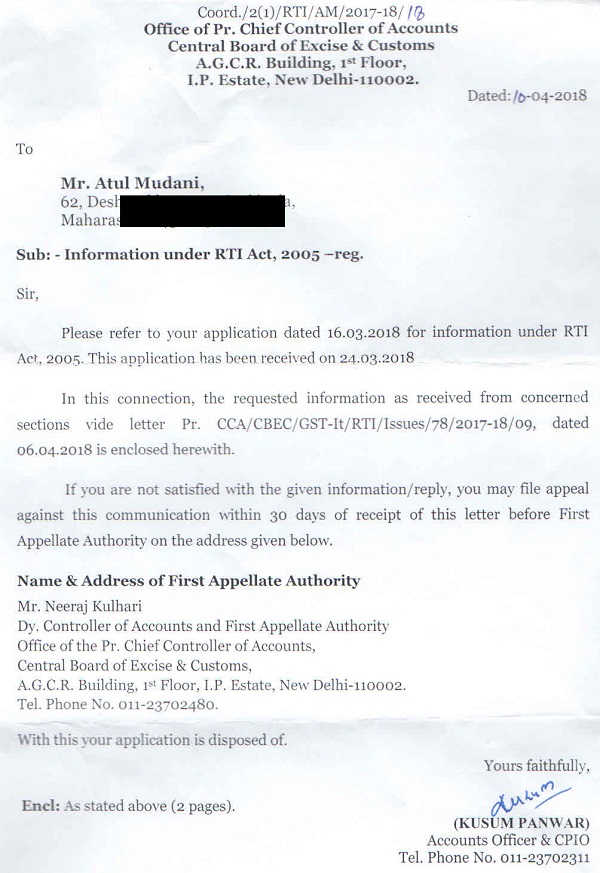

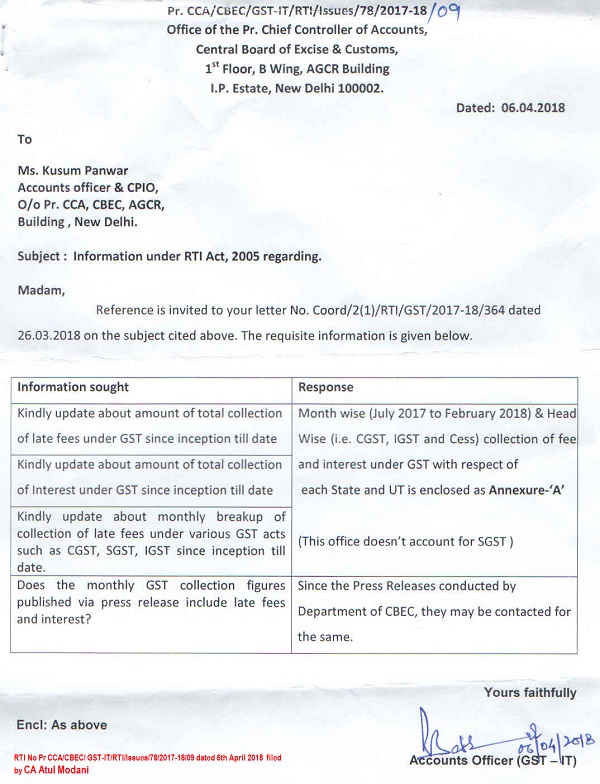

To get further insight into this aspect, I have lodged an RTI with respect to collection of Late Fees and Interest on account of GST return filing so as to co-relate with the process of GST Return filing in vogue. I have received following communication from Principal Chief Controller of Account, Central Board of Excise & Customs with respect to same.

Interest on Late GST Payment:

An interest of 18 percent is levied on the late payment of taxes under the GST regime. The interest would be levied for the days for which tax was not paid after the due date.

Penalty (Late Fees) for non-filing of GST Returns:

In case a taxpayer does not file his/her return within the due dates, he/she shall have to pay a late fee of Rs. 200/- i.e. Rs.100/- for CGST and Rs.100/- for SGST per day (up to a maximum of Rs. 5,000/-) from the due date to the date when the returns are actually filed.

Note: In case of GSTR-3B,

- For the months July to September, 2017, the late fee payable for failure to furnish the return has been waived completely.

- From the month of October 2017 onwards, the GST Council has recommended that the amount of late fee payable by a taxpayer whose tax liability for that month is ‘NIL’ is Rs. 20/- per day (Rs. 10/- per day each under CGST & SGST Acts). However, if the tax liability for that month is not ‘NIL’, the amount of late fee is Rs 50/- per day (Rs. 25/- per day each under CGST & SGST Acts)

Following initial observations can be drawn from the above RTI Reply received

1) The Office have written SGST is not accounted by them and hence Information with Regards to Late fees and Interest collection under SGST is not available in the Annexure.

2) However as the GST return is combined return under all the acts it can very well be assumed that the Late fees under SGST will be equal to CGST as both are to be paid as per relevant section. However the same is not correct as far as Interest is concerned because it depends upon the liability under particular act.

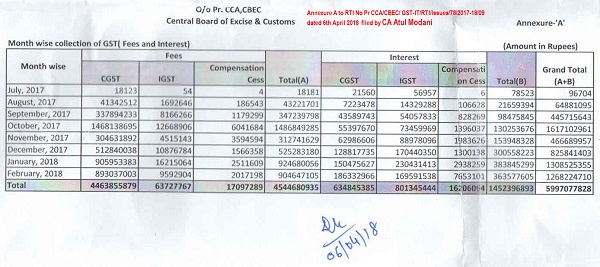

3) Thus following is the summary of collection of Late Fee and Interest for 8 month period July 2017 to February 2018.

| (RS In Crores) | |||

| ACT | Late Fees | Interest | Total |

| CGST | 446.39 | 63.48 | 509.87 |

| SGST (Assumed as above as per Act and Return filing Process) | 446.39 | NA | NA |

| IGST | 6.37 | 80.13 | 86.5 |

| Compensation Cess | 1.71 | 1.62 | 3.33 |

| Total | 900.86 | 145.23 | |

If we consider interest under SGST as equal to or more than SGST, still it is clear that the amount of collection of Late Fees under GST is 4.5 times more than the amount of interest from taxpayers. This clearly shows that Taxpayers had initiation to pay tax and comply the provisions of law but the technical glitches held them back from fulfilling their duty of filing the return.

The continued problems faced by exporters to get refund and special drive to give those refund of exporters (lastly done by physical mode in end of March 2018) also justifies the many lacunae in the GSTN system that needs to be addressed on priority so that the system becomes seamless and taxpayer don’t have to bear the burnt in the form of Late Fees. The Industry faced the menace of working capital blockage and non-payment of interest as per provisions of Act.

Hope the above Information in RTI is useful for the fraternity, businesses, Industries and to govt also to take up the matter of further simplification of GST Return filing process so that the unnecessary non- compliance, late fees burden are taken care of.

The Author is a Practicing Chartered Accountant and regular contributor of taxation articles and other legal updates on various social media platforms.

Late fee amount can’t not surpass to tax liability for particular month this amendment needed under the GST act for making trade friendly law and encourage gst compliance government can not treat corporate and unorganized sector in same way

Late fee for particular return can not exceed from tax liability for that particular month this correction if made in Act that’s give relief to traders and encourage compliance under the gst

Government should treat their people like it’s children

Govt can slightly beat like a father certainly they must not break their legs as gst late fee. It is very high ordinary people cAnnot bear this burden .govt must refund the paid late fee since their program not allows us subsequent filing if a single month late fee is not pAid. Then the result is enormous late fee which breaks our heart why the hell we should do businessgovt must return gst late fee and cAncel it

Why the PIL is not filed against the late fees levy as this is the first year of gst, and there are many reasons due to which returns could not be filed.

I hope Government is interested in collecting GST Late fees instead of getting interest in collection of Taxes through SGST/CGST and IGST. Small businessman who doesn’t aware of computers skill and they relay on accountants and consultants. Who makes delays in filing returns due to pre-occupied schedules, unnecessary businessman have to bear Late fees in spite of paying taxes in time. Previously 45 days were provided to file single returns, now its very short days are provided to file both returns GST 1 and GST 3B. So please look into the matter.

When late fee is waived of for the period from July to September why the figures furnished by RTI is showing late fee for the months of July, Aug and Septmber

It seems that this government is interested in late fees rather than taxes. why demand late fees when you have no roadmap to implement GST and no way to solve glitches of the GST website. i pity those persons who have drafted the law. They suggested Rs. 50 late fee for tax payers who have Rs. 5 tax payable and for those also who have Rs. 5 lacs tax payable. This is ridiculous.

I also find intentions of these government is malafide. The persons sitting on highest chairs have no knowledge of any business and have no idea how business runs on ground level.

In the initial year, they should have granted at least 45 days to file returns. But as I say when intention is not bonafide nothing can go in right.

Same was the case of demonetization. Their intention itself was not bonafide. If their intention was bonafine, they should not have printed Rs.2000/- notes.

why we do not rise our voice again This to much per late fees structure and penalty interest because of we all are almost higher Tax pay b/f our end user b/f collect and pay to our government,,,as i thought This GST system is killed small business men lief ,,,,Then i oppose ..late fess per day wise and also on interest system ….

its a very good job sir this is not Digital India this is called made by the govt for its own sake. Govt has no interest of normal people. We are cutputali (dolls) in the eyes of govt. However govt has to relaxed this new regime for initial 31st march 2018 so that people can understand this gst process and well known about this. Server issue is not govt it is our fault that we are living in this digital India initial server was closed from at night up to 3:30 am and hence there is no chance for correction first software in this world. How people will encourage to use this software how they will pay taxes in time.There is no sunwai (provision) on behalf of taxpayer.

Really commendable job, getting this information out by RTI. Trade & Industry collecting taxes on behalf of the government like ‘bandhua majdoor’ and then paying penalties for glitches in GSTN for no fault on their part.’ Achchee din’.

Sushil Sureka,

General Secretary, Ahilya Chamber, Indore .

dear nayan

god bless u for selfless efforts and info to we all pl keep it up like NGO-A CONTRIBUTION TO SOCIETY

Can any one please tell me that GST is applicable for Real Sector ?? if it is applicable then how they will claim the output GST and from whom ??

Great Job sir.

In my view, late fees should also be in multiple of Rs.10/- or Rs.5/- (No odd figure)

(Rs.100/-, 50/-, 25/- or 20/-)

Can any one please tell me?

How the late fees under IGST & Compensation Cess will be the account for in the RTI reply?

Email Id:- canayanjain@rediffmail.com