Month: April 2026

1,943 articlesGoods and Services Tax

Goods and Services Tax

Inter-play between Input Tax Credit and IBC

Goods and Services Tax

Goods and Services Tax

Videography & advocate presence in GST summons allowed on humanitarian grounds

Finance

Finance

Incentives under Maharashtra Global Capability Centre (GCC) Policy 2025

Goods and Services Tax

Goods and Services Tax

End of Intermediary Conundrum: Omission of Section 13(8)(b) of IGST Act

Fema / RBI

Fema / RBI

RBI Monetary Policy April 2026 – Key Rates and Measures

Corporate Law

Corporate Law

Downstream Investments By FOCCS: Regulatory Challenges And Way Forward

Goods and Services Tax

Goods and Services Tax

Inter-State ITC Transfer under GST as going concern between distinct persons

CA, CS, CMA

CA, CS, CMA

Analysis of Notifications and Circulars for Week Ending 5th April 2026

Goods and Services Tax

Goods and Services Tax

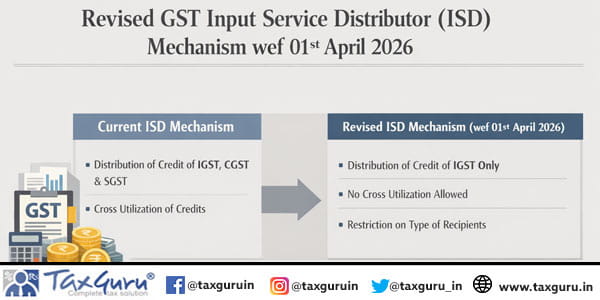

Revised GST Input Service Distributor (ISD) mechanism wef 01st April 2026

Goods and Services Tax

Goods and Services Tax