Month: January 2026

2,391 articlesIncome Tax

Income Tax

New Tax Regime Benefit Allowed Despite One-Day Delay in Form 10IE Filing: ITAT Surat

Goods and Services Tax

Goods and Services Tax

Ex Parte GST Adjudication Invalid for Failure to Grant Hearing: Allahabad HC

Custom Duty

Custom Duty

DRI power to issue SCN u/S.4 was upheld in recovery of drawback amount

Goods and Services Tax

Goods and Services Tax

Bail Denied Due to Alleged Large-Scale Fake ITC Through Bogus Firms

Income Tax

Income Tax

ITAT Mumbai Allows Professional Fees & Foreign Branch Expenses u/s 37(1) for Strategic Investments

Finance

Finance

Family Term Insurance: Understanding Lump Sum and Monthly Payout Options

Income Tax

Income Tax

SLP Filed Only to Get SC Stamp Dismissed Due to 426-Day Delay & Vague Explanation

Income Tax

Income Tax

Gujarat HC Quashed Reopening Due to Absence of Fresh Tangible Material

Income Tax

Income Tax

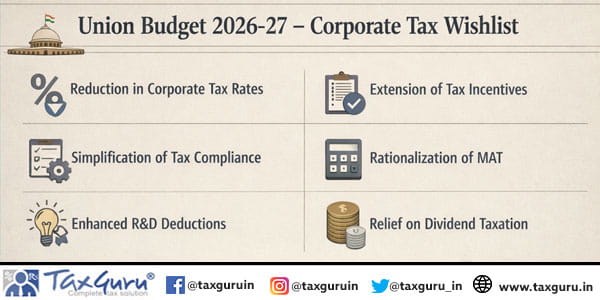

Union Budget 2026-27 – Corporate Tax Wishlist

Income Tax

Income Tax