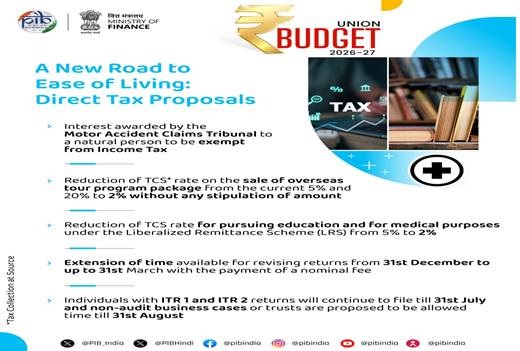

The Union Budget 2026–27 introduces a series of direct tax reforms aimed at improving ease of living and simplifying compliance, particularly for small and individual taxpayers. Presenting the proposals, Nirmala Sitharaman announced that any interest awarded by the Motor Accident Claims Tribunal to a natural person will be fully exempt from income tax, with no TDS requirement. TCS rates on overseas tour packages, education, and medical remittances under the Liberalised Remittance Scheme are reduced to 2 percent. To reduce procedural friction, manpower services are clearly brought within the contractor TDS framework, capped at 1 or 2 percent. The Budget proposes a rule-based automated system for granting lower or nil TDS certificates, extends the deadline for revising returns to 31 March with a nominal fee, and staggers return filing timelines. A one-time six-month foreign asset disclosure scheme is introduced for small taxpayers, offering immunity from penalty and prosecution on specified conditions.

Ministry of Finance

EASE OF LIVING BY DIRECT TAX REFORMS : UNION BUDGET 2026-2027

ANY INTEREST AWARDED BY THE MOTOR ACCIDENT CLAIMS TRIBUNAL TO A NATURAL PERSON TO BE EXEMPT FROM INCOME TAX

SCHEME FOR SMALL TAXPAYERS TO ENABLE OBTAINING A LOWER OR NIL DEDUCTION CERTIFICATE BY A RULE-BASED AUTOMATED PROCESS

TIME AVAILABLE FOR REVISING RETURNS EXTENDED FROM 31st DECEMBER TO 31st MARCH, FOR A NOMINAL FEE

ONE-TIME 6-MONTH FOREIGN ASSET DISCLOSURE SCHEME FOR SMALL TAXPAYERS TO DISCLOSE INCOME OR ASSETS

Posted On: 01 FEB 2026 12:52PM by PIB Delhi

A range of proposals on Direct Taxes to ensure ‘Ease of living’ for taxpayers have been announced by Union Minister for Finance and Corporate Affairs Smt. Nirmala Sitharaman during the Union Budget 2026-27 speech in Parliament today.

Ease of Living

The Budget proposes that any interest awarded by the Motor Accident Claims Tribunal to a natural person will be exempt from Income Tax, and any TDS on this account will be done away with. It proposes to reduce TCS rate on the sale of overseas tour program package from the current 5 percent and 20 percent to 2 percent without any stipulation of amount.

It aims to reduce TCS rate for pursuing education and for medical purposes under the Liberalized Remittance Scheme (LRS) from 5 percent to 2 percent. Supply of manpower services is proposed to be specifically brought within the ambit of payment to contractors for the purpose of TDS to avoid ambiguity. Thus, TDS on these services will be at the rate of either 1 percent or 2 percent only.

Ease for Taxpayers

A scheme for small taxpayers is proposed wherein a rule-based automated process will enable obtaining a lower or nil deduction certificate instead of filing an application with the assessing officer. For the ease of taxpayers holding securities in multiple companies, the budget proposes to enable depositories to accept Form 15G or Form 15H from the investor and provide it directly to various relevant companies. It extends time available for revising returns from 31st December to up to 31st March with the payment of a nominal fee.

Relaxed Tax return Timeline

The Budget proposes to stagger the timeline for filing of tax returns. Individuals with ITR 1 and ITR 2 returns will continue to file till 31st July and non-audit business cases or trusts are proposed to be allowed time till 31st August. TDS on the sale of immovable property by a non-resident is proposed to be deducted and deposited through resident buyer’s PAN based challan instead of requiring TAN.

Focus on Small Taxpayers

To address practical issues of small taxpayers like students, young professionals, tech employees, relocated NRIs, and such others, it aims to introduce a one-time 6-month foreign asset disclosure scheme for these taxpayers to disclose income or assets below a certain size. This scheme would be applicable for two categories of taxpayers namely, (A) who did not disclose their overseas income or asset and (B) who disclosed their overseas income and/or paid due tax, but could not declare the asset acquired.

For category (A), the limit of undisclosed income/asset is proposed to be up to 1 crore rupees. They need to pay 30 percent of Fair Market Value of asset or 30 percent of undisclosed income as tax and 30 percent as additional income tax in lieu of penalty and would thereby get immunity from prosecution. For category (B), asset value is proposed to be up to 5 crore rupees. Here, immunity from both penalty and prosecution will be available with the payment of fee of 1 lakh rupees.

****