Case Law Details

Lexus Paints And Coating Vs C.C.-Mundra (CESTAT Ahmedabad)

Introduction: In a case before the Customs, Excise, and Service Tax Appellate Tribunal (CESTAT) in Ahmedabad, the allegations of mis-declaration were challenged by the appellant. The CESTAT concluded that allegations of mis-declaration cannot be upheld without complete evidence and when there has been a violation of the principles of natural justice.

Background of the Case: The appellant in this case had filed two Shipping Bills for the export of Iron Oxide to Saudi Arabia. The appellant had classified the export product under Tariff Item 2821 1010. To determine the nature of the export product, samples were drawn from the consignment and sent to the Custom House Laboratory (CRCL) in Kandla.

The CRCL Test Reports: The CRCL’s test reports, dated December 4, 2015, and February 12, 2016, confirmed that the consignment consisted of Iron Oxide. The test results showed that the Iron Oxide content was about 68.4% and later 97.84%. The test reports were unambiguous in identifying the export product as “Iron Oxide.”

Allegations by the Department: However, the Department took a different view based on a report that questioned the classification. They alleged that the export consignment was not Iron Oxide but “Iron Ore,” classifiable under a different Customs Tariff Heading. Subsequently, a Show Cause Notice (SCN) was issued, alleging mis-declaration and demanding a 30% duty.

Lack of Specific Inquiry: The appellant contended that there was no specific inquiry during the statement recording regarding the manner in which undisclosed income was derived. They argued that Section 113(d) of the Customs Act, 1962, should not apply in this case.

CESTAT’s Decision: The CESTAT carefully examined the case and noted that the CRCL test reports were clear in identifying the export product as “Iron Oxide.” They also considered a report from the Joint Director CRCL which contradicted the earlier findings. However, the appellant had not been provided with this report, leading to a violation of the principles of natural justice.

Violation of Natural Justice: The CESTAT observed that the appellant was not provided with the Joint Director CRCL’s report that was relied upon to allege mis-declaration. Therefore, they found a gross violation of the principles of natural justice. They relied on the initial CRCL test reports, which stated that the export consignment was made of Iron Oxide, and concluded that charges of mis-declaration had not been established.

CESTAT’s Ruling: In light of the findings, the CESTAT ruled that the impugned order in original and the order in appeal were without merit. They set aside both orders, allowing the appeal.

Conclusion: The CESTAT’s decision in this case highlights the importance of adhering to principles of natural justice in legal proceedings. Allegations of mis-declaration, especially when based on conflicting evidence and incomplete disclosure to the appellant, cannot be upheld. It emphasizes the need for fairness and transparency in administrative and legal processes.

FULL TEXT OF THE CESTAT AHMEDABAD ORDER

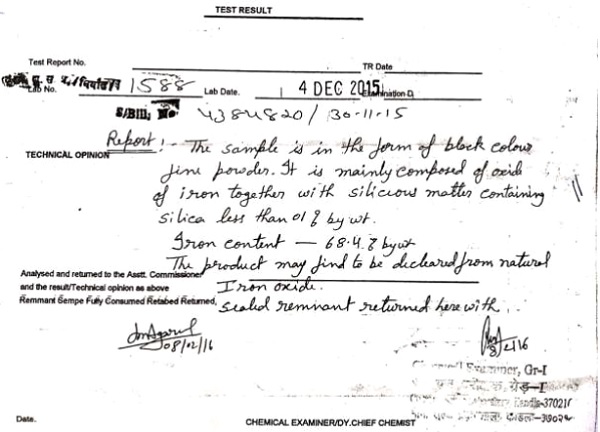

The brief facts of the case are that the appellants have filed two Shipping Bills No. 4384820 dated 30th November, 2015 and 4324962 dated 26th November, 2015 for export of Iron Oxide to Saudi Arabia. The appellants have classified their export product under Tariff Item 2821 1010. At the time of the clearance of export consignment, representative samples were drawn from the export consignment and sent to CRCL, Kandla for determining the nature of the export product, and to determine whether the export consignment pertains to Iron Oxide or “Iron Ore” classifiable under Customs Tariff Heading 2601 1119. The CRCL, Kandla vide its report No. 1588 dated 04th December, 2015 has reported as below:

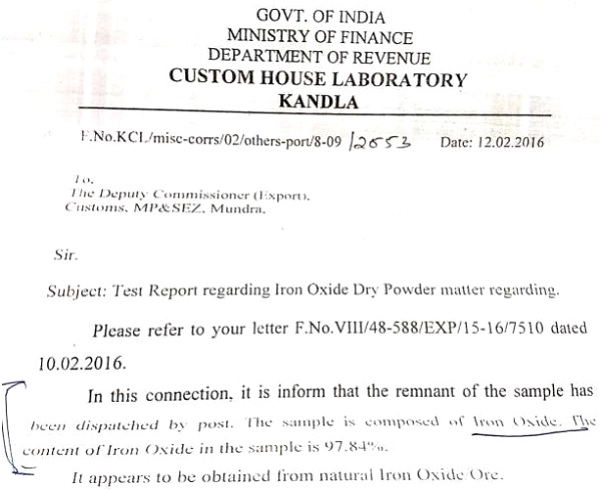

1.1 It can be seen from above test report that the test report holds that the consignment consist of Oxide of Iron, wherein the iron content are about 68.4% by weight. It further been mentioned with above test report that the product may find to be declared from “Natural Iron Oxide”. The Custom House Laboratory, Kandla vide its letter dated 26.02.2016, in response to a letter of Deputy Commissioner of Export Customs, Mundra dated 10.02.2016, has further reported as follows:

“In this connection, it is to inform that the remnant of the sample has been dispatched by post. The sample is composed of Iron Oxide. The content of Iron Oxide in the sample is 97.84%.”

2. The Department on the basis of first test report entertained view that the export consignment under above mentioned two shipping bills are not of the Iron Oxide Dry Powder, but of “Iron Ore’”, which is classifiable under Customs Tariff Heading 2601119, accordingly SCN dated 03.03.2016 alleging mis-declaration of the export consignment and demanding the duty @ of 30% was issued. The provisions of Section 113(d) of Customs Act, 1962 has also been invoked.

3. We have heard both the sides. We are of the view that the test report dated 14 December, 2015, and a clarification issued in the form of letter dated 02.2016, Wherein the remnant sample has been put for re-test and wherein the samples were found to be of Iron Oxide of 97.84%, hold without any ambiguity that the subject consignment pertains to ‘Iron Oxide’. The learned Advocate has drawn our attention to the impugned order-in-original dated 21 March, 2018, para 4.3, wherein a reference has been made to a letter of Joint Director CRCL having File No. KCL/Misc-Corrs/KDLMundra/01/08-09/173 dated 8th January, 2018, wherein following report has been quoted:

“Based on the (combined) Iron content of 68.4% reported by this Laboratory, it is confirmed that the samples u/r is Iron ore/ concentrate, as the (Combined) Iron content is less than 70%, this sample cannot be considered as, Iron Oxides and hydroxide, Earth colors”

3.1 It has been the contention of the Learned Advocate that this report of Joint Director CRCL on the basis of which the Learned Adjudicating Authority has decided that the export consignment under above mentioned two shipping bills have been mis-declared by the appellant, has never been provided to the appellant, and therefore, they have been gross violation of principle of natural justice.

3.2 After detailed perusal of the appeal papers, and the test reports, we feel that the both the test reports of the CRCL dated 04 December, 2015 as well as 12 February, 2016, which are reproduced below:

3.3 It can be seen from the above test report that the consignments consisted of Iron Oxide and the only evidence on the basis of which it has been held that the subject consignments are of Iron ore/ concentrate by the Adjudicating Authority is Joint Director CRCL’s letter dated 12.02.2016 which has neither been provided to the appellant nor that was existing at the time of issuing SCN. We don’t take the cognigence of the Joint Deputy CRCL’s letter as the Adjudicating Authority has failed to provide the same to the appellant and therefore has grossly violating the principals of natural justice following the principle of the natural justice. At the same time since the initially two reports clearly holds that export consignments are made of the Iron Oxide. We are of the opinion that charges of mis-declaration of description of subject consignments is not established.

3.4 In view of the above, we find that there is no mis-declaration in the export consignments, the classification of the export consignment under the CTH 2821 1010 of the Customs Tariff Act is based on facts and we do not find any mis-declaration in this case.

3.5 In view of the above findings, we hold that the impugned order in original and order in appeal are without any merit, and therefore, we set aside the same.

4. The appeal is accordingly allowed.

(Pronounced in the open Court on 04.10.2023)