No Mens Rea, No Misconduct: ICAI Clears CA in Alleged Bribery Trap Case

The ICAI Board of Discipline cleared CA of professional misconduct in a case arising from an alleged CBI trap involving bribery linked to an Income Tax Officer. The allegation was that the CA acted as an intermediary to receive illegal gratification for release of seized FDRs (₹7 crore).

However, after examining witness testimony, call transcripts, and surrounding circumstances, the Board found no evidence of knowledge (mens rea) or conscious involvement of the Respondent. It noted that the CA was not named in the FIR initially, and even during proceedings, no demand or acceptance of bribe by him was established.

Crucially, the call recordings and transcripts showed that the money was meant for the Income Tax Officer and that the Respondent repeatedly refused to accept the packet and asked that it be handed over directly to the officer. The Board held that mere physical handling of money, without knowledge of its nature or purpose, does not constitute misconduct.

The Board emphasized that disciplinary proceedings require proof on the preponderance of probabilities, and in the absence of intent and knowledge, the charge fails. Accordingly, the Respondent was held “Not Guilty”, and proceedings were closed, with clarification that the finding is limited to disciplinary jurisdiction.

BOARD OF DISCIPLINE

(Constituted under Section 21A of the Chartered Accountants Act 1949)

FINDINGS OF THE BOARD OF DISCIPLINE UNDER RULE 14 (9) READ WITH RULE 15(2) OF THE CHARTERED ACCOUNTANTS (PROCEDURE OF INVESTIGATIONS OF PROFESSIONAL AND OTHER MISCONDUCT AND CONDUCT OF CASES) RULES, 2007

File No: PR/G/191/2019/DD/92/2021/BOD/788/2025

CORAM: (PRESENT IN PERSON)

CA.Rajendra Kumar P, Presiding Officer

Ms. Dolly Chakrabarty, Government Nominee

IN THE MATTER OF:

Superintendent of Police & Head of Branch

CBI, ACB, …. Complainant

Versus

CA. Samrat Chandra

M/s. Samrat Chandra & Associates ……… Respondent

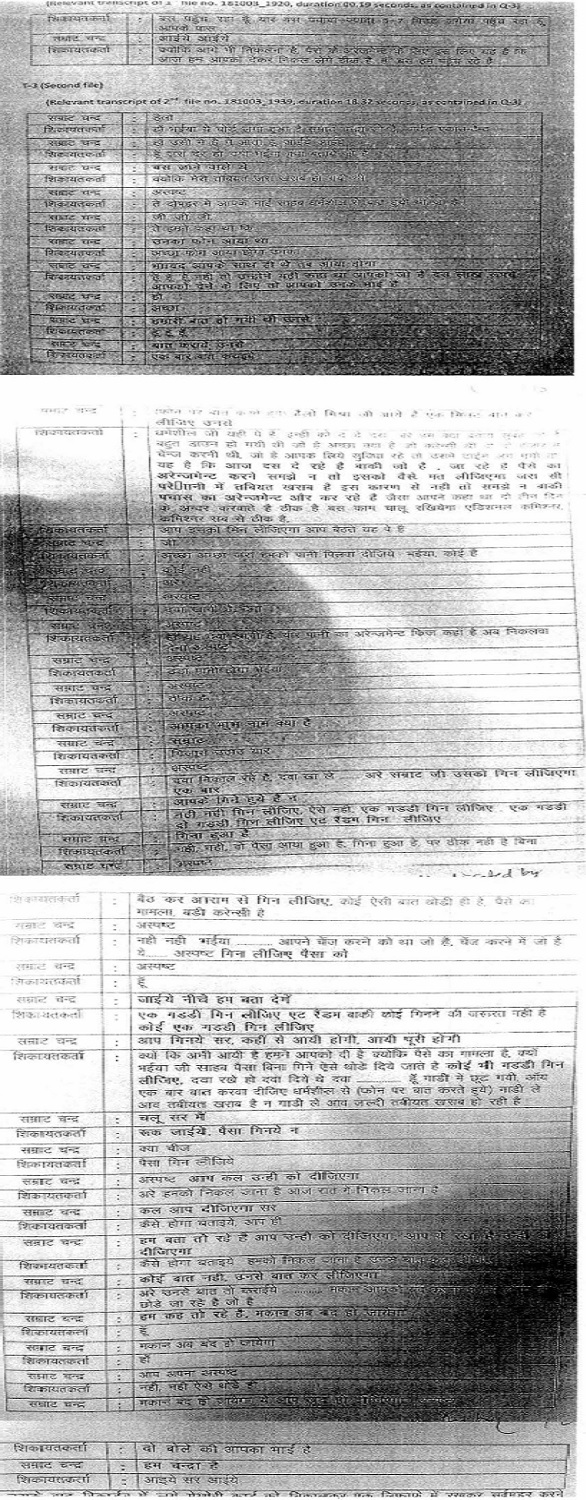

Date of Final Hearing 16th January 2026

Place of Final Hearing ICAI Bhawan, Lucknow

PARTY PRESENT (IN PERSON):

Counsel for Complainant; Shri. Pinkeshwar Gangwar, Public Prosecutor, (Representative of Complainant Dept.)

Counsel for Respondent: Shri. Ritwick Rai, Advocate

Respondent: CA. Samrat Chadha

Witness : Shri. Dharamshel Agarwal, Income Tax Inspector

FINDINGS:

BACKGROUND OF THE CASE:

1. The instant matter pertains to allegations of corruption involving an Income Tax Officer and officials of M/s Jedy Tapes Private Limited (JTPL). JTPL had acted as a guarantor for a loan availed by Shyam Vanaspati Oils Limited, Kolkata, from the State Bank of Hyderabad, Sapru Marg, Lucknow. In connection with this guarantee, JTPL had deposited approximately Rs. 7 crores in fixed deposits with the said bank. In the year 2009, the Income Tax Department, Lucknow Division, conducted raids at the premises of Shyam Vanaspati Oils Limited in both Kolkata and Lucknow. During the investigation, the Income Tax Department allegedly seized the fixed deposits worth Rs. 7 crores belonging to JTPL.

2. Subsequently, JTPL received an income tax notice, following which Shri Pratyoosh Kumar Mishra (PKM), the authorized representative of JTPL, approached Shri Dharamsheel Agarwal, Inspector, Income Tax Department, Central Circle, Lucknow, regarding the matter. It is alleged that the said Income Tax Officer demanded a bribe of Rs. 60 lakhs from PKM for settling the income tax issues. Based on this alleged demand, a written complaint was filed by PKM on 03rd October 2018, leading to the registration of a criminal case by the Central Bureau of Investigation (CBI) on the same date.

3. Following the registration of the case, trap proceedings were initiated by the CBI. During these proceedings and acting on the clear instructions of the Income Tax Officer, PKM handed over the bribe amount to the Respondent. The Respondent was subsequently arrested by the CBI during the trap operation. However, he was later granted bail by the court, subject to the condition that he would remain present before the trial court as required.

4. Upon completion of the investigation, a charge sheet dated 03rd October 2018, was filed before the Court of Special Judge, Anti-Corruption (West), Lucknow, against the Income Tax Officer and the Respondent. The accused have been charged under Section 120B read with Section 7 and 7A of the Prevention of Corruption Act, 1988, for criminal conspiracy and bribery.

5. The Director (Discipline), vide his Prima Facie Opinion bearing reference No. PR / G / 191 /2019/DD/92/2021 dated 25th November 2024, held the Respondent Not Guilty in respect of the allegations made in the present complaint. However, the Board, in its 332nd Meeting held on 17th January 2025, did not concur with the reasoning and conclusions arrived at by the Director (Discipline).

6. Upon consideration of the Prima Facie Opinion of the Director (Discipline) and after examining documents on record as well as the allegations levelled against the Respondent, the Board formed the view that further inquiry into the conduct of the Respondent is warranted. In this regard, the Board noted that, at one instance, the Respondent, in his Written Statement dated 20th May 2021, had stated that he did not know Shri Pratyoosh Kumar Mishra (PKM). However, at another instance, the Respondent stated that although he had initially not taken the packet, Shri Pratyoosh Kumar Mishra had insisted upon him to take it, and that he thereafter left the packet on a two-seater.

7. In view of the aforesaid apparent inconsistency in the Respondent’s statements, the Board, did not concur with the opinion of the Director (Discipline) holding the Respondent to be Not Guilty of Other Misconduct falling within the meaning of Item (2) of Part IV of the First Schedule to the Chartered Accountants Act, 1949 and decided to hear the parties in the matter.

CHARGE ALLEGED:

8. The Respondent in connivance with the Income Tax Officer agreed to accept illegal gratification of Rs. 10 lakhs from PKM on behalf of the Income Tax Officer in the matter of release of the FDRs seized by the Income Tax Department, Lucknow. As per the Complainant, the aforesaid misconduct falls within the meaning of Item (2) of Part IV of the First Schedule to the Chartered Accountants Act, 1949.

BRIEF OF PROCEEDINGS HELD:

9. The details of the hearings fixed and held in the instant matter are given as below:

| S. No. | Date of Hearing | Status of hearing |

| 1. | 01St September 2025 | Part Heard and Adjourned. |

| 2. | 16th January 2026 | Matter Heard and Concluded. |

SUBMISSION OF THE PARTIES:

10. The Respondent vide email dated 28th August 2025, submitted that a complaint dated 20 January 2021 had been filed against him by Shri S. K. Khare, the then Superintendent of Police and Head of Branch, CBI, ACB, Lucknow, pursuant to which disciplinary proceedings had been initiated under Section 21 of the Chartered Accountants Act, 1949. He further submitted that the Director (Discipline), after having conducted a detailed inquiry and having duly considered the statements of witnesses, documents on record, and the submissions of both parties, had rendered a Prima Facie Opinion dated 25th November 2024, holding that the allegations made in the complaint had not been proved and that the Respondent had not been guilty of other misconduct falling within the meaning of Item (2) of Part IV of the First Schedule to the Act.

11. The Respondent submitted that, in the criminal case investigated and prosecuted by the CBI, it had never been alleged that he had been in connivance with Shri Dharamsheel Agarwal or that he had possessed any prior knowledge of the alleged transaction. He submitted that, contrary to this consistent position in the criminal proceedings, the disciplinary complaint had sought to attribute connivance to him, thereby revealing a clear inconsistency in the stand of the complainant authorities. He further submitted that the alleged aggrieved person, Shri Pratyoosh Kumar Mishra, had never made any allegation against him, and that the complaint had been pursued solely by CBI officials despite the absence of any direct accusation.

12. The Respondent submitted that the FIR registered by the CBI had not named him as an accused and that even during the verification process, no incriminating material or conduct had been found against him. He submitted that the prosecution witnesses examined before the Trial Court had consistently deposed that there had been no demand or acceptance of any illegal gratification by him and that he had repeatedly refused to accept the packet and had directed the complainant to hand it over directly to Shri Dharamsheel Agarwal. He further submitted that the evidence on record had clearly established that he had no prior knowledge of the contents of the packet or the nature of the alleged transaction.

13. The Respondent submitted that even the Hon’ble High Court, while granting him bail, had recorded a specific observation that the transcription did not indicate any mens rea on his part. He submitted that knowledge and intent being essential ingredients of the alleged misconduct, the absence of both had rendered the allegations wholly unsustainable. He further submitted that his conduct throughout the incident had been consistent with innocence and professional propriety.

14. The Respondent submitted that he had enjoyed an unblemished professional career of more than a decade and had maintained an impeccable reputation in the Chartered Accountancy profession. He submitted that, considering the absence of any evidence against him and the well-reasoned Prima Facie Opinion of the Director (Discipline), the disciplinary proceedings deserved to be dropped and he should be declared not guilty in accordance with law.

OBSERVATIONS OF THE BOARD:

15. The Board carefully considered the complaint, the submission made by the Respondent, the Prima Facie Opinion of the Director (Discipline) and oral arguments advanced by the parties during the hearing, including witness testimonies. The Board also examined the evidence led during the proceedings held on 16th January 2026, wherein the Respondent, his counsel, the Complainant’s representative, and the witness, Shri Dharamsheel Agarwal, were present and heard at length.

16. The Board noted that the central issue for determination was whether the Respondent had any knowledge of the contents of the packet allegedly handed over to him and whether his conduct demonstrated any deliberate or conscious involvement in the alleged bribery transaction. The Board observed that the criminal case arising out of the same incident is still pending trial before the competent court and that the Respondent was not named in the FIR at the initial stage but was subsequently arrayed as an accused in the charge-sheet. The Board further noted that the Respondent had been granted bail and that the criminal proceedings were at the stage of trial, with no finding of guilt recorded against him.

17. During the hearing, the witness, Shri Dharamsheel Agarwal, was examined by the Board. While certain inconsistencies were noted in his deposition, it clearly emerged that the witness denied having made any demand through the Respondent and stated that there was no discussion with the Respondent regarding money on the relevant date. The Board also took note of the submissions of the Complainant’s representative that voice recordings and transcripts existed indicating conversations between the witness and the complainant. However, the Board observed that even as per the transcripts placed on record, there was no material to conclusively establish that the Respondent was aware that the packet contained money or that he had agreed to receive any illegal gratification.

18. Further, the transcript of the call recordings indicates that the money was for the Income Tax Officer, and it was PKM who insisted the Respondent to count the same. Therefore, mere receiving the money for other persons without knowing the intention / purpose and counting the money on insisting of other persons does not establish mens rea on the part of the Respondent. The relevant portion of transcription of call recording were as under:-

19. The Board observed that the transcripts and oral evidence consistently indicated that once the Respondent realized that the packet, contained money, he repeatedly refused to accept it and directed the Complainant to hand it over directly to Shri Dharamsheel Agarwal. The Respondent’s conduct, as reflected from the contemporaneous recordings and witness testimonies, did not suggest any demand, acceptance, or conscious facilitation of illegal gratification. The mere physical handling of the packet, without proof of prior knowledge or mens rea, was found insufficient to establish misconduct.

20. In view of the above facts and circumstances and considering that disciplinary proceedings require proof based on preponderance of probabilities, the Board was of the considered opinion that the essential element of knowledge and intent on the part of the Respondent had not been established. Accordingly, the Board was of the view that mere receipt of a packet at the Respondent’s professional premises, in the absence of evidence showing conscious or deliberate involvement, did not amount to “Other Misconduct” under Item (2) of Part IV of the First Schedule to the Chartered Accountants Act, 1949.

21. The Board, therefore, held that the Respondent is Not Guilty of the charge of Other Misconduct falling within the meaning of Item (2) of Part IV of the First Schedule to the Chartered Accountants Act, 1949. It was further clarified by the Board that the decision in this matter is confined strictly to the disciplinary proceedings before the Board and the Institute of Chartered Accountants of India and shall not be relied upon or used by either party in any other proceedings before any court or authority. Accordingly, the proceedings stood concluded.

CONCLUSION:

22. Thus, in conclusion, in the considered opinion of the Board, the Respondent is ‘Not Guilty’ of Other Misconduct falling within the meaning of Item (2) of Part IV of the First Schedule to the Chartered Accountants Act, 1949. Accordingly, the Board passed an Order for closure of the case in terms of the provisions of Rule 15 (2) of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007.

23. Ordered Accordingly. The Case stands disposed of.