The study on Resolution Professionals (RPs), conducted by the Management Development Institute with support from the Insolvency and Bankruptcy Board of India, examines the role, effectiveness, and challenges faced by RPs within the framework of the Insolvency and Bankruptcy Code (IBC), 2016. The IBC was introduced to establish a time-bound and value-maximizing insolvency resolution mechanism, aimed at improving corporate governance, preserving business continuity, and strengthening the credit system. Within this framework, RPs serve as a central pillar, responsible for managing the Corporate Insolvency Resolution Process (CIRP) from initiation to resolution or liquidation.

The study adopts a mixed-method approach, combining secondary data analysis with surveys and interviews of Resolution Professionals. It evaluates multiple dimensions of RP functioning, including appointment processes, conflict of interest safeguards, operational management of distressed firms, facilitation of resolution plans, valuation processes, fairness in conducting CIRP, fraud detection capabilities, and stakeholder protection.

The findings indicate that the appointment and eligibility of RPs are governed by clearly defined rules under the IBC and regulations issued by the Insolvency and Bankruptcy Board of India. Professionals must be registered insolvency professionals, possess requisite qualifications, and pass the Limited Insolvency Examination. They must also maintain independence from the corporate debtor to avoid conflicts of interest. The Committee of Creditors (CoC) plays a significant role in confirming or replacing the RP, ensuring creditor oversight in the process. While the current framework ensures competence and independence, the study identifies scope for improvement by incorporating professionals with diverse managerial and financial expertise and by adopting more practical, case-based examination formats.

The study highlights that RPs are required to manage the corporate debtor as a “going concern,” ensuring continuity of operations while preserving asset value. They assume control of the company’s management, including assets, records, and operations, and may appoint professionals, raise interim finance, and modify contracts as necessary. Evidence suggests that this approach has contributed to improved firm performance post-resolution, including increases in sales, asset base, capital expenditure, and market valuation. However, a key gap identified is the limited managerial expertise of RPs in handling large and complex enterprises. To address this, the study proposes a “Segregated Dual System in CIRP” for large cases (above ₹1,000 crores), wherein Insolvency Professional Entities (IPEs) oversee the resolution process, while specialized entities or Special Purpose Vehicles (SPVs) manage day-to-day operations. This separation is intended to enhance efficiency and reduce value erosion.

In facilitating resolution plans, RPs are responsible for verifying claims, maintaining creditor records, and ensuring compliance with statutory requirements. They examine resolution plans to ensure conformity with the Code but do not evaluate their commercial viability, which remains the domain of the CoC. The study suggests that RPs could be given greater authority to provide detailed analysis of resolution plans, thereby strengthening the decision-making process. Timely verification of claims and use of technology or artificial intelligence are identified as areas that could improve efficiency.

The appointment of registered valuers is required to be conducted on an arm’s length basis through a transparent process. RPs must appoint two valuers within prescribed timelines to determine the fair and liquidation value of the corporate debtor. The qualifications, experience, and independence of valuers are critical to maintaining the integrity of the valuation process.

The conduct of CIRP by RPs is generally found to be fair and compliant with legal requirements. The process involves constitution of the CoC, convening meetings, inviting resolution applicants, evaluating plans, and submitting approved plans to the Adjudicating Authority. The RP plays a coordinating role among stakeholders, ensuring transparency and adherence to timelines. The study notes that RPs largely perform these functions effectively, though continuous monitoring and improved governance mechanisms can enhance accountability.

Despite the structured framework, several irregularities and challenges are identified. These include delays in public announcements, inadequate examination of financial affairs, delays in filing applications, ineffective management leading to value erosion, and failure to maintain a balance of stakeholder interests. To address these issues, the study recommends introducing performance guarantees or bonds for RPs. Such mechanisms would create accountability by linking performance with financial security and contractual obligations.

Fraud detection is identified as a critical responsibility of RPs. They are required to investigate potential fraudulent or wrongful trading and report such findings to the Adjudicating Authority. Effective fraud detection requires strong analytical skills, financial expertise, and the ability to conduct comprehensive examinations of corporate debtor transactions. The study emphasizes the need for a proactive approach and the use of forensic expertise where necessary.

In terms of stakeholder protection, RPs are tasked with balancing the interests of creditors, employees, and other stakeholders. Data indicates that a significant number of cases have been resolved or closed, with notable recovery rates for creditors. The study highlights that resolution plans have yielded substantial realizations compared to liquidation values, demonstrating the effectiveness of the CIRP framework. However, maintaining equilibrium among stakeholders remains a key responsibility, requiring transparency, communication, and fair decision-making.

The interview analysis supports the overall findings, indicating that RPs generally meet eligibility criteria and possess significant experience. Respondents emphasized the importance of stakeholder engagement, operational management, and transparent processes. They also highlighted challenges related to coordination with regulatory authorities and suggested improvements such as better technological integration, standardized dashboards, and enhanced evaluation mechanisms.

The study concludes that RPs play a crucial role in the success of the insolvency resolution framework. While the existing system has achieved significant outcomes, including improved resolution rates and value realization, there is a need for continuous improvement in areas such as expertise, process efficiency, governance, and accountability. Recommendations include enhancing eligibility criteria, adopting practical examination methods, implementing dual management structures for large cases, strengthening valuation processes, introducing performance guarantees, and leveraging technology for improved transparency and efficiency.

****

Insolvency and Bankruptcy Board of India

Press Release No. IBBI/PR/2026/6 08th April 2026

Research study on Resolution Professionals conducted by Management Development Institute, Gurgaon

The Management Development Institute, Gurgaon has undertaken a research study titled “Study on Resolution Professionals”. The study examines the role, responsibilities, and functioning of Resolution Professionals (RPs) within the Corporate Insolvency Resolution Process (CIRP) under the Insolvency and Bankruptcy Code, 2016 (IBC/Code).

2. The study recommends strengthening the insolvency ecosystem and enhancing the role of Insolvency Professionals (IPs). It proposes expanding eligibility to include professionals with managerial and financial expertise. For large CIRPs above ₹1,000 crore, it suggests a dual structure where IPs or IPEs handle resolution and compliance, while a specialised SPV manages operations. The study also recommends introducing a case-based examination system for IPs, similar to those in the US and UK. To safeguard the integrity of the process, it suggests that IPs found guilty of fraudulent conduct should be removed from all assignments, including ongoing cases. Further, the report recommends that Resolution Professionals provide a performance guarantee after their appointment, ensure the arm’s length appointment of valuers through an open and fair process, and undertake structured capacity-building and training programmes for IPs and IPEs.

3. The report provides valuable insights into the role and responsibilities of Resolution Professionals in India’s insolvency framework and offers recommendations to further strengthen the effectiveness, transparency, and efficiency of the CIRP under the IBC.

The full report is available on the website of the Insolvency and Bankruptcy Board of India at https://ibbi.gov.in/uploads/resources/bcfead24a4ac23bbf2a1bbaf4cd660dc.pdf.

*******

Management Development Institute

STUDY ON

RESOLUTION

PROFESSIONALS

March 2026

Professor Sandeep Goel

MANAGEMENT DEVELOPMENT INSTITUTE GURGAON

Executive Summary

The Insolvency and Bankruptcy Code (IBC) was passed in 2016 to improve the effectiveness of insolvency and bankruptcy procedures of Indian businesses. It has transformed India’s insolvency resolution landscape. In order to enable a time-bound and value-maximizing resolution process, it seeks to combine and modify the laws pertaining to insolvency and bankruptcy. In this regard, Resolution Professionals (RPs) play an important role throughout the resolution process.

The IBC’s role in maintaining the operational viability of financially distressed enterprises, protecting investments, and preserving jobs by concentrating on their revival and continuity is widely acknowledged. In fact, it goes beyond these immediate outcomes. It has a broader economic impact in terms of improving country’s credit system and quality of corporate governance. A multi-prolonged approach to examining the role of RPs is necessary in order to comprehend the impact of the resolution process and optimising troubled businesses in the interests of all stakeholders.

The study explores the role of the Resolution Professional, who is appointed in accordance with the rules and regulations set forth by the Insolvency and Bankruptcy Board of India for the Corporate Insolvency Resolution Process (CIRP) until the corporate debtor is either reorganized, reinstated, acquired by another corporate entity, or is liquidated. It examines whether the RPs perform their roles and responsibilities effectively and result in a successful outcome for the firms that emerged from the process. The results show that RPs play a crucial role in the CIRP mandated by the IBC. They are appointed to supervise the operations of a business undergoing CIRP in order to maximise asset value and reach a time-bound resolution. However, there is a need-based gap in their appointment, functionality, and process that needs to be improved for better management.

The report is divided into three parts. Part 1 provides the background, significance, objectives and methodology adopted for the study. Part 2 discusses the findings from the detailed qualitative descriptive analysis and analyzese the RPs modalities in regard to various objectives undertaken. It also discusses the findings of the survey and interviews for examining a practical insight into their functionalities about the possible impact on resolution process of the distressed units. Part 3 concludes the findings of the study and offer the required directions for future orientation.

Acknowledgements

I gratefully acknowledge the support provided by the Insolvency and Bankruptcy Board of India (IBBI) for conducting the study. I am thankful to Mr. Ravi Mittal, Chairperson, IBBI for the wholehearted cooperation during the course of this study. I would also like to express my gratitude to Dr. Bhushan Kumar Sinha, Whole-Time Director; Mr. Jithesh John, Executive Director; Mr. Ravinder Maini, Executive Director; Mr. Shiv Anant Shanker, Chief General Manager; Ms. Namisha Singh, Assistant General Manager; and Ms. Anjali Priya, Research Associate for providing the necessary support, resources and data-set for the completion of the study.

Abbreviations

AA – Adjudicating Authority

AFA – Authorisation for Assignment

AI – Artificial Intelligence

BLRC – Bankruptcy Law Reforms Committee

CD – Corporate Debtor

CIRP – Corporate Insolvency Resolution Process

CoC – Committee of Creditors

DRT – Debt Recovery Tribunal

IBBI – Insolvency and Bankruptcy Board of India

IBC – Insolvency and Bankruptcy Code

IM – Information Memorandum

IP – Insolvency Professional

IPs – Insolvency Professionals

IPA – Insolvency Professional Agency

IPE – Insolvency Professional Entity (Entities)

IRP – Interim Resolution Professional

IUs – Information Utilities

JIEB – Joint Insolvency Examination Board

NCLT – National Company Law Tribunal

QCBS – Quality and Cost-Based Selection

RA – Resolution Applicant

RFP – Request for Proposal

RP(s) – Resolution Professional(s)

SPV – Special Purpose Vehicle

1. Introduction

1.1 Background of the study

A time-bound, market mechanism for the reorganization and insolvency resolution of firms and individuals (businesses, limited liability partnerships, partnership and proprietorship firms, and individuals) in financial distress is provided by the Insolvency and Bankruptcy Code (IBC), 2016. To assist the stakeholders in managing their stress, the Code offers an ecosystem with four pillars. The first group of regulated individuals are insolvency professionals (IPs). The Bankruptcy Law Reforms Committee (BLRC), which conceptualised the Code, observed: “Insolvency professionals form a crucial pillar upon which rests the effective, timely functioning as well as credibility of the entire edifice of the insolvency and bankruptcy resolution process.”1 The Information Utilities (IUs) in the private sector make up the second pillar. They eliminate delays and disputes during the resolution process and store debtors’ financial information in an electronic database. The third is the adjudicating authority (AA), which includes their appellate tribunals and the National Company Law Tribunal (NCLT) in the case of corporate insolvency and the Debt Recovery Tribunal (DRT) in the case of individual insolvency. The regulator, the Insolvency and Bankruptcy Board of India (IBBI), is the fourth pillar. As a unique regulator, it regulates a profession as well as processes.

Resolution Professionals (RPs) are specialized positions within the Corporate Insolvency Resolution Process (CIRP). During the CIRP, the RP is in charge of overseeing the corporate debtor’s (CD) affairs, safeguarding its assets as an appointee of the creditors liaising with creditors, and assisting in the creation and execution of a resolution plan. Their main job is to develop a resolution plan that will either revitalize or liquidate the business while optimizing value for all parties involved.

In the backdrop of the significance of RPs in the entire resolution process, the present study is undertaken. They play an important role in the resolution of corporate debtor in a time bound manner for maximization of value of the assets, promoting entrepreneurship, facilitating the availability of credit, and balancing the interests of all the stakeholders.

1.2 Objectives of the study

Primarily, the study aims at examining the existing roles and responsibilities of Resolution Professionals (RPs), outlining the gaps in their modus-operandi, and suggesting potential areas of improvement for future orientation.

Specifically, it is expected to achieve the following objectives:

- To examine the appointment process of Resolution Professionals (RPs) with respect to eligibility and qualifications under the said Regulations.

- To check out for conflict of interest in the appointment of RPs, as above.

- To find out whether RPs manage the corporate debtor (CD) as a “going concern,” meaning they must maintain the company’s operations and preserve its assets during the insolvency process so that the company remains viable and attractive for potential resolution applicants.

- To determine do RPs facilitate the development of a viable resolution plan and collect, collate, and admit claims from creditors, and present these plans to the Committee of Creditors (CoC) for approval.

- To check if the appointment of registered valuers by RPs is arm’s length.

- To overview if RPs conduct the resolution process (CIRP) in a fair and just manner without any undue influence, regarding: (i) constitution of the CoC, (ii) convening its meeting, (iii) inviting prospective resolution applicants to submit a resolution plan, (iv) presenting to the COC, for its evaluation, and (v) submitting the resolution plan approved by CoC to AA.

- To explore options for curtailing irregularities by RPs by having the requirements of performance guarantees/bonds.

- To look into the capabilities of RPs for possible fraud detection in the CIRP

- Finally, to measure whether RPs are able to protect the interests of all stakeholders, including creditors, employees, and the company itself.

1.3 Significance of the study

In case of insolvency and resolution process, Resolution Professionals (RPs) have received considerable attention all over the world and although much has been said about them yet there is a requirement of detailed deliberation about them. The study would be a significant but a humble attempt to critically analyse their rationale to an organization in a sinking phase, exposing both its strengths and weaknesses.

It is hoped that the study will reveal to a large measure, the actual state of affairs of these RPs by tracing out various hazards undertaken by them. The conclusions drawn will provide a practical guidance for the management of these distressed corporations and initiate action for the improvement of quality of their earnings through the right guidance of RPs.

It increases the stakeholders’ understanding of the financial state of affairs of these corporations, and helps them in assessing their reliability when they consider investment opportunities. This will, arguably avoid erosion of value addition.

1.4 Research methodology of the study

The study adopted the following methodology to achieve the stated objectives, as outlined above.

First, a baseline was established “as is” with respect to information available at IBBI pertaining to RPs, their work-process, involved resolution processes, and concerned stakeholders. This was further evident by assessing and using secondary information from relevant laws and regulations, including the IBC Code, IBBI Regulations, Published Reports, and datasets. Thus, for the purpose of the present study, the main data used is secondary in nature, keeping in view its nature.

Second, the information was collected for further analysis through survey method with RPs to examine their process documentation and procedures followed over time. The questionnaire method was adopted, using a standardized set of questions to gather information from the respondents (RPs); administered online. Further, in-depth ‘focused interviews’ were conducted with select RPs for gathering qualitative data about how they perceive and understand the resolution process and mechanism. “These interviews are a very specific kind of discussion, directed by the researcher and employed for particular purposes” (Knott et al., 2022).

Thus, a mixed-method approach was used for disclosure analysis on secondary (published) and primary (experiential) data, focusing on arguments (from each key stakeholder), narration, description, and their exposition for future viability.

Additionally, the data analysis was well supported by various accounting and statistical techniques. Accounting techniques comprise of comparative statements analysis and trend analysis. Statistical tools include bar charts, pie charts and area charts to display the distribution of responses and identify the specific patterns and trends.

2. Conceptual overview, findings and discussion

2.1 Conceptual overview

Bankruptcy laws aim to address the coordination issues amongst the creditors by enforcing a state-provided law enforceable on all stakeholders (Schwartz, 1997). They require a process for resolving a company’s bankruptcy. Additionally, the bankruptcy process lessens the holdout issues brought on by conflicting stakeholder interests (Brown, 1989).

The Insolvency and Bankruptcy Code, 2016 (hereinafter referred to as “The Code”) is a code enacted by the Parliament in the Sixty-seventh year of the Republic of India on 28th May, 2016 with the purpose to consolidate and amend the laws relating to reorganization and insolvency resolution of corporate person, partnership firms and individuals in a time bound manner for maximization of value of the assets of such persons, to promote entrepreneurship, availability of credit and balance the interests of all the stakeholders including alteration in the order of priority of payment of government dues and to establish an Insolvency and Bankruptcy Board of India (IBBI) and for matters connected therewith or incidental thereto.2

The Indian scenario of insolvency before the Code was put into effect was a patchwork of unfitting parts. There were confusion and a lack of policy direction because insolvency was governed by a long list of statutes. Business failure and insolvency are unavoidable consequences of operating any kind of business, but the current system did not encourage a simple way to resolve insolvency. The code’s provisions introduced a centralized theme with a thorough rethinking on the process and mechanism.

The “Resolution Professional” as defined under the Code means a professional appointed to conduct the Corporate Insolvency Resolution Process (CIRP) and includes an interim resolution professional (IRP).3 The CIRP process is fully governed by the IBC. Any dispute pertaining to a default in debt payment by a company registered under the Companies Act, 1956 and the Companies Act, 2013 regarding financial, operational, or self-interested debtors is brought before the Adjudicating Authority (AA).

The Resolution Professionals (RPs) according to the Code is a key player in the CIRP. They play an essential role to the successful completion of the process covered by the code; their role is crucial to the CIRP’s quick process and timely assistance of those in need without causing harm to either the debtors or the creditors (Bhargava, 2024). Their role is to catalyse reorganization and insolvency resolution process in the interests of all stakeholders. Insolvency professionals (IPs) play a crucial role in managing distressed businesses and facilitating insolvency proceedings. It cannot be denied that role of the resolution professional is very important in the success or failure of the CIRP (Arora & Shrivastava, 2023).

However, RPs’ goal should be to have an optimal bankruptcy regime. An optimal bankruptcy regime is one which avoids taking/giving loans during financial crisis, provides a provision for entrepreneurship, and further provides for achieving a maximum total value for the distressed firm (Puchakayala & Veluchamy, 2023).

Undoubtedly, the entire resolution procedure conducted in accordance with the Code in India depends on insolvency and resolution professionals. Along with participating in the CIRP/liquidation process, they also fulfil their obligations as administrators, supervisors, or nominees in bankruptcy proceedings; facing numerous challenges in fulfilling these responsibilities.

2.2 Qualitative Descriptive analysis

A qualitative descriptive study is an important and appropriate design for research questions that are focused on gaining insights4 and making sense of the collected information. The present section makes use of descriptive analysis for examining the research objectives in detail. It involves organizing, summarizing, and analysing the information collected from various sources to describe themes and insights of the objective being studied and interpret findings effectively, and identifying the action points.

2.2.1 Appointment of Resolution Professionals (RPs)

1. The Insolvency and Bankruptcy Board of India is required to recommend the name of an Insolvency Professional (IP) on receiving reference from the National Company Law Tribunal and Debt Recovery Tribunal (Adjudicating Authority), in respect of the Corporate Insolvency or Individual Insolvency, as the case may be, for appointment as an Interim Resolution Professional (IRP), Resolution Professional (RP) under Sections 16(4), 34(6), 97(4), 98(3), of the “”5 Additionally, the Board can share a Panel of Insolvency Professional (IPs) with the Adjudicating Authority, who may be appointed as resolution professionals to prevent administrative delays in the IP appointment process.

2. The committee of creditors, may, in the first meeting (which shall be held within seven days of the constitution of the committee), by a majority vote of not less than sixty-six per cent of the voting share of the financial creditors, either resolve to appoint the interim resolution professional as a resolution professional or to replace the interim resolution professional by another resolution professional.6

(3) To be appointed as Resolution Professionals, a person must be an Insolvency Professional [Section 5 (27) of the Code], and fulfill the eligibility criterion as specified in the Regulations 4 & 5 of IBBI (Insolvency Professionals) Regulations, 2016. The Code prohibits any person from rendering his services as IP without being enrolled as a member of an IPA and registered with the IBBI. Thus, the IBBI acts the principal regulator of the insolvency profession, while the “Insolvency Professional Agencies” (IPAs) are frontline regulators.

Due to the specialized nature of insolvency and bankruptcy processes, it is essential for Insolvency & Resolution Professionals to possess specific domain expertise. Therefore, specialization is necessary for professionals in this field.

In ‘India’, prospective Insolvency Professionals (IPs) are required to successfully complete the IBBI’s ‘Limited Insolvency Examination’ to register. It is an online (computer-based and in a proctored environment) examination (duration 2 hours) with objective multiple-choice questions conducted by IBBI across India. This examination evaluates a professional’s comprehension of the challenges faced by distressed companies, with a special focus on a comprehensive understanding of the Insolvency and Bankruptcy Code (IBC). It is conducted to test the knowledge and practical skills of individuals in the areas of insolvency, bankruptcy and allied subjects.

Presently, individuals with a decade (ten years) of professional experience in the field of law, management, or graduates having 15 years of management experience must successfully complete an examination. After passing the exam, they must complete the pre-registration course offered by the “Insolvency Professional Agency” (IPA) within a year, after his enrolment as a professional member, and then apply to the IBBI to become registered as an Insolvency Professional (IP).

However, those without the requisite professional or managerial experience must meet the requirements of the IBBI’s Post Graduate Insolvency Program (PGIP), pass the Limited Insolvency Examination, and complete the remaining steps as applicable above.

(4) An insolvency professional shall be eligible 7 to be appointed as an interim resolution professional or a resolution professional, as the case may be, for a corporate insolvency resolution process of a corporate debtor if he, and all partners and directors of the insolvency professional entity of which he is a partner or director, are independent of the corporate debtor.

To be independent of the corporate debtor, if he:

(a) is eligible to be appointed as an independent director on the board of the corporate debtor under section 149 of the Companies Act, 2013, where the corporate debtor is a company;

(b) is not a related party of the corporate debtor; or

(c) is not an employee or proprietor or a partner.

5. An interim resolution professional or a resolution professional, as the case may be, shall make disclosures at the time of his appointment and thereafter in accordance with the Code of Conduct.

6. According to Chauhan & Pandey (2024), in contrast to nations like the UK, where separate licenses are required for personal and corporate insolvencies, each with its own evaluation criteria, this unified registration process as an IP in India under the Code eliminates the need for separate examinations or licenses/certificates to handle various types of insolvencies.

In the UK, the “Joint Insolvency Examination Board (JIEB) exams,” which comprise three exam papers, must be passed in order to become an IP. Similar to this, becoming an insolvency professional in the US usually entails fulfilling specific professional and educational requirements in addition to acquiring the necessary licenses or certifications.

However, exams in India by the IBBI are based on objective multiple-choice questions that emphasize the evaluation of theoretical knowledge; in contrast, exams in the UK and the USA though are open-book but involve case analysis. The multiple-choice questions, and not case studies-based examination format has a detrimental effect on the assessment of candidates’ situational ability in real-corporate world scenarios.

7. Further, RPs with adequate experience in similar industry and/or of handling similar projects will prove to be advantageous for the viability of CIRP. The number of years of this domain experience, as per the prescribed managerial experience for completing the Insolvency examination, can range from 10-15 years. This will help RPs to act not only as good administrators but also as efficient fiduciaries, coordinators, and compliance officers.

8. Insolvency Professionals (IPs) who have not undertaken any assignment or do not hold Authorisation for Assignment (AFA) during the past three years may be considered for removal.

It is evident, there are well-defined rules & regulations for eligibility and appointment of RPs under the Code and IBBI Regulations. The Code forbids anyone from providing IP services unless they are registered with the IBBI and enrolled as an IPA member. To register in India, aspiring insolvency professionals (IPs) must pass the “Limited Insolvency Examination” administered by the IBBI. Further, an IP should be independent of the corporate debtor.

However, there is always a room for improvement, such as professionals with diverse managerial background, in particular with financial proficiency can be appointed. That can be included as an eligibility criterion for their in-take. This will lead to the appointment of experienced managerial professionals with financial enrichment, and result in more effective resolution process. Further, like the US and the UK, the examination can be conducted in the “case” format for practical and applied interface.

Additionally, RPs with sufficient experience in related fields and/or managing related projects will be beneficial to CIRP’s sustainability.

2.2.2 Conflict of interest in the appointment of RPs

As per Regulation 3(1)8, for ensuring integrity, an interim resolution professional is appointed “independent from corporate debtor” as per the qualifications laid down in the given statute. Thus, in accordance with Regulation 3(3), “An interim resolution professional or a resolution professional, who is a director or a partner of an insolvency professional entity, shall not continue as the interim resolution professional or resolution professional, as the case may be, in a corporate insolvency resolution process.” This is subject to the insolvency professional entity or any other partner or director of such insolvency professional entity represents any other stakeholder in that process.

For representation of creditors in a class ascertained under sub-regulation (1) in the committee, the interim resolution professional shall identify three insolvency professionals who are-

a. not his relatives or related parties;

b. eligible to be resolution professional under regulation 3; and

c. willing to act as authorised representative of creditors in the class.9

With the aid of Section 14 under the Code (Kothari & Bansal, 2019) which provides a period of moratorium, the code ensures that there is a timeline for the procedure which has resolved the problems of delays and inefficiency. Practices such as misusing “related parties” and engaging in wrongful trading are punishable by severe penalties (Chatterjee et al., 2018).

According to The First Schedule of the (Insolvency Professionals) Regulations, 201610, the Resolution Professional should act independently, not be connected to or have any personal interest in the corporate debtor, and make decisions that benefit the corporate debtor rather than his own development or gain. The RP as a professional, being an outsider assigned to manage a business that is unrelated to him. He is subject to a salary as a professional, which is set in accordance with the code’s rules. The corporate debtor’s funds should not be used by RP for personal gain or to invite friends and family to obstruct the transparent process. The Resolution Professional are expected to operate impartially and independently; the CIRP process should be transparent and available for public review.

Thus, in accordance with IBBI Regulations, 2016, there is a provision of due consideration to avoid any conflict on interest in the appointment of IRP (RP). In order to maintain integrity, an IRP is appointed independent from corporate debtor and is well-identified with no involvement to the concerned stakeholders. As a professional, the RP is an outsider tasked with running a company that has nothing to do with him, and gets compensated according to the guidelines of the code. Serious penalties are imposed for actions like using “related parties” improperly and engaging in wrongful trading.

The CIRP procedure can be made more transparent to the public, with IBBI already actively promoting this goal through mandatory disclosures (such as losses and allottee information) on their website. To improve accountability and stakeholder participation, the increased emphasis can be on use of artificial intelligence (AI) and digital tools. AI can reduce human error and guarantee timely and comprehensive disclosures to all stakeholders by automating the process of disseminating the financial data.

2.2.3 Management of the corporate debtor (CD) as a “going concern by RPs

The impact on firm performance for continuity of operations by RPs is analyzed here. It shall be the duty of the resolution professional to preserve and protect the assets of the corporate debtor, including the continued business operations of the corporate debtor11as a going concern.

The interim resolution professional or resolution professional, as the case may be, shall take custody and control as specified under this regulation from the personnel of the corporate debtor, its promoters or any other person associated with the management of the corporate debtor as the case may be, of the following: –

(a) the records of information relating to the assets, finances and operations of the corporate debtor referred in clause (a) of section 18 and such other information required under regulation 36;

(b) the assets recorded in the balance sheet of the corporate debtor or in any other records referred in clause (f) of section 18.12

Without prejudice to section 17(2)(d), the interim resolution professional or the resolution professional, as the case may be, may access the books of account, records and other relevant documents and information, to the extent relevant for discharging his duties under the Code, of the corporate debtor.13

For the above purposes, the interim resolution professional shall have the authority-

a. to appoint accountants, legal or other professionals as may be necessary;

b. to enter into contracts on behalf of the corporate debtor or to amend or modify the contracts or transactions which were entered into before the commencement of corporate insolvency resolution process;

c. to raise interim finance provided that no security interest shall be created over any encumbered property of the corporate debtor without the prior consent of the creditors whose debt is secured over such encumbered property.14

{For the appointment of accountants, legal or other professionals and to procure their services as in point (a) above, RPs can follow the Quality and Cost-Based Selection (QCBS) method. It is a procurement process typically used for selecting consultants in government tenders, where both technical quality and cost (fees) are considered. The technical and financial scores are given

different weights to create a combined score. The bidder designated as H1 and chosen for the engagement is the one with the highest total score. This method guarantees a balanced approach by giving priority to the selection of a highly qualified professional (quality assurance) rather than just the lowest bidder (least-cost selection).}

Kothari & Bansal (2019) stressed upon that the Resolution Professional appointed under the Insolvency and Bankruptcy Code is required to effectively manage the corporate debtor’s business, thus must assume the role of the CEO or Managing Director and endeavor to address the debtor’s problems while optimizing stakeholder value. The resolution professional oversees the CIRP’s operations, navigates the process, tries to keep control of the situation, and keeps resolving issues in order to guarantee that there is resolution rather than liquidation—since resolution serves the interests of all parties involved and liquidation should be the last resort.

Furthermore, the insolvency resolution professional or resolution professional’s job description goes beyond simply managing the company; he must also make sure it remains a going concern and consider how he can reach a suitable resolution within the time frame specified by the Code. In addition to maintaining the indebted corporate debtor as a going concern, RP works to ensure that a resolution applicant promptly acquires the corporate debtor. RP serves as a liaison between the Adjudicating Authority and other stakeholders, as well as between the Committee of Creditors and Resolution Applicant (RA). RP is the true heir to CIRP, having been entrusted with the responsibility of objective evaluation.

Reasonable efficacy in restructuring financially distressed entities has been demonstrated by RPs, with priorities in business continuity over dissolution. This value-maximizing strategy has resulted in notable gains in capital, productivity, and capacity. The reintegration of these

resources into the mainstream of economy has increased national economic productivity in accordance with the objectives, principles, and codes. The study by Ram Mohan & Gopalakrishnan (2023) on functioning of firms that have undergone resolution under the Code reaffirmed it. Key improvements in the company’s performance after the resolution were noted, including a 76 percent increase in average sales, an improvement in EBITDA and net margin, the accumulation of tangible assets, as evidenced by a 50 percent increase in average total assets and a 130 percent increase in average capital expenditures, convergence of profitability ratios with benchmark averages, a three-fold increase in aggregate market valuation, and an 80 percent improvement in liquidity.

All the responsibilities of the corporate debtor are passed over to the IRP under Section17 and Section 20 of the Code (Kothari & Bansal, 2019) that “the professional is required to act in an ongoing concern while managing the company” Insolvency and Bankruptcy Code framework supports that the acts are carried out keeping in mind the business to be a going concern. {The noteworthy point under Section 1715 is IRP’s power of suspending the powers vested in the partners of the corporate debtor or board of directors. This is done to protect creditors’ interests so that a professional can start CIRP without interference, encouraging long-term investment in mergers and acquisitions and the spirit of entrepreneurship.}

Despite the above success ratio, RPs lack adequate management expertise for handling the firm for continuity which is a major lacuna in the complete CIRP. The resultant ratio of the viability of the firms can be improved much better with their due role clarity and discharge of specialists’ function as resolution professionals. In the present system, as discussed above IPs (RPs) deal with both process management and operational control. This can continue in case of small firms with admitted claims of less than Rs. 1,000 crores.

However, in case of large concerns with admitted claims of more than Rs. 1,000 crores with higher stakes being involved a better approach for future efficacy of CIRP can be “Segregated Dual System in CIRP.” There can be separation of resolution process oversight and operational management between IPs and SPVs as follows:

(i) Insolvency Professional Entities (IPEs) may be appointed over individual insolvency professionals as “IPs” in these firms, keeping in view the case technicalities. They shall oversee the CIRP and ensure compliance with the Code.

{IPEs combine the resources and skills of multiple IPs. Therefore, in order to potentially speed up the resolution process and stop asset value erosion, they can be considered for such large and complex cases involving high stakes or complex legal issues. However, the decision to select the most suitable expert or organization for the particular case ultimately rests with the appointing authority — the Adjudicating Authority (AA) or the committee of creditors (CoC).}

Further, there can be a ‘fit and proper’ criterion for IPEs as IPs. It is mentioned in IBBI Regulations, 2016 as well that an insolvency professional entity shall be jointly and severally liable for all acts or omissions of its partners or directors as insolvency professionals committed during such partnership or directorship.16

(ii)A specialized company or special purpose vehicle (SPV) may take care of the

functioning of the business, including managing the daily operations and the functional areas, like finance, human resource, etc. Furthermore, they will be responsible for the supervision and asset management of the firm.

{In above mentioned large cases, an SPV’s main duties are risk mitigation and asset protection, which guarantees the continuation of vital business operations and the preservation of the value of particular assets (such as technology, patents, or trademarks) for creditors or possible buyers.}

Case example17: A well-known global example of an SPV managing a particular business function is the development of “Canary Wharf financial district” in London, which employed a Special Purpose Vehicle (SPV) to oversee the extensive construction, isolate project risks and draw investment from a variety of sources.

The IPs’ role definition to IPs only gets an inspiration as laid down in Section 144 of the Companies Act, 2013, wherein Auditors are not to render certain services including (a) accounting and book keeping services; (b) internal audit; (c) design and implementation of any financial information system; (d) actuarial services; (e) investment advisory services; and others18

Further, the composition of specialised company is in alignment with global best practices such as the UK’s “Special Managers’ Framework” in their Section 177 of the Insolvency Act 1986. It states: where a company has gone into liquidation, or provisional liquidation the court may appoint any person to be the special manager of the business or property of the company.19Thus, it is a court-appointed insolvency resolution process wherein a special manager is typically appointed when the nature of the company’s business is such that it requires a particular type of expertise, not possessed by a regular insolvency practitioner.

It is known, company’s ability to continue operating as a going concern, is the resolution professional’s responsibility. He shall take the custody and control of the relevant documents and assets from the corporate debtor to efficiently oversee the corporate debtor’s operations; they must take on the responsibilities of the CEO or Managing Director fully and work to resolve the debtor’s issues while maximizing stakeholder value. RP acts as a mediator between the Committee of Creditors and Resolution Applicant (RA), as well as between the Adjudicating Authority and other interested parties. In order to ensure that there is resolution rather than liquidation—the resolution professional manages the CIRP’s operations, navigates the process, controls the situation, and continues to resolve issues. The most notable feature is the suspension of the authority held by corporate debtor, board of directors, etc. while it is transferred to the Interim Resolution. But the evident concern is that RPs lack adequate management expertise for handling the firm in the CIRP, so for better process management and operational control, the above dual process by individual IPs/RPs can continue in small firms with claims < Rs. 1,000 crores. But in case of large concerns with claims > Rs. 1,000 crores, a better strategy for CIRP’s future effectiveness may be “Segregated Dual System in CIRP” with IPs looking after the insolvency and resolution process, and a specialized company handling the management of the business. These IPs handling projects worth more than Rs. 1,000 crores, for better skill management, may be recommended a personalized 1-2 days of orientation program to be conducted by the IBBI.

It has been shown that financially distressed entities can be restructured with remarkable effectiveness, giving business continuity precedence over dissolution by RPs. Capital, productivity, and capacity have all increased significantly as a result of this value-maximizing approach.

2.2.4 Facilitation of the development of a viable resolution plan by RPs

“Resolution plan” means a plan proposed by resolution applicant for insolvency resolution of the corporate debtor as a going concern in accordance with Part II of the Code.20

The Resolution Professional ought to facilitate the CIRP process timely; and the plan should be prepared fairly and equally, and timely taking into account the interests of all parties involved. RP must examine each resolution plan received by him/her to check if it provides for and conforms to all requirements mentioned in Section 30(2) of the Code. Verification of claims21 by RPs in due time is must for developing a viable resolution plan. The interim resolution professional or the resolution professional, as the case may be, shall verify every claim, as on the insolvency commencement date, within seven days from the last date of the receipt of the claims, and thereupon maintain a list of creditors containing names of creditors along with the amount claimed by them, the amount of their claims admitted and the security interest, if any, in respect of such claims, and update it.

Determination of amount of claim22 needs to be followed as the next step in the process. Where the amount claimed by a creditor is not precise due to any contingency or other reason, the interim resolution professional or the resolution professional, as the case may be, shall make the best estimate of the amount of the claim based on the information available with him. He shall revise the amounts of claims admitted, including the estimates of claims made above as soon as may be practicable, when he comes across additional information warranting such revision.

Therefore, in order to ensure that the plan is prepared promptly, fairly, and with consideration for the interests of all parties, the Resolution Professional should facilitate the CIRP process in a timely manner. What assumes importance here is that RPs must quickly verify claims in order to create a workable resolution strategy, as prescribed within seven days of the last day of receiving the claims. This in fact can be further shortened up through the use of modern technology tools, professional assistance, or AI, making the overall insolvency resolution process more efficient.

For some qualified corporate debtors (such as small businesses), the IBC offers a particular framework called the ‘Fast Track CIRP’ that is intended to resolve insolvency more quickly.

The role of RP only to ‘examine’ and ‘confirm’ that each Resolution Plan conforms to the provisions of the Code is a limiting factor. RP can be given substantial authority and must be entitled to provide a detailed deliberation about the Resolution Plan.

{By substantial authority to RPs, the implication is “Not direct court power,” but significant authority granted to oversee the process, carefully examine plans, and assess a proposed corporate turnaround/resolution plan. This will help them in ensuring legal compliance and it will be advantageous for all stakeholders before the Adjudicating Authority (NCLT) approves it.}

Additionally, he will make the best estimate of the claim amount based on the information at his disposal including contingencies.

2.2.5 Appointment of Registered Valuers at arm’s length by RPs

(1) The resolution professional shall, within seven days of his appointment but not later than forty seventh day from the insolvency commencement date, appoint two registered valuers to determine the fair value and the liquidation value of the corporate debtor in accordance with regulation 35.23

The interim resolution professional or the resolution professional, as the case may be, may appoint any professional, in addition to registered valuers under sub-regulation (1), to assist him in discharge of his duties in conduct of the corporate insolvency resolution process, if he is of the opinion that the services of such professional are required and such services are not available with the corporate debtor.

2. The valuer must be an IBBI-registered valuer as defined under Companies (Registered Valuers and Valuation) Rules, 2017, and possess valid authorization for the relevant asset class.24

3. The appointment of a professional under this regulation should be on an ‘arm’s length’ basis following an objective and transparent process. There should be no conflict of interest.

4. The invoice for fee and other expenses incurred by a professional appointed under this regulation shall be raised in the name of the professional and be paid directly into the bank account of such professional.25

It is apparent, professional (valuer) should be appointed “arm’s length” through an impartial and open procedure. The resolution professional must designate two registered valuers to ascertain the fair value and liquidation value of the corporate debtor within seven days of his appointment, but no later than forty-seven days from the date the insolvency began. The said time-lines specified in the regulations are crucial for maintaining the integrity and due efficiency of the insolvency resolution process. The qualifications and experience of a registered valuer in a “specific discipline” are defined as pertinent to the valuation of an ‘asset class,’ which is specified under Annexure IV26 as follows:

| Asset class | Experience in specified discipline |

| Plant and Machinery | (i) Five years

(i) Three years |

| Land and Building | (ii) Five years

(ii) Three years |

| Securities or Financial Asset | (i) Three years |

2.2.6 Conduct of resolution process (CIRP) by RPs in a fair and just manner

To determine the fairness of corporate insolvency resolution process without any undue

influence regarding the stated factors, following is the discussion below.

i. constitution of the CoC.

Under the Code, the constitution of the Committee of Creditors (CoC) is governed by Section 21, comprising all financial creditors of the corporate debtor. Related parties of the CD are excluded.

The Interim Resolution Professional (IRP) shall after collation of all claims received against the corporate debtor and determination of the financial position of the corporate debtor, constitute a committee of creditors. It is final once formed. The decisions within the CoC are made by a voting share of the financial creditors.

ii. convening its meeting. As per Section 22 of the Code, the “first meeting” of the committee of creditors shall be held within seven days of the constitution of the committee of creditors.

As mentioned in part 2.2.1 above, the CoC, may, in the first meeting, by a majority vote of not less than sixty-six per cent of the voting share of the financial creditors, either resolve to appoint the interim resolution professional as a resolution professional or to replace the interim resolution professional by another resolution professional.

The members of the committee of creditors may meet in person or by such electronic means as may be specified. All meetings of the committee of creditors shall be conducted by the ‘resolution professional.’ [Section 24 of the Code].

(iii) inviting prospective resolution applicants to submit a resolution plan. Under the Code, the RP invites prospective resolution applicants to submit resolution plans after obtaining approval from the CoC. As per Section 29A of the Code, a person shall not be eligible to submit a resolution plan, if such person, or any other person acting jointly or in concert with such person—

a. is an undischarged insolvent;

b. is a willful defaulter in accordance with the guidelines of the Reserve Bank of India issued under the Banking Regulation Act, 1949 (10 of 1949);

c. at the time of submission of the resolution plan has an account, or an account of a corporate debtor under the management or control of such person or of whom such person is a promoter, classified as non-performing asset in accordance with the guidelines of the Reserve Bank of India issued under the Banking Regulation Act, 1949.

Request for Resolution Plan.The resolution professional shall, within five days of the date of issue of the final list under sub-regulation (12) of regulation 36A, issue the information memorandum (IM), evaluation matrix and a ‘request for resolution plans’ to every resolution applicant in the final list:

(i) The request for resolution plans shall detail each step in the process, and the manner andpurposes of interaction between the resolution professional and the prospective resolution applicant, along with corresponding timelines.

(ii) The request for resolution plans shall allow prospective resolution applicants a minimum of thirty days to submit the resolution plan(s).

In accordance with Section 30 of the Code, a resolution applicant submits a resolution plan [along with an affidavit stating that he is eligible under section 29A] to the resolution professional prepared on the basis of the information memorandum.

(iv) presenting to the COC, for its evaluation. In accordance with Section 30 of the Code, the resolution professional shall examine each resolution plan received by him to confirm that each resolution plan –

a. provides for the payment of insolvency resolution process costs in a manner specified by the Board;

b. provides for the payment of debts of operational creditors in such manner as may be specified by the Board.

As verified above, RP submits the plan along with fair value and liquidation value reports, to the CoC members. The CoC, using its commercial wisdom, evaluates the plan’s feasibility, viability, and distribution based on an ‘evaluation matrix’ and approves it with at least a 66% majority vote. {The two registered valuers appointed under regulation 27 shall submit to the resolution professional an estimate of the fair value and of the liquidation value computed in accordance with internationally accepted valuation standards, after physical verification of the inventory and fixed assets of the corporate debtor.} The resolution professional and registered valuers shall maintain confidentiality of the fair value and the liquidation value.28

(v) submitting the resolution plan approved by CoC to AA. The RP then submits the approved plan to the Adjudicating Authority (NCLT). According to Section 31(1) of the Code, if the Adjudicating Authority is satisfied that the resolution plan as approved by the committee of creditors meets the requirements as in sub-section (2) of section 30, it shall by order approve the resolution plan which shall be binding on the corporate debtor and its employees, members, creditors.

Where the Adjudicating Authority is satisfied that the resolution plan does not confirm to the requirements referred to in sub-section (1), it may, by an order, reject the resolution plan.

During the Corporate Insolvency Resolution Process, the RP attempts to continue operating the company while the interested parties seek resolutions to rebuild the corporate debtor. The RP is in charge of all management and operations of the corporate debtor for the duration of the specified time as specified in the code read with the pertinent rules and regulations. For smooth conduct of the resolution plan, it is essential to have the following considerations:

- Timely appointment. Section 16 provides for the appointment of IRP. The Adjudicating Authority shall appoint an interim resolution professional [on the insolvency commencement date.] The aim of this appointment is to maximize the company’s value or ensure its survival before proceeding to liquidation.

- Further, the term of the interim resolution professional [shall continue till the appointment of the resolution professional by the CoC under section 22]. This is to ensure continuity until a long-term professional takes over.

- Managerial role. The RP has to be in charge of acting as the managerial head of the Corporate Debt’s operations once the corporate is accepted for a CIRP process. It becomes their responsibility to ensure that employees receive their salaries on time and work with high morale. Additionally, in these circumstances, it is crucial to provide them with the much-needed support to complete the tasks in hand.

- Pro-active governance. RPs should to protect and assist a dying company by doing everything within their power to restore it and re-establish it as a going concern. One way to do this is by actively participating in and conducting the plan at every level that is feasible.

It is clear that largely RPs conduct the resolution plan in a fair and just manner without any undue influence from stated corners. The Code governs the composition of the CoC, which is made up of all of the corporate debtor’s financial creditors, excluding the CD’s related parties. In their first meeting, the committee of creditors decide to either appoint the interim resolution professional as a resolution professional or to replace the interim resolution professional with another resolution professional by a majority vote of at least 66% of the financial creditors’ voting shares.

Following CoC approval, the RP extends an invitation to potential resolution applicants to submit resolution plans and reviews each resolution plan to ensure that each one confirms to the required guidelines. After the receipt of resolution plans, the resolution professional will have to electronically distribute the fair value, liquidation value, and valuation reports to each committee member upon receiving an undertaking from the member with a narrative of keeping the fair value confidential. Finally, RP sends the approved plan to the Adjudicating Authority (NCLT).

As the focus is on rebuilding the corporate debtor, the RP tries to keep the business running during the CIRP. The factors like on-time appointment, managerial position, and pro-active leadership must be taken into account for the plan to run smoothly and safeguard and support a dying business. Although the RP assumes management, they may not be in charge of all day-to-day operations. In order to maintain the company’s viability as a going concern, they are required to oversee the general operations, with the exiting operational management usually carrying on running the daily business under the RP’s general supervision and control.

2.2.7 Irregularities by RPs – Requirements of performance guarantees

The First Schedule of the (Insolvency Resolution Professional) Regulation, 201629 provides for the Code of Conduct for Insolvency Professionals, yet following irregularities and procedural lapses can be observed in their working:

- Delay in announcements. There are delays on the part of RPs in making public announcements within the stipulated time which hamper the CIRP.

- Inadequate examination. RPs failing to carry out a comprehensive examination of the corporate debtor’s financial activities will help CDs to hide possible frauds.

- Filing delays. Under section 19(2) of the Code, where any personnel of the corporate debtor, its promoter or any other person does not assist or cooperate, the interim resolution professional may make an application to the Adjudicating Authority for necessary directions. Delays in filing these non-cooperation applications on the part of RPs disrupt the CIRP.

- Poor control and management. By not restoring timely, they make a dying company reach to its end. Their failure to take control and custody of assets and lack of active participation at various levels make it happen.

- Value erosion. They don’t carry out their responsibilities effectively and always in the best interests of all parties involved, leading to value destruction. One such example is permitting suspended management to continue operations. Another case is allowing suspended management to represent CD in legal matters.

- Supremacy of interests. They fizzle out in of maintaining a balance of interest to benefit either the stakeholders nor the creditors solely gain. However, when verifying the resolution plan as presented at the CoC meeting, equilibrium should be preserved.

In view of the above lacunas, performance guarantees and bonds assume significance requiring a “formal agreement” outlining the scope of work, financial security from a third party (such as bank), and strict adherence to the agreed terms. If the RP does not deliver on their end, penalties are there in place under the Code and disciplinary actions by the IBBI. However, a suitable bond amount as a percentage of the total contract value can be decided initially, providing a safety net for the client. One exemplary indication for future inspiration, may not be completely similar, is discussed below.

Case: Regulated performance bond “A regulated performance bond can be issued by a bank or a financing company, like in France, that has been authorised by the Prudential Supervision and Resolution Authority (ACPR). These banks or financing companies then become members of the ‘Fonds De Garantie Des Depots Et De Resolution’: French deposit insurance and resolution fund (FGDR) under this mechanism and are required to contribute to it annually. This contribution is an express condition of their business.

These performance bonds are issued by the bank or the financial institution to business professionals who are required by law to provide a guarantee to their customers. These professionals may be builders, travel agents, insurance brokers, etc. Thus, if these professionals go out of business or disappear before fulfilling their obligations to their end customers, the bank or financial institutionwould assume responsibility for the agreed service without customers having to pay for it a second time.

When the institution that issued a mandatory performance bond in favour of a business professional fails, the FGDR takes its place in order to fulfil the commitment made by the professional to the end customer. This is known as “assumption of commitment” by the FGDR (Article L. 313-50 of the French Monetary and Financial Code). If the professional subsequently defaults vis-à-vis their customer, the FGDR compensates the customer.” 30

The noticeable fact is although the Code of Conduct for Insolvency Professionals is outlined in the First Schedule of the (Insolvency Resolution Professional) Regulation, 2016, the following anomalies in their operations can be noted: (i) insufficient analysis, (ii) ineffective administration, (iii) value destruction, and (iv) interest dominance. These issues need to be adequately addressed for ensuring fair and sound working by RPs in the entire process. Therefore, warrant of performance guarantee by RPs after their appointment becomes essential. Given the aforementioned shortcomings, performance guarantees and bonds may be required, necessitating a “formal agreement” detailing the extent of the work, third-party financial security (like a bank), and rigorous adherence to the terms of the agreement with an appropriate bond payout to the client. Performance guarantees and bonds are commonly required in construction and infrastructure projects, government procurement, large-scale IT projects, and commodity supply contracts. These documents assure the project owner that the selected vendor will fulfill his contractual obligations. So, a performance bond guarantee scheme can be created as discussed above, in comparable industries internationally. This will have long-term implications for all the concerned stakeholders, ensure fair and just process, and pave the path for better road-map of resolution.

2.2.8 Competence and Capabilities of RPs for fraud detection in CIRP

Prevention of “fraudulent” or “wrongful” trading shall be the foremost job of the resolution professional. The Code provides for the following: –

1. If during the corporate insolvency resolution process or a liquidation process, it is found that any business of the corporate debtor has been carried on with intent to defraud creditors of the corporate debtor or for any fraudulent purpose, the Adjudicating Authority may on the application of the resolution professional pass an order that any persons who were knowingly parties to the carrying on of the business in such manner shall be liable to make such contributions to the assets of the corporate debtor as it may deem fit.

2. On an application made by a resolution professional during the corporate insolvency resolution process, the Adjudicating Authority may by an order direct that a director or partner of the corporate debtor, as the case may be, shall be liable to make such contribution to the assets of the corporate debtor as it may deem fit.31

Thus, fraud detection and prevention are a significant part of the entire resolution process for the benefit of all. Therefore, RPs need to take a proactive and reactive role both. The prerequisites below determine the competence level of RPs in the exercise.

1. Understanding of CD. The entire procedure starts when the Interim Resolution Professional has been assigned by the Adjudicating Authority and the corporate debtor is handed over to the IRP to look after its initial management. It is crucial for the IRP and then the RP to understand the business of the Corporate Debtor, as only then they would be able to manage the CD’s day-to-day operations.

2. Integrity and Objectivity. An insolvency professional must act impartially and with integrity in all of his professional interactions, free from prejudice, conflicts of interest, undue influence, or coercion from any party, and refrain from purchasing the debtor’s assets.

3. Comprehensive study. The resolution professional ought to be mandated to carry out a comprehensive examination of the corporate debtor’s financial matters. The goal of this inquiry should be to find any misconduct on the part of the corporate debtor’s management.

It is obvious, the resolution professional’s top priority is to stop “fraudulent” trading. If it is discovered during a corporate insolvency resolution or liquidation process that a corporate debtor’s business was conducted with the intention of defrauding the debtor’s creditors or other, RP should not wait for the consequences and as ‘pro-active’ approach must recommend to the adjudicating authority for the necessary order. During the corporate insolvency resolution process, he is also expected to have knowledge about CD, the required objectivity and integrity, and a thorough investigation about him for the necessary action, if required.

2.2.9 Protection of interests of all the stakeholders by RPs

The role of Interim Resolution Professional32 and Resolution Professional is a significant aspect of the code that lays down the framework for corporate governance. The IRP/RP’s responsibilities include ensuring a fair and equitable outcome, forming a committee of creditors, creating a resolution plan, and managing the business’s affairs properly.

They must maintain a coherence of interest so that neither the stakeholders nor the creditors solely gain. When verifying the resolution plan as presented at the CoC meeting, equilibrium should be preserved. With respect to CIRP, RPs ought to ensure the balance of interests while earlier, there existed fraud, bad loans and banks held non-performing assets and lagging insolvency cases taking up to 4.3 years on an average which compared to other jurisdictions like the UK were remarkably long.33 This is examined on the facets of both CDs and responsibilities towards Creditors and their realization as below.

A. CDs

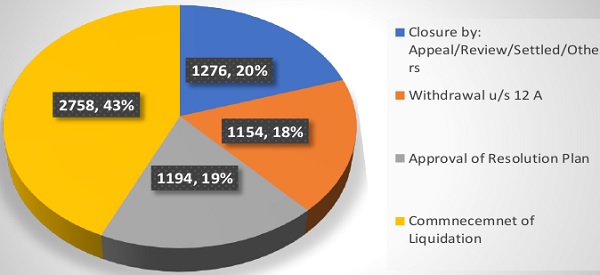

IBBI in their newsletter34 presents the performance overview of the IBC for eight years. Table 1 shows the status of corporate insolvency process since the inception of the Code. 1194 CDs have been rescued through resolution process. Further, 1276 cases have been settled through appeal or review of settlement and 1194 cases have been withdrawn under section 12A. 2758 CDs were referred for liquidation under the process.

Table 1. Status of CIRP

| Sl. No. | Particulars | October 2016- March 31, 2024 | 2024-25 | Total

(As on March ____ 31, 2025) |

| 1. | Total number of IBC cases admitted | 7984 | 724 | 8308 |

| 2. | Total CIRPs cases closed | 5667 | 715 | 6382 |

| 3. | Closure by:

Appeal/Review/Settled/Others |

1177 | 99 | 1276 |

| 4. | Withdrawal u/s 12 A | 1083 | 71 | 1154 |

| 5. | Approval of Resolution Plan | 935 | 259 | 1194 |

| 6. | Commencement of Liquidation | 2472 | 286 | 2758 |

| 7. | Ongoing CIRPs | 1917 | NA | 1926 |

Figure 1. CIRPs closure

As depicted in figure 1, Total CIRPs closed were 6382, stand at 76.82 percentage of the total cases admitted. It is a quite promising figure with a success ratio of more than 50 percent cases getting closed. Resolution Plans approved were 1194, with a figure of 19 per cent. This can be enhanced for future viability.

B. Creditors’ safeguard and Realization by Creditors

Interim resolution professional has the duty to receive and collate all claims of the creditors submitted by creditors to him pursuant to public announcement [Section 18(b) of the Code]. IRP or RP must verify every claim, as on the insolvency commencement date, and thereupon maintain a list of creditors containing names of creditors along with the amount claimed by them, the amount of their claims admitted and the security interest, if any, in respect of such claims, and update it. This verification must be completed within seven days from the last date of the receipt of claims [Regulation 13 of the IBBI (IRP) Regulations, 2016]

The Creditors have released Rs. 3.89 lakh crore under the resolution plans till March, 2025. This realisation is more than 32.8 per cent as compared to the admitted claims and more than 170.1 per cent as compared to the liquidation value. Resolution plans on average yield 93.41 per cent of fair value of the CDs. Till March, 2025, 1374 CDs have been completely liquidated with submission of final report. Out of the 1374 CDs 878 have been closed. In the closed liquidations, the creditors have released Rs. 9330 crore which is nearly 90 per cent realisation as compared to the liquidation value.

The above indicators speak of the role of RPs in protection of the interest of all stakeholders. Due accountability of the RPs in fulfilling their duties efficiently and in the interest of all the stakeholders must be maintained for the way forward. For this, the Committee of Creditors (CoC) should be the representative of all stakeholders. By giving more powers to the CoC will help in overseeing the Resolution Professionals’ activities. With the regulators providing for various measures in the context of RPs for stakeholders’ interests at large, it is expected that RPs will come out as more effective pillars of the CIRP.

In nutshell, RPs must uphold a coherence of interest of all stakeholders and ensure that neither the creditors nor the stakeholders benefit exclusively. RPs’ credibility, integrity, and competence are vital for stakeholders’ confidence and code efficiency. Equilibrium should be maintained when confirming the resolution plan, as presented and discussed. With respect to CIRP, they should pace up the lagging insolvency cases existed in the past as in countries like the UK.

With a success rate of over 50% of cases being closed, it is a very encouraging number. On average, resolution plans produce 93.79 percent of the CDs’ fair value. They highlight the part RPs play in safeguarding the interests of all parties involved.

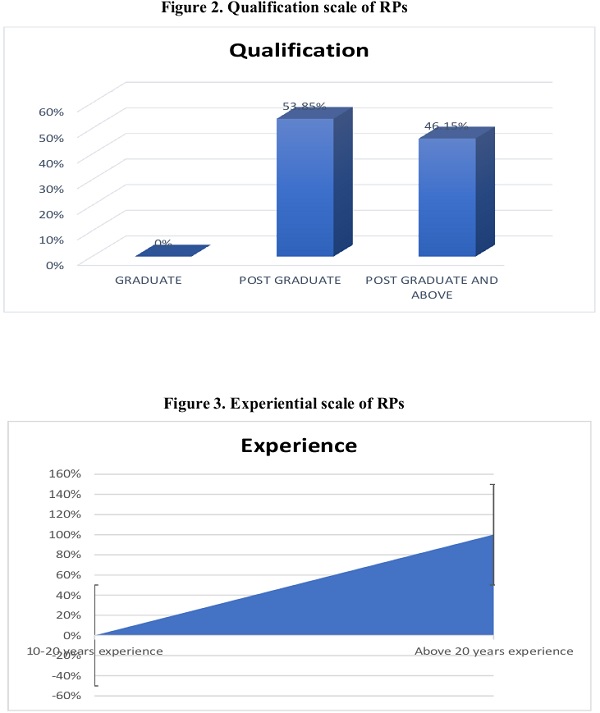

2.3 Interview analysis

This is the second part of formal analysis of the project. At this stage, the interview-based discussions were conducted in two-stage process; first by sending the structured questionnaires to over 30 Resolution Professionals (RPs). Subsequently, the data collected was substantiated by conducting interviews with 13 of them, based on their availability. It was also done to gather their views on those indicators which they feel were not there in the above structured questionnaire and could be helpful to the final analysis. The interviews lasted about 20 minutes each per participant. It helped to get a detailed review and suggestions about their appointment, role and modus-operandi, and CIRP. They indicated satisfaction with the overall process of appointment.

Additionally, they communicated that certain improvements are desirable in the future. The participants did, however, bring up process issues with other the regulator (IBBI) and government agencies, including the RBI and Income-tax Department. The interview responses broadly support our descriptive findings. The final data-set for interview analysis is given in table 2 and its charts are given in figures 2 and 3.

Table 2. Interview matrix

| S. No. | Variable | Number | Graduate | Post Graduate | Post Graduate and above |

Less than 20 years | Above 20 years |

| 8. | RPs – Final Respondents | 13 | |||||

| 9. | Qualification | 0 | 7 | 6 | |||

| 10. | Experience | 0 | 13 |

Figure 2. Qualification scale of RPs

Based on the above, following discussion emerges out on the stated objectives:

1. On an average, RPs fulfill the eligibility criteria in their appointment process. They are professionals with adequate qualification and experiential requirement, all possessing post graduate, and 46.15% having post graduate, and above qualifications with more than 20 years of experience. However, diverse experience in managerial and functional domain can be stressed upon. Further, IBBI Circular directing the NCLTs to 43 appoint a different person other than the Resolution Professional, as a Liquidator seems a bit harsh and counterproductive, since the Resolution Professional, having gained the knowledge of the asset would ideally be best placed to get the best value under the Liquidation process.

2. To manage the corporate debtor (CD) as a “going concern, their primary focus is on “preservation of value.” The management of the CD as a going concern is not a way but a process. The process involves engagement with the employees, vendors, utility providers as well as the Committee of Creditors for approvals either as mandated under the Code or as per the situations. The key thing is to get deeply involved in the business operations of the company and take a high-level view of the business and communicate with all stakeholders so as to understand the key value drivers and the constraints. In case of very large or complex operations, it is always prudent to have a technical expert on board who can act as a conduit between the RP/CoC and the management to identify gaps, leaks and run the operations. There is no one size fits all solutions. Each CD presents unique challenges, and the RP has to find a way to address them adequately. Various ways of managing their affairs comprise of the following:

- Custody and Control of bank accounts and assets;

- Focus on managing working capital for liquidity: Reviewing cash flows, arranging for interim finance (with CoC approval), and ensuring payment of operational expenses to retain continuity;

- Staff and Contract Management: Retaining essential personnel, renew or renegotiate contracts with vendors and customers;

- Prioritization of critical payments and operations: Ensuring supply chains are functional, production continues, and key client relationships are maintained;

- Deployment of security; identification of all locations (owned/ third party and operating / non-operating);

- Regulatory Compliance: Facilitating ongoing compliance with legal requirements;

- Stakeholder engagement: Maintaining transparent communication with the Committee of Creditors (CoC), employees, creditors regarding the CD’s status and actions being taken;

- Appointment of Experts: Engaging accountants, legal or technical professionals as required to manage complex affairs and address specialized challenges;

- Timely updates / approvals from COC on key operational matters.