Month: September 2020

1,318 articlesGoods and Services Tax

Goods and Services Tax

CBIC extends exemption on 2 type of transportation Services

Goods and Services Tax

Goods and Services Tax

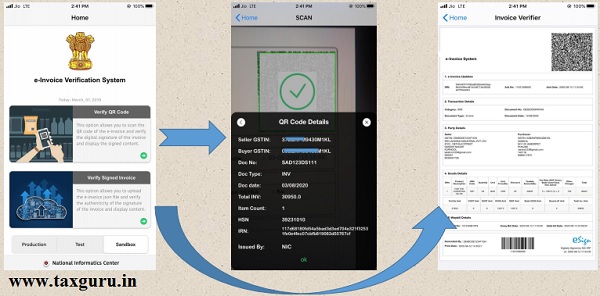

Relaxation in E-Invoice Provisions Implementation for Oct 2020

Goods and Services Tax

Goods and Services Tax

GST E-Invoice- CBDT amends rules related to IRN & QR Code

Goods and Services Tax

Goods and Services Tax

Dynamic QR Code on B2C invoices requirement deferred to 01.12.2020

Goods and Services Tax

Goods and Services Tax

GST Case Law Updates – September 2020

Goods and Services Tax

Goods and Services Tax

CBIC extends UTT exemption on 2 type of transportation Services

Goods and Services Tax

Goods and Services Tax

CBIC extends IGST exemption on 2 type of transportation Services

Income Tax

Income Tax

Detection of substantial unaccounted cash & other valuables during surveys under section 133A of Income Tax Act, 1961

Company Law

Company Law

Checklist for DPT 3

Income Tax

Income Tax