When we say Our life is Priceless, Do we really mean it? But for our loved ones it is Truly Priceless.

A few days ago I was at a bank for some work and while I was waiting for my turn, a lady in her mid twenties came up to the bank personnel and asked if her late father had any life insurance policies. Since this lady was sitting adjacent to me, I naturally happened to hear the conversation between her and the bank person (say, Mr. B). Mr. B requested the lady to look up the documents in her house and find out if there were any insurance policies in the name of her father as the bank would not have that record. The lady helplessly told Mr. B she was not aware of where such documents would be and the bank help her..

While this conversation was going on.. A whirl wind of thoughts started in my mind.

We plan for everything in life but there is something which only the Almighty can plan. Can we ever be prepared for it..? NO, but we can follow 4 key steps to ensure our families are least stressed at such times :

1. Evaluate if our Life Insurance is adequate to give the same lifestyle to our families which they are enjoying now.

More about Understanding your Life Insurance needs:

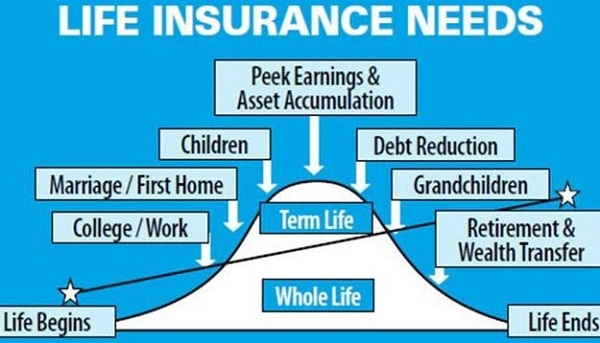

- As a general rule, one required 10-12 times of his/her income as Life Insurance Cover. Please note the important word here is Income. Any non-earning member does not require Life Insurance. Non earning members would include housewife, student, retired persons.

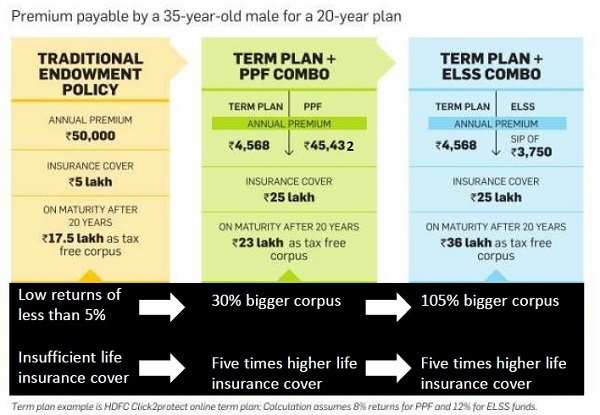

- NEVER Mix INSURANCE and INVESTMENTS

When we first started our journey as financial planners, we noted that many Indians were lacking on the first step of financial planning i. e. INSURE. Before we plan our finances, we need INSURE events which are not in our control. Most of our clients would argue that they held traditional life insurance plans or ULIP.

The most important concept to understand here is that INSURANCE and INVESTMENTS should be separate.

The need arose for analysis of customised reports for giving the clients an understanding that neither the traditional life insurance provided sufficient LIFE COVER nor RETURN on investments.

2. Keep all medical and life insurance papers in one file and each member of family should be aware about it.

3. Keep all asset documents in some cabinet and update the family members periodically about the same.

4. In this world of internet most of our insurance and other assets details are in our email accounts. Use Inactive account feature (available in gmail) which will notify and give access to another pre-decided email id after a certain period of inactivity. This way our family can access important data from the email account.

CA Mitsu Buddhadev

CA Nitesh Buddhadev

Nimit Wealth Management

For feedback or suggestions, you may reach out to us at info@nimitwealthmanagement.com

Thanks Heena. I am glad you liked the article.

Help us Spread financial literacy by sharing it with your friends and family.

Thank you Nitesh for this wise advice.