After the spread of pandemic ‘COVID-19’, GOI has announced many relief packages for MSME sector to boost industry as well as economy of the country. Government initiatives include ease of doing business, Digital India, start-ups, easy loans , Make in India, subsidies, moratorium for loans, reduced rate of interest, simple tax compliances & transparency in working to make ‘Aatam Nirbhar Bharat’. Govt is also working on several initiatives, such as preparation of huge land pools, to attract potential investors to India amid the corona virus-triggered turbulence. Govt has re-defined MSME law & relaxed many provisions accordingly so that many enterprises can avail benefits available, including those which were earlier deprived off. Govt has introduced concept of ‘Udyam Registration’ w.e.f. 01/07/2020 for existing registered under ‘EM-II’ & ‘Udyog Aadhar Memorandum- UAM’ as well as new MSME enterprises. Let us study about Udyam Registration Number in detail.

Page Contents

- 1. Classification of MSME Enterprises (referred to as ‘Udyam’)

- 2. How to Register with Udyam Registration Portal?

- 3. How criteria of Turnover & Investment would be decided for Udyam Registration?

- 4. How to calculate investment in plant and machinery or equipment for Udyam Registration?

- 5. How to calculate Turnover for Udyam Registration?

- 6. What is process for Udyam Registration Number?

- 7. What is process for Udyam registration of existing enterprises?

- 8. What is procedure for updation of information and transition period in Udyam classification?

1. Classification of MSME Enterprises (referred to as ‘Udyam’)

An enterprise shall be classified as a micro, small or medium enterprise on the basis of the following criteria:-

| Enterprise | Investment Criteria | Turnover Criteria |

| Micro Enterprise | where the investment in plant and machinery or equipment does not exceed one crore rupees and; | Turnover does not exceed five crore rupees |

| Small Enterprise | where the investment in plant and machinery or equipment does not exceed ten crore rupees and; | Turnover does not exceed fifty crore rupees |

| Medium Enterprise | where the investment in plant and machinery or equipment does not exceed fifty crore rupees and; | Turnover does not exceed two hundred and fifty crore rupees |

2. How to Register with Udyam Registration Portal?

√ Any person who intends to establish a micro, small or medium enterprise may file Udyam Registration online in the Udyam Registration portal.

√ Based on self-declaration only

√ No requirement to upload documents, papers, certificates or proof

√ On registration, an enterprise (referred to as ―Udyam) in the Udyam Registration portal will be assigned a permanent identity number to be known as ―Udyam Registration Number (URN).

√ An e-certificate, namely, Udyam Registration Certificate shall be issued on completion of the registration process.

3. How criteria of Turnover & Investment would be decided for Udyam Registration?

√ A composite criterion of investment and turnover shall apply for classification of an enterprise as micro, small or medium i.e. both Turnover & Investment to be considered jointly for enterprise to be covered in one of Micro, small or medium

√ If an enterprise crosses the ceiling limits specified for its present category in either of the two criteria of investment or turnover, it will cease to exist in that category and be placed in the next higher category

√ Once registered, no enterprise shall be placed in the lower category unless it goes below the ceiling limits specified for its present category in both the criteria of investment as well as turnover.

√ All units with Goods and Services Tax Identification Number (GSTIN) listed against the same Permanent Account Number (PAN) shall be collectively treated as one enterprise and the turnover and investment figures for all of such entities shall be seen together and only the aggregate values will be considered for deciding the category as micro, small or medium enterprise

4. How to calculate investment in plant and machinery or equipment for Udyam Registration?

√ The calculation of investment in plant and machinery or equipment will be linked to the Income Tax Return (ITR) of the previous year filed under the Income Tax Act, 1961.

√ In case of a new enterprise, where no prior ITR is available, the investment will be based on self-declaration of the promoter of the enterprise and such relaxation shall end after the 31st March of the financial year in which it files its first ITR.

√ The expression ―plant and machinery or equipment of the enterprise, shall have the same meaning as assigned to the plant and machinery in the Income Tax Rules, 1962 framed under the Income Tax Act, 1961 and shall include all tangible assets (other than land and building, furniture and fittings).

√ The purchase (invoice) value of a plant and machinery or equipment, whether purchased first hand or second hand, shall be taken into account excluding Goods and Services Tax (GST), on self-disclosure basis, if the enterprise is a new one without any ITR.

√ The cost of certain items specified in the Explanation I to sub-section (1) of section 7 of the Act shall be excluded from the calculation of the amount of investment in plant and machinery. Explanation to sub-section (1) of Section 7 of the Micro, Small and Medium Enterprises Development Act, 2006 is reproduced below:

Explanation 1 —For the removal of doubts, it is hereby clarified that in calculating the investment in plant and machinery, the cost of pollution control, research and development, industrial safety devices and such other items as may be specified, by notification, shall be excluded

5. How to calculate Turnover for Udyam Registration?

√ Exports of goods or services or both, shall be excluded while calculating the turnover of any enterprise whether micro, small or medium, for the purposes of classification.

√ Information as regards turnover and exports turnover for an enterprise shall be linked to the Income Tax Act or the Central Goods and Services Act (CGST Act) and the GSTIN.

√ The turnover related figures of such enterprise which do not have PAN will be considered on self-declaration basis for a period up to 31st March, 2021 and thereafter, PAN and GSTIN shall be mandatory.

6. What is process for Udyam Registration Number?

(1) The form for registration shall be as provided in the Udyam Registration portal.

(2) There will be no fee for filing Udyam Registration.

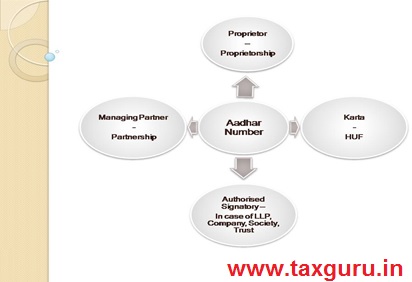

(3) Aadhaar number shall be required for Udyam Registration.

(4) The Aadhaar number shall be of the proprietor in the case of a proprietorship firm, of the managing partner in the case of a partnership firm and of a Karta in the case of a Hindu Undivided Family (HUF).

(5) In case of a Company or a Limited Liability Partnership or a Cooperative Society or a Society or a Trust, the organization or its authorised signatory shall provide its GSTIN and PAN along with its Aadhaar number.

(6) In case an enterprise is duly registered as an Udyam with PAN, any deficiency of information for previous years when it did not have PAN shall be filled up on self-declaration basis.

(7) No enterprise shall file more than one Udyam Registration, provided that any number of activities including manufacturing or service or both may be specified or added in one Udyam Registration.

(8) Whoever intentionally misrepresents or attempts to suppress the self-declared facts and figures appearing in the Udyam Registration or updation process shall be liable to such penalty as specified under section 27 of the Act.

7. What is process for Udyam registration of existing enterprises?

(1) All existing enterprises registered under EM–Part-II or UAM shall register again on the Udyam Registration portal on or after the 1st day of July, 2020.

(2) All enterprises registered till 30th June, 2020, shall be re-classified in accordance with new notification.

(3) The existing enterprises registered prior to 30th June, 2020, shall continue to be valid only for a period up to the 31st day of March, 2021.

(4) An enterprise registered with any other organization under the Ministry of Micro, Small and Medium Enterprises shall register itself under Udyam Registration.

8. What is procedure for updation of information and transition period in Udyam classification?

(1) An enterprise having Udyam Registration Number shall update its information online in the Udyam Registration portal, including the details of the ITR and the GST Return for the previous financial year and such other additional information as may be required, on self declaration basis.

(2) Failure to update the relevant information within the period specified in the online Udyam Registration portal will render the enterprise liable for suspension of its status.

(3) Based on the information furnished or gathered from Government’s sources including ITR or GST return, the classification of the enterprise will be updated.

(4) In case of graduation (from a lower to a higher category) or reverse-graduation (sliding down to lower category) of an enterprise, a communication will be sent to the enterprise about the change in the status.

(5) In case of an upward change in terms of investment in plant and machinery or equipment or turnover or both, and consequent re-classification, an enterprise will maintain its prevailing status till expiry of one year from the close of the year of registration.

(6) In case of reverse-graduation of an enterprise, whether as a result of re-classification or due to actual changes in investment in plant and machinery or equipment or turnover or both, and whether the enterprise is registered under the Act or not, the enterprise will continue in its present category till the closure of the financial year and it will be given the benefit of the changed status only with effect from 1st April of the financial year following the year in which such change took place.

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Author can be reached at casagargambhir@gmail.com for any queries, issues & recommendations relating to article.

Author Bio

Exclusion of cost of Pollution Control, Research & Development and Industrial Safety Devices during WHICH AMOUNT

we registered udyam aadhar & got reg no. UDYAM-xx-**-0000***. Is it correct no?, bcoz when we enter it some other place it highlight notification that reg no. Should be xx-**-x-*******.! How should we use it? We need udyog aadhar ? Plz clear confusion.

Am udog aadar nambar TN-02-0001899

Can I register my e – commerce business in udaym MSME website ? i cannot found NIC number for ECOMMERCE

Hi

On https://udyogaadhaar.gov.in/UA/UAM_Registration.aspx guidelines are given.

Q. 17 deals with P&M investment:

“17. Investment in Plant & Machinery / Equipment- While computing the total investment , the original investment ( purchase value of items) is to be taken into account excluding tho cost of pollution control, research and development, industrial safety devices, and such other items as may be specified, by notification of RBI. If an enterprise started with a set of plant and machinery purchased in 2008 worth Rs. 70.00 lakh has procured additional plant and machinery in the year 2013 worth Rs. 65.00 lakh, then the total investment in Plant & Machinery may be treated as Rs. 135.00 lakh.”

Which value of Plant & Machinery to be considered as per previous ITR filled i.e. gross value or Net value After depreciation as per I.T.Act or Company Act while filing registration form for Udyam Registration