Case Law Details

Adesh Ventures LLP Vs Initiating Officer (Appellate Tribunal Under SAFEMA Delhi)

Benami Web Exposed: Tribunal Upholds Attachments in Rs 80+ Cr Layered Accommodation Entry Case

The Appellate Tribunal under SAFEMA dismissed a batch of appeals challenging provisional attachment of properties under the Prohibition of Benami Property Transactions Act, 1988, holding that a clear case of benami transactions was established. The Tribunal found that the appellants (ARC group entities and related individuals) had generated unaccounted cash through online betting and gambling, which was subsequently routed through multiple entities via accommodation entries and introduced into books as bogus unsecured loans, capital, commission, and trading income.

The Tribunal rejected the contention that the Benami Prohibition Unit (BPU) could not rely on Income Tax search material, holding that there is no legal bar on using such evidence, especially when supported by corroborative electronic records and statements. It emphasized that retracted statements can still be relied upon if supported by independent evidence, such as digital records (e.g., “Hisab” sheets and “Octonwards Final” data showing cash-to-bank entry mapping).

It further held that assessment of income under the Income-tax Act does not preclude benami proceedings, as both operate in different domains-taxability vs. ownership/beneficial interest. The Tribunal concluded that the layered routing of funds through third parties itself establishes benami character, and that the corporate entities acted as benamidars for the beneficial owners. Accordingly, the provisional attachments were upheld and all appeals were dismissed.

FULL TEXT OF THE ORDER OF APPELLATE TRIBUNAL UNDER SAFEMA AT NEW DELHI

By a batch of appeals filed under Section 46 of the Prohibition of Benami Property Transactions Act, 1988 (in short “the Act of 1988”), a challenge has been made to the order dated 14.11.2023 passed by the Adjudicating Authority, PBPTA, Mumbai confirming the provisional attachment of the properties while answering the reference sent by the Initiating Officer.

Brief facts of the case:

2. It is a case where a search was conducted by the Income Tax Department in the premises of Shri Ramesh Chaurasia, Shri Achal Chaurasia and ARC group of companies on 15.02.2022. It was found that the income from online gaming business was shown to be out of the business of commodity, broking and management / business consultancy activities. It was revealed that M/s Adesh Ventures LLP (in short hereinafter referred as “AV LLP”) had received bogus unsecured loan from various entities over a period of time. The funds were used to purchase listed securities and mutual funds. It is, otherwise, a Limited Liability Partnership firm incorporated on 01.10.2014 with total contribution of Rs.2,00,000/-. The said AV LLP had invested more than Rs.91 Crores in shares and mutual funds. It was using the LLP as benamidar by Shri Achal Chaurasia and Shri Ramesh Chaurasia for investment in the equities and mutual funds from unaccounted, illegally generated income. The firm was not doing any real business and therefore there was no genuine source of income. The investment by AV LLP in listed securities and mutual funds was found amounting to Rs. 82.37 Crores as per the balance sheet of year 2021-22. The source of the funds to purchase the shares / mutual funds was the unsecured loans amounting to Rs.6,10,55,270/- which remained outstanding till 15.02.2022. The said firm, further, received unsecured loan from various entities over a period of time which is tabulated as under: –

| Name | Opening balance as on 01.04.2015 | AY 2018-19 | AY 2019-20 | AY 2020-21 | AY 2021-22 | AY 2022-23 |

| Adesh Ventures LLP | 13,10,270 | 26,62,39,500 | 61,30,000 | 65,00,000 | 9,00,00,000 | 24,00,000 |

3. In the Financial Year 2016-17, Penant Commotrade Pvt. Ltd. became a partner in AV LLP with a fixed capital of 18,000 and Authentic Finance Pvt. Ltd. became a partner in the Financial Year 2020-21 with a fixed capital of 20,000. The share of partnership of Penant Commotrade Pvt. Ltd. and Authentic Finance Pvt. Ltd. remained 9% and 10% in AV LLP. The fact aforesaid was taken into consideration to analyze the capability of AV LLP for investment of more than Rs.82.37 Crores in shares and mutual funds. The contribution by way of capital was negligible.

4. The AV LLP shown income from commission, professional service and business of the entities engaged in diverse business such as online pharmacy, steel, pipes and fittings, IT, wholesale and retail trade, medical equipment manufacturer etc.. However, during the course of enquiry, it was found that AV LLP is only on papers and thus not involved in any business. The AV LLP was used to channelize the cash earned by the beneficial owner to acquire the assets. It was out of online gaming and betting business. On finding material to make out a prima facie case of benami transaction, the Initiating Officer caused a notice to the benamidar with the copy to the beneficial owner before causing provisional attachment of the properties. The allegation in the notice was contested by the appellants herein.

However, the Initiating Officer sent reference to the Adjudicating Authority after provisional attachment of the properties. The Adjudicating Authority has confirmed the provisional attachment of the properties and accordingly appeals have been preferred by the appellants herein.

Arguments of the Ld. Counsel for the appellants:

5. Counsel for the appellants submitted that out of many appeals, few are by the corporate being LLP or private limited companies. Corporates have been taken to be the benamidars. The shareholder/partner of LLP to be the beneficial owners.

6. Counsel for the appellants has given description of the 5 separate orders passed in the year 2023. The details of the separate orders against each appellant has given as follows for the clarity and better understanding:

| Sl. No. | Appeal No. | Name of Entity | Date of Impugned Order | Pg. No. |

| 1. | FPA-PBPT-287 | Adesh Ventures LLP | 14.11.2023 | 11 |

| 2 | FPA-PBPT-288 | Achal R Chaurasia | 10 | |

| 3. | FPA-PBPT-289 | Ramesh L Chaurasia | 10 | |

| 4. | FPA-PBPT-290 | ARC Vastu Nirman Pvt. Ltd. | 16.11.2023 | 11 |

| 5. | FPA-PBPT-291 | Achal R Chaurasia | 11 | |

| 6. | FPA-PBPT-292 | Ramesh L Chaurasia | 11 | |

| 7. | FPA-PBPT-293 | ARC International Pvt. Ltd. | 17.11.2023 | 11 |

| 8. | FPA-PBPT-294 | Achal R Chaurasia | 11 | |

| 9. | FPA-PBPT-295 | Ramesh L Chaurasia | 11 | |

| 10. | FPA-PBPT-296 | Adesh Agricare LLP | 20.11.2023 | 10 |

| 11. | FPA-PBPT-297 | Achal R Chaurasia | 11 | |

| 12. | FPA-PBPT-298 | Ramesh L. Chaurasia | 11 | |

| 13. | FPA-PBPT-299 | ARC Agrobasket LLP | 20.11.2023 | 11 |

| 14. | FPA-PBPT-300 | Achal R Chaurasia | 11 | |

| 15. | FPA-PBPT-301 | Ramesh L Chaurasia | 11 |

7. The challenge to the orders referred to above have been made on common ground.

8. It was submitted that the Benami Prohibition Unit (“BPU”) had not conducted any independent enquiry to draw a conclusion of benami transaction, rather, it mechanically relied upon the information supplied by the Income Tax Department. It was the information collected by the Income Tax Department out of the raid conducted on 15.02.2022 and the statements recorded thereupon. The statements so recorded by the Income Tax Department were retracted later on, thus, it could not have been relied by the respondent for causing the provisional attachment order. A reference of the retraction made by the witness, Purvi Ashara, Sameer Chaudhary, Lokesh Kumar Khavya, Saurabh Sethi, Yogesh Jangid, Sanjay Shah and Hauman Mal Tatar was given. Once the witness retracted from their statements, it could not have been relied by the respondent and otherwise respondent did not cause any independent enquiry to collect material to find out whether a case of benami transaction is made or not. In the light of the facts given above, the impugned order relying on the retracted statement of the witnesses deserved to be set-aside.

9. Ld. Counsel for the appellants, further, submitted that BPU could not have cherry picked the information to make a case of benami transaction. The respondent ought to have looked into the entire material and for which to have conducted an independent enquiry which does not exist.

10. Ld. Counsel for the appellants, further, submitted that the benami property has already been attached as taxable income of the corporate vide various orders by the Income Tax Department. It is after assessing the appellant for alleged undisclosed income and accordingly assessment order was passed. Once the income was added in the hands of the corporate, it could not have taken to be benami property of shareholder/partner. It is with the further statement that once the BPU has relied on the income-tax proceedings then they could not have taken a different view than taken by the Income Tax Department for making assessment of undisclosed income. Once the disclosed income was assessed, it could not have been taken to be a case of benami transaction. Ignoring the aforesaid, the impugned order has been passed on surmises and conjectures.

11. Ld. Counsel for the appellants, further, submitted that the theme of the benami transaction is earning of the shareholders/partners (beneficial owners) engaged in illegal betting and gambling business through which cash is alleged to have been generated. The cash was thereafter given to the third-party entities who thereafter provided accommodation entries to the corporate persons through various modalities. The allegation aforesaid could not be proved by the respondent despite burden of proof on them to make out a case of benami transaction. It is with the further statement that the shareholders and partners were discharged by various Courts in regard to the allegation of illegal betting and gambling, thus, it could not have been accepted to be a case of generation of cash out of illegal betting and gambling. The Adjudicating

Authority failed to appreciate the aforesaid aspect. In fact,

there was no question of cash generation or accommodation entries and therefore, impugned order has been caused without appreciation of facts on record.

12. Ld. Counsel for the appellants submitted that the partners/shares of the LLP, namely, Shri Rakesh Chaurasia and Shri Achal Chaurasia were held to be beneficial owners while the corporate to be the benamidars without considering that corporate could not have held to be the benamidar of which the partners/shareholders to be the beneficial owners. The finding has been recorded even in ignorance of the fact that partners of the LLP or the shareholders of the entities infused funds by way of capital or loan. The infusion of the capital or loan could not have been taken to be a benami transaction and therefore the impugned order deserves to be interfered.

13. Counsel for the appellants, further submitted that the alleged accommodation entries were in fact received from third party in various modalities with capital infusion, unsecured loan, capital gains and sale of land. However, the respondent without any enquiry and application of mind alleged the transaction to be accommodation entries. In fact, the said transactions were legal commercial transactions undertaken in the commercial wisdom and business prudence of corporate. The aforesaid aspect has also been ignored by the Adjudicating Authority, thus, interference in the impugned order may be caused holding appeals to be the beneficial owners and benamidars respectively.

14. Ld. Counsel for the appellants did not raise any other argument despite an opportunity given to the Ld. Counsel for the appellants by this Tribunal, rather, Ld. Counsel closed his argument with the prayer for acceptance of the appeals.

Arguments of the Ld. Counsel for the respondent:

15. Ld. Counsel for the respondent made elaborate arguments to contest the issues raised by the appellants. It would be referred while recording our findings on each issue raised by the appellants to avoid repetition of the same facts and for the sake of brevity.

Findings of the Tribunal:

16. The fact on records shows that a search was conducted by the Income Tax Department on 15.02.2022 in the premises of Shri Ramesh Chourasia and Anchal Chaurasia and ARC Group entities. It was revealed that AV LLP (ARC Group) is engaged in online gambling and betting through multiple websites such as www. gamekingindia. co. in, www. planetgonline. com and others in the garb of gaming sites, video game portals, gaming centres and cyber cafes. The huge unaccounted fund generated by the group from online gambling and betting was routed in the books of accounts by way of bogus security premium, bogus partners capital, bogus unsecured loan, bogus commission income, bogus trading and bogus capital gain.

17. The allegations aforesaid were defended by the appellants by filing reply to the notice served by the Initiating Officer followed by the Adjudicating Authority on a reference after causing provisional attachment order by the Initiating Officer.

18. The first argument raised by the appellants is that the BPU did not cause an independent enquiry to collect the material for making out a case of benami transaction. It has relied on the material seized by the Income Tax Department during the course of search and the statements recorded therein. No independent material was collected by the respondent by causing an enquiry and therefore the entire proceedings for provisional attachment of the properties after holding it to be the benami transaction deserves to be set-aside.

19. The argument has been defended by the respondent. It is submitted that there is no illegality if the Initiating Officer relies on the material supplied by the Income Tax Department which may be the documentary evidence apart from the statement of the witness recorded under Section 132(4) of the Income-tax Act, 1961. There is no bar under the Act of 1988 or vis-à-vis under the Income Tax Act to rely the evidence collected under one set of statute. Ld. Counsel for the appellant could not make a reference of any of the provision of the Act of 1988 causing bar for placing reliance on the material collected by the Income Tax Department during the course of search under the Income Tax Act. The emphasis of the appellant thereupon remained that burden of proof is on the agency alleges benami transaction and cited the judgment to support his arguments. There is no quarrel that burden of proof of the benami transaction lies on the person alleges benami transaction. The issue would be as to whether it has been discharged by the respondent or not and for which conclusion would be drawn after analyzing the evidence on record. However, before we proceed to analyze the evidence, we need to conclude that there is no prohibition or bar to rely on evidence collected by the Income tax authorities. Accordingly, we do not find any illegality in the action of the respondent to place reliance on the material collected by the Income tax authorities during the course of search and further proceedings.

20. We may now analyze the issue as to whether the material on record makes out a case of benami transaction. The modus operandi of the appellant has been given which is to infuse the cash and route it through other companies to ultimately reach to the benamidar. At the first instance when the beneficial owner has routed the cash in other companies, a case of benami transaction would make out and further transaction have to be governed by Section 6 of the Act of 1988 because ultimately benami property reaches to the benamidar company of which beneficial owner may be the shareholders or the promoters. If they were required to infuse the money in the benamidar company, they were not required to route the same through other entities but could have infused that money in the benamidar company directly and in that case the argument raised by the appellant would have been worth of acceptance. However, in the instant case the beneficial owner infused the money in favour of other companies to reach ultimately to the benamidar company. With the adoption of the route at the first instance, a case of benami transaction was made out because money was not infused by the beneficial owner in his own company but it routed through other companies and with the adoption of the route at the first instance, a case of benami transaction was made out.

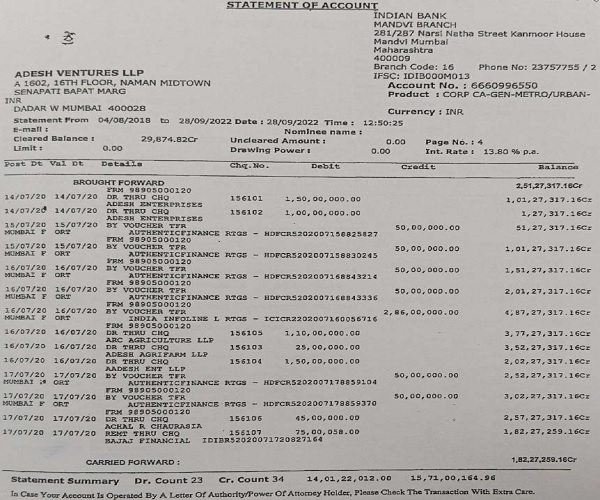

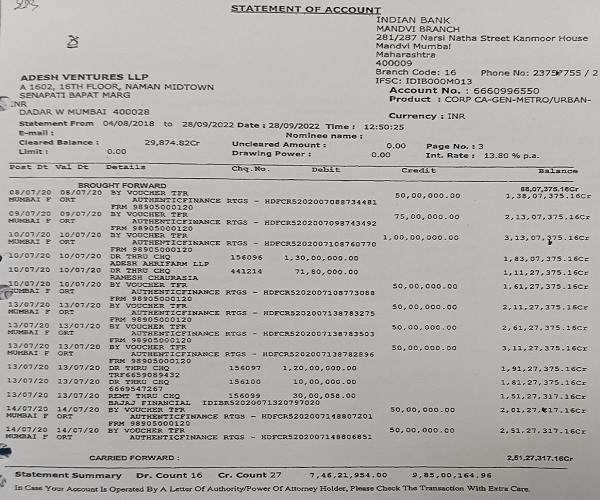

21. The main issue now remains as to whether the material supplied to the respondent was sufficient to make out a case of benami transaction. For the aforesaid, we need to analyze the evidence on which reliance has been placed. During the course of search, electronic evidence to show routing the cash and keeping account/ managing record of such movement under the head “Hisab” was recovered. The statement of Sameer Chowdhary (CA of AV LLP / ARC Group) was recorded who stated that he was managing the cash and routing it through ARC entities. He accepted to have provided accommodation entry to the tune of Rs. 1000 Crores into ARC entity.

22. Apart from the statement of aforesaid, statement of Purvi Ashara was also recorded. She explained the contents of monthly PDF sheets and stated that cash was given to CA Sameer Chowdhary against the amount received from M/s Parineeta Commercial Private Limited. The statement was to corroborate by receipt of cash with accommodation entry found in the whatsapp chat ground “working group 2” in which CA Sameer Chowdhary was part of the chat group and has accepted the amount as accommodation entry in exchange of cash.

23. The respondent have relied on the digital evidence introducing cash into books of account of ARC entity and taken it to be corroborative evidence. Digital excel sheet by the name of “OCTONWARD FINAL” was found in which cash entries were recorded against the transactions carried out by the ARC entities. The Accountant, Purvi Ashara recorded the cash transaction in “Hisab” of the group to introduce the cash in book of accounts through accommodation entry. She had created a different worksheet in the “Octonwards Final” in the name of persons who were arranging the entries and thus she had recorded both the sides of the transaction i.e. date wise and entity wise fund movement in the bank account and corresponding cash sent or delivered for the transaction. It was, thus, found that the evidence was available not only in the form of statement of the persons to show a benami transaction but was corroborated by the electronic evidence of which further reference would be given by us not only in reference to the statements recorded during the course of search but the statement of the relevant witnesses recorded thereafter. The respondent Department was having material to prove a case of benami transaction and for which they have not only relied on the statement recorded by the Income Tax authorities but the electronic evidence collected during the course of search, thus the statements were corroborated with the material.

24. It is with the further clarification that the respondent could have placed reliance on the statement and the electronic evidence collected by the Income Tax authorities to find out a case of benami transaction. This even answer the question raised by the appellant about their involvement in betting and gambling. The respondent could prove generation of cash out of betting and gambling in reference to the statement of the witnesses out of which we have given reference of two witnesses, otherwise, statement of other witnesses i.e. Lokesh Kumar Khavya, Saurabh Sethi, Yogesh Jangid, Sanjay Shah and Hauman Mal Tatar were further fortified the allegations which could not be nullified by the appellants. They could not defend the allegation of cash transaction out of gambling and betting and thereupon routing it through accommodation entries. The appellant rather submitted that the amount came to ARC Group was out of the premium, capital, unsecured loan, commission and other transactions. It was found that as against the capital contribution, the fund infused by the company in share and in the mutual funds is Rs. 82.37 Crores while initial capital contribution was Rs.2,00,000 and thereupon to be of Rs.18000 as fixed capital by M/s Penant Commotrade Pvt. Ltd. and Rs.20000 by M/s Authentic Finance Pvt. Ltd. It is apart from the fact that the ARC group said to have received unsecured loan with the admission that no repayment of loan was made. The defence aforesaid is falsified when the appellant made a reference of the income-tax assessment showing income out of agriculture which defence was not taken earlier but was to seek assessment of undisclosed income. The theory of involvement of loan and income from other business remain in contradiction, thus cannot be accepted. The appellant, ARC group and the individuals did not disclose agriculture income other than the service and no amount was disclosed towards expenses for agriculture. The agriculture income was disclosed in the revised return after the order passed by the Initiating Officer for provisional attachment and the transaction taken to be benami. It is for the reason that even the legal income can be involved in benami transaction and for which we can give illustration. If a person is having income from disclosed income and such income is transferred to a third person to purchase a property in his name and it results in registration of the land in the name of the third person, then despite disclosed income, if transferred to third party, it would be taken to be a benami transaction. Merely for the reason that Income-tax Department has assessed undisclosed income used for benami transaction, it cannot be ignored. It is more so when the stand of the appellant for generation of fund was in contradiction and in conflict with source of income for the Income Tax Department and separately to save it from benami transaction. The conflicting stand of the appellant may have ignored by the Income Tax Department but would not be binding on the respondent to determine the issue as to whether a case involves benami transaction or not.

25. At this stage, we would further deal with the issue raised by the appellant that the Income Tax Department has assessed the income based on the evidence collected by them, thus respondent could not have taken a different view. The argument has been raised in ignorance of different sets of proceedings. The Income Tax Department has relied the material to come to the conclusion about the undisclosed income and thereupon to make assessment for the taxing purpose whereas the respondent made a scrutiny of the case to find out whether a case of benami transaction is made out. It has placed reliance on the same material but for different purpose and under different set of proceedings. The object of the Income Tax Department is to deal with the case for Income Tax purpose while the respondent to deal with the case under the Act of 1988. Therefore, with the illustration we have given, it cannot necessarily be concluded that once Income Tax Department has assessed the undisclosed income, such income should not be accepted for benami transaction despite making out a case. In view of the above, we are unable to accept any of the arguments raised by the appellants.

26. The reference of few statements has been given by us, however, we further analyze the case. The complete modus operandi of routing the cash and for keeping the account, it was recorded in “Hisab”. At this stage, we may refer to certain material relied by the respondent and has been analyzed by the Adjudicating Authority. The relevant para 5.1 is quoted hereunder for ready reference:

5.11 From the “Octonwards Final” it is seen that M/ s. Adesh Ventures LLP has received funds in the form of unsecured loans and partner’s capital from Penant Commotrade Put. Ltd. and Authentic Finance Put. Ltd. The amount has been received as unsecured loans and partner’s capital from these entities against the cash which has been recorded by Smt. Purvi Ashara in its “Hisab” under the worksheet of Sh. Sameer Chaudhary naming it as “SC”. The amounts in the sheet match with the amount received in the bank account of M/ s. Adesh Ventures LLP.

Thus “Octonwards Final” reflects true nature of the corresponding bank entries which have been arranged for in lieu of cash paid. The said entries maintained electronically rendering the true picture of how the LLP is used as a name lender to bring unaccounted /illegally generated cash into mainstream of commerce. The extract of bank statements is reproduced in which the accommodation entries from Authentic Finance Put Ltd can be clearly seen for reference.

—

An excel sheet named “Octonwards final” which was uploaded on Google drive associated with ashafaassociatesl@gmall.com was found. On perusal of the said excel sheet, it can be seen that the entries in the bank statements are matching with entries in the “Octonwards final” file, this is further corroborated by statement of Smt. Purvi Ashara who has explained the modus operandi as to how the record of accommodation entries in lieu of cash exchange was handled…..

27. We may further refer to the relevant question raised and answered by the witness regarding OCTONWARD sheet and is quoted hereunder:

Q.21 As per your response to the previous question, the Income from online betting activities is not reflected in the Books of Accounts. Instead, the Income is shown only from Commission, Real Estate and Agricultural Business. As the person In-charge of preparing Books of Accounts of the ARC group, you are asked to answer as to where the cash received from online gambling and betting is reflected in the Books of Accounts?

Ans. Madam, I confirm I am the Accountant of the ARC group. I do not know the exact details of how the cash is generated. However, Shivbabu Chaurasia of the ARC group shares with me a monthly cash “hisab”. The cash that is reflected in the monthly “hisab” is only that cash, in exchange for which cheque entries/ bank entries are arranged from various 3rd party entities. The cheque entries are arranged by Mr. Samir Choudhary, CA, Mr. Yogesh Jangid, CA and Mr. Ravi Trithani, CS. Further, I make and maintain a monthly summary of the cash delivered to these entities (as per the hisab) and the corresponding cheque/ bank entries received in the bank accounts of ARC group companies. No entry of cash income is made in the books of account.

Q.22 Explain in detail what is your role in the modus operandi of the ARC group entities?

Ans. Madam, as I have stated above, my role is the following:

-

- I make and maintain a monthly summary of the cash delivered to third party entities (as per the hisab sent to me by Mr. Shivbabu Chaurasia) and the corresponding cheque/ bank entries received in the bank accounts of ARC group companies.

Further, this fact is substantiated by the statement given by CA Sameer Choudhary in which he has stated that he has provide accommodation entries for ARC group. Relevant part of the statement is reproduced below:

Q.14 Please explain the kind of consultancy provided by you to ARC Group.

Ans. Sir, as far as I know, Rakesh, Achal and Aadesh Chaurasia are also in the business of online gaming through which cash is generated. I am not involved in the cash generation part. I am handed over some cash from time to time by ARC and I think the cash handed over to me is from online gaming business. I help the ARC Group to systematically route this cash into books of account of several companies in ARC Group as accommodation entries, There is a person by name Shiv Chaurasia who contacts me on Whatsapp from his number +1 520 433 3783. He is ARC Group’s single point of contact for me for cash handling. He informs me that cash is available with him and as mutually agreed the cash is delivered to my office in Opera House at Panchratna building mostly through his employee Manoj (+91 88550031701) and seldom through other persons like Tharu,. Ashish etc. but apart from Manoj, I do not have any contacts/ phone numbers of them with me. The cash so handed over to me, I use various contacts of mine in the market to procure RTGS entries into bocks of account of ARC Group. For providing this consultancy service, I am paid commission of 0.5% if entry is in the form of income, And 0.24% per annum of interest component if it is taken as unsecured loan (if loan is 100 Cr and interest is 12%, annual interest is 12 Cr. and I am paid 24% of 12 Cr.). I have been doing this work for ARC Group since 2016. I receive this consultancy income in cash and I offer this as income in my ITRs by inflating billings from my existing clients (for example if I have to show Rs. 10 as consultancy income, and I have an existing client A who would bill me Rs. 100 for my work, I will make my client A offer me Rs. 110 and give him Rs. 10 back in cash.)

Q.23 What is your association with Amrit Sales Promotion Pvt. Ltd.

Ans. Amrit Sales Promotion Pvt. Ltd. is a company under ENSO group of companies. It is operating from building no. 3, Navjivas Commercial Premises, Lamington Road, Mumbai. I have done tax audit for it in 2019-2020 and 2020-2021. In 2018-19, I have helped the ARC group in infusing 96 crores capital from Amrit Sales Promotion Pvt. Ltd. and more ENSO group of companies. The other six ENSO group companies are – Kalyan Vyasper Pvt. Ltd., Takmin Trading Pvt. Ltd, August Trading Pvt. Ltd., symphony Merchante Pvt. Ltd. TCK Finance and Leasing Pvt. Ltd. and Yashodham Merchants Pvt. Ltd. Out of the above amount 50 crore was the actual investment and rest accommodation entries. I arranged for accommodation entries from these companies. I cannot recollect the exact amount of accommodation entry from each company as these are old transactions and we had destroyed the chits for those. I received 0.5% commission for the accommodation entries. I offered this in my books of account by inflating professional service charges from my genuine client. Which exact clients. I am unable to recall because these are old transactions.

28. The relevant statement and the reference of the electronic document have been quoted to find out whether sufficient evidence was available to find out a case of benami transaction. It is necessary to add that for reliance on the electronic evidence, necessary certificate was obtained by the respondent. The electronic evidence was sufficient to corroborate the statement of the witnesses.

29. Counsel for the respondent has made a reference of the retraction of the statement of the witnesses without realizing that retracted statement can be relied if corroborative evidence existed. It is with the clarification that retraction of the statement cannot be for the sake of it, rather, it is not that statement was recorded in the custody so as to make a case of retraction unlike in the case of the Customs and under similar legislation. The retraction of the statement cannot be accepted for the sake of it as no justified reason for it was given with proof and otherwise statement of the witness is corroborated by the electronic evidence collected by the respondent.

30. It is a case where the beneficial owner generated unaccounted cash out of the gambling and betting and thereupon was channelized through the entities to infuse it in the LLP and other entities of ARC group. It was, thus, rightly taken a case of benami transaction where the infusion of money by the partners/ shareholders is not by simply putting the capital or extending loan, rather, it is a case where money was routed through accommodation entries in favour of benamidars for future benefit of the beneficial owner. Thus, a case of benami transaction was rightly taken by the respondent and has been proved. It got proved at the first instance when beneficial owner diverted the money for accommodation entry for his further benefit which happened with further transfer to the benamidar.

31. We may, further, refer the argument of the appellants for relying third party bank account sheet without showing its to the appellant. The argument has been raised without realizing that the respondent successfully referred the evidence to make out a case of benami transaction. The benamidar infused the money further for purchase of shares and mutual funds and for which Director, Shri Hanuman Mal Tater in his statement has categorically accepted for providing accommodation entries through his company to AFPL group entries. Shri Sameer Chowdhary, CA of ARC Group of entities was also in contact with the Director of AFPL for providing accommodation entries. It is a fact that the accommodation entry was shown as loan without referring to any loan document or its repayment. Thus, the Adjudicating Authority had rightly drawn his conclusion in regard to the benami transaction. It is apart from the fact that ARC group of entities having no business. The respondent has successfully relied the material collected by the Income Tax Department to show use of various websites for gambling and betting which remain unexplained by the appellant in the set of appeals.

32. The oral argument was raised about the interference in the FIR containing allegation of gambling and betting. The argument has been raised without realizing that in the criminal case the standard of proof is different than for the Civil proceedings and otherwise the material available on records is sufficient to draw conclusion for involvement of the appellants in gambling and betting which resulted in generation of cash. The set of evidence produced before the Criminal Court may be different than the evidence relied by the respondent in this case. It is to be clarified that for the criminal case, the prosecution has to prove its case beyond doubt and for that they may have relied the evidence collected during the course of investigation wherein in the present matters there is no such rigour, rather, material collected by the Income Tax Department can be relied in the proceedings for the Act of 1988. Thus, in view of above, the case of the appellants cannot be accepted in their favour.

33. In the light of above discussion, we do not find any merit in the arguments raised by the appellants and accordingly appeals fail and are dismissed.

Author Bio