Related Party and Related Party Transaction

In India statistics indicate that maximum of total enterprises are family-controlled businesses which contribute to substantial portion of the total employment. Unlike transactions with third parties , the distinguishing factor of an Related Party Transaction is the special relationship between the parties transacting, which if misused , can lead to serious consequences. The instances of Related Party transactions (RPTs) can cause actual or potential conflict of interest between the company and its shareholders.

In this article an overview is given how and what have been clarified about related party and related party transaction by different government bodies and act.

Related Party:-

A “related party” is a person or an entity that is related to the reporting authority . The person includes a legal person who can be individuals, company, firm, LLP, Co-operative society, local authority. It also includes entities incorporated outside India.

Before we discuss related party and Related Party Transaction we would come across few terminologies which needs to be clarified.

Arm’s Length Basis:

“Arm’s Length” is an expression which is commonly used to refer to transactions in which two or more unrelated and unaffiliated parties agree to do business , acting independently and in their self-interest.

Arm’s length price is a price at which a willing buyer and a willing unrelated seller would freely agree to transact or a trade between related parties that is conducted as if they were unrelated, so that there is no conflict of interest in the transaction.

A company named XYZ,UK entered into a contract with its subsidiary company ABC, USA, for the purchase of raw material. The price per kg of raw material was decided for 10 pound. Had XYZ,UK purchased the raw material from other vendors supplying the same raw material located in the USA, they would have got the raw material at a price of 7 pound per kg.

Here, XYZ, UK has tried to increase its expenses by purchasing from a related party at a higher price (10 pound) than the fair price (7 pound). By doing so, it has attempted to shift its profits to its related party located in the USA. Clearly, the motive is to save taxes in the UK and shift the profits to USA.

The transaction between XYZ,UK and ABC USA is not at arm’s length. Had the price agreed between them would have been within a reasonable range of 7 pound, then it would have been at arm’s length.

As per section 188 of Companies Act,2013 arm’s length price transaction means a transaction between two related parties that is conducted as if they were unrelated , so that no conflict of interest.

As per section 92F define Arm’s length price is the price applied or proposed to be applied , when two unrelated persons enter into a transaction is uncontrolled conditions.

Unrelated person- As per section 92A , the persons said to be unrelated if they are not associated or deemed to be associated enterprise.

Uncontrolled conditions are that conditions which are not controlled or suppressed or moulded for achievement of a predetermined results.

Where an assessee has entered into various types of international transactions with associate enterprise , arm’s length should be determined on a transaction by transaction basis not on an aggregate basis.

Underwriting the subscription:

With subscription , the purchaser of the financial product applies to acquire them directly from the issuer . With underwriting , a financial company e,g, bank assumes the risk and commitment of reselling the total issue of the product to individual investor. The types of underwriting are a) loan underwriting b) insurance underwriting c) securities underwriting.

Any office or place of profit in Company:

Office or place of profit means any office or place where such office or place is held by a director receives from X company anything by way of remuneration over and above the remuneration to which he is entitled as director by way of salary, fee, commission, perks, any rent-free accommodation.

Significant Influence:

Significant influence may be exercised in several ways for example , by representation on the Board of directors, participation in the policy making process, material inter-company transaction, interchange of managerial personnel or dependence on technical information.

Listed and Unlisted Company:

A listed company is a public company. It has issued shares of its stock through an exchange.

An unlisted company can be public limited or private limited and not listed on any stock exchange.

Related party as per SEBI ( Securities and Exchange Board of India)

With an aim to review and strengthen the regulatory norms pertaining to RPTs, undertaken by listed entities in India, SEBI constituted a Working Group in November 2019 comprising members from the Primary Market Advisory Committee (PMAC), including persons from the Industry, Intermediaries, Proxy Advisors, Stock Exchanges, Lawyers, Professional bodies, etc.

As per existing provisions in the LODR (Listing Obligations and Disclosure Requirements )

a) Regulation 2 (zb) of LODR Regulations defines “related party” as related parties defined under section 2(76) of the Companies Act, 2013 or under the applicable accounting standards.

b) LODR Regulation further deems any person or entity belonging to the promoter or promoter group of the listed entity and holding 20% or more of the shareholding of the listed entity, to be a related party.

As per recommendation of the Working Group

a) All persons or entities belonging to the ‘promoter’ or ‘promoter group’, irrespective of their shareholding in the listed entity, shall be deemed to be related parties.

b) Further, any person or any entity, directly or indirectly (including with their relatives), holding 20 percent or more of the equity shareholding in the listed entity, shall be deemed to be a related party.

Related Party as per Companies Act, 2013

According to section 2(76) of the Company’s act , 2013 related party with reference to company means –

i) a director or his relative;

) a key managerial personnel or his relative;

i) a firm, in which a director, manager or his relative;

ii) a private company in which a director or manager or his relative is a member or director;

iii) a public company in which a director or manager is a director and holds along with his relatives, more than 2% of its paid-up capital;

iv) any body corporate whose Board of Directors, managing director or manager is accustomed to act in accordance with the advice, directions or instructions of a director or manager.

v) any person on whose advice, directions or instructions a director or manager is accustomed to act provided that nothing in sub-clauses (vi) and(vii) shall apply to the advice ,directions or instructions given in a professional capacity.

vi) any body corporate which is-

A) a holding , subsidiary or an associate company of such company;

B) a subsidiary of a holding company to which it is also a subsidiary ; or,

C) an investing company or the venturer of a company means a body corporate

Let’s say , Mr X,Y and Z are directors of Company XYZ Ltd.. The related parties for the company, in general, are as under:

1. A director or his relative. Relative means a member of the same HUF , husband, wife, father, stepfather, mother, stepmother, son, stepson, daughter, stepdaughter, son’s wife, daughter’s husband, brother, stepbrother, sister, stepsister.

Mr X, Mr Y and Mr. Z are directors and the relatives of these Directors are considered as related parties.

2. Key managerial personnel or his relative

Say, Mr A is a Company Secretary , his relatives will be considered as related parties.

3. A firm in which a director, manager or relative is a partner

Mr X is a partner at PQR Pvt. Ltd., another firm. This firm will also be considered as a related party.

4. A private company in which a director , manager , or relative is a member or director

Mr. Y is a director of B Pvt. Ltd.- in this case B Pvt. Ltd. Becomes a related party. Even when Mr Y’s relative is a member or director in B Pvt. Ltd., this company will be considered as a related party.

5. A public limited company in which a director or manager is a director and holds along with his relatives more than 2% of its paid-up capital

Mr Z along with his relatives holds more than 2% of the paid-up capital of C Ltd.. In this case ,Mr Z will be considered as a related party.

6. Any body corporate whose board of directors , MD or manager is required to act in accordance with the advice , directions or instructions of a director or manager(Not applicable in cases when these directions are followed in a professional capacity).

When P Ltd. acts on the directions of Mr. X, P Ltd. will be a related party.

7. Any person on whose advice , directions or instructions a director or manager is required to act (Not applicable when this done in a professional capacity)

Mr A holding 51% in XYZ Ltd. on whose advice Mr. X has to act will be considered as a related party.

8. Holding , Subsidiary or Associate of such company

These all will be considered as related parties:

– ABC Ltd holding 51% in XYZ Ltd. (Holding Company)

– XYZ Ltd. holding 51% in LMN Ltd. (Subsidiary Company)

– PQR Ltd. holding 30% in XYZ Ltd. (Associate Company)

9. Any subsidiary which is a subsidiary of a holding company to which it is also a subsidiary.

PQR Ltd. & XYZ Ltd. are both subsidiaries of ABC Ltd.. Thus PQR Ltd also becomes a related party.

Related Party as per Goods and Service Tax( GST)

Legal persons and persons who are associated in the business of one another in that one is the sole agent or sole distributor or sole concessionaire, of the other. Further, related parties are also referred to as related persons or distinct persons under GST. Persons include a legal person who can be individuals, HUF, company, firm, LLP, co-operative society, a body of individuals, local authority, government, or an artificial juridical person. It also includes entities incorporated outside India. Persons who are associated with one another’s business or is a sole agent or sole distributor or sole concessionaire shall be deemed to be related.

Related persons are defined u/s 2(84) of the GST Act. Persons shall be deemed to related if they fall under any of the categories below:

a) Officer or director of one business is the officer/director of another business

b) Businesses legally recognised as partners

c) An employer and an employee

d) Any person who holds at least 25% of shares in another company , either directly or indirectly

e) One of them controls the other directly or indirectly

f) They are under common control or management

g) The entities together control another entity

h) The promoters or managerial persons are members of the same family

Related Party as per Income tax Act,1961

As per section 2(41) of Income Act,1961 the relative means in relation to individual means spouse, brother or sister or any lineal ascendant or descendant of that individual.

As per section 56(2) of the Income tax Act ,1961 relative means in case of an individual –

a) Spouse of an individual

b) Brother or sister of the individual

c) Brother or sister of the spouse of the individual

d) Brother or sister of either of the parents of the individual

e) Any lineal ascendant or descendant of the individual

f) Any lineal ascendant or descendant of spouse of the individual

g) Spouse of the persons referred to in items (b) to ( f)

Summing up, the related parties for the company shall be the directors themselves and their relatives such as the spouse, father, stepfather, mother, stepmother, son, son’s wife, stepson , daughter, stepdaughter , brother, stepbrother , sister, stepsister , daughter’s husband etc.

Related Party as per Customs:

Customs looks at the seller and buyer relationship because that relationship may affect the price , which may affect the value being declared on the customs entry.

The term “related” has been defined in Rule 2 (2) of the CVR to provide that buyer and seller shall be deemed to be “related” if

- They are officers or directors of one another’s businesses;

- They are legally recognized partners in business;

- They are employer and employee;

- Any person directly or indirectly owns, controls or holds five per cent or more of the outstanding voting stock or shares of both of them;

- One of them directly or indirectly controls the other;

- Both of them are directly or indirectly controlled by a third person;

- Together they directly or indirectly control a third person; or

- They are members of the same family.

Therefore, typically all transactions involving import of goods by an Indian company and its holding company or any associated/affiliated Group company located outside India are considered to be transactions between related parties which are investigated by the Customs authorities.

Related Party as per Accounting Standards Accounting Standard-18

Related party means at any time during the year, one party has an ability to: Control the other party, exercise significant influence over the other party in making financial and/or operating decisions.

Here control means

a) ownership , direct or indirect of more than 50% of the voting power of an enterprise. In case of company control of the composition of the board of directors

b) substantial interest in voting power and power to direct the financial and / or operating policies of the enterprise.

The objective of this standard is to establish requirements for disclosure of

a) related party relationship

b) transaction between a reporting enterprise and its related parties

Related party transaction is transfer of resources or obligations between related parties, regardless of whether or not a price is charged.

As per AS-18 a relative broadly includes-

- Associate Companies

- Subsidiaries

- Fellow Subsidiary

- Intermediary Companies

- Controlled Companies

- Holding Company

- Key Managerial Personnel and there relatives

- Individuals owning direct or indirect interest in Enterprise the voting power of the reporting enterprise or having significant influence over the reporting company or relatives of such individuals.

As per AS-18 KMP means Key Managerial Personnel which includes “those persons who have the authority and responsibility for planning, directing and controlling the activities of the reporting enterprise”.

Indian Accounting standard 24:

Indian Accounting Standard 24 requires disclosures to be made by a parent entity regarding its transactions , outstanding balances with entities i.e. associates, joint ventures or subsidiaries, collectively referred to as Related party. Hence related party refers to an entity or person that is related to the reporting entity

The objective of IAS 24 is to ensure that an entity’s financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit or loss may have been affected by the existence of related parties and by transactions and outstanding balances, including commitments, with such parties.

A related party is a person or entity that is related to the entity that is preparing its financial statements (in this Standard referred to as the ‘reporting entity’).

(a) A person or a close member of that person’s family is related to a reporting entity if that person: (i) has control or joint control of the reporting entity;

(ii) has significant influence over the reporting entity; or

(iii) is a member of the key management personnel of the reporting entity or of a parent of the reporting entity.

(b) An entity is related to a reporting entity if any of the following conditions applies:

(i) The entity and the reporting entity are members of the same group (which means that each parent, subsidiary and fellow subsidiary is related to the others).

(ii) One entity is an associate or joint venture of the other entity (or an associate or joint venture of a member of a group of which the other entity is a member).

(iii) Both entities are joint ventures of the same third party.

(iv) One entity is a joint venture of a third entity and the other entity is an associate of the third entity.

(v) The entity is a post-employment benefit plan for the benefit of employees of either the reporting entity or an entity related to the reporting entity. If the reporting entity is itself such a plan, the sponsoring employers are also related to the reporting entity.

(vi) The entity is controlled or jointly controlled by a person identified in (a).

(vii) A person identified in (a)(i) has significant influence over the entity or is a member of the key management personnel of the entity (or of a parent of the entity).

The entity, or any member of a group of which it is a part, provides key management personnel services to the reporting entity or to the parent of the reporting entity.

Key management personnel are those persons having authority and responsibility for planning, directing and controlling the activities of the entity, directly or indirectly, including any director (whether executive or otherwise) of that entity.

Case-1 Director/KMP and his relative

Related Party Transaction:

Related Party Transaction can be understood as a deal or arrangement made between two parties or entities who are joined by a pre-existing business relationship or common interest. It is a transfer of resources , services or obligations between a reporting entity and a related party, regardless of whether a price is charged.

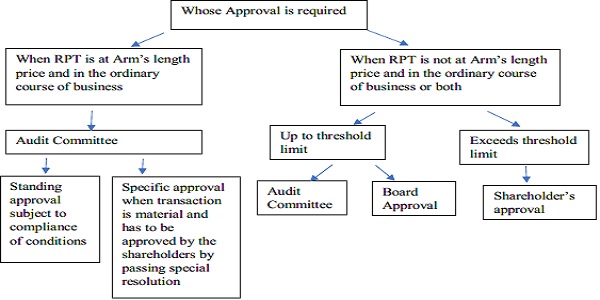

All related party transactions require approval of Audit Committee. All contracts that are (1) not in the ordinary course of business but at arm’s length (2) in the ordinary of course of business but not at arm’s length or (3) not in the ordinary course of business and not at arm’s length require prior approval of board of directors or shareholders based on certain thresholds.

Penalties: Any director or any other employee of the company , who had entered into or authorised the contract in violation, as per section 188 of the companies act they are punishable :-

a) In case of listed companies, imprisonment upto 1 year or fine from 25,000 to 5 lakhs or both

b) In case of other companies , fine from 25,000 to 5 lakhs.

Main purpose of Related Parties regulation:- To regulate transactions between the company , its subsidiaries and its related parties with a view to ensure that such transactions are executed on an arm’s length basis and is transparent and fair manner.

Why are Related Party Transactions are important?- They provide transparency on how its financial position and financial performance may be affected by transaction with related parties which may or not be conducted on an arm’s length basis.

Under the new law, in relation to every RPT, directors have to necessarily check most importantly the following two criteria-

a) Whether the contracts or arrangements is in the “ordinary course of the business” of the company

b) Whether the terms and conditions of such contracts or arrangements are on “arms length basis”.

The transaction will be with Related Party in case it is with any of the following:-

a) With any Director of Company

b) With any relative of a Director

c) With any KMP or relative of a KMP

d) With any firm in which Director or his relative is a partner.

e) With any private Company in which a Director is a member or Director)

f) With a Public Company in which a Director is a member or Director and additionally holds along with his relative(s) 2% or more paid-up share capital of a Public Company.

g) With a Subsidiary Company

h) With an Associate Company in which Company has more than shareholding

i) With a body corporate which is significantly influenced by a Director of a company

j) With a person who has control or significant influence over the Company.

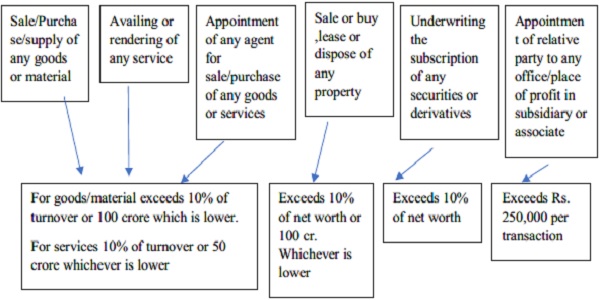

Following transactions with above related parties will constitute related party transactions:-

a) Sale, Purchase or supply of any goods or material by a Company

b) Selling or disposing off or buying any property by Company

c) Leasing of any property by Company

d) Availing or rendering of any services by Company

e) Appointment of any agent for purchase or sale of goods, materials, services or property by Company

f) Any related party’s appointment to any office or place of profit in Company

g) Company or its subsidiary Company or its associate Company

h) Underwriting the subscription of any securities or their derivatives of Company

To determine a transaction a related party transaction following points to be ensured:-

a) The transaction should be entered on an Arm’s length basis

b) Take prior approval of Audit Committee of the Board in respect of all related party transactions

c) Approval of shareholders through special resolution if the related party transaction during a financial year exceeds 10% annual consolidated turnover of a company.

d) Prior approval of the Board is required in case a related party transaction is not in the ordinary course of business and not on an Arm’s length basis.

Related-party transactions are legitimate activities and serve practical purposes:

- They are recognized in corporate and taxation laws.

- They have their own standards for accounting treatment.

- Systems of checks and balances have been built around them to make sure they are conducted within these boundaries.

Why related-party transactions, and why now?

- Any listed company that is big and liquid enough to be on the radar of foreign investors is likely to be a part of a larger business group, either as its flagship or as one of its affiliates. Some of its affiliates may also be listed, while others are privately held.

- Ownership of a company is likely to be concentrated in a single group: a family or the state. In family-controlled entities, senior management and board positions, including director and key managerial personnel, are often filled by family members. In state-controlled entities, these roles are filled by political appointees. In other words the business is managed by a dominant shareholder who also has controlling ownership. These affiliations formed under the umbrella of common ownership are not just on paper; they are exploited as needed. The dominant control structure makes it easy for related-party transactions to take place, especially when some of the entities complement or exist to support the operations of others.

What is the objective of related party transaction?

The objective of IAS 24 is to ensure that an entity’s financial statements contain the disclosures that it’s financial position and profit or loss may have been affected by the existence of related parties and by transactions and outstanding balances with such parties.

Diagram of Related Party Transaction:

Related Party Transactions as per SEBI

As per existing provisions in the LODR

Regulation 2 (zc) of LODR Regulations defines RPT as any transfer of resources, services or obligations between a listed entity and a related party regardless of whether a price is charged or not and a “transaction” with a related party shall be construed to include a single transaction or a group of transactions.

As per recommendation of the Working Group

“RPT” means a transaction involving a transfer of resources, services or obligations between:

i. the listed entity or any of its subsidiaries on one hand and a related party of the listed entity or any of its subsidiaries on the other hand; or

ii. the listed entity or any of its subsidiaries on one hand, and any other person or entity on the other hand, the purpose and effect of which is to benefit a related party of the listed entity or any of its subsidiaries.

Thresholds for classification of RPTs as material

As per existing provisions in the LODR

Regulation 23 (1) of LODR Regulations inter-alia specifies that transaction with a related party shall be considered material if the transaction(s) to be entered into individually or taken together with previous transactions during a financial year, exceeds 10 percent of the annual consolidated turnover of the listed entity as per the last audited financial statements of the listed entity.

As per recommendation of the Working Group

Any transaction with a related party shall be considered material if the transaction(s) to be entered into individually or taken together with previous transactions during a financial year, exceeds Rs.1,000 crore or 5 percent of the annual total revenues, total assets or net worth of the listed entity on a consolidated basis as per the last audited financial statements of the listed entity., whichever is lower, provided that the criterion relating to net worth shall not be applicable if the net worth of the listed entity is negative.

Approval requirements of the Audit Committee

As per existing provisions in the LODR

Regulation 23(2) of LODR Regulations mandates that all RPTs shall require prior approval of the audit committee.

Recommendation of the Working Group

a) All RPTs and subsequent material modifications shall require prior approval of the audit committee of the listed entity.

b) RPTs to which the subsidiary of a listed entity is a party but the listed entity is not a party, shall require prior approval of the audit committee of the listed entity. Such approval is mandatory only if the value of RPT (whether entered into individually or taken together with previous transactions during a financial year) exceeds 10 percent of the annual total revenues, total assets or net worth of the subsidiary, on a standalone basis, for the immediately preceding financial year, whichever is lower, provided that the criterion relating to net worth shall not be applicable if the net worth of the subsidiary is negative.

c) Further, prior approval of the audit committee of the listed entity shall not be required for RPTs of listed subsidiaries where the listed entity is not a party.

Regulation 23(1) of LODR regulations specifies that transaction with a related party shall be considered material if the transaction(s) to be entered into individually or taken together with previous transactions during a financial year exceeds 10% of the annual consolidated turnover of the listed entity as per audited statement.

Approval of shareholders for material RPTs

As per existing provisions in the LODR

In terms of regulation 23(4) of LODR Regulations, all material RPTs shall require approval of the shareholders through resolution and no related party shall vote to approve such resolutions whether the entity is a related party to the particular transaction or not.

As per recommendation of the Working Group

a) All material RPTs and subsequent material modifications, shall require prior approval of the shareholders through resolution and no related party shall vote to approve such resolutions whether the entity is a related party to the particular transaction or not.

b) Prior approval of the shareholders of a listed entity shall not be required for a RPT to which the listed subsidiary is a party but the listed entity is not a party.

Exemption from the applicability of provisions related to RPTs

As per existing provisions in the LODR

In terms of regulation 23(5) of LODR, provisions of regulation 23 (2), (3) and (4) of LODR (dealing with prior approval of audit committee, omnibus approval and shareholder approval, respectively) are not applicable in the following cases:

(a) transactions entered into between two government companies;

(b) transactions entered into between a holding company and its wholly owned subsidiary whose accounts are consolidated with such holding company and placed before the shareholders at the general meeting for approval.

As per recommendation of the Working Group

The Working Group recommended to exempt transactions entered into between two wholly-owned subsidiaries of the listed holding company, whose accounts are consolidated with such holding company and placed before the shareholders at the general meeting for approval from the provisions of regulation 23 (2), (3) and (4) of LODR in addition to the existing exemptions.

Diagram of RPTs as per Existing Provision:-

Diagram of RPTs as per Recommendation of Working Group

Related Party Transaction as per Companies Act:

Section 188 of the Companies Act describes provisions of Related Party transaction. It talks about Related Party Transactions that are applicable to both Private and Public Limited Company.

Generally, any person or any entity which is related to the reporting entity is said to be a related party. Further, a related party can be the situation when a person or a close member of that person’s family is associated with an entity.

Except with the consent of the Board of Directors given by a resolution at a meeting of the Board no company shall enter into any contract or arrangement with a related party with respect to—

(a) sale, purchase or supply of any goods or materials;

(b) selling or otherwise disposing of, or buying, property of any kind;

(c) leasing of property of any kind;

(d) availing or rendering of any services;

(e) appointment of any agent for purchase or sale of goods, materials, services or property;

(f) such related party’s appointment to any office or place of profit in the company, its subsidiary company or associate company; and

(g) underwriting the subscription of any securities or derivatives thereof, of the company:

Provided that no contract or arrangement, in the case of a company having a paid-up share capital of not less than such amount, or transactions exceeding such sums, as may be prescribed, shall be entered into except with the prior approval of the company by a resolution

Provided further that no member of the company shall vote on such resolution, to approve any contract or arrangement which may be entered into by the company, if such member is a related party

Provided also that nothing in this sub-section shall apply to any transactions entered into by the company in its ordinary course of business other than transactions which are not on an arm‘s length basis

Provided also that the requirement of passing the resolution under first proviso shall not be applicable for transactions entered into between a holding company and its wholly owned subsidiary whose accounts are consolidated with such holding company and placed before the shareholders at the general meeting for approval.

Related Party Transaction as per Income Tax Act:

Section 40A(2) of Income Tax Act,1961 deals with payments to relatives and associated persons.

Where any assessee , being an individual who carries on business or profession, makes any payment for any expenditure to any relative of such individual , then the transaction is a related party transaction under section 40A(2)(b)(i) of Income Tax Act ,1961.

Example: Mr. X is a Chartered Accountant who derives his income from the profession. For the financial year 2020-21 , he has made payment for office rent to his wife Mrs. Y. As per section 2(41), the spouse of an Individual is a relative , hence the rent transaction is a ‘related party transaction’ for the purpose of Income tax.

As per section 40A(2)(b)(ii) of Income tax act , any transaction between a company and its director or any relative of any of its directors is a ‘related party transaction’ for the purpose of income tax act.

Example: Mr. X is a director of ABC Ltd. Which is engaged in the business of manufacturing plastic bags . For the financial year 2020-2021 , ABC Ltd.

has made payment for office electricity charge to Mrs.Y wife of Mr.X.

As per section 2(41) , the spouse of an Individual is a relative , hence the electricity charge transaction between ABC Ltd and Mrs Y, wife of director Mr. X is a ‘related party transaction’ for ABC Ltd. under the income tax act.

Similarly any transaction between a firm and its partner or any relative of any of its partners is a ‘related party transaction’ for the purpose of income tax under section 40A(2)(b)(ii).

Example: Mr. X is a partner of ABC Ltd. which is engaged in the business of garments . For the financial year 2020-2021 , ABC Ltd. has made payment for publicity expenses to Mr Z, son of Mr. X.

As per section 2(41), the spouse of an individual is a relative, hence the publicity transaction between ABC Ltd. and Mr.Z, son of Mr. X is a ‘related party transaction’ for ABC Ltd. Under the income tax.

As per section 40A(2)(b)(iii) income tax act, where an assessee makes any payment for any expenditure to any individual who has a substantial interest in the business or profession of the assessee or any relative of such individual, then the transaction is a related party transaction.

Example : ABC Ltd. has made payment for marketing expenses to Mr.X who holds 25% of shares of ABC Ltd. . This is a ‘related party transaction’ for ABC Ltd. under the income tax. The position will also remain the same if such expense is paid to the wife or son of Mr. X.

If Mr. X holds 10% shareholding in the company instead of 25% then it would be treated as irrelevant. For determining the threshold limit of substantial holding, standalone holding needs to be considered and shall not be clubbed under any circumstances.

As per section 40A(2)(b)(iv) of income tax act where any assessee makes any payment for any expenditure to any company which has a substantial interest in the business or profession of the assessee and any director of such a company or any relative of such director , then the transaction is a related party transaction.

Example: ABC Ltd has made payment for publicity expense to XYZ private limited which holds 25% of shares of ABC Ltd. Mr. X is a director of XYZ private limited. This is a ‘related party transaction’ for ABC Ltd under the income tax. The position will also remain the same if the expense is paid to Mr. X or his relative.

In this case it must be remembered that payment transaction from the holding company to subsidiary company is not covered under section 40A(2)(b)(iv) since the holding company holds substantial interest in the subsidiary company and not the subsidiary company holds any interest in the holding company. If the subsidiary company makes any payment to its holding company then the transaction will be treated as related party transaction for the subsidiary company.

Example: A Ltd holds 35% shares in B Ltd and 25% shares in C Pvt ltd . Hence ,any transaction between C Pvt ltd and B Ltd shall be a related party transaction under section 40A(2)(b)(iv) for C Pvt ltd.

As per section 40A(2)(b)(v) where any assessee makes any payment for any expenditure to any company whose any of the director of the company has a substantial interest in the business or profession of the assessee the any transaction with such a company in which he is a director or any other director of the company is a related party transaction.

Similar provision is provided for a firm, associate and HUF.

Example: Mr. X is a director of XYZ Ltd. holds 25% equity shares of Y Ltd. He is also a partner of ABC Ltd. having a 30% profit sharing ratio.

Y Ltd. paid rent to XYZ ltd. and purchased goods from ABC Ltd. during FY 2020-2021. The rent transaction between Y Ltd and ABC Ltd is a related party transaction since the payee’s director holds substantial interest in Y Ltd. The position would remain same had the rent was paid to Mr. X or his relative instead of XYZ Ltd.

Similarly the purchase transaction between Y Ltd and ABC Ltd is also a related party transaction for the above mentioned reason.

As per section 40A(2)(b)(iv)

a) where any individual assessee makes any payment for any expenditure to any person having business or profession and the individual or any relative of such individual has a substantial interest in the business or profession of that person , then any payment for expenditure between the individual and the person shall be regarded as a related party transaction for the purpose of income tax.

b) Where the assessee is a company and makes any payment for any expenditure to any person having business or profession and the company or any director of the assessee company or relative of such director HSS a substantial interest in the business or profession of that person , then any payment for expenditure between the company and the person shall be regarded as a related party transaction for the purpose of income tax.

Similar provision is provided for a firm or an AOP /HUF and the partners and members and relatives of such partner or member. The related party transactions are determined from the point of assessee. The relationship may be due to being a relative of the specified individuals or because of substantial interest.

It is further to be noted that simply making payments to related parties does not amount to disallowance. The disallowance of any such expenditure is restricted to the excessive or unreasonable portion of the expenditure as compared to the market value of the goods , services or facilities. So the excessive or unreasonable expenditure considered by the assessing officer shall not be allowed as deduction.

Example : If X purchases goods from Y for Rs. 30,000 and debits the said amount in the profit and loss account . But the fair market value of such goods is only Rs. 20,000 . This means X should have charged only Rs. 20,000 in the Profit and loss account.

Therefore according to section 40A(2) of income tax act , excess amount of Rs. 10,000 is to be added back to be profit while computing business income of X.

Related Party Transaction Approval Matrix:

Where members(shareholders) approval required:

Related Party Transaction as per Goods and Service Tax (GST):

Supplies between the related persons with consideration in arm’s length shall constitute as ‘Supply’ like any other transaction. Whereas, the supply made between related persons for inadequate or no consideration is covered under Schedule I of the GST Act.

Schedule I – Section 7 of CGST Act

Transactions between related persons and other activities of GST Schedule I will be treated as supply even if made without any consideration under Schedule I of the GST Act.

For instance, TATA Steel and TATA Motors are both considered separate legal entities under TATA Sons, even though the former supplies inputs to the latter. Such business entities which may have separate legal existence while sharing a common control, fall under the definition of ‘related person” under GST law.

Activities to be treated as Supply even if made without consideration

1) Permanent transfer or disposal of business assets where input tax credit has been availed on such assets.

2) Supply of goods or services or both between related persons or between distinct persons as specified in section 25, when made in the course or furtherance of business:

Provided that gifts not exceeding fifty thousand rupees in value in a financial year by an employer to an employee shall not be treated as supply of goods or services or both.

3) Supply of goods—

(a) by a principal to his agent where the agent undertakes to supply such goods on behalf of the principal; or

(b) by an agent to his principal where the agent undertakes to receive such goods on behalf of the principal.

4) Import of services by a taxable person from a related person or from any of his other establishments outside India, in the course or furtherance of business.

Related Party Transactions as per Customs:

Rule 3 of the export value declaration stipulates that the Transaction Value for export goods shall be accepted even where buyer and seller are related, provided that the relationship did not influence the price of the goods.

As per rule 5 of export value declaration the proper officer of customs shall , wherever possible, use a sale of similar goods at the same commercial level and in substantially the same quantities as the goods being valued.

Rule 3(3)(a) provides that where the buyer and the seller are related, the circumstances surrounding the sale shall be examined and the transaction value shall be accepted as the value of imported goods provided that the relationship did not influence the price.

Rule 3(3)(b) provides an opportunity for the importer to demonstrate that the transaction value closely approximates to a “test” value previously accepted by the proper officer of customs and is therefore acceptable under the provisions of rule 3.

The investigation is done by “special valuation branch(SVB) who investigated transactions involving special relationship between buyer-seller or those involving other special circumstances surrounding the sale of imported goods.

Related Party Transactions as per Accounting Standards:

Accounting Standard 18

As per AS-18, Related Party Transaction includes:

- Salary to Director

- Advance against share capital given

- Lease Rent on equipment received

- Securities Deposit Receipt-Refunded

- Unsecured Loan (taken/given/returned)

- Loan & Advances

- Share application money invested

- Share Application money received

- Shares Issued.

Indian Accounting Standard 24

A related party transaction is a transfer of resources, services or obligations between a reporting entity and a related party, regardless of whether a price is charged. If an entity has had related party transactions during the periods covered by the financial statements, IAS 24 requires it to disclose the nature of the related party relationship as well as information about those transactions and outstanding balances, including commitments, necessary for users to understand the potential effect of the relationship on the financial statements.

IAS 24 requires an entity to disclose key management personnel compensation in total and by category as defined in the Standard.

FAQ on Related Party and Related Party Transaction:

1) Is a related party a third party?- Third parties include unrelated business entities such as unrelated vendors, customers, banks etc. Related parties include group companies such as holding company, subsidiary company, key management personnel and shareholders that have substantial interest in the business entity.

2) Is associate company a related party?- An associate includes subsidiaries of the joint venture. Therefore an associate’s subsidiary and the investor that has significant influence over the associates are related to each other.

3) Is promoter a related party?- Yes. The definition of the related party under the listing regulation explicitly includes a promoter or member of a promoter group of a listed entity.

4) Is liaison office a related party?- A liaison office is not a separate legal entity . It is considered as an extension of its principal office. All the expenses of the liaison office are met by the head office . As per master circular of RBI a liaison office (LO) can undertake only liaison activities i.e. It can act as a channel of communication between Head office abroad and parties in India. It is not allowed to undertake any business activity in India and cannot earn any income.

5) Why are Related Parties Important?: Related parties control authorising and approving significant transactions and arrangements with related parties and authorising significant transactions outside the entity’s normal course of business.

6) How would I know arm’s length price followed or not:- Where more than one price is determined by the most appropriate method , the arm’s length shall be taken to be the arithmetic mean of such prices or at the option of the assessee , a price which may vary from the arithmetic mean by an amount not exceeding 5% of such arithmetic mean.

7) What is recurrent related party transaction?- Recurrent Related Party Transaction refers to a related party transaction which is recurrent, of a revenue or trading nature, which is necessary for day to day operations of the company or it’s subsidiaries.

8) What is Material Related Party Transactions?

A transaction with a related party shall be considered material if the transaction(s) to be entered into individually or taken together with previous transactions during a financial year, exceeds 10% of the annual consolidated turnover.

9) A Corporate group has several foreign subsidiaries . Will provisions in relation to related parties apply to foreign companies as well?

Company incorporated under the relevant legislation of a foreign country is not a “company” under companies act,2013. However transaction by Indian company with a foreign company, which is a subsidiary , associate, joint venture etc. would be covered.

10) In case of Companies Act, is the board required to approve all related party transaction?

The Companies Act, 2013 prescribes that a company needs approval of the audit committee on all related party transactions.

11) What assessment is required of existing RPTs , if any?

All Companies are required to comply with requirements in relation with RPTs. Any default will be regarded as non-compliance and may attract penal provisions under the Companies Act, 2013.

12) Which types of transactions will be regarded as ordinary course of business?

The ordinary course of business is not defined under the Companies Act, 2013. It seems that the ordinary course of business will cover the usual transactions, customs and practices of a business. The institute of Chartered Accountants of India has included following few examples of transactions that are considered outside the entity’s normal or ordinary course of business-

a) Complex equity transaction e.g. corporate restructuring or acquisitions,

b) Transactions with offshore entities,

c) Sales transactions with unusually high discounts/ returns

d) Transactions under contracts

13) Whether the provisions pertaining to “related parties” are applicable based on a financial year?

The provisions pertaining to “related party” and “related party transactions” are applicable for all contracts with related parties entered on or after 01st April,2014, irrespective of accounting year followed by the Company.

14) Whether the contracts or arrangements of transaction with related parties entered on or before 01st April,2014 are also governed the provisions of the Companies Act,2013?

No, the contracts or arrangements of transactions with related parties entered on or before 01st April,2014 shall continue to be governed by the provisions of the erstwhile act and any other applicable provisions.

15) Whether any modification in the contracts or arrangements of transactions with related parties entered on or before 01st April,2014 are also governed by the provisions of Companies Act, 2013?

Modification made to such contracts/arrangements on or after 01st April, 2014 shall be governed by the provisions of Companies Act, 2013.

16) Whether the provisions relating to special resolutions u/s 188 are also applicable to transactions with wholly owned subsidiaries?

No, wholly owned subsidiary companies are exempted from the requirements of passing a special resolutions, provided requirement of the special resolutions have been c0mplies by the holding company.

17) Can there be a situation in which contracts or arrangements require special resolution with related party only when under amended listing agreement and not under the Companies Act, 2013?

Yes, contracts or arrangements with related parties in the ordinary course of business and at arm’s length prices are exempted from the approval from the shareholders and board, except the prescribed approvals under section 177 of Companies Act,2013. Whereas clause 49 of SEBI requires material related party transactions to be approved by way of a special resolution in the member’s meeting, in spite of such transaction being in the ordinary course of business and carried out at an arm’s length price.

18) How to interpret the term “Ordinary course of its business (OCB) as used in the context of related party transactions under companies Act,2013?

Which are directly or indirectly connected to or necessary to conduct its business. For example : Company ABC which is primarily engaged in the business of manufacturing and selling auto parts and advancing loans to a related party which is in the business of providing information technology services , could be viewed as a transaction not in OCB . Whereas if the company ABC entered into a contract with a related party to avail travel services for its employees such services being necessary for ABC, ordinary activities could be regarded as OCB.

19) Are shareholders related parties IAS 24?

Major shareholder and his wife are related parties, because they are a person or a close family member of that person (wife) who control the entity A. Entity B is a related party of an entity A, because it is controlled by close family member of a major shareholder of A (not because it is the sole customer).

20) Regulation 2(1)(b) of LR defines an ‘associate company’ to mean any entity which is an associate under the Companies Act, 2013 or under the applicable accounting standards. Whether both conditions have to be met or either of the two?

The definition of associate company should be viewed under the Companies Act, 2013 as well as Accounting Standards. If the condition is met under either of the two, then such entity should be classified as an associate company.

21) Regulation 2(1) (zb) of LR defines the term ‘Related party’ to mean related party under the Companies Act, 2013 or under the applicable Accounting Standards. Whether both conditions have to be met or either of the two?

The definition of related party should be viewed under the Companies Act, 2013 as well as Accounting Standards. If the condition is met under either of the two, then such party should be classified as a related party. Further, any person or entity belonging to the promoter or promoter group of the listed entity and holding 20% or more of shareholding in the listed entity shall be deemed to be a related party.

22) Regulation 23 (4) provides that all material related party transactions shall require approval of the shareholders through resolution and no related party shall vote to approve such resolutions whether the entity is a related party to the particular transaction or not. In this regard, whether only those related parties who are related to the concerned transaction/ contract should not vote to approve or whether related parties should altogether not vote to approve such transaction?

The requirement under Regulation 23(4), is applicable for listed entities subject to the provisions of Regulation 15. Hence, for applicable entities, the regulations clearly provide that all material related party transactions shall require approval of the shareholders through resolution and no related party shall vote to approve such resolutions whether the entity is a related party for the particular transaction or not.

230 Regulation 24(1) prescribes having at least one independent director on the board of directors of the listed entity as a director on the board of directors of ‘unlisted material subsidiary, incorporated in India or not’. Sub-regulations (2), (3) and (4) to the same regulation refer to ‘unlisted subsidiary’. Whether such sub-regulations (2), (3) and (4) are applicable to all unlisted subsidiaries or only material unlisted subsidiaries incorporated in India?

Listed entities may be guided by the provisions of Regulation 24. Wherever ‘unlisted material subsidiary’ and ‘unlisted subsidiary’ have been distinctly mentioned in a particular subregulation, such sub-regulation shall be applicable to material unlisted subsidiaries or all unlisted subsidiaries as the case may be.

24) Regulation 24 (4) requires that the management of the unlisted subsidiary shall periodically bring to the notice of the board of directors of the listed entity, a statement of all significant transactions and arrangements entered into by the unlisted subsidiary. Whether the requirement is applicable only to the material unlisted subsidiary?

The requirement is applicable to all unlisted subsidiaries.

25) Does every related party import needs to be referred to SVB Are there any exemptions?

Are there any exemptions? As per the prescribed procedures, following cases are not required be taken up for inquiries by SVBs: Import of samples and prototypes from related sellers; Imports from related sellers where duty chargeable is unconditionally fully exempted or nil.

26) What is the basis of valuation of goods for the purpose of computing customs duties?

Custom Duties are calculated on the ‘assessable value’ of the goods as per Section 14 of the Customs Act, which is the ‘transaction value’ agreed between the supplier and the importer subject to certain inclusions (such as freight, insurance etc) in the transaction value if not already included and subject to the condition that the buyer and seller are not related. In case the buyer and seller of the goods are related, the value is to be determined as per Customs Valuation (Determination of value of Imported Goods) Rules, 2007 (‘CVR’) framed in this regard.

27) Which department of customs authorities investigates related party transactions . What is a Customs SVB?

The SVB is a special unit within the Indian Customs department which specializes in investigating the valuation of the transactions between ‘related persons’, as defined under Rule 2 (2) of CVR. Specific customs officials are posted to this department of customs who carry out the investigation and evaluate whether the intercompany prices of goods are influenced due to the relationship between the parties, with the intention to reduce the Customs Duty liability or not.

28) Does every related party import needs to be referred to SVB? Areb thre any exemption?

As per the prescribed procedures, following cases are not required be taken up for inquiries by SVBs:

- Import of samples and prototypes from related sellers;

- Imports from related sellers where duty chargeable is unconditionally fully exempted or nil.

- Any transaction where the value of imported goods is less than INR 100 Thousand but cumulatively these transactions do not exceed INR 2.5 Million in any financial year.

Author Bio

Is ultimate holding company is covered under related party and company needs to take approval of Board and shareholders for the transaction of purchase or sales of goods and services with ultimate holding company under section 188 of the companies act, 2013?

Related parties include group companies such as holding company, subsidiary company, key management personnel and shareholders that have substantial interest in the business entity.