Ind AS 1 Presentation of Financial Statements

Scope of the standard

- Applicable in preparing and presenting general purpose financial statements in accordance with Ind ASs. [Except Ind As 34]

- Other Ind ASs set out the recognition, measurement and disclosure requirements for specific transactions and other events.

- It applies equally to all entities, including those that present Consolidated financial statements.

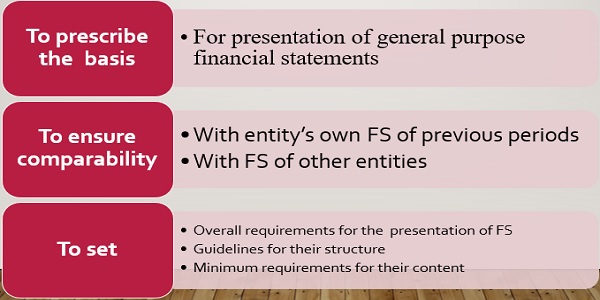

Objective of Ind AS 1

Purpose of Financial Statements

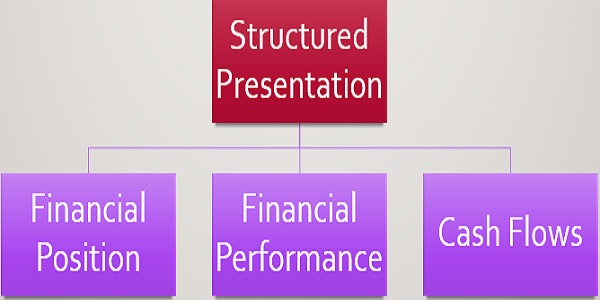

Components/ Complete set of financial statements

General features/ Overall Considerations

Overall considerations

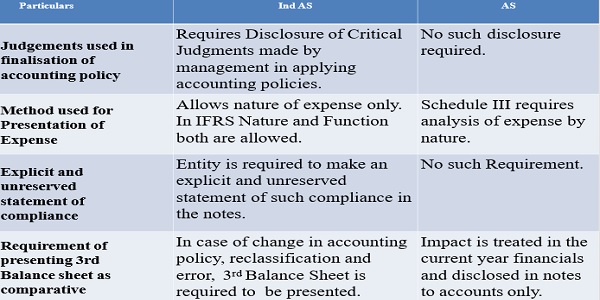

> Presentation of True & Fair View and Compliance with Ind AS

- True & Fair view assumed through application of Ind AS

- Explicit & Unreserved Statement of Compliance of All Ind AS needs to be disclosed

> Departure from Compliance of Ind AS

- In extremely rare circumstances, where compliance with a Standard would be misleading so it would conflict with objective set out in the framework

- Departure is permissible, if regulatory framework requires or does not prohibit

- Specified disclosure required

Going concern

When preparing financial statements, management shall make an assessment of an entity’s ability to continue as a going concern:

- An entity shall prepare financial statements on a going concern basis unless there

- is intention to liquidate or to cease trading or

- no other alternative except to do so

- Disclose in case of Material uncertainty

- If FS are not prepared on Going Concern basis – Disclose fact, basis and reason for that

Overall considerations

Accrual basis

- Transactions and events are recognised when they occur, and

- In the periods to which they relate

Consistency

Presentation & classification be retained

- Unless change in nature of operations necessitates another presentation

- A standard or an interpretation requires a change

Materiality & Aggregation

- Material – present separately

- Immaterial – aggregate with other items

Offsetting

- Assets, Liabilities, Income and expenses shall not be offset unless required or permitted

- (Measuring assets net of valuation allowances- for e.g. obsolescence allowances on inventories and doubtful debts allowances on receivables is not offsetting)

Comparative information

- Includes narrative & descriptive information

- If an entity changes the presentation or classification of items in its FS, it shall reclassify comparative amounts unless reclassification is impracticable.

- When an entity reclassifies comparative amounts, it shall disclose: (Para 41)

- the nature of the reclassification;

- the amount of each item or class of items that is reclassified; and

- the reason for the reclassification.

- When it is impracticable to reclassify comparative amounts, an entity shall disclose: (Para 42)

- the reason for not reclassifying the amounts, and

- the nature of the adjustments that would have been made

- if the amounts had been reclassified

Structure and content – General

- Identification of financial statements

- Clearly distinguished from other information

- Reporting period- At least annually, To explain if longer or shorter period

- Information required

- Name and change, if any

- Individual or group financials

- Period covered

- Currency

- Level of rounding

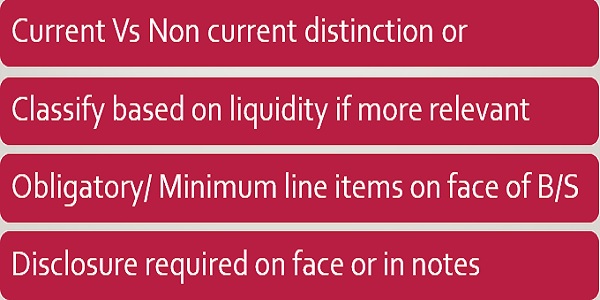

Structure and Content – Balance Sheet

- Relevant sub-classifications of items above

- Information on share capital and reserves

Structure and Content – Balance Sheet

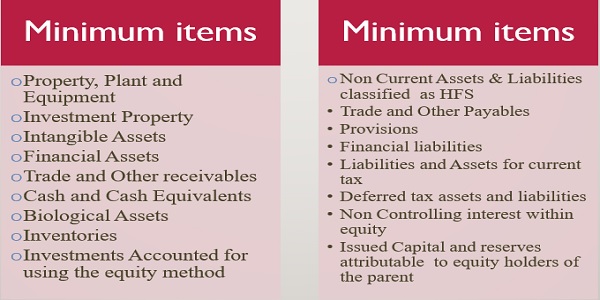

Current Assets

Current Liabilities

- Settled in the normal course of operating cycle or due to be settled within 12 month of the balance sheet date

- Held primarily for the purpose of being traded

- No unconditional right to defer settlement for at least 12 months

- All other Liabilities are non-Current

Carve outs in respect of long term loans

- Where there is a breach of a material provision of a long-term loan arrangement on or before the end of the reporting period with the effect that the liability becomes payable on demand on the reporting date, the entity does not classify the liability as current, if the lender agreed, after the reporting period and before the approval of the financial statements for issue, not to demand payment as a consequence of the breach.

- However, an entity classifies the liability as non-current if the lender agreed by the end of the reporting period to provide a period of grace ending at least twelve months after the reporting period, within which the entity can rectify the breach and during which the lender cannot demand immediate repayment.

Structure and content – Statement of Profit and Loss

- Concepts of profit and loss and other comprehensive income:

- Profit or loss is defined as “the total of income less expenses, excluding the components of other comprehensive income”.

- Other comprehensive income is defined as comprising “items of income and expense (including reclassification adjustments) that are not recognised in profit or loss as required or permitted by other Ind ASs”.

- Total comprehensive income is defined as “the change in equity during a period resulting from transactions and other events, other than those changes resulting from transactions with owners in their capacity as owners”.

Statement of Profit and Loss

- Includes Profit or loss and Other Comprehensive Income

- obligatory line items on face of statement of Profit & loss

- To show as allocation

- Profit or loss attributable to NCI

- Profit or loss attributable to equity holders of the parent

- expenses analysed on basis of Nature only like Salaries, depreciation, etc (allowed in both IFRS and Ind AS)

- Classification based on function like Selling and distribution, Administration etc (allowed in IFRS but not allowed in Ind AS)

Minimum line Items on the face of the Profit & Loss :

- Revenue

- Finance Costs

- Impairment losses

- Share of profit or loss of associate and JV by equity method

- Tax expense

- Sum of profit or loss on discontinued operations plus gain

- or loss on the disposal of discontinued operations assets

- gains and losses arising from the derecognition of financial

- assets measured at amortised cost.

- No extraordinary items

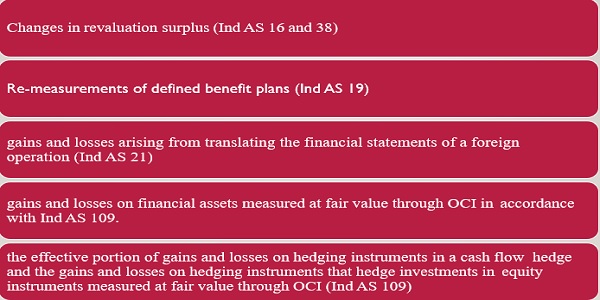

Structure and content – OCI

Statement of changes in equity

- Separate component of financial statements

- On the face for each component of equity a reconciliation between carrying amount at beginning and at end of period

- Profit or loss for the period

- other comprehensive income

- Effect of retrospective application or restatement

- Also in statement or in the notes

- Capital transactions with owners

- Movements in accumulated profit

- Movements in capital and reserves

Structure and content

- Role of statement of changes in equity

- Broader performance indicator

- ‘Total recognised gains and losses’ or

- ‘Comprehensive income’

- Cash flow statement in accordance with Ind AS 7

Structure and content – Notes to the Financial Statements

- The notes shall:

- Present information about the basis of preparation of the financial statements and the specific accounting policies;

- Disclose the information required by Ind ASs that is not presented elsewhere in the financial statements; and

- provide information that is not presented elsewhere in the financial statements, but is relevant to an understanding of any of them.

- Notes shall be presented in a systematic manner and cross-reference in the following order:

- Statement of compliance with Ind AS

- Summary of significant accounting policies applied

- Supporting information for items presented in FS, in the order in which each statement and each line item is presented; and

- Other disclosures, including: contingent liabilities and unrecognised contractual commitments, and other non-financial disclosures

Structure and content – Other Disclosures

- Critical Management Judgments

- Examples

- Substance over form issues

- Sale of goods/ financing arrangements

- Existence of control over SPEs

- Critical Estimates

- Examples

- Recoverability of internally generated intangible assets

- Impairment of goodwill

- Useful lives of property, plant and equipment etc.

- Capital Management policies

Key Differences

–