Securities and Exchange Board of India

1. BACKGROUND

1.1. There is increasing debate about the need to enable issuance and listing of shares with differential voting rights, commonly known as DVRs in India; and dual class shares or DCS in the international context. Such shares have rights disproportionate to their economic ownership. In promoter / founder led companies where promoters! founders are instrumental in the success of the company, such structures enable them to retain decision-making powers and rights vis-à-vis other shareholders either through retaining shares with superior voting rights or issuance of shares with lower or fractional voting rights to public investors.

1.2. The matter was deliberated in the Primary Market Advisory Committee of SEBI and a group (DVR Group) was constituted amongst the Committee members to do an in-depth study of the proposal of introduction of dual-class shares in Indian Scenario.

1.3. The DVR Group has submitted its report [DVR Group report] to SEBI. The Report proposes to structure the regulation of DVR issuance under two broad heads. The broad heads will cover issuance by companies whose equity shares are already listed on stock exchanges; and companies with equity shares not hitherto listed but proposed to be offered to the public.

2. PUBLIC COMMENTS

Considering the implications of the said matter on the market participants including issuers and investors, public comments are invited on the proposals contained in the DVR Group Report. Specific comments!suggestions as per the format given below would be highly appreciated:

| Name of entity / person / intermediary/ Organization: | |||

| Sr. No. | Pertains to specific recommendation in DVR Group Report | Suggestion(s) | Rationale |

The comments may please be e-mailed on or before April 20, 2019, to Mr. Abhishek Rozatkar, Assistant General Manager at abhishekr@sebi.gov.in or sent by post, to:

Smt. Yogita Jadhav

Deputy General Manager

Corporation Finance Department Securities and Exchange Board of India

SEBI Bhavan Plot No. C4-A, “G” Block Bandra Kurla Complex

Bandra (East), Mumbai – 400 051 Ph: +91-22–2 6449583

Issued on: March 20, 2019

PMAC DVR GROUP REPORT

February 2019

Issuance of Equity Shares with Differential Voting Rights

Table of Contents

| 1 | Introduction | 2 |

| 2 | Need for DVR in India | 2 |

| 3. | Advantages and disadvantages for consideration in the context of DVRs | 3 |

| – Issuer | ||

| – Investor | ||

| 4. | Regulatory considerations in India | 4 |

| – The Companies Act | ||

| – SEBI Regulations | ||

| – Securities Contracts (Regulation) Rules, 1957 | ||

| – SEBI (LODR) Regulations, 2015 | ||

| 5. | Comparison across various jurisdictions | 6 |

| – USA | ||

| – Canada | ||

| – Hong Kong | ||

| – Singapore | ||

| – Regulators’ views on DCS structures | ||

| 6. | Market considerations and Companies with listed DVRs in India | 10 |

| – Share price performance of DVRs | ||

| – History and analysis of DVRs by Indian companies | ||

| 7. | Recommendations of the PMAC DVR Group | 13 |

| Annexures | 25 |

1. Introduction

The common rule of one share – one vote is considered convenient for corporate governance, both from the point of view of the shareholders and the promoters of a company. However, there is increasing debate about the need to enable issuance and listing of shares with differential voting rights, commonly known as DVRs in India; and dual class shares or DCS in the international context. Such shares have rights disproportionate to their economic ownership. In promoter! founder led companies where promoters! founders are instrumental in the success of the company, such structures enable them to retain decision-making powers and rights vis-à-vis other shareholders either through retaining shares with superior voting rights or issuance of shares with lower or fractional voting rights to public investors.

Such structures help in fund raising without dilution of control and serve as defense mechanism against any hostile bid for change in control. While the promoters! founders can maintain control as they would hold shares with the superior voting rights, the shareholders participating in the shares with lower or fractional voting rights get the opportunity to participate in the growth of the company, through higher dividends and capital appreciation, besides the gains in case of a sunset clause, even though they have lower voting rights.

In India, the current regulatory regime does not permit DVRs with higher or superior voting rights. However, subject to certain conditions, DVR shares with lower voting rights are permitted. DVR shares with lower voting rights may be of some interest to small shareholders as dividend yield and capital appreciation probably rank higher than voting rights in their investment decisions.

DVR with lower voting rights shares are typically priced lower at issuance and offer higher dividends; in return, the voting rights are limited.

2. Need for DVRs in India

India is experiencing a high growth phase, which requires companies to raise capital to sustain this growth. For companies with high leverage or asset light models may prefer equity over debt capital. Raising equity on a periodic basis leads to dilution of founder! promoter stake, which can be effectively addressed through use of DVRs as a mode of capital raising.

This is especially relevant for new technology firms which have asset light models, with little or no need for debt financing. These firms, however, continuously require grow only through equity, which dilutes promoter’s! founder’s stake, thereby diluting control. It is pertinent to note that in such cases, retaining founder’s interest & control in the business is of great value to all shareholders͘

This can be achieved by:

a) Issue of shares with superior voting rights to founders and!or

b) Issue of shares with lower or fractional voting rights to raise funds from private! public investors

One way to let Indian entrepreneurs have some autonomous space for managing and growing their business without the suppliers of their capital over-supervising them and offering advice they cannot refuse is to allow them to issue shares with differential voting rights to the founders! promoters. Will foreign funds want to invest in such companies where founders hold higher voting rights? If the business model and execution capability on offer are compelling, they would, attracted by the financial return promised by the venture. Research shows that firms with an exciting story to tell issue dual-class shares. Market will be willing to give up control to an insider who has proven to be successful.

3. Advantages and disadvantages for consideration in the context of DVRs 1

The success of dual-class structures in many companies has led both Nasdaq and the NYSE to continue to permit dual-class listings. For example, Nasdaq recently released a report that included an endorsement of dual-class stock, including laying out the arguments why companies with dual-class stock should continue to be listed. Among the reasons cited by Nasdaq was the recognition that encouraging entrepreneurship and innovation in the U.S. economy is best done by “establishing multiple paths entrepreneurs can take to public markets”. “Because of this, each “publicly traded company should have flexibility to determine a class structure that is most appropriate and beneficial for them, so long as this structure is transparent and disclosed up front so that investors have complete visibility into the company. Dual-class structures allow investors to invest side-by-side with innovators and high-growth companies, enjoying the financial benefits of these companies’ success.”

While there is ongoing debate in the SEC about the continuation of DCS2, NYSE continues to actively seek to list companies with multi-class stock, including Alibaba, which chose to list on the NYSE after the Hong Kong stock exchange raised significant questions about its capital structure.

Presented below is an analysis of the advantages and disadvantages of dual class structures for issuers and investors:

a. Advantages to the Issuer:

- A company can raise money and founders of the company can continue to keep control over the company. DVR is a good instrument that would allow founders, especially in case of tech startups, to raise capital without losing control.

- In the case of ordinary equity shares, there is a possibility that a person/institution can acquire majority of the shares and hence take over the control of the company from the management, which is not possible if the founders hold superior voting right shares.

- Founder led companies with effective interest of the founders in such companies is good for growth of the business and thereby for all shareholders.

b. Downsides for the Issuer:

- Usually strategic investor/PE investors want voting rights as they would like to play a role in the management of the company. Many such investors are prohibited by their charters to invest in such shares where they hold voting rights than are inferior to any other shareholder. Hence, it may pose some challenge for issuers to find investors in situations where founders may hold superior voting rights. (A retail investor on the other hand, might be more interested in higher dividends and capital appreciation than in the management of the company and hence may be less averse to such structures.)

- There are always additional questions on corporate governance in companies with dual class

- Lack of investor awareness pursuant to which investors might not be able to understand the DVR structures or risks associated with it to make an informed investment decision.

c. Advantages to Investors:

- In case of pre-existing superior voting rights with the founders, investors would have the comfort of continued involvement of the founders in the company due to control exercised through superior voting rights held by them

- Investors very often invest in a company because of the “trust” they have in the founders and entrepreneurs behind such companies

- If the company issues shares with lower or fractional voting rights, the DVR shareholder gets equal or higher dividend inspite of lower voting rights.

- DVRs with lower or fractional voting rights are usually offered at a discount to the price of the normal equity shares.

- Such shares generally pay more dividend than the normal equity shares.

d. Downsides for Investors:

- When voting interest is separated from economic interests, it may lead to other externalities such as misalignment of interests among shareholders, excessive compensation of management, reduced dividend pay-out, management entrenchment and expropriation

- There is a concern about whether recourse is available to minority shareholders if founders holding superior voting rights are unable to deliver results.

- DVRs with lower or fractional voting rights are often illiquid.

- DVRs with superior voting rights with the founders or large proportion of DVRs with lower or fractional voting rights with public investors make management excessively powerful, leading to issues of corporate governance

- While DCS structures are allowed in countries like the U.S., Canada, Hong Kong and Singapore, they are the exception rather than the norm

4. Regulatory Considerations in India

The regulatory framework in India protects the rights of the dual class shareholders, as well as the minority shares. For example, in the United States, Berkshire Hathaway Inc. Class A equity shareholders can convert their shares into class B equity shares, having fewer voting rights. However, under the Indian Law, a company cannot convert its existing equity share capital with voting rights into equity share capital carrying differential voting rights and vice versa.

a. The Companies Act, 2013

The Companies Act, 2013, Section 47 provides for every shareholder of a company to have a right to vote on every resolution presented before the company.

However, as per Section 43(a)(ii) of the Companies Act, 2013, a company incorporated under the laws of India and limited by shares is permitted to have equity shares with differential voting rights as part of its share capital. The differential rights appended to such equity shares may be with respect to dividend, voting (higher or lower) or otherwise. Such equity shares may be issued by a company as per Rule 4 of the Companies (Share Capital & Debentures) Rules, 2014 prescribed under the Companies Act, 2013.

It is pertinent to note that the Rules have clarified that existing equity shares with differential rights will continue to have the rights that have been provided at the time of their issuance and have accordingly been grandfathered. Shares with differential voting rights would be valid provided a company has the powers to issue and structure such class of shares under the Articles of Association of the company.

Two limiting factors in the Companies Act, 2013 are:

1. “The company must have a consistent track record of distributable profits for the last 3 years”. However, the 3-year criterion is silent on IPOs. Further, the same also needs to be looked into with SEBI regulations viz. 6(1), 6(2) of the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (“SEBI ICDR Regulations”). While it appears that the criteria may not be beneficial for startups, a view needs to be taken whether the intention was to open up for all companies including non-profit making or have a filter as in have it initially for mature

2. “The shares with differential rights shall not exceed 26% of the total post-issue capital, including equity shares with differential rights issued at any point of time”.

b. SEBI Regulations

With the apprehension of possible misuse of “superior voting rights” by the issue of shares by the listed companies, SEBI prohibited the issue of such shares in July 21, 2009. The plausible justification for prohibition was the prevention from detriment of the shareholders. However, shares with inferior voting rights are permitted by SEBI. The question of the hour that arises is how different the shares with “superior voting rights” are from shares with “differential voting rights”, as it is the latter term that has attained some measure of popularity under Indian law and practice.

It is significant to comprehend the interpretation of terms “superior and differential voting rights”. It appears that while the expression “differential voting rights” is more generic in nature, “superior voting rights” means any rights that give the shareholder more than one vote per share on a poll, which is the usual norm. This step justifies the prevention of people in control of a company from issuing shares to themselves which provide equal economic benefits with other shareholders (thereby requiring equal outflow of financial resources to obtain those shares), but one which gives greater voting rights and hence, better control. Hence, it is possible for listed companies to issue shares with differential voting rights which provide voting rights below the normal “one-share-one-vote” rule, conferring voting rights greater than that is prescribed.

In the Jagatjit Industries case3, the two brothers, Anand and Jagatjit, moved the CLB against the company’s decision in 2004 on preferential allotment of shares with DVRs, giving Karamjit 64% voting rights on his 32% stake in the company. CLB , in its order, upheld the resolution to allot shares with DVRs to the promoter of the company.

Furthermore, while listed companies will now be allowed to issue differential voting entitlements only with rights inferior to one-vote-per-share, unlisted companies will still be governed by Section 86 of the Companies Act, 1956 (Section 43 of the Companies Act, 2013) and the law laid down in Jagatjit case whereby they have greater flexibility in issuing shares with differential voting rights, both superior and inferior.

Some judgments relating to DVRs are briefly described in Annexure 1.

c. Securities Contracts (Regulation) Rules, 1957 (‘SCRR’):

Rule 19(2)(b) of the SCRR provides for the minimum offer and allotment to public in terms of offer document, which shall be:

a. at least 25% of each class or kind of equity shares/ debenture convertible into equity shares issued by the company, if the post issue market capitalization of company is less than or equal to 1600 crore rupees.

b. at least such percentage of each class or kind of equity shares/ debenture convertible into equity shares issued by the company equivalent to the value of 400 crore rupees, if the post issue market capitalization of the company is more than 1600 crore rupees but less than or equal to 4000 crore rupees

c. at least 10% of each class or kind of equity shares/ debenture convertible into equity shares issued by the company, if the post issue market capitalization of company is above 4000 crore rupees.

Thus, in light of the above rule, it is unclear if, for a company with different class of shares, the IPO needs to be undertaken for all class of shares or the company can proceed with listing of any one class of share thereby keeping the other class of share as unlisted.

d. SEBI (LODR) Regulations, 2015 (“SEBI LODR Regulations”):

Regulation 41(3) of the SEBI LODR Regulations states that the listed entity shall not issue shares in any manner which may confer on any person, superior rights as to voting or dividend vis-à-vis the rights on equity shares that are already listed.

Thus, though the SEBI LODR Regulations also permits an issuer to have DVR shares, such DVR shall not contain any superior voting rights which shall restrict or reduce the voting rights of the existing shareholders.

5. Comparison across Various Jurisdictions

While many countries have permitted the listing of companies with Dual Class Shares, some countries like UK, Australia, Spain, Germany and China do not permit the Issuers with DCS structure for listing. DCS structure was allowed in UK for listing on Standard Listings. However, subsequently the issuers with DCS structure were not allowed listing on standard listings or premium listings. Singapore and Hong Kong have recently permitted DCS structures with detailed checks and balances.

> The key features for issuance & listing of DCS structure in different jurisdictions is as follows:

a. USA:

- Issuers with DCS structures are permitted to list on the NYSE and NASDAQ. Section 313A of NYSE Listing Manual provides for shares with differential voting rights with enhanced disclosure and safeguarding policies.

- However, listing is permitted only issuers with pre-existing DCS structure4. Once listed, issuer with one share one vote structure is not permitted to implement the DCS structure that would reduce or restrict the interest of existing shareholders.

- Sunset Clause: There is no mandatory requirement to have a sunset clause for issuer or companies with DCS structure, however some companies have voluntarily adopted a sunset period of 5 years post which all the shares with multiple (higher) voting rights will be automatically converted into ordinary shares having one vote for one share.

- Some examples in the US5:

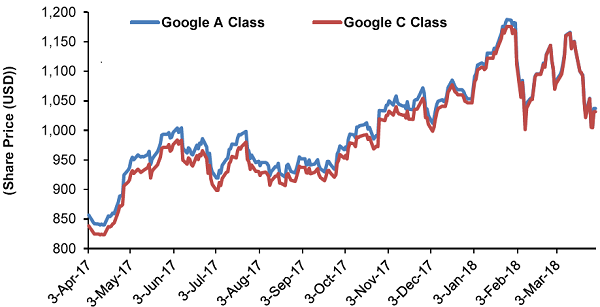

− Google founders retain control of the listed entity Alphabet and have subsequently restructured their capital structure, creating three classes of shares. Class A shares carry one voting right (listed through an IPO and held by public shareholders), Class B shares carry 10 votes each (not listed, held by Larry Page and Sergey Brin and has a sunset clause)6, while Class C shares carry no voting rights (issued to all Class A shareholders and Class B shareholders, listed – issued in 20147). The current market price of Class A (1:1 voting right) and Class C shares (no voting rights) is trading at almost the same price. Further over time, founders have converted part of their holding in Class B shares to Class A shares for liquidity.

− Facebook has issued Class A shares which carry one voting right (listed through the IPO and held by public shareholders), Class B shares which carry 10 votes each (not listed, held by Mark Zuckerberg and affiliates with no sunset clause). Their proposal to issue Class C shares carrying no voting rights in lieu of dividend was withdrawn pursuant to investor resistance8.

− Alibaba – has partisanship structure where 27 partners have the right to appoint majority of the Board. Through this partnership structure, the founders get the majority control on the affairs of the company.

− Snapchat has three classes of shares: Class A, Class B, and Class C. Class A common stock is non-voting. Snapchat became the first company to issue no-vote stock in its IPO. Each share of Class B common stock is entitled to one vote and is convertible into one share of Class A common stock. Each share of Class C common stock is entitled to ten votes and is convertible into one share of Class B common stock. The Class C common stock, which is held by the founders, represents ~90% of the voting power of the outstanding capital stock. There is no sunset clause for founders. There is no sunset clause for founders9.

− Nike has issued Class A shares which has power to elect 75% of the Board of Directors (unlisted and held by Philip Knight, Travis Knight, Mark Parke and Trevor Edward) and Class B shares which has power to elect 25% of the Board of Directors (listed and held by public shareholders).

− Viacom10 has issued Viacom is listed on NASDAQ and trades under the symbols “VIA” for Class A common stock (with 1:1 voting rights) and “VIAB” for Class B common stock (non-voting stock.). While both are listed, Class A common stock is held by Sumner M. Redstone, the controlling stockholder of National Amusements, and Class B is held with public shareholders Viacom Class A common stock can be converted into shares of Class B common stock on a one-for-one basis, but Viacom Class B common stock cannot be converted into Class A common stock. Shareholders have been resisting the >80% control by the CEO through its ~10% shareholding.

- Regulatory updates! investor feedback on this subject is at Annexure 2.

b. Canada:

- DCS structures are permitted under Canadian federal corporate law and also under Toronto Stock Exchange (“TSX”) rules, subject to certain safeguards.

- In case a listed company wants to create a multiple voting class of shares, the company needs to obtain approval from a majority of the votes cast by holders voting at a meeting, other than the promoters, directors, officers, insiders of an issuer or proposed recipient of such shares.

- TSX imposes a ‘coat tail’ provision for companies with a DCS structure.

- Canadian Coalition of Good Governance in its dual class share policy has published some best practices principles for DCS companies such as:

- Holders of MV shares should be entitled to nominate a number of directors equal to the least of (i) two-thirds of the board, (ii) the number obtained when the board size is multiplied by the percentage of total voting rights held by the MV shares, and (iii) if the holders of MV shares are related to the management of a company with a controlling shareholder (i.e. able to elect the board or direct the management), then one-third of the board.

- The share structure should allow a “meaningful equity ownership stake”, which generally requires a voting rights ratio of not more than 4 to 1.

- There should be standard coat tail provisions

- The DCS structure should collapse at an appropriate time as determined by the board and, if practicable, as set out in the articles, where a one-for-one conversion occurs, unless a majority of the holders of OV shares voting separately as a class approve its continuation (for a period no longer than 5 years at each vote). Further, no premiums should be paid to the holders of MV shares for the collapse.

- MV shares sold by a holder should convert automatically to OV shares on a one-for-one basis.

c. Hong Kong:

- Listing by companies that have issued dual class shares or Weighted Voting Rights (WVR) was introduced in April 2018 by incorporation in the mainboard listing rules.

- Some of the eligibility norms for issuers are as follows:

a. Only innovative issuers! biotech companies with certain eligibility criteria permitted to issue WVRs through an IPO.

b. Issuer should have meaningful third party investment from at least one sophisticated investor before the IPO. Such investor(s) should retain an aggregate 50% of their investment for at least 6 months post the IPO. This is exempt for a company spun off from a parent company

c. Market Capitalization: (i) HK$ 40 bn or (ii) HK$ 10 bn & HK$ 1 bn revenue in latest audited FY.

d. The beneficiaries of the WVR should be an individual with active executive role in the business and has contributed materially to the growth of the business. Each of the beneficiaries should be a director on the board at IPO.

e. The beneficiaries of the WVR should hold at least 10% of economic interest in total issued share capital.

- If the beneficiaries of WVR shares die, cease to be director or transfer their shares to another person, the rights attached to such WVR shall lapse.

- The maximum voting rights per share an issuer can allow cannot exceed 10 times the voting rights on ordinary shares.

- Companies with WVR structure need to adopt enhanced corporate governance measures for investor protection.

- This is applicable for new listing applicants only. Secondary listing for companies with WVR/ DCS structures that are listed on NYSE/ NASDAQ or London premium listing segment11

- There is no time-defined “sunset” clause for the WVR, instead the WVR shall lapse on occurrence of events mentioned above.

d. Singapore:

- In June 2018, Singapore Stock Exchange introduced rules for listing of dual class shares structures on Mainboard. The amendment was followed by two rounds of public consultation.

- The Key features based on framework for permitting the listing of companies with DCS structure on SGX are as follows:

- Only new issuers shall be permitted for listing with DCS structure, subject to various suitability factors including business model, track record, role and contribution of Multiple Votes shareholders, participation by sophisticated investors, among other

- Holder of Multiple Voting shares must to director of the Issuer or member of the

permitted group. The holders of Multiple Voting shares must be disclosed at IPO - Automatic conversion of Multiple Voting shares to Ordinary shares in case the Multiple Voting shares are sold or transferred or the Multiple Voting shares group director ceases to be director (unless new director is appointed)

- The maximum voting rights per share an issuer can allow cannot exceed 10 times than voting rights on ordinary shares (one vote one share are OV).

- The holders of MV shares need to observe a moratorium (lock-in) period of 12 months in both MV shares and OV shares post listing.

- Issuer is prohibited from issuing any shares with multiple voting rights (MV) post listing except in case of Rights issue or other corporate actions like face value split, consolidation etc. Provided that, in case of rights issue, the Issuer needs to ensure that the proportion of MV share to OV shares does not change post rights issue based on additional subscription by holders of MV shares.

- OV shareholders holding 10% of the voting rights should be allowed to convene a general meeting.

- For an issuer with a dual class share structure, disclosure shall prominently include: (a) a statement on the cover page that the issuer is a company with a dual class share structure; and (b) information on the voting rights of each class of shares.

- The majority of each of the committees performing the functions of an audit committee, a nominating committee and a remuneration committee, including the respective chairmen, must be independent.

In jurisdictions where DCS is permitted, “one-share-one vote” concept is provided as a default principle, however, it is expected that the public shareholders of the listed class of shares hold ordinary shares with one share one vote (OV) structure and the founder/ promoters hold the DCS with superior voting rights or MV structures, thus retaining control. S&P 500 has removed Snap from their index and has decided to bar new entrants with multiple classes of shares from the S&P 500.

> Regulators’ views on DCS12 structures:

- ~700 public companies in the US have DCS structures, predominant listed ones being Google, Facebook, Snapchat, Nike and Alibaba. There is ongoing debate in the SEC about the continuation of DCS13.

- There is increasing investor activism against concentrated voting rights with a few founders/

- Hong Kong and Singapore recently allowed Dual-class shares to encourage more new-technology firms to list.

- In the UK14, DCS structures were used in the 1960s to protect corporations from hostile takeovers or for the Queen to have ‘golden share’, before institutional investors expressed strong opposition to such structures. DSC is presently not allowed in the UK

- Over the past decade, a number of European governments have implemented or debated the use of different voting rights.

- US, Canada, HK, Singapore, Denmark, Spain, Sweden15and Italy allow dual-class shares. Germany, Spain, China, Australia disallow listing of shares of companies with DCS structures.

6. Market Considerations and Companies with Listed DVRs in India

The Amendment to Companies Act, 1956 in the year 2000 (Section 86 of the Companies Act, 1956, read with Rules of 2001) allowed, for the first time, issuance of shares with differential voting rights. Similar provisions are in the Companies Act, 2013 (Section 43 of the Companies Act, 2013, read with applicable Rules).

Only 5 listed companies have issued DVRs to the public in India till now viz. Tata Motors; Pantaloons Retails (Now: Future Enterprises Ltd.); Gujarat NRE Coke Ltd.; Jain Irrigation Systems Ltd. and Stampede Capital.

History and analysis of the DVRs shares issued by some Indian Corporates is given hereunder:

Sr. No. |

Company

|

Year of

|

Features |

|||||||||||||||||||||||

1. |

Tata Motors |

2008 |

> Tata Motors came out with Rights issue of DVR Shares after 8 years of amendment in Co. Act.> To fund the Jaguar – Land Rover acquisition> Issued 6.4 crores DVRs (“A” Ordinary Shares) priced at Rs. 305 per share as against Rs. 340 for an ordinary share as Rights issue. (10% discount)> DVRs has 5% higher dividend on these shares as compared to ordinary shares> DVRs carry 1/10th voting rights> The issue was undersubscribed and promoter subscribed to the unsubscribed DVRs> These DVRs reported very low trading volumes> Market price of DVRs as on Oct 8, 2018 was Rs. 115.45 and that of ordinary shares it was Rs. 212.75 (45% discount).> An analysis of average trading in the DVRs as compared to Ordinary shares in last one month is given hereunder:

|

|||||||||||||||||||||||

2. |

Pantaloons Retails (Now: Future Enterprises Ltd.) |

2009 |

> Pantaloons issued DVRs as bonus shares with the ordinary

|

|||||||||||||||||||||||

Average No. of shares traded |

Weighted Average Trading Price (Rs.) |

|||

Period |

Ordinary |

DVRs |

Ordinary |

DVRs |

Last one month (Sep 07 to Oct 05, 2018) |

1,24,598 |

2,105

|

42 |

41 |

Last one year (Oct 06, 2017 to Oct 05, 2018) |

4,43,594 |

4,991

|

43 |

42 |

In 2009, in the matter of Anand Pershad Jaiswal and Ors upheld the issuance of DVR shares which resulted in an promoters who held only 32% of economic stake in the company,

Following this judgement, SEBI came up with letter dated July 21, 2009 addressed to all stock exchanges which prohibited issue of DVRs with superior rights as to dividend or voting. Similar provisions are there in Reg. 41(3) of SEBI LODR Regulations mentioned above.

So now an issue of the likes of Tata Motors or Pantaloons with higher dividends with lower voting rights is not possible.

3.

Gujarat NRE Coke Ltd. (post SEBI letter dated 21.07.2009)

2009

> DVR were issued as bonus shares in the ratio of one DVR bonus share for every 10 equity shares

> DVR bonus shares had a voting right which was 1/100th of an ordinary share

> The dividend rights are at par with ordinary sharesØ

> Trading in the scrip of company is suspended due to procedural reasons. NCLT has ordered liquidation of company under The Insolvency and Bankruptcy Code, 2016.

4.

Jain Irrigation Systems Ltd.

2011

> DVR shares were issued as bonus shares in the ratio of 1 DVR Bonus equity share for every 20 ordinary equity shares.

> DVR bonus shares had a voting right which was 1/10th of an ordinary share

> The dividend rights are at par with ordinary shares

> Market price of DVRs as on 08.10.2018 was Rs.41.95 and that of ordinary shares it was Rs.61.45

> An analysis of average trading in the DVRs as compared to Ordinary shares in last one month is given hereunder:

Average No. of shares traded |

Weighted Average Trading Price (Rs.) |

|||

Period |

Ordinary |

DVRs |

Ordinary |

DVRs |

Last one month (Sep 07 to Oct 05, 2018) |

8,55,875 |

8,429 (1% of ordinary shares) |

76 |

50 (34% Dis.) |

Last one year (Oct 06, 2017 to Oct 05, 2018) |

9,55,672 |

27,884 (2.91% of ordinary shares) |

104 |

65 (36% Dis.) |

Share price performance* of DVRs in India:

| Particulars | CMP (₹) |

52 week High (₹) | 52 week Low (₹) | Dividend per Share (₹) |

Market Capitalisation (₹ Crores) |

| Tata Motors | 468.45 | 598.40 | 336.00 | 0.20 | 88,039.58 |

| Tata Motors DVR | 278.50 | 378.15 | 244.15 | 0.30 | 14,232.98 |

| Gujarat NRE Coke | 2.75 | 4.40 | 2.45 | 0.50 | 169.46 |

| (17.09.2012) | |||||

| Gujarat NRE Coke DVR | 2.15 | 3.85 | 1.70 | 0.50 | 7.56 |

| (17.09.2012) | |||||

| Futures Enterprises Ltd. | 26.90 | 156.45 | 14 | 0.10 | 496.41 |

| Futures Enterprises DVR | 26.65 | 139.80 | 12.45 | 0.14 | 29.16 |

| Jain Irrigation Systems | 89.55 | 108.60 | 54.50 | 0.50 | 2,846.52 |

| Jain Irrigation Systems DVR | 59.40 | 66.90 | 37.05 | 0.50 | 80.36 |

| Stampede Capital# | 1.50 | 10.75 | 1.45 | Nil | 8.59 |

| Stampede Capital DVR# | 1.90 | 19.10 | 1.90 | Nil | 43.51 |

*data as on March 10, 2017; Source- NSF and Bloomberg Note- CMP= Current Market Price, MC=Market Capitalisation

# data as on October 10, 2018.

DVRs are traded at lower price than ordinary shares but earned better dividend as compared to ordinary shares.

Considering the strict corporate governance requirements for companies to list dual class shares in India and the various laws protecting the rights of DVR shareholders against hostility, it can be argued that the discount of 35-45% for DVR shares is a bit excessive. This might be partly explained by the fact that these shares are not understood and tracked by investors, and that we might see the discount narrowing once there is more awareness about the features of such shares in the market.

Even a few years after shares with differential voting rights (DVRs) were introduced in India, very few companies have issued DVR shares. Some of them continue to trade at a big discount vis-à-vis ordinary shares. Very low additional dividends, discomfort with losing voting powers, and lower interest among investors seem to be the reasons.

The DVR construct in India is unique. In India, it is possible to issue shares with inferior (less than one vote per share) voting rights. Further, in the case of India, both the classes of shares are listed, whereas precedents from the US (except a few cases such as Alphabet) and regulations from HK and Singapore permit listing of the ordinary shares and shares while the multiple rights, held by the founders, remain unlisted.

The comparison of trading pattern of DCS in US and India is given in Annexure 3.

7. Recommendations of the DVR Group

Issuance of Equity Shares with Differential Voting Rights

The expressions “differential voting rights” and “dual class shares” are generic in nature. They can mean shares carrying superior voting rights (a multiple of voting power on an ordinary equity share) or shares carrying inferior voting rights (a fraction of the voting power on an ordinary equity share). In addition to voting rights, there can be other differential rights such as dividends etc.

An ordinary equity share is an equity share carrying one vote for one share. For clarity, in this Report, “SR Shares” will mean shares with superior voting rights as compared to ordinary equity shares and “FR Shares” means shares with fractional voting rights as compared to ordinary equity shares. References to the term “DVR” will mean shares with differential voting rights in a generic manner i.e. including SR Shares as well as FR Shares.

This Report is a product of deliberations of the Group formed by the Primary Market Advisory Committee to work on the subject at its meetings held on 4th October, 2018, 15th October, 2018, 3rd November 2018 and 2nd January, 2019.

This Report proposes to structure the regulation of DVR issuance under two broad heads. The broad heads will cover issuance by companies whose equity shares are already listed on stock exchanges; and companies with equity shares not hitherto listed but proposed to be offered to the public.

Conditions Precedent

A company would be entitled to issue DVR Shares, subject to following pre-conditions:

- issue of DVR Shares must have been be authorized in the articles of association of the company; and

- the issue of DVR Shares is authorized by a special resolution passed at a general meeting of the shareholders (for companies already listed, by way of e-voting in accordance with Companies Act, 2013) with notice of specific matters, including but not limited to, size of issuance, ratio of the difference in the voting rights, rights as to differential dividends, if any, sunset clause, “coat-tail provisions”, etc., as made applicable by SEBI regulations to be notified in this regard.

COMPANIES WHOSE EQUITY SHARES ARE ALREADY LISTED – ISSUANCE OF FR SHARES

First issue of FR Shares

A company, whose equity shares are already listed and traded on a recognized stock exchange for at least one year, shall be permitted to issue FR Shares by way of: (i) rights issue; (ii) bonus issue pro rata to all equity shareholders; or (iii) a Follow-on Public Offer (“FPO”) of FR shares͘ The first two would provide the FR shares to all existing equity shareholders while the third would provide a right to all existing shareholders to subscribe to the FR shares, along with third parties.

Subsequent issues of FR Shares once FR Shares are already listed

Rights Issue or Bonus Issue: A company that has already listed FR Shares shall be eligible to transact a rights issue or a bonus issue of FR Shares of the same class to all shareholders on a pari-passu basis.

Qualified Institutions Placement (“QIP”) or preferential issue: A company, whose FR Shares are listed for at least one year, shall be eligible to do a preferential issue or a QIP of FR Shares of the same class.

Pricing: The pricing of FR shares shall be in accordance with regulatory considerations applicable to mode of issuance of FR Shares.

Depository Receipts: A company whose FR Shares are listed for at least one year shall be eligible to issue depositary receipts where the underlying shares are FR Shares.

Convertible Instruments: A company can issue convertible instruments which will convert into FR Shares subject to applicable regulatory considerations.

Face Value of FR Shares: The face value of a company’s FR Shares shall be the same as that of its ordinary equity shares.

Number of FR Shares: The number of FR Shares that may be issued by a company shall be subject to provisions of the Companies Act, 2013 and the rules framed thereunder.

Fast-track: A company shall be eligible to issue FR Shares in a rights issue or an FPO through the fast-track method in case it meets the eligibility criteria of fast-track issuances.

Voting and Other Rights on FR Shares: The FR Shares shall not exceed a ratio of 1:10, i.e. one vote as applicable to one Ordinary Equity Share, would be voting entitlement on 10 FR Shares. The ratio can be in full numbers from 1:2 to 1:10. However, at any point of time, the company can only have one class of FR Shares.

The company shall disclose any other rights that shall be provided (and also disclose those not provided) to the holders of FR Shares.

Dividends: The company may, at its discretion, decide to pay additional dividend per FR Share compared to dividend paid on Ordinary Equity Share, which shall be higher than the dividend per Ordinary Equity Share and the same shall be stated in the terms of the offering. No dividend may be payable on FR Shares for such years where no dividend has been declared by the company for the ordinary equity shares.

Minimum Public Shareholding: The company shall comply with the minimum public shareholding requirements for each class of equity shares, both ordinary equity shares and FR Shares, subject to the provisions of the Securities Contracts (Regulation) Rules, 1957 (“SCRR”) and other applicable regulations formulated in this regard.

Conversion: The FR Shares can be converted into ordinary equity shares only in cases of schemes of arrangement.

Extinguishment: The FR Shares can be extinguished only through buy-back by the company or reduction of capital in accordance with applicable laws.

Delisting: The company can delist the FR Shares in accordance with the Securities and Exchange Board of India (Delisting of Equity Shares) Regulations, 2009. However, in the event ordinary equity shares of the company are delisted, the company shall be mandatorily required to delist the FR Shares.

Listing and Trading: The FR Shares shall be held in dematerialized form. However, FR Shares can be issued in physical form, if such FR Shares have been issued pursuant to a bonus issue and the underlying shares are held in physical form.

The FR Shares shall be listed and traded on all stock exchanges where ordinary equity shares of the company are listed with a separate identifier from the ordinary equity shares.

Post-Issue Disclosures: The shareholding pattern filed by the company with the stock exchanges shall provide the details of the FR Shares separately and in the format specified by the Securities and Exchange Board of India and the stock exchanges.

ESOPs: A company can issue ESOPs of FR Shares post the listing of such shares, subject to applicable laws.

Applicability of other SEBI Regulations: SEBI regulations in respect of buy-back, and takeovers shall apply to FR Shares, subject to such modification as may be required in the context of FR Shares. The FR Shares once listed shall not be delisted on a standalone basis and may be delisted as and when the ordinary equity shares are delisted. Required changes in these regulations are stated in Appendix 1 to this Report.

Bonus issue by the company which has issued FR shares: If a company which has issued FR shares issues bonus shares, then it shall issue to FR shareholders bonus FR shares in the same proportion in which bonus shares are issued on ordinary equity shares.

COMPANIES WHOSE EQUITY SHARES ARE PROPOSED TO BE LISTED – ISSUANCE OF SR SHARES

Eligibility

First issue of SR Shares

SR Shares can be issued only to the promoters of a company by an unlisted company. An unlisted company where the promoters hold SR Shares shall be permitted to do an Initial Public Offer (“IPO”) of only ordinary equity shares provided the SR Shares are held by the promoters for more than one year prior to filing of the draft offer document with SEBI.

Subsequent issue of SR Shares

A company shall not be permitted to issue SR Shares to any person, including to the promoters, in any manner whatsoever, including by way of rights issue or bonus issue, once its ordinary equity shares have been listed.

Subsequent issue of FR Shares

A company whose SR Shares and ordinary equity shares are already listed shall be permitted to issue FR Shares in terms of the applicable provisions for issue of FR Shares by listed companies.

Face Value of SR Shares

The face value of a company’s SR Shares shall be the same as of that of the ordinary equity shares͘ Number of SR Shares

A company shall be permitted to issue any number of SR Shares of the same class prior to an IPO, subject to provisions of the Companies Act, 2013.

Lock-in of SR Shares

All SR Shares shall remain under a perpetual lock-in after the IPO. Pledge of SR Shares

Creation of any encumbrance over SR Shares including pledge, lien, negative lien, non-disposal undertaking, etc. shall not be permissible. In other words, no third-party interest may be created over the SR Shares and any instrument purporting to do so would be void ab initio.

Voting and Other Rights on SR Shares

The SR Shares shall be treated at par with the ordinary equity shares in every respect except in the case of voting on resolutions.

The SR Shares shall be of a maximum ratio of 10:1, i.e. ten votes for every SR Share held. The ratio can be in whole numbers from 2:1 to 10:1. A ratio once adopted by a company shall remain valid for any subsequent issuances of SR Shares. A company can issue only one class of SR Shares.

Any rights or bonus issue by the company post-listing shall be offered only as ordinary equity shares to the holders of the SR Shares.

On certain matters to be notified by regulations, the SR Shares would be treated as having only one vote. The initial list of the same is set out in the “coat-tail” provisions set out later in this Report.

Dividend and Other rights

Post IPO, the SR shares shall be eligible for the same dividend and other rights as ordinary equity shares, except for superior voting rights.

Initial Disclosures

The company shall disclose, in the offer document, the names of all holders of SR Shares, with complete details of all special rights that have been provided to them.

No change in the terms of the SR Shares, which are favourable to the SR shareholders, shall be permitted post-IPO, other than sunset clause.

Minimum Public Shareholding

The company shall comply with the minimum public shareholding requirements in terms of the SCRR for the ordinary equity shares that will be listed. Post-listing, the voting rights with the promoters through the SR Shares and ordinary equity shares shall not exceed 75% of the total voting rights.

Coat-tail Provisions

Post-IPO, the SR Shares shall be treated as ordinary equity shares in terms of voting rights (i.e. one SR share one vote) in the following circumstances:

- provisions relating to appointment or removal of independent directors and/or auditor;

- in case there is a change in control of the company;

- any contract or agreement of the company with any person holding the SR Shares, in excess of the materiality threshold prescribed under Regulation 23 of the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirement) Regulations, 2015 (“SEBI LODR Regulations”);

- voluntary winding up of the company;

- any material changes in the company’s Article of Association or Memorandum, including but not limited to, undertaking variation in the voting rights of the shareholders, changing the principal objects of the company, granting special rights in favour of a particular shareholder or shareholder groups and such other items as may be prescribed by the SEBI;

- initiation of a voluntary resolution plan under the Insolvency and Bankruptcy Code, 2016;

(g) extension of the validity of the SR Shares post completion of 5 years from date of listing of ordinary equity shares; and

(h) any other provisions notified by SEBI in this regard from time to time.

Sunset Clause/ Conversion of SR Shares

The SR Shares shall get converted into ordinary equity shares on the 5th anniversary of the listing of the Ordinary Shares of the company i.e. they would lose their superior voting rights and each SR Share would carry an entitlement to a single vote as if it were an Ordinary Equity Share. The validity of the SR Shares can be extended by another 5 years with the approval shareholders by way of a special resolution in a general meeting where all members vote on one-share-one vote basis irrespective of the nature of their shareholding. The promoters, however, may do an accelerated conversion of their SR Shares into ordinary equity shares at any time prior to the 5th anniversary or such extended period.

The SR Shares shall get compulsorily converted into ordinary equity shares in the event of a merger or acquisition of the company or whenever these are sold by the identified promoters who hold such shares or in the case of demise of the promoter(s). Transfer of SR Shares amongst promoters or persons of the promoter group(s), even though they are inter-se transfers between persons acting in concert, shall not be permitted.

Listing and Trading

All SR Shares shall be held in dematerialized form and shall be listed on the main board platform of the recognized stock exchanges. For listing of SR Shares, exemption will be granted from Rule 19(2)(b) of SCRR. The SR Shares, however, cannot be traded except upon conversion into ordinary equity shares.

Post-Issue Disclosures

The shareholding pattern to be filed by the company with the stock exchanges shall provide the details of both ordinary equity shares and SR Shares in the format specified by SEBI and the stock exchanges.

Applicability of other SEBI Regulations

SEBI regulations in respect of buy-back, and takeovers shall be applicable to SR Shares, subject to such modification as may be required in the context of SR shares.

Appendix 1 Relevant Provisions in Acts/Regulations/Rules and Suggested Changes

The Companies Act, 2013

Pursuant to Rule 4(1)(d) of the Companies (Share Capital and Debenture) Rules, 2014, “the company must have a consistent track record of distributable profits for the last 3 years” in case it desires to issue DVR Shares.

SEBI permits IPOs of companies without a consistent track record of distributable profits for the last 3 years under Regulation 6(2) of the SEBI ICDR Regulations. New generation technology companies and innovative technologies primarily focus on growing revenue or gross merchandise value in order to rapidly scale their business in the initial years by concentrating on customer outreach and business expansion, and subsequently aim to generate profits. Additionally, new generation technology companies and innovative companies focus on sacrificing short term financial gains in the event certain projects create long term value for shareholders. The current regulatory regime prohibits such companies from issuing DVR shares. The extant provision should be amended to clarify that SEBI standards on to be listed companies as covered under Regulation 6(2) of the SEBI ICDR Regulations would be applicable in case of companies without a consistent track record of distributable profits.

SEBI Regulations

SEBI ICDR Regulations

The SEBI ICDR Regulations do not have a provision for a company to have dual class shares at the time of IPO.

The SEBI ICDR Regulations will need to be amended to allow SR Shares to be held by the promoters’ post the listing of the company’s ordinary equity shares. Further, provisions with respect to issuance of FR Shares post the listing of the company’s ordinary equity shares through modes such as Rights/ Bonus/ follow on would need to be incorporated.

Further, SEBI ICDR Regulations need to be amended to include provisions relating to coat-tail; sunset clause in case of SR Shares; restrictions on transferability of SR Shares, differential dividend related disclosures in case of FR Shares, etc.

SCRR

The SCRR provides for the minimum offer and allotment to public in terms of offer document, which shall be:

(a) at least 25% of each class or kind of equity shares! debenture convertible into equity shares issued by the company, if the post issue market capitalization of company is less than or equal to 1600 crore rupees.

(b) at least such percentage of each class or kind of equity shares! debenture convertible into equity shares issued by the company equivalent to the value of 400 crore rupees, if the post issue market capitalization of the company is more than 1600 crore rupees but less than or equal to 4000 crore rupees.

(c) at least 10% of each class or kind of equity shares / debenture convertible into equity shares issued by the company, if the post issue market capitalization of company is above 4000 crore rupees.

A company with multiple classes of equity shares at the time of undertaking an IPO, is required to make an offer of each such class of equity shares to the public in an IPO. The minimum dilution and minimum subscription requirements as prescribed under Rule 19(2)(b) of SCRR have to be met separately for each class of equity shares. In addition, a company with multiple classes of equity shares at the time of an IPO does not have an option of listing only one or some of the classes and should mandatorily list all classes of its equity shares, including equity shares with DVR. In light of the abovementioned regulatory framework and the challenge in successfully concluding an IPO for each class of the equity shares, till date, no company has undertaken an IPO with multiple classes of equity shares in India.

In light of the above rule, Rule 19(2)(b) of the SCRR must be amended to permit companies with multiple classes of shares to list one or more classes of shares to the exclusion of other classes of shares, so that SR shares held by promoters can remain unlisted while ordinary shares can be listed.

SEBI LODR Regulations

Regulation 41(3) of the SEBI LODR Regulations states that the listed entity shall not issue shares in any manner which may confer on any person, superior rights as to voting or dividend vis-à-vis the rights on equity shares that are already listed.

The Regulations shall need to be amended to allow Superior Rights Shares to be held by the promoters post-IPO of its ordinary equity shares and also allow additional dividend for FR shares.

SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 (“SEBI Takeover Code”)

1) Provisions Relating to Trigger of Open Offer:

The SEBI Takeover Code is applicable to both direct and indirect acquisitions of voting rights in or control over a target company. In accordance with the provisions of the SEBI Takeover Code, an acquirer is required to make a public announcement of an open offer, if an acquirer is entitled to exercise 25% or more shares or voting rights in a target company, in terms of Regulations 3 and 4 of the SEBI Takeover Code.

In light of the above regulations, Regulation 10 of the SEBI Takeover Code should be amended to clarify that any increase beyond the threshold of entitlement to voting rights as stipulated in Regulation 3 of the SEBI Takeover Code would not trigger an open offer obligation in the hands of the person acquiring voting rights beyond such threshold by reason of the lapse of superior voting power and conversion of SR Shares into ordinary equity shares provided that there is no attendant change in control in favour of the person crossing such threshold.

2) Disclosure requirements:

As change in voting rights due to extinguishment of voting right on SR Shares is an involuntary act on behalf of holder of ordinary equity shares, no disclosure would be required for acquisition of additional voting right by holder of the ordinary equity shares in such situation under Regulation 29 of the SEBI Takeover Code. The format of disclosure under Regulation 30 of the SEBI Takeover Code must be modified to provide for separate disclosure of voting rights for SR Shares, FR Shares and ordinary equity shares and consolidated voting right.

3) Provisions relating to open offer:

In case of open offer, offer need to be made for 26% of outstanding ordinary equity shares and 26% of the outstanding FR Shares.

The pricing of open offer for ordinary equity shares will be based on trading price of ordinary equity shares and pricing of FR Shares will be based on trading pricing of FR shares.

Securities and Exchange Board of India (Buy- Back of Securities) Regulations, 2018 (‘Buy Back Regulations’)

Reservation

Pursuant to Regulation 6 of the Buy Back Regulations through the Tender Offer, a company can buy-back its shares or other specified securities from its existing securities holders on a proportionate basis. Further, 15 per cent of the number of securities proposed to be bought back by the company is required to be reserved for small shareholders.

Buy Back Regulations should be amended to clarify that (i) company will be required to buy back both ordinary equity shares and FR Shares. Allocation of buy back amount between ordinary equity shares and FR Shares will be in the proportion of paid up capital of the company. For this purpose, SR Shares will be deemed to be part of ordinary equity shares, and (ii) the current reservation of 15% for small shareholders would apply to both small shareholders holding FR Shares and small shareholders holding ordinary equity shares.

Spill Over

The Buy Back Regulations must be amended to provide for spill over between buy back for ordinary equity shares and FR Shares in case of undersubscription in one category and oversubscription in another category. In case shares tendered in one of the categories is less than the number of shares to be bought in that category, companies must be permitted to buy back additional shares from the category where shareholders have shown interest to tender shares in excess of the maximum permissible limit, subject to compliance with minimum public shareholding norms prescribed under SCRR.

Pricing

Pursuant to Regulation 5(iv)(c)(i) of the Buy Back Regulations, in the event of a buy-back of securities through a tender offer, the explanatory statement must include the maximum price at which the buy-back of shares shall be made. Additionally, pursuant to Rule 17 of the Companies (Share Capital and Debentures) Rules, 2014 read with Section 68 of the Companies Act, 2013, a company is free to choose the method for undertaking the buy back and is further required to include the basis for arriving at the buy-back price in the explanatory statement.

Buy Back Regulations should be amended to permit, in case of companies that have issued SR Shares, FR Shares and ordinary equity shares, to price the SR Shares and ordinary equity shares with identical price, while FR Shares can be priced differentially. However, companies must be mandated to include justification for pricing FR Shares differentially.

Buy back through stock exchange mechanism

The provisions in relation to proportionate allocation amongst ordinary shares and FR shares as applicable in buy back through tender route will apply mutatis mutandis to buy-back through stock exchange mechanism.

Regulation 15 of the Buy Back Regulation will apply separately for buy-back of ordinary equity shares and FR Shares.

In case of buy-back through book building process, separate book building process would be carried out for ordinary equity shares and FR Shares.

Securities and Exchange Board of India (Delisting of Equity Shares) Regulations, 2009 (“Delisting Regulations”)

Floor Price:

The floor price will be calculated separately for ordinary equity shares and FR Shares as per the existing formula under SEBI Delisting Regulations.

Pursuant to Regulation 15 of the SEBI Delisting Regulations, the offer price shall be determined through book building process.

The SEBI Delisting Regulations must be amended to clarify, in case of companies with FR Shares and ordinary equity shares, separate reverse book building processes must be employed for determining the offer price of FR Shares and ordinary equity shares.

Related party transactions

23. (1) The listed entity shall formulate a policy on materiality of related party transactions and on dealing with related party transactions [including clear threshold limits duly approved by the board of directors and such policy shall be reviewed by the board of directors at least once every three years and updated accordingly].

Explanation—A transaction with a related party shall be considered material if the transaction(s) to be entered into individually or taken together with previous transactions during a financial year, exceeds ten per cent of the annual consolidated turnover of the listed entity as per the last audited financial statements of the listed entity.

[ (1A) Notwithstanding the above, a transaction involving payments made to a related party with respect to brand usage or royalty shall be considered material if the transaction(s) to be entered into individually or taken together with previous transactions during a financial year, exceed two per cent of the annual consolidated turnover of the listed entity as per the last audited financial statements of the listed entity.]

(2) All related party transactions shall require prior approval of the audit committee.

(3) Audit committee may grant omnibus approval for related party transactions proposed to be entered into by the listed entity subject to the following conditions, namely—

(a) the audit committee shall lay down the criteria for granting the omnibus approval in line with the policy on related party transactions of the listed entity and such approval shall be applicable in respect of transactions which are repetitive in nature;

(b) the audit committee shall satisfy itself regarding the need for such omnibus approval and that such approval is in the interest of the listed entity;

(c) the omnibus approval shall specify:

(i) the name(s) of the related party, nature of transaction, period of transaction, maximum amount of transactions that shall be entered into,

(ii) the indicative base price/current contracted price and the formula for variation in the price if any; and

(iii) such other conditions as the audit committee may deem fit:

Provided that where the need for related party transaction cannot be foreseen and aforesaid details are not available, audit committee may grant omnibus approval for such transactions subject to their value not exceeding rupees one crore per transaction.

(d) the audit committee shall review, at least on a quarterly basis, the details of related party transactions entered into by the listed entity pursuant to each of the omnibus approvals

(e) such omnibus approvals shall be valid for a period not exceeding one year and shall require fresh approvals after the expiry of one year.

(4) All material related party transactions shall require approval of the shareholders through resolution and [no related party shall vote to approve] such resolutions whether the entity is a related party to the particular transaction or not:

Provided that the requirements specified under this sub-regulation shall not apply in respect of a resolution plan approved under section 31 of the Insolvency Code, subject to the event being disclosed to the recognized stock exchanges within one day of the resolution plan being approved;

(5) The provisions of sub-regulations (2), (3) and (4) shall not be applicable in the following cases:

(a) transactions entered into between two government companies;

(b) transactions entered into between a holding company and its wholly owned subsidiary whose accounts are consolidated with such holding company and placed before the shareholders at the general meeting for approval.

Explanation—For the purpose of clause (a), “government company(ies)” means Government company as defined in sub-section (45) of section 2 of the Companies Act, 2013.

(6) The provisions of this regulation shall be applicable to all prospective transactions.

(7) For the purpose of this regulation, all entities falling under the definition of related parties shall [not vote to approve the relevant transaction] irrespective of whether the entity is a party to the particular transaction or not.

(8) All existing material related party contracts or arrangements entered into prior to the date of notification of these regulations and which may continue beyond such date shall be placed for approval of the shareholders in the first General Meeting subsequent to notification of these regulations.

[ (9) The listed entity shall submit within 30 days from the date of publication of its standalone and consolidated financial results for the half year, disclosures of related party transactions on a consolidated basis, in the format specified in the relevant accounting standards for annual results to the stock exchanges and publish the same on its website.]

Annexure 1

DVRs: Some Judgments

An interesting perspective by the SEBI was presented in the case of Ashwin K Doshi V SEBI, wherein the law was primarily stressed upon the regulations and rules of SEBI but a constructive reference on the Companies Act (Amendment) was placed. The main issue for consideration was whether the transaction in question amounted to consolidation of control which in turn was a violation of SEBI regulations as no public offer was made. After referring to the Companies Act (Amendment) 2000, the judge was of the view that since a company can issue differential voting rights or non-voting rights shares therefore there is no prohibition in even transferring the control. However, two guiding factors before such transfer were also recorded and that is equality of treatment and opportunity to all shareholders and protection of interests of shareholders while administering regulations.

In the same year, Bombay High Court also laid down similar rules with regard to the applicability of DVRs in the corporations. In the case of Zycus Infotech, the appellant had issued shares with no voting rights from his equity share capital. This precedent essentially reasserted the law defining differential voting rights when the original owners gained control over their company. Since the new amendment as per 2013 Act was non-existent, hence the Companies Act, 2000 (Amendment) was applied. As per the 2000 Act, only two type of shares could be issued, “equity shares” and “preferential shares”͘ In equity shares, further demarcation is done, as the shares can be allotted on the basis of dividend, voting or otherwise.

Annexure 2

Regulatory updates/ investor feedback on DVRs

1. Proposed updates: In February 2018, the SEC’s Investor Advisory Committee issued a paper regarding dual class and other “entrenching governance structures” and made a series of recommendations to the staff of the Division of Corporation Finance. The proposals included additional disclosures relating to risks that may accompany dual class structures as well as data regarding the difference between the economic ownership of the control group versus the voting rights that accompany the super voting shares owned by that group. In response to the recommendations of the Investor Advisory Committee, a bill has been introduced in Congress (the Enhancing Multi-Class Share Disclosures Act) that would enhance the disclosure obligations of issuers with respect to disparate voting structures. The enhanced disclosure would require companies to clearly show the difference between the voting power and economic rights of a shareholder or group of shareholders owning “super voting” shares. To date, neither IOSCO nor OECD has adopted a “one share one vote” principle in connection with their governance related studies and position papers. While OECD endorses the notion that all holders within a given class should have the same voting rights, it has also recognized that many countries permit multiple class capital structures with disparate voting rights and “does not take a position on the desirability of “one share, one vote”.

2. Investors Petition NYSE, NASDAQ to Curb Listings of IPO Dual-Class Share Companies Traders Magazine Online News, October 24, 201816

The Council of Institutional Investors (“CII”) recently filed petitions with the New York Stock Exchange (NYSE) and the NASDAQ, asking both to limit listings of companies with dual-class share structures.

Specifically, the petitions ask the exchanges to amend their listing standards to require that, going forward, companies seeking to list that have multiple share classes with differential voting rights include in their governing documents provisions that convert the share structure within seven years of the initial public offering (IPO) to “one, share-one, vote.” This will ensure voting power directly proportional to an investor’s capital at risk.

CII, which represents pension funds and other long-term investors, is urging the exchanges to act to counter the trend of companies going public with unequal voting rights, which deprive shareholders of the means to hold executives and directors accountable.

“While some companies that are controlled by virtue of special voting rights function as benevolent dictatorships, we have seen others stumble because of self-dealing, lack of strategic planning and ineffective boards,” said CII Chair Ash Williams, executive director and CIO of the Florida State Board of Administration. “When problems emerge, external shareowners have little recourse. Now, a consensus is emerging—among investors, companies and the law firms and other IPO gatekeepers—that time-based sunsets are a sensible solution to the growing problem of unequal voting rights, which poses danger to long-term resilience of an increasing number of companies.”

BlackRock, the largest global asset manager, believes that one share, one vote is the preferable structure for publicly listed companies. BlackRock also supports time-based sunset provisions for multi-class companies and believes that listing exchanges must play an important role.

“BlackRock believes that equal voting rights are a fundamental tenet of good corporate governance. Multiple stakeholders – including listing exchanges and policymakers – must play a role in setting effective corporate governance standards to protect shareholder rights,” said BlackRock Co-founder and Vice Chairman Barbara Novick. “We encourage U.S. exchanges to show global leadership on voting rights by requiring companies to either automatically convert or give shareholders the right to extend a multi-class structure. Doing so will re-establish the importance of equal voting rights for all public shareholders.”

Donna Anderson CFA, vice president and head of corporate governance at asset manager T. Rowe Price, said, “A confluence of events has led to what we believe is a growing consensus on the issues surrounding differential voting rights. We would like to see the U.S. stock exchanges lead the process to find a solution that serves the long-term interests of all market participants.”

California State Teachers’ Retirement System Chief Executive Officer Jack Ehnes said, “One of the strengths of the U.S. economy is the dynamism of U.S. companies. Successful American companies are constantly changing—and reinventing the way they do business. So it only makes sense that they should embrace change in their own governance that ultimately will strengthen shareholder value.”

“CalPERS believes in one share, one vote,” said Simiso Nzima, the California Public Employees’ Retirement System’s head of corporate governance. “However, we also understand that early in a company’s public life, there may be a need for protections that enable management to focus on building out a company’s vision and creating the long-term sustainable shareowner value we are looking for as investors. We strongly believe such protection should not be perpetual, and mandatory time-based sunsets should act as an important safeguard against managerial entrenchment.”

CII Executive Director Ken Bertsch agreed that there is convergence in favor of time-based sunsets within seven years after IPO as a condition of listing on a U.S. exchange:

- Recent academic research shows that while dual-class companies on average have a valuation premium at the time of IPO, that advantage dissipates between six and nine years after IPO and then disappears. “We believe seven years is sufficient time for a company to capitalize on whatever benefits and control a multi-class structure provides,” Bertsch said. “After that, it starts to look like a management-entrenchment device.”

- A growing number of companies are making their public debut with time-based sunsets. Of 38 S. companies that went public in 2017 and 2018 with multi-class structures, CII has tracked 11 (29%) that incorporated simple time-based sunsets.

- A small but growing share of multi-class IPO companies have used time-based sunsets Examples include Groupon (converted to a single share class after five years), Texas Roadhouse (converted after five years) and MaxLinear (converted after seven years).

- Investors have soured on Snap and other high-profile companies (Altice USA, Blue Apron) that made their IPO authorizing zero-vote shares.

- Well-established dual-class companies (notably CBS and Viacom) have been hugely distracted by fights related to control, and even privately-owned Uber decided to go to one-share, one-vote after scandal rocked the company

Background:

Silicon Valley entrepreneurs like to boast about disrupting the status quo. With good reason: From Alphabet (Google’s parent) to Zillow, young tech companies have achieved success by upending traditional business models in one sector after another. But when it comes to how they govern their companies many founders embrace frameworks that are bulwarks against change. In recent years, a significant number of start-up companies, most but not all tech-based, have gone public with dual- or even triple-class stock structures with unequal voting rights that guarantee founders and other insiders voting control that can last decades—even as their equity stake shrinks. In 2017, we saw the advent of zero-vote shares for outside holders when Snap went public.

Last year, 19% of U.S. companies that went public on U.S. exchanges had at least two classes of stock with differential voting rights. That is up from just 1% in 2005. In most cases, the superior class has 10 votes per share, while the inferior class has one vote per share. Supporters say this enables entrepreneurs to focus on the long term and resist pressure from investors to keep

earnings growing every quarter.

But this “founder knows best” approach challenges the bedrock corporate governance principle of “one share, one vote”: Providers of capital should have a right to vote in proportion to the size of their ownership. A single class of common stock with equal voting rights makes the board of directors accountable to all of the shareholders—and more likely to respond when management stumbles. Multi-class structures deprive public shareholders of a meaningful voice in how the company is run because the public shareholders lack the votes to influence the board or management.

Academic research supports time-based sunsets͘ A recent study, “The Life Cycle of Dual Class Firms,” found that while multi-class companies have a value premium over single-class counterparts at the time of their initial public offering (IPO), that benefit fades to a discount six to nine years after IPO. Other studies show that multi-class companies have a substantially lower total shareholder return compared to single-class companies over 10 years.

The Securities and Exchange Commission (SEC) believes it lacks the statutory authority to compel U.S. exchanges to amend their listing rules. Over the past year, providers of benchmark indexes—FTSE Russell, MSCI and S&P Dow Jones—have stepped into the breach, with varying curbs on multi-class companies in indexes that are used widely by institutional investors. A listing standard would put all dual-class companies on the same footing.

Comparison of trading pattern of DCS in US and India

Note

1. https://www.directorsandboards.com/news/pros-cons-dual-class-stock-structure-two-corporategovernance-experts-battle-it-out

2. http://www.pionline.com/article/20180216/ONLINE/180219888/sec-commissioner-calls-for-curb-on-dualclass-forever-shares#1

3. https://indiacorplaw.in/2009/03/differential-voting-rights-ruling-by.html

4. https://www.nasdaq.com/article/facebook-fb-decides-against-the-creation-of-class-c-shares-cm8504694

5. https://www.law.ox.ac.uk/business-law-blog/blog/2018/01/should-securities-regulators-allow-companiesgoing-public-dual-class

6. https://www.recode.net/2017/6/13/15788892/alphabet-shareholder-proposals-fair-shares-counted-equallyno-supervote

7. http://blogs.marketwatch.com/thetell/2014/04/02/google-investors-are-about-to-get-goog-and-googlshares-in-stock-split/

8. https://www.washingtonpost.com/news/on-leadership/wp/2018/05/10/a-huge-pension-fund-saysfacebook-is-like-a-dictatorship/ ?noredirect=on&utm_term=.bfa99de5fe16

9. https://www.reuters.com/article/us-usa-investors-voting/top-u-s-funds-seek-sunset-rules-on-dual-classshare-listings-idUSKCN1M X37C

10. https://www.thestreet.com/story/13612197/1/viacom-and-27-other-stocks-that-come-with-restrictedvoting-rights.html56789

11. DCS structures currently not permitted on London SE

12. https://www.bloomberg.com/quicktake/dual-class-shares

13. http://www.pionline.com/article/20180216/ONLINE/180219888/sec-commissioner-calls-for-curb-on-dualclass-forever-shares#