Introduction: The Reserve Bank of India (RBI) released its Monetary Policy Statement for 2023-24 on August 10, 2023. The Monetary Policy Committee (MPC) met and discussed the current economic situation before announcing its decisions related to the policy repo rate and other key rates. The policy aims to balance inflation control with supporting economic growth.

Analysis: The RBI’s MPC decided to keep the policy repo rate under the liquidity adjustment facility unchanged at 6.50 percent. The standing deposit facility rate and the marginal standing facility rate were also maintained at 6.25 percent and 6.75 percent, respectively. The focus of the policy is on gradually withdrawing accommodation to ensure that inflation aligns with the target while continuing to support growth.

The assessment highlights the global economy’s slowdown, with varying growth trajectories across regions. The domestic economy remains resilient, supported by urban and rural demand, industrial production growth, and various indicators such as e-way bills, toll collections, and composite purchasing managers’ index (PMI). However, risks from external factors like weak global demand and geopolitical tensions are noted.

The outlook for inflation indicates a temporary spike due to factors like vegetable prices, which is expected to correct as fresh market arrivals happen. The RBI projects CPI inflation at 5.4 percent for 2023-24, with risks balanced across quarters. On the economic growth front, GDP growth for 2023-24 is projected at 6.5 percent, with Q1 at 8.0 percent, Q2 at 6.5 percent, Q3 at 6.0 percent, and Q4 at 5.7 percent.

The RBI emphasizes vigilance regarding supply disruptions caused by adverse weather conditions, and it’s prepared to take appropriate actions to prevent persisting effects on prices. The MPC’s decision to maintain the policy repo rate unchanged reflects the cumulative rate hikes undertaken previously.

Conclusion: The RBI’s August 2023 monetary policy maintains a delicate balance between controlling inflation and supporting economic growth. With an unchanged policy repo rate and a focus on aligning inflation to the target, the central bank aims to ensure stable and sustainable economic conditions amidst global and domestic uncertainties.

******

RESERVE BANK OF INDIA

Monetary Policy Statement, 2023-24 Resolution of the Monetary Policy Committee (MPC) August 8-10, 2023

Date : Aug 10, 2023

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (August 10, 2023) decided to:

- Keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 6.50 per cent.

The standing deposit facility (SDF) rate remains unchanged at 6.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent.

- The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

The main considerations underlying the decision are set out in the statement below.

Assessment

Global Economy

2. The global economy is slowing and growth trajectories are diverging across regions amidst moderating but above target inflation, tight financial conditions, simmering geopolitical conflicts, and geoeconomic fragmentation. Sovereign bond yields have hardened. The US dollar fell to a 15-month low in mid-July on expectations of an early end to the monetary tightening cycle, although it recouped some of the losses subsequently. Equity markets have gained on expectations of a soft landing for the global economy. For several emerging market economies, weak external demand, elevated debt levels and tight external funding conditions pose risks to their growth prospects.

Domestic Economy

3. Domestic economic activity is maintaining resilience. The cumulative south-west monsoon rainfall was the same as the long period average up to August 9, 2023 although the temporal and spatial distribution has been uneven. The total area sown under kharif crops was 0.4 per cent higher than a year ago as on August 4, 2023. The index of industrial production (IIP) expanded by 5.2 per cent in May while core industries output rose by 8.2 per cent in June. Amongst high frequency indicators, e-way bills and toll collections expanded robustly in June-July, while rail freight and port traffic recovered in July after remaining muted in June. The composite purchasing managers’ index (PMI) rose to a 13-year high in July.

4. Urban demand remains robust, with domestic air passenger traffic and household credit exhibiting sustained double digit growth. The growth in passenger vehicle sales has, however, moderated. In the case of rural demand, tractor sales improved in June while two-wheeler sales moderated. Cement production and steel consumption recorded robust growth. Import and production of capital goods continued in expansion mode. Merchandise exports and non-oil non-gold imports remained in contraction territory in June. Services exports posted subdued growth amidst slowing external demand.

5. Headline CPI inflation picked up from 4.3 per cent in May to 4.8 per cent in June, driven largely by food group dynamics on the back of higher prices of vegetables, eggs, meat, fish, cereals, pulses and spices. Fuel inflation softened during May-June, primarily reflecting the fall in kerosene prices. Core inflation (i.e., CPI excluding food and fuel) was steady in June.

6. The daily absorption of liquidity under the LAF averaged ₹1.8 lakh crore during June-July as compared with ₹1.7 lakh crore in April-May. Money supply (M3) expanded by 10.6 per cent y-o-y as on July 28, 2023 as against 10.1 per cent on May 19, 2023. Bank credit grew by 14.7 per cent y-o-y as on July 28, 2023 as compared with 15.4 per cent on May 19, 2023. India’s foreign exchange reserves stood at US$ 601.5 billion as on August 4, 2023.

Outlook

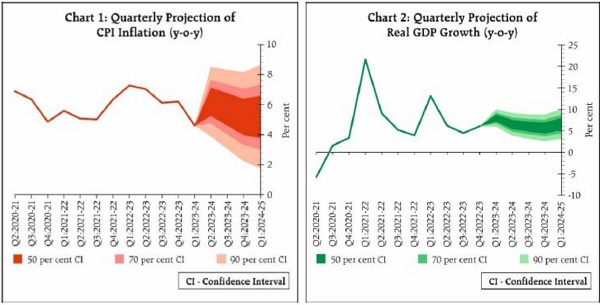

7. Going forward, the spike in vegetable prices, led by tomatoes, would exert sizeable upside pressures on the near-term headline inflation trajectory. This jump is, however, likely to correct with fresh market arrivals. There has been significant improvement in the progress of the monsoon and kharif sowing in July; however, the impact of the uneven rainfall distribution warrants careful monitoring. Crude oil prices have firmed up amidst production cuts. Manufacturing, services and infrastructure firms polled in the Reserve Bank’s enterprise surveys expect input costs to ease but output prices to harden. Taking into account these factors and assuming a normal monsoon, CPI inflation is projected at 5.4 per cent for 2023-24, with Q2 at 6.2 per cent, Q3 at 5.7 per cent and Q4 at 5.2 per cent, with risks evenly balanced. CPI inflation for Q1:2024-25 is projected at 5.2 per cent (Chart 1).

8. Looking ahead, the recovery in kharif sowing and rural incomes, the buoyancy in services and consumer optimism should support household consumption. Healthy balance sheets of banks and corporates, supply chain normalisation, business optimism and robust government capital expenditure are favourable for a renewal of the capex cycle which is showing signs of getting broad-based. Headwinds from weak global demand, volatility in global financial markets, geopolitical tensions and geoeconomic fragmentation, however, pose risks to the outlook. Taking all these factors into consideration, real GDP growth for 2023-24 is projected at 6.5 per cent with Q1 at 8.0 per cent; Q2 at 6.5 per cent; Q3 at 6.0 per cent; and Q4 at 5.7 per cent, with risks broadly balanced. Real GDP growth for Q1:2024-25 is projected at 6.6 per cent (Chart 2).

9. The headline inflation is likely to witness a spike in the near months on account of supply disruptions due to adverse weather conditions. It is important to be vigilant about these shocks with a readiness to act appropriately so as to ensure that their effects on the general level of prices do not persist. There are risks from the impact of the skewed south-west monsoon so far, a possible El Niño event and upward pressures on global food prices due to geopolitical hostilities. Domestic economic activity is holding up well, supported by domestic demand in spite of the drag from weak external demand. With the cumulative rate hike of 250 basis points undertaken by the MPC working its way into the economy, the MPC decided to keep the policy repo rate unchanged at 6.50 per cent, but with preparedness to undertake policy responses, should the situation so warrant. The MPC will maintain a close vigil on the evolving inflation scenario and remain resolute in its commitment to aligning inflation to the target and anchoring inflation expectations. The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth.

10. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted to keep the policy repo rate unchanged at 6.50 per cent.

11. Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth. Prof. Jayanth R. Varma expressed reservations on this part of the resolution.

12. The minutes of the MPC’s meeting will be published on August 24, 2023.

13. The next meeting of the MPC is scheduled during October 4-6, 2023.

(Yogesh Dayal)

Chief General Manager

Press Release: 2023-2024/723

*****

Date : Aug 10, 2023

Statement on Developmental and Regulatory Policies

This Statement sets out various developmental and regulatory policy measures relating to (i) Financial Markets; (ii) Regulation and Supervision; (iii) Payment Systems; and (iv) FinTech.

I. Financial Markets

1. Review of Regulatory framework for Financial Benchmark Administrators

In June 2019, the Reserve Bank issued a regulatory framework on administration of ‘significant benchmarks’ by benchmark administrators in the financial markets regulated by the Reserve Bank such as the USD/INR Reference Rate, Overnight MIBOR, and valuations of government securities administered by the Financial Benchmarks India Private Limited (FBIL). Considering the evolution of the domestic financial markets since then and global best practices, the regulations for financial benchmarks have been reviewed and it has been decided to put in place a comprehensive, risk-based framework covering administration of all benchmarks related to foreign exchange, interest rates, money markets and government securities such as benchmarks on certificate of deposits (CDs) rates, repo rates, and FX Options Volatility Matrix as well as other benchmarks on government securities. Revised Directions which are being issued separately, envisage regulatory prescriptions for benchmark administrators, encompassing, inter alia, governance and oversight arrangements, conflict of interest, controls, and transparency. These Directions will provide greater assurance about the accuracy and integrity of benchmarks.

II. Regulation and Supervision

2. Review of Regulatory Framework for NBFC – Infrastructure Debt Funds (IDF-NBFCs)

Infrastructure Debt Fund was created as a separate category of NBFCs in 2011. To enable the IDFs to play a greater role in financing of the infrastructure sector and to move towards the regulatory objective of harmonisation of regulations applicable to various categories of NBFCs, a review of the extant regulatory framework for IDFs has been undertaken in consultation with the Government of India. The revised framework envisages – (i) withdrawal of the requirement of a sponsor for the IDFs; (ii) permission to finance Toll Operate Transfer projects (ToT) as direct lenders, (iii) access to ECBs; and (iv) making tri-partite agreement optional for PPP projects. Detailed guidelines shall be issued shortly.

3. Responsible Conduct in Lending: Greater transparency in Interest Rate Reset of Equated Monthly Instalments (EMI) based Floating Interest Loans

The supervisory reviews undertaken by the Reserve Bank and the feedback and references from members of public have revealed several instances of unreasonable elongation of tenor of floating rate loans by lenders without proper consent and communication to the borrowers. To address the issue, it is proposed to put in place a proper conduct framework to be implemented by all REs to address the issues faced by the borrowers. The framework envisages that lenders should clearly communicate with the borrowers for resetting the tenor and/or EMI, provide options of switching to fixed rate loans or foreclosure of loans, transparent disclosure of various charges incidental to the exercise of these options, and proper communication of key information to the borrowers. The detailed guidelines in this regard shall be issued shortly.

4. Consolidation and harmonisation of instructions for Supervisory data submission

The Reserve Bank of India has, from time to time, issued several guidelines and instructions to its supervised entities (SEs) viz. SCBs, NBFCs, UCBs, AIFIs etc. for submission of supervisory returns. Certain issues are being faced by SEs while complying with these instructions due to changes in technology platforms, modes of submission, and variations in the return submission timeframes.

In order to consolidate and harmonise the instructions for submission of applicable Supervisory Returns, provide greater clarity and reduce the compliance burden, it is proposed to consolidate all the existing instructions on submission of data into a single Master Direction which will be a single point of reference for all SEs.

III. Payment Systems

5. Conversational payments in UPI

UPI, with its ease of usage, safety and security, and real-time feature, has transformed the digital payment ecosystem in India. Addition of many new features over time have enabled UPI to facilitate diverse payment needs of the economy. As Artificial Intelligence (AI) is becoming increasingly integrated into the digital economy, conversational instructions hold immense potential in enhancing ease of use, and consequently reach, of the UPI system. It is, therefore, proposed to launch an innovative payment mode viz., “Conversational Payments” on UPI, that will enable users to engage in a conversation with an AI-powered system to initiate and complete transactions in a safe and secure environment. This channel will be made available in both smartphones and feature phones-based UPI channels, thereby helping in the deepening of digital penetration in the country. The facility will, initially, be available in Hindi and English and will subsequently be made available in more Indian languages. Instructions to NPCI will be issued shortly.

6. Offline payments in UPI

To increase the speed of small value transactions on UPI, an on-device wallet called “UPI-Lite” was launched in September 2022 to optimise processing resources for banks, thereby reducing transaction failures. The product has gained traction and currently processes more than ten million transactions a month. To promote the use of UPI-Lite, it is proposed to facilitate offline transaction using Near Field Communication (NFC) technology. This feature will not only enable retail digital payments in situations where internet / telecom connectivity is weak or not available, it will also ensure speed, with minimal transaction declines. Instructions to NPCI will be issued shortly.

7. Enhancing transactions limits for small value digital payments

A limit of ₹200 per transaction and an overall limit of ₹2000 per payment instrument has been prescribed by the Reserve Bank for small value digital payments in offline mode including for National Common Mobility Card (NCMC) and UPI Lite. By removing the need for two-factor authentication for small value transactions, these channels enable faster, reliable, and contactless mode of payments for everyday small value payments, transit payments etc. Since then, there have been demands for enhancing these limits. To encourage wider adoption of this mode of payments and bring in more use cases into this mode, it is now proposed to increase the per transaction limit to ₹500. The overall limit is, however, retained at ₹2000 to contain the risks associated with relaxation of two-factor authentication. Instructions in this regard will be issued shortly.

IV. FinTech

8. Public Tech Platform for Frictionless Credit

With rapid progress in digitalization, India has embraced the concept of digital public infrastructure which encourages FinTech companies and start-ups to create and provide innovative solutions in payments, credit, and other financial activities. For digital credit delivery, the data required for credit appraisal are available with different entities like Central and State governments, account aggregators, banks, credit information companies, digital identity authorities, etc. However, they are in separate systems, creating hindrance in frictionless and timely delivery of rule-based lending.

To address this situation, a pilot project for digitalisation of Kisan Credit Card (KCC) loans of less than ₹1.60 lakh was started in September 2022. The pilot tested end-to-end digitalisation of the lending process in a paperless and hassle-free manner. The KCC pilot is currently underway in select districts of Madhya Pradesh, Tamil Nadu, Karnataka, UP, Maharashtra and the initial results are encouraging. The pilot also enables doorstep disbursement of loans in assisted or self-service mode without any paperwork. A similar pilot is being carried out for dairy loans based on milk pouring data with Amul in Gujarat.

Based on the learnings from the above pilots and expand the scope to all types of digital loans, a digital Public Tech Platform is being developed by the Reserve Bank Innovation Hub (RBIH). The Platform would enable delivery of frictionless credit by facilitating seamless flow of required digital information to lenders. The end-to-end digital platform will have an open architecture, open Application Programming Interfaces (APIs) and standards, to which all financial sector players can connect seamlessly in a ‘plug and play’ model.

The Platform is intended to be rolled out as a pilot project in a calibrated fashion, both in terms of access to information providers and use cases. It shall bring about efficiency in the lending process in terms of reduction of costs, quicker disbursement, and scalability.

(Yogesh Dayal)

Chief General Manager

Press Release: 2023-2024/724

*****

Date : Aug 10, 2023

Governor’s Statement: August 10, 2023

As we celebrate India’s 77th Independence Day in a few days, I am happy to note that the Indian economy is exuding enhanced strength and stability despite the massive shocks to global economy in recent years. Our economy has continued to grow at a reasonable pace, becoming the fifth largest economy in the world1 and contributing around 15 per cent to global growth. We have also made significant progress towards controlling inflation. Our banks remain healthiest in more than a decade with historically high levels of capital, declining levels of non-performing assets and rising profitability. Corporate balance sheets are robust, with lower leverage, improving debt servicing capacity and strong profitability. Lower current account deficit and ample capital flows have imparted strength to our external sector. The resultant accretion to forex reserves has provided a buffer against external shocks. Overall, India’s strong macroeconomic fundamentals have laid the foundations for sustainable growth.

2. In a moment like this, we need to continue with our efforts to maintain macro-financial stability while pushing our growth frontier further. India is uniquely placed to benefit from the ongoing transformational shifts in global economy in the wake of geopolitical realignments and technological innovations. A large economy marching ahead with vast domestic demand, untapped resources and demographic advantages, India can become the new growth engine for the world.

Decisions and Deliberation of the Monetary Policy Committee (MPC)

3. The Monetary Policy Committee (MPC) met on 8th, 9th and 10th August 2023. After detailed deliberation on all relevant aspects, it decided unanimously to keep the policy repo rate unchanged at 6.50 per cent. Consequently, the standing deposit facility (SDF) rate remains at 6.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent. The MPC also decided by a majority of 5 out of 6 members to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth.

4. Let me now explain the MPC’s rationale for these decisions on the policy rate and the stance. Headline inflation, after reaching a low of 4.3 per cent in May 2023, rose in June and is expected to surge during July-August led by vegetable prices. While the vegetable price shock may reverse quickly, possible El Niño weather conditions along with global food prices need to be watched closely against the backdrop of a skewed south-west monsoon so far. These developments warrant a heightened vigil on the evolving inflation trajectory. The cumulative rate hike of 250 basis points undertaken by the MPC is working its way into the economy. Nonetheless, domestic economic activity is holding up well and is likely to retain its momentum, despite weak external demand. Considering this confluence of factors, the MPC decided to remain watchful and evaluate the emerging situation. Consequently, the MPC decided to keep the policy repo rate unchanged at 6.50 per cent with preparedness to act, should the situation so warrant. The MPC remains resolute in its commitment to aligning inflation to the 4 per cent target and anchoring inflation expectations.

5. Further, with monetary transmission still underway2 and headline inflation remaining higher than the 4 per cent target, the MPC decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth.

Assessment of Growth and Inflation

Global Growth

6. The global economy continues to face daunting challenges of elevated inflation, high levels of debt, tight and volatile financial conditions, continuing geopolitical tensions, fragmentations and extreme weather conditions. Belying earlier apprehensions, a number of economies have demonstrated remarkable resilience and the grim prospects of hard landing appear to have receded. Nevertheless, global growth is likely to remain low by historical standards in the current year and next few years, despite the upward revision in the global growth forecast for 2023 by the IMF3. World merchandise trade volume growth is projected by the WTO to decelerate from 2.7 per cent in 2022 to 1.7 per cent in 2023. Headline inflation is easing unevenly across countries and remains above the target in major economies. While the pace of monetary tightening has been scaled down, policy rates could stay higher for longer. Financial markets, which had been buoyed by expectations of an early end to the cycle of monetary tightening, have turned volatile with sizeable two-way movements in response to recent rating event and incoming data.

Domestic Growth

7. These external factors are likely to impinge on the growth prospects of most major advanced and emerging economies. India is, however, expected to withstand these external headwinds far better than many other countries.

8. The momentum of overall economic activity in India continues to be positive. On the supply side, crop sowing has picked up with steady progress in the south-west monsoon.4 The temporal and spatial distribution of monsoon has, however, been uneven. Industrial activity is holding ground as is evident from the latest data on index of industrial production (IIP), core industries output and purchasing managers’ index (PMI) for manufacturing5. Buoyant services activity is reflected in healthy expansion in e-way bills, toll collections, railway freight and a sharp jump in services PMI.6 On the other hand, commercial vehicle sales and domestic air cargo traffic contracted during Q1: 2023-24.

9. Aggregate demand conditions continue to be buoyant. Among urban demand indicators, domestic air passenger traffic, passenger vehicle sales and households’ credit are exhibiting sustained growth. In the case of rural demand, tractor and fertiliser sales improved in June while two-wheeler sales moderated. High growth in agricultural credit and improving sales volume of major fast moving consumer goods (FMCG) companies suggest incipient recovery in rural demand, which will be reinforced by improving kharif prospects.

10. Investment activity gained further steam on the back of government capital expenditure7, rising business optimism and revival in private capex in certain key sectors.8 Continued increase in import and production of capital goods further reaffirms this trend. Construction activity also remained strong in Q1 as indicated by healthy growth in cement production and steel consumption. Capacity utilisation in the manufacturing sector at 76.3 per cent (and 74.1 per cent on seasonally adjusted basis) remained above the long-term average of 73.7 per cent.9 The total flow of resources to the commercial sector from banks and other sources taken together has increased by ₹7.5 lakh crore during the financial year 2023-24 so far (up to July 28) as compared with ₹5.7 lakh crore a year ago10. On the downside, merchandise exports and non-oil non-gold imports contracted further in June and the growth in services exports decelerated amidst slowing external demand.

11. Looking ahead, these underlying developments and the upcoming festival season are expected to provide support to private consumption and investment activity. The spillovers emanating from weak external demand and protracted geopolitical tensions, however, pose risks to the outlook. Taking all these factors into consideration, real GDP growth for 2023-24 is projected at 6.5 per cent with Q1 at 8.0 per cent; Q2 at 6.5 per cent; Q3 at 6.0 per cent; and Q4 at 5.7 per cent. Real GDP growth for Q1:2024-25 is projected at 6.6 per cent. The risks are evenly balanced.

Inflation

12. The moderation in headline inflation to 4.6 per cent in Q1 of 2023-24 was in line with the projections set out in the June MPC meeting. There was a pick-up in headline inflation to 4.8 per cent in June due to an upturn in food inflation. On the positive side, inflation excluding food and fuel (core inflation) has softened by more than 100 basis points from its recent peak in January 2023. The month of July has witnessed accentuation of food inflation, primarily on account of vegetables. The spike in tomato prices and further increase in prices of cereals and pulses have contributed to this. Consequently, a substantial increase in headline inflation would occur in the near-term.

13. Going by the past trends, vegetable prices may see a significant correction after a few months. The prospects of kharif crops have brightened, thanks to improvement in the progress of the monsoon. Uncertainties, however, remain on domestic food price outlook due to sudden weather events and possible El Niño conditions in August and beyond. Global food prices are also exhibiting a hardening bias on renewed geopolitical tensions. Crude oil prices have firmed up in recent weeks and its outlook is clouded by demand-supply uncertainties.

14. Assessment of the future trajectory of inflation is a continuous process. We have a choice to modify our inflation projections in every meeting of MPC, if warranted, in the interest of better guidance; or avoid frequent changes and revise them only on fewer occasions for simplicity of presentation. Given the continuing uncertainties, our latest CPI inflation projections for 2023-24, assuming a normal monsoon, is revised to 5.4 per cent, with Q2 at 6.2 per cent, Q3 at 5.7 per cent and Q4 at 5.2 per cent. CPI inflation for Q1:2024-25 is projected at 5.2 per cent. The risks are evenly balanced.

15. Headline inflation projection for Q2 of 2023-24 has been revised up substantially, primarily due to the price shock from vegetables. Given the likely short-term nature of these shocks, monetary policy can look through high inflation prints caused by such shocks for some time. The frequent incidences of recurring food price shocks, however, pose a risk to anchoring of inflation expectations, which has been underway since September 2022. The role of continued and timely supply side interventions assumes criticality in limiting the severity and duration of such shocks. In such circumstances, it is necessary to be watchful of the emerging trends and risks to price stability. We have to stand in readiness to go beyond keeping Arjuna’s eye to deploying policy instruments, if necessary. I reiterate what I said in my June policy statement: bringing headline inflation within the tolerance band is not enough; we need to remain firmly focused on aligning inflation to the target of 4.0 per cent.

Liquidity and Financial Market Conditions

16. The level of surplus liquidity in the system has gone up in the recent months on the back of return of ₹2000 banknotes to the banking system, RBI’s surplus transfer to the government, pick up in government spending and capital inflows. The overall daily absorption under the liquidity adjustment facility (LAF) was ₹1.7 lakh crore in June and ₹1.8 lakh crore in July 2023.

17. Despite such surplus liquidity, market response to RBI’s 14-day variable rate reverse repo (VRRR) auctions was lukewarm; instead, banks preferred to place their surplus liquidity in the less remunerative standing deposit facility (SDF). Although the fine-tuning VRRR auctions of 1-4 days maturity during this period evoked better response from the market11, this essentially reflects greater risk aversion among banks to park large funds under the main operation. In this context, it is necessary to reiterate that fine-tuning operations (overnight and up to 13 days) are undertaken to deal with special or exceptional situations and cannot become the rule.

18. In recent years, our stated stance on liquidity is to maintain adequate liquidity in the system to meet the productive requirements of the economy. Excessive liquidity, on the other hand, can pose risks to price stability and also to financial stability. Hence, efficient liquidity management requires continuous assessment of the level of surplus liquidity so that additional measures are taken as and when necessary to impound the element of excess liquidity. Accordingly, it has been decided that with effect from the fortnight beginning August 12, 2023, scheduled banks shall maintain an incremental cash reserve ratio (I-CRR) of 10 per cent on the increase in their net demand and time liabilities (NDTL) between May 19, 2023 and July 28, 2023. This measure is intended to absorb the surplus liquidity generated by various factors referred to earlier including the return of ₹2000 notes to the banking system. This is purely a temporary measure for managing the liquidity overhang. Even after this temporary impounding, there will be adequate liquidity in the system to meet the credit needs of the economy. The I-CRR will be reviewed on September 8, 2023 or earlier with a view to returning the impounded funds to the banking system ahead of the festival season. I must add that the existing cash reserve ratio (CRR) remains unchanged at 4.5 per cent.

Financial Stability

19. The Indian financial sector has been stable and resilient, as reflected in sustained growth in bank credit, low levels of non-performing assets and adequate capital and liquidity buffers.12 Macro stress tests for credit risk reveal that scheduled commercial banks (SCBs) would be able to comply with the minimum capital requirements even under severe stress scenarios. There is, however, no room for complacency because it is during tranquil and good times that vulnerabilities may creep in. Hence, buffers are best built up during these periods. A stable financial system is a prerequisite for price stability and sustained growth. This is a shared responsibility in which regulated entities like banks, NBFCs and others are important stakeholders. On its part, the Reserve Bank remains steadfast in its commitment to safeguard the financial system from the emerging and potential challenges. We expect the same from the regulated entities also.

External Sector

20. India’s current account deficit (CAD) was contained at 2.0 per cent of GDP in 2022-23 as compared with 1.2 per cent in 2021-22. Merchandise trade deficit has narrowed in Q1 of 2023-24 with contraction in imports exceeding contraction in exports. Services exports and remittances are, however, expected to provide cushion to the current account deficit. We, therefore, expect CAD to remain eminently manageable during the current financial year also.

21. On the financing side, foreign portfolio investment (FPI) flows have remained buoyant in 2023-24 so far. Net FPI inflows have been US$ 20.1 billion up to August 8, 2023 which is the highest since 2014-15. In the corresponding period of the previous year, there were net outflows of US$ 12.6 billion. The inflows under external commercial borrowings also witnessed a turnaround, with net inflows of US$ 6.0 billion during April-June 2023 as against net outflows of US$ 2.9 billion a year ago. Net foreign direct investment (FDI) flows to India, on the other hand, fell to US$ 5.5 billion during April-May 2023 from US$ 10.6 billion a year ago, reflecting a global slowdown in FDI flows. Latest available data suggest that India’s external debt to GDP ratio improved to 18.9 per cent at end-March 2023 from 20.0 per cent at end-March 2022.

22. The Indian rupee has remained stable since January 2023. Foreign exchange reserves have crossed US$ 600 billion mark. The umbrella has gathered further strength; and I am not saying this in the context of the monsoon rains!13

Additional Measures

23. I shall now announce certain additional measures.

Review of Regulatory Framework for Financial Benchmark Administrators

24. It has been decided to revise the extant regulations issued in June 2019 and put in place a comprehensive, risk-based framework for administration of financial benchmarks. This will cover all benchmarks related to foreign exchange, interest rates, money markets and government securities. The revised directions will provide greater assurance about the accuracy and integrity of financial benchmarks.

Review of Regulatory Framework for Infrastructure Debt Fund – NBFCs (IDF-NBFCs)

25. At present, Infrastructure Debt Funds (IDFs) provide refinancing facilities for lenders in the infrastructure sector. The extant regulatory framework for IDFs has been revised. The key changes in the revised framework are: (i) withdrawal of the requirement to have a sponsor for the IDFs; (ii) allowing IDFs to finance toll-operate-transfer (ToT) projects as direct lenders; (iii) permitting IDFs to raise funds through ECBs; and (iv) making tri-partite agreements optional for PPP projects. These changes are expected to further augment the capacity for infrastructure financing in the country.

Greater Transparency in Interest Rate Reset of Equated Monthly Instalments (EMI) based Floating Interest Loans

26. It is proposed to put in place a transparent framework for reset of interest rates on floating interest loans. The framework will require Regulated Entities to (i) clearly communicate with borrowers for resetting the tenor and/or EMI; (ii) provide options for switching to fixed rate loans or foreclosure of loans; (iii) disclose various charges incidental to the exercise of the options; and (iv) ensure proper communication of key information to borrowers. These measures will further strengthen consumer protection.

Consolidation and Harmonisation of Instructions for Supervisory Data Submission

27. The Reserve Bank has, from time to time, issued several guidelines on submission of supervisory returns by supervised entities. It has been decided to consolidate and harmonise such guidelines into a single Master Direction to reduce compliance burden and to promote greater ease of doing business for supervised entities.

Conversational Payments and Off-line Capability on UPI; Enhancement in Transaction Limit of Small Value Off-line Digital Payments

28. With the objective of harnessing new technologies for enhancing the digital payments experience for users, it is proposed to (i) enable “Conversational Payments” on UPI, which will enable users to engage in conversation with AI-powered systems to make payments; (ii) introduce offline payments on UPI using Near Field Communication (NFC) technology through ‘UPI-Lite’ on-device wallet; and (iii) enhance the transaction limit for small value digital payments in off-line mode from ₹200 to ₹500 within the overall limit of ₹2000 per payment instrument. These initiatives will further deepen the reach and use of digital payments in the country.

Public Tech Platform for Frictionless Credit

29. The Reserve Bank, in association with the Reserve Bank Innovation Hub (RBIH), started a pilot project in September 2022 for frictionless credit delivery through end-to-end digital processes, starting with Kisan Credit Card (KCC) loans. The pilot for KCC loans is currently operational in select districts of Madhya Pradesh, Tamil Nadu, Karnataka, UP and Maharashtra. Recently, dairy loans have been included in the pilot project in select districts of Gujarat. Based on the learnings from the pilots and to expand the scope of end-to-end digital lending processes, a Public Tech Platform for Frictionless Credit delivery is being developed by the RBIH. The Platform is intended to be rolled out as a pilot project in a calibrated manner. It will have an open architecture and open Application Programming Interface (API) and Standards, to which all financial sector players can connect seamlessly. This initiative will accelerate the penetration of credit to hitherto underserved regions and further deepen financial inclusion.

Conclusion

30. We have made good progress in sustaining India’s growth momentum. While inflation has moderated, the job is still not done. Inflationary risks persist amidst volatile international food and energy prices, lingering geopolitical tensions and weather-related uncertainties. In charting the course of monetary policy, we continuously assess the impact of our past actions, the evolving inflation dynamics and the implications of incoming data for the economic outlook. I reiterate our commitment to align CPI inflation to the 4 per cent target on a durable basis. We do look through idiosyncratic shocks, but if such idiosyncrasies show signs of persistence, we have to act. As we prepare to celebrate the Independence Day, the air is filled with hope and promise. Let me end by recalling the prophetic words of Mahatma Gandhi “…I have no doubt that our country would rise to the greatest height among the nations of the world.”14

Thank you. Namaskar.

(Yogesh Dayal)

Chief General Manager

Press Release: 2023-2024/725

1 In terms of GDP at market exchange rate.

2 During the accommodative phase of monetary policy, i.e., February 2019 to March 2022, the weighted average domestic term deposit rate (WADTDR) on fresh deposits of scheduled commercial banks and the weighted average lending rate (WALR) on fresh loans had fallen by 259 basis points and 232 basis points, respectively, in response to the repo rate cut of 250 basis points. In the recent tightening phase, i.e., May 2022 to June 2023, the repo rate has increased by 250 basis points, fully offsetting the reduction in the easing phase. However, the increase in the WADTDR on fresh deposits and the WALR on fresh loans at 231 basis points and 169 basis points, respectively, trails the reduction seen in these rates during the accommodative phase.

3 According to the IMF, annual average global growth rate during 2000 to 2019 was 3.8 per cent.

4 The total area sown under kharif crops was 0.4 per cent higher than a year ago as on August 4, 2023. Cumulative rainfall during south-west monsoon was the same as the long period average up to August 9, 2023. The storage in major reservoirs on August 3 was at 56 per cent of the full capacity, higher than the decadal average of 50 per cent, but below 60 per cent a year ago.

5 The index of industrial production (IIP) expanded by 5.2 per cent in May while core infrastructure output rose by 8.2 per cent in June. The purchasing managers’ index (PMI) for manufacturing was 57.7 in July.

6 PMI services rose to 62.3 in July from 58.5 in June led by robust demand and new business gains, signaling the sharpest expansion in output since June 2010.

7 The capital expenditure by the Central government increased by 59.1 per cent (y-o-y) during Q1:2023-24. Information available for 20 states indicates that their capital expenditure jumped by 74.4 per cent (y-o-y) during Q1:2023-24 as compared with a contraction of 8.7 per cent a year ago.

8 Metals, petroleum, automobile, chemicals, iron and steel, cement and food and beverages.

9 76.3 per cent pertains to Q4:2022-23; long term average pertains to Q1:2008-09 to Q4:2022-23 excluding Q1:2020-21.

10 Data on flow of resources exclude the impact of the merger of a non-bank with a bank.

11 The average bid-cover ratio of five14-day VRRR auctions was 38.4 per cent and that of 11 fine-tuning VRRR auctions of 1-4 days maturity was 46.2 per cent.

12 The capital to risk-weighted assets ratio (CRAR) and the common equity tier 1 (CET1) capital ratio of SCBs were at historical highs of 17.1 per cent and 13.9 per cent, respectively, in March 2023. SCBs’ gross non-performing assets (GNPA) ratio continued downtrend and fell to a 10-year low of 3.9 per cent in March 2023, while the net non-performing assets (NNPA) ratio declined to 1.0 per cent.

13 The forex reserves are accumulated by RBI when the capital inflows are strong. Similarly, when forex outflows cause excessive volatility in the exchange rate of Indian Rupee, the RBI supplies US dollars to the market to curb volatility and to ensure that there is adequate forex liquidity. Thus, forex reserves are like an umbrella to use during rainy days (Please see: “Banking Beyond Tomorrow”; RBI Governor’s speech at the Bank of Baroda’s Annual Banking Conference, July 2022).

14 The Collected Works of Mahatma Gandhi, Volume 95; April 30-July 6, 1947.