Standard Operating Procedure (SOP) issued in case of non filling of GST returns

Vide Circular No. 129/48/2019 – GST on 24th December 2019, CBIC has issued Standard operating procedure to be followed in case of non-furnishing of GST return is being issued.

In the 38th GST council meet, one of the recommendation was to set a SOP for tax officers in respect of action to be taken in cases of non-filing of FORM GSTR-3B returns.

A standard operating procedure is a set of step-by-step instructions compiled by an organization to help workers carry out complex routine operations. In context of procedure to be followed by tax officers (i.e. action to be exercised) in case of non-furnishing of return under section 39 or section 44 (annual returns) or section 45 (final returns) of the Central Goods and Services Tax Act, 2017, a set of standard operating procedure is being issued via Circular No. 129/48/2019 – GST. The need arose to bring uniformity in the existing divergent practices being followed in case of non-furnishing of the said returns.

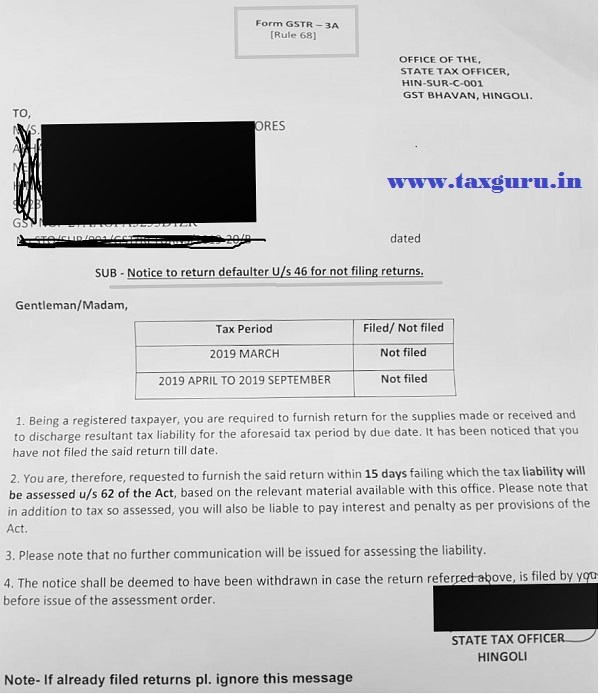

Section 46 of the CGST Act r.w. rule 68 of the CGST Rules, 2017 requires issuance of a notice in FORM GSTR-3A to a registered person who fails to furnish return under section 39 or section 44 or section 45 requiring him to furnish such return within 15 days. Further section 62 provides for assessment of non-filers of return of registered persons who fails to furnish return under section 39 or section 45 even after service of notice under section 46.

FORM GSTR-3A provides as under:

As such, no separate notice is required to be issued for best judgment assessment under section 62 and in case of failure to file return within 15 days of issuance of FORM GSTR3A, the best judgment assessment in FORM ASMT-13 can be issued without any further communication.

Following is the step by step procedure explaining the set procedure issued to be followed in event of non-filling of GST returns by tax payers.

Step 1: Preferably, a system generated message would be sent to all the registered persons 3 days before the due date to nudge them about filing of the return for the tax period by the due date.

Step 2: Once the due date for furnishing the return under section 39 is over, a system generated mail or message would be sent to all the defaulters regarding non filling.

It is to be sent to the authorized signatory as well as the proprietor/partner/director/Karta, etc.

Note: Being proactive and handling hundreds of returns and non-filling chaos a last moment can only be possible by providing a facility to taxpayer to view real time update of their status of return.

Step 3: Five days after the due date of furnishing the return, a notice in FORM GSTR-3A shall be issued electronically to defaulters, requiring them to furnish such return within fifteen days.

Step 4: In case the return is not furnished within 15 days of said period, proper officer may proceed to assess the tax liability of the said person u/s 62 of the CGST Act, to the best of his judgement taking into account all the relevant material which is available or which he has gathered and would issue order under rule 100 of the CGST Rules in FORM GST ASMT-13.

The proper officer would then be required to upload the summary thereof in FORM GST DRC07.

Step 5: For the purpose of assessment of tax liability under section 62 of the CGST Act, the proper officer may take into account

- details of outward supplies available in the statement furnished under section 37 (FORM GSTR-1)

- details of supplies auto populated in FORM GSTR-2A

- information available from e-way bills

- any other information available from any other source including from inspection under section 71.

Step 6: In case the defaulter furnishes a valid return within thirty days of the service of assessment order in FORM GST ASMT-13, the said assessment order shall be deemed to have been withdrawn. But, the liability for payment of interest u/s 50 or for payment of late fee u/s 47 shall continue.

However, if the said return remains unfurnished, then proper officer may initiate proceedings under section 78 and recovery under section 79 of the CGST Act.

In deserving cases, based on the facts of the case, the Commissioner may resort to provisional attachment to protect revenue u/s 83 of the CGST Act before issuance of FORM GST ASMT-13.

Further, the proper officer would initiate action under section 29(2) of the CGST Act for cancellation of registration in cases where the return has not been furnished for the period specified in section 29.

General Problems and solutions:

First problem is that second reminders are to be sent to taxpayer by the consultants in case data is not received by last days.

Solution to this is already provide in first step as this burden shall be reduced by department it self.

Second Problem here arises as we have all seen that although returns are sometimes filled, still system generated messages are sent to taxpayers. That should be taken care to be avoided by department.

Solution: As to check return filling status, there exists no need to login to account to taxpayers, so by the help of automated tools or applications, both consultants and taxpayers can be proactive by generating timely reports.

Third problem may arise in consultant’s offices where taxpayers are generally relaxed. Earlier, constant too was relaxed as they had till last date to furnish return, now these earlier reminders will unnecessary clog up the situation in already tensed last moment.

Solution: Here as per my opinion consultants should just advice clients to forward message received to a particular number and then dump all messages to a messaging group. This will create record at one place and then follow can be done easily.

To be seem as a burden initially, but these early reminders can be actually beneficial as taxpayers will now start to submit data to consultants now much earlier as expected before.

Author Bio

Very well explained