DECLARATION AND PAYMENT OF DIVIDEND

SECTION 123 TO 127 OF COMPANIES ACT, 2013 READ WITH THE COMPANIES (DECLARATION AND PAYMENT OF DIVIDEND) RULES, 2014

DIVIDEND- SECTION 2(35)

“Dividend” includes any interim dividend;

Where in simple words, dividend can be defined as the sum of money paid by a company, to its shareholders, out of the profits made by a company, if so authorised by its articles, in proportion to the amount paid- up on each share held by them. (Section 51)

Under the Companies Act, 2013 (hereinafter referred to as “CA ACT 2013”), Section 123 to 127 of Chapter VIII deals with the provisions related to the declaration and payment of dividend.

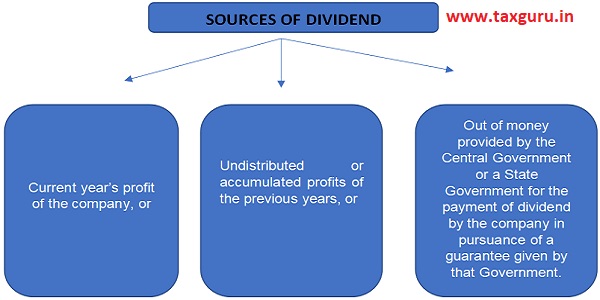

DECLARATION OF DIVIDEND: SECTION 123

(Note: No company shall declare dividend unless carried over previous losses and depreciation not provided in previous year or years are set off against profit of the company for the current year.)

(Note: In case of, Inadequacy of Profits resulting declaration of dividend out of previous year undistributed profits: –

Where, owing to inadequacy or absence of profits in any financial year, any company proposes to declare dividend out of the accumulated profits earned by it in previous years and transferred by the company to the reserves, such declaration of dividend shall not be made except in accordance with Rule 3 of Companies (Declaration and Payment of Dividend) Rules, 2014.)

RULE 3 OF COMPANIES (DECLARATION AND PAYMENT OF DIVIDEND) RULES, 2014: DECLARATION OF DIVIDEND OUT OF RESERVES DECLARATION OF DIVIDEND OUT OF RESERVES

In the event of inadequacy or absence of profits in any year, a company may declare dividend out of free reserves subject to the fulfillment of the following conditions, namely:

(1) The rate of dividend declared shall not exceed the average of the rates at which dividend was declared by it in the three years immediately preceding that year:

Provided that this sub-rule shall not apply to a company, which has not declared any dividend in each of the three preceding financial year.

(2) The total amount to be drawn from such accumulated profits shall not exceed one-tenth of the sum of its paid-up share capital and free reserves as appearing in the latest audited financial statement.

(3) The amount so drawn shall first be utilised to set off the losses incurred in the financial year in which dividend is declared before any dividend in respect of equity shares is declared.

(4) The balance of reserves after such withdrawal shall not fall below fifteen per cent of

The amount of the dividend, including interim dividend, shall be deposited in a scheduled bank in a separate account within five days from the date of declaration of such dividend

PAYMENT OF DIVIDEND

No dividend shall be payable except by way of cash, where dividend payable in cash can also be paid through cheque, warrant or in any electronic mode, to the shareholder who is entitled to the dividend.

Condition: – A company who has committed any default in compliance with the provisions of section 73 and 74 relating to the acceptance and repayment of deposits would be barred to declare dividend.

INTERIM DIVIDEND- SECTION 123(3)

Board of directors of a company may declare interim dividend during any financial year or at any time during the period from closure of financial year till holding of the annual general meeting, out of the profits made by the company during such financial year or out of previous year undistributed profits (subject to Companies (Declaration and Payment of Dividend) Rules, 2014).

In case the company has incurred loss during the current financial year up to the end of the quarter immediately preceding the date of declaration of interim dividend, such interim dividend shall not be declared at a rate higher than the average dividends declared by the company during the immediately preceding three financial years.]

Note: As per Section- 2(35) “dividend includes interim dividend” signifies that the provisions of Companies Act 2013, applicable to the final dividend to the extent possible, shall also applicable on interim dividend.

PROCEDURE OF DECLARATION AND PAYMENT OF DIVIDEND

Issue atleast 7 clear days notice of the meeting of Board of directors. (In case of listed companies, notify stock exchange(s) where the securities of the company are listed, at least 2 working days in advance of the date of the meeting as per regulation 29 of SEBI (LODR) Regulations, 2015)

⇓

Hold Board meeting and pass resolution for recommending the final amount of dividend.

*Listed companies are required to give atleast 7 days notice of Book closure to stock exchange as per regulation 42 of SEBI(LODR) Regulations 2015.

⇓

Close the register of members and the share transfer register of the company

⇓

Hold a Board/committee meeting for approving registration of transfer/ transmission of the shares of the company, which have been lodged with the company prior to the commencement of book closure.

*The listed entity shall declare recommend or declare all dividend atleast 5 working days before the record date fixed for the purpose.

⇓

Hold the annual general meeting and pass an ordinary resolution declaring the payment of dividend to the shareholders of the company as per recommendation of the Board.

*In case of Interim dividend, it is not mandatory to take approval of shareholders for declaration of Dividend, the Board may declare it in the Board meeting-section 123(3)).

⇓

Prepare a statement of dividend in respect of each shareholder and it must be ensured that the dividend tax is paid to the tax authorities within the prescribed time.

⇓

Separate Bank Account is required to be opened and amount of dividend payable shall be credited to the said account within 5 days of declaration.

* If the company is listed, then for payment of dividend it has to mandatorily use, either directly or through its Registrars to an Issue and Share Transfer Agents (RTI & STA), any Reserve Bank of India approved electronic mode of payment such as Electronic Clearing Services (ECS), National Electronic Fund Transfer (NEFT), etc.

*Provided that where it is not possible to use electronic mode of payment, ‘payable-at-par’ warrants or cheques may be issued but where the amount payable as dividend exceeds one thousand and five hundred rupees, the ‘payable-at-par’ warrants or cheques shall be sent by speed post (Regulation 12 of SEBI(LODR) Regulations 2015).

⇓

Make arrangements with the bank and in collaboration with other banks if required, for payment of the Dividend Warrants at par.

⇓

Dispatch dividend warrants within thirty days of the declaration of dividend. In case of joint shareholders, dispatch the dividend warrant to the first named shareholder.

⇓

In case dividend remaining unpaid or unclaimed, Company is required to arrange for transfer of unpaid or unclaimed dividend to a special account named “Unpaid dividend Account” within 7 days after expiry of the period of 30 days of declaration of final dividend. (Section 124).

⇓

Transfer unpaid dividend amount to Investor Education and Protection Fund (IEPF) after the expiry of seven years from the date of transfer to unpaid dividend A/c.

EXAMPLE 1: ABC Private Limited, a domestic company declared an interim dividend of Rs. 15,00,000 in its Board meeting held on 19.03.2020 to be paid to the shareholders of the company. what are the applicable provisions as per the companies Act and Income tax Act?

AS PER COMPANIES ACT, 2013

- The company is required to deposit the amount of dividend so declared within 5 days from the date of declaration of Dividend i.e. 19.03.2020 (up to 23.03.2020)

- Further, the company is required to make the payment within 30 days of declaration of dividend (up to 17.04.2020), failing which company will be liable to pay interest @18% p.a. for the period of default. Moreover, it is required to deposit the unpaid dividend amount in the special account within 7 days from expiry of 30 days (i.e. 23.04.2020).

AS PER INCOME TAX ACT, 1961

- The company is liable to pay tax on dividend, known as Dividend Distribution Tax (DDT) or Corporate Dividend Tax (CDT) at an effective rate of 20.555% (Basis rate 15% including surcharge (12%) and cess (4%)) (Refer Section 115O of the Income tax Act)

In this Case, DDT to be paid by the company is:

15,00,000*20.555%= 3,08,325

*Note: The amount of dividend of Rs 5,00,000 (in excess of Rs 10 lakh) is taxable in the hands of shareholder at a rate of 10% (section 115BBDA). (This provision is not applicable in case shareholder is a company or religious or charitable trust)

- The amount of DDT as calculated above shall be deposited with the Central Government within 14 days from the date of:

(a) declaration of any dividend; or

(b) distribution of any dividend; or

(c) payment of any dividend,

whichever is earliest.

In this case, it must be paid maximum by 01.04.2020, failing which company will be liable to pay by way of interest at the rate of 1% of the DDT from the date following the date on which such DDT was payable till the time such DDT is actually paid to the government.

(*Note: Dividend amount of Rs 10,00,000 is fully exempt in the hands of shareholder. Provided, if the dividend amount exceeds Rs 10 lakh, then the amount in excess of Rs 10 Lakh shall be taxable in the hands of shareholder at a special rate of 10% (Refer Section 115BBDA)

EXAMPLE 2: ABC Private limited, a domestic company declared a final dividend of Rs. 10,00,000 in its Annual general meeting held on 30.09.2020 to be paid to the shareholders of the company. what are the applicable provisions as per the companies Act and Income tax Act?

AS PER COMPANIES ACT, 2013

- The company is required to deposit the amount of dividend so declared within 5 days from the date of declaration of Dividend i.e. 30.09.2020 (up to 04.10.2020)

- Further, the company is required to make the payment within 30 days of declaration of dividend (up to 29.10.2020), failing which company will be liable to pay interest @18% p.a. for the period of default. Moreover, it is required to deposit the unpaid dividend amount in the special account within 7 days from expiry of 30 days (i.e. 29.10.2020).

AS PER INCOME TAX ACT, 1961

- The company is liable to pay tax on dividend, known as Dividend Distribution Tax (DDT) or Corporate Dividend Tax (CDT) at an effective rate of 20.555% (Basis rate 15% including surcharge (12%) and cess (4%)) (Refer Section 115O)

In this Case, DDT to be paid by the company is:

10,00,000*20.555%= 2,05,550

- The amount of DDT as calculated above shall be deposited with the Central Government within 14 days from the date of:

(a) declaration of any dividend; or

(b) distribution of any dividend; or

(c) payment of any dividend,

whichever is earliest.

In this case, it must be paid maximum by 13.10.2020, failing which company will be liable to pay by way of interest at the rate of 1% of the DDT from the date following the date on which such DDT was payable till the time such DDT is actually paid to the government.

NOTE:

- Taking into consideration Example 1 and 2, for the F.Y 2019-2020, the company has declared the total dividend of Rs. 25,00,000 and DDT paid on the same is Rs. 5,13,875.

- Provisions applicable to Final dividend is also applicable on Interim Dividend to the extent possible.

UNPAID DIVIDEND ACCOUNT: SECTION 124

In case, Where a dividend has been declared by a company but has not been paid or claimed within 30 days from the date of declaration

⇓

Within 7 days from the date of expiry of 30 days, the company shall transfer the amount to Unpaid Dividend Account

⇓

Within 90 days of making such transfer, a statement (containing the names, address and amount of unpaid dividend) is required to be prepared and to be placed on the website of the company, if any and any other website as approved by CG.

In case of default in transferring the amount to unpaid dividend account company shall be liable to pay interest @ 12% p.a. from the date of such default.

⇓

Amount lying in unpaid dividend account remains unpaid or unclaimed for Seven consecutive years or more shall be transferred to Investor Education and Protection Fund (herein referred to as the Fund) and a statement (Form No. IEPF 1) to be sent to the administrative authority.

⇓

All shares in respect of which dividend has not been paid or claimed for seven consecutive years or more shall be transferred by the company in the name of Fund along with a statement (Form No. IEPF-4) containing such details as prescribed in the rules.

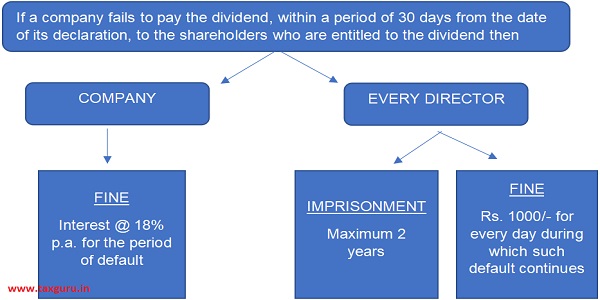

Note: If a company fails to comply with any of the requirements of this section, the company shall be punishable with fine which shall not be less than five lakh rupees but which may extend to twenty-five lakh rupees and every officer of the company who is in default shall be punishable with fine which shall not be less than one lakh rupees but which may extend to five lakh rupees.

PUNISHMENT FOR FAILURE TO DISTRIBUTE DIVIDENDS: SECTION 127

EXCEPTIONS- In the following cases, no offence shall be deemed to have been committed

(a) where the dividend could not be paid by reason of the operation of any law;

(b) where a shareholder has given directions to the company regarding the payment of the dividend and those directions cannot be complied with and the same has been communicated to him;

(c) where there is a dispute regarding the right to receive the dividend;

(d) where the dividend has been lawfully adjusted by the company against any sum due to it from the shareholder; or

(e) where, for any other reason, the failure to pay the dividend or to post the warrant within the period under this section was not due to any default on the part of the company

AUTHOR OF THIS ARTICLE IS CS YOGESH GUPTA & CAN BE REACHED AT YOGESH.GUPTA@IURISCONSULTANTS.IN OR 7742681270

Author Bio

Hi Sir

I have a query with regard to trf of Dividend to Dividend a/c. As per law trf of dividend to dividend a/c has to be done within 5 days from date of declaration. If Dividend is declared on 12 August 2022 and it’s a Bank Holiday for next 4 days (i.e. 13 to 16 are holidays on a/c Saturday/Sunday/Independence Day & Parsi New year). Can it be trf on 17th Aug 2022?