The SEBI (PIT) Regulation provided for the restriction regarding the communication of the of Unpublished price sensitive information, so that no one can take undue advantage of such information to trade in securities to earn unmerited profit. Further, the regulation bars the insiders to trade in the securities of the company, as they may possess UPSI while trading in the securities however, the regulations does not provide for absolute restrictions and hence, some exemptions/ situations have been provided where the restrictions are not applicable.

Terms such as insider, connected persons, UPSI have been discussed in SEBI (Prohibition of Insider Trading) Regulation, 2015

In order to comply with the PIT Regulations and to ensure compliance of the policies prepared under the regulations, the company needs to appoint a “Compliance officer”.

The term compliance officer has been defined in the Regulations as:

> Any senior officer, so designated and reporting to the board or the head of the organization, as the case may be.

> Who is Financially literate, and

> Is capable of understanding the regulatory and legal compliance as per the regulations, and

> Who shall, under the supervision of the board or head of the organization, be responsible for:

- compliance of policies and procedures

- Maintenance of records

- Monitoring adherence to the rules for preservation of UPSI

- Monitoring of trades

- Implementation of the rules as per the code.

Regulation 3: Restriction on communication and procurement of UPSI

(1) An insider is explicitly restricted from communicating or allowing the access to any UPSI, that relates to:

> a company, or

> securities listed, or

> Securities proposed to be listed.

However, the insider may communicate such information while performing his duties of discharging his legal obligations or in furtherance of legitimate purpose.

NOTE: This provision is intended to cast an obligation on all insiders who are essentially persons in possession of unpublished price sensitive information to handle such information with care and to deal with the information with them when transacting their business strictly on a need-to-know basis. It is also intended to lead to organisations developing practices based on need-to-know principles for treatment of information in their possession.

(2) Further, the regulation 3(2) bars every person to procure or cause the communication by an insider of UPSI, that relates to:

> a company, or

> securities listed, or

> Securities proposed to be listed.

However, a person may procure or cause the communication of such information while performing his duties of discharging his legal obligations or in furtherance of legitimate purpose.

Legitimate purpose: The BOD of a listed company shall make policy for determination of the legitimate purpose and it shall form part of the “Code of fair disclosure and conduct” formulated under Regulation 8. Further, any person who receives the UPSI pursuant to a legitimate purpose, shall be considered as insider for such UPSI and a notice, to maintain confidentiality, shall be given to such person.

Some illustrations of legitimate purpose as provided in the code: Sharing of unpublished price sensitive information in the ordinary course of business by an insider with partners, collaborators, lenders, customers, suppliers, merchant bankers, legal advisors, auditors, insolvency professionals or other advisors or consultants, provided that such sharing has not been carried out to evade or circumvent the prohibitions of these regulations.

(3) Exception to Regulation 3

Notwithstanding anything contained in this regulation, an unpublished price sensitive information may be communicated, provided, allowed access to or procured, in connection with a transaction that would:–

i. Entail an obligation to make an open offer under the takeover regulations and the board of directors of the listed company is of informed opinion that sharing of such information is in the best interests of the company;

Therefore, the UPSI can be shared only with the consent/ decision of such BOD of the listed entity.

Legislative Note: Any/ all information disclosed to the person making the open offer, shall also be disclosed to the public in the letter of offer, so that the public shareholders can take decision regarding the disinvestment or retention in the securities.

ii. Not attract the obligation to make an open offer under the takeover regulations but where the board of directors of the listed company is of informed opinion that sharing of such information is in the best interests of the company.

But, such communicated information that includes unpublished price sensitive information shall be made generally available at least two trading days prior to the proposed transaction being effected in such form as the board of directors may determine to be adequate and fair to cover all relevant and material facts.

The reason for making the information generally available, at least 2 Trading days prior to the proposed transaction is to rule out any information asymmetry in the market.

(4) The BOD shall require the parties, to whom the UPSI has been disclosed, to execute Confidentiality contracts and Non- disclosure agreements and such party shall keep the information so received as confidential. Further, such party shall not trade in the securities while in possession of UPSI, except as per regulation 3(3).

(5) The board of directors shall ensure that a structured digital database is maintained containing the names of such persons or entities, with whom information is shared under this regulation along with the Permanent Account Number or any other identifier authorized by law where Permanent Account Number is not available.

Such databases shall be maintained with adequate internal controls and checks such as time stamping and audit trails to ensure non-tampering of the database.

Regulation 4: Trading when in possession of UPSI

(1) The sub regulation 1 states that no insider shall trade in the securities of a listed company or a company proposed to be listed, when in possession of UPSI.

Since, the term insider includes any person who is in possession of UPSI therefore, the regulation restricts every person who is in possession of UPSI.

Exceptions: A person may, in the understated situation, trade while in possession of UPSI, without violating the Regulations:

> The transaction is an off-market inter-se transfer between the insiders, where such insiders are in possession of the same UPSI and such possession has been made without the breach of Regulation 3 also, the parties are required to make a conscious and informed trade decision.

Provided that the UPSI has not been provided under Regulation 3(3).

Provided further, that such Off-market trade shall be reported by the insiders to the company within 2 working days of making such transaction and the company shall notify the stock exchange within 2 trading day of receipt of such information.

> The transaction was carried out through the block deal window mechanism between persons who were in possession of the unpublished price sensitive information without being in breach of regulation 3 and both parties had made a conscious and informed trade decision;

*Block Deal Window mechanism is a separate window is provided by the Exchange for executing block deals i.e. trades having value greater than or equal Rs. 10 crores, executed through Block deal window.

Block deal windows shall be available on all trading days in Equity segment. Timings:

Morning Block Deal Window: 8:45 am to 9:00 am.

Afternoon Block Deal Window: 2:05 pm to 2:20pm.

> Transaction was carried out pursuant to a statutory or regulatory obligation to carry out a bona fide transaction.

> Transaction was undertaken pursuant to the exercise of stock options in respect of which the exercise price was pre-determined in compliance with applicable regulations.

> Trades were pursuant to a trading plan set up in accordance with regulation 5.

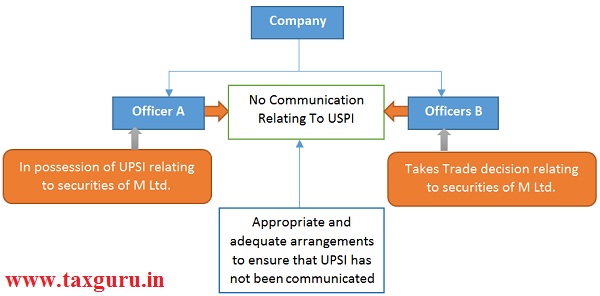

> In case of non-individual insiders:

- the individuals who were in possession of such UPSI were different from the individuals taking trading decisions and such decision-making individuals were not in possession of such UPSI when they took the decision to trade; and

- appropriate and adequate arrangements were in place to ensure that these regulations are not violated and no unpublished price sensitive information was communicated between such individuals

(2) In the case of connected persons the onus of establishing, that they were not in possession of unpublished price sensitive information, shall be on such connected persons and in other cases, the onus would be on the Board.

Refer my next article for discussion on trading plans, pre clearance trades, block deal window mechanism, etc.

For any clarification please reach out to me on vishalhirawat@yahoo.com