It is a fact that in the rapidly changing business world, every company, while pursuing its activities has to comply with numerous rules and regulations under Companies Act, SEBI, FEMA, and multiple other Laws. Thus, under section 204 of the companies act, 13, the mechanism of secretarial audit has been included to examine the compliance of an organization to various Laws, rules, regulations, notifications, circulars etc.

Page Contents

What is secretarial audit?

In the legal terms audit is defined as an independent and systematic examination of books of account, statutory records, documents and vouchers of an organization to ascertain that the financial and non-financial, records and disclosure present a true and fair view of the organization.

Comparably, Secretarial audit is an independent and strategic examination of the non-financial records to ensure that the legal and procedural requirements are duly complied with.

Secretarial audit is an effective tool for corporate compliance management which helps to detect non-compliance and to take corrective measures.

Applicability of Secretarial audit

In accordance with section 204 of the Companies Act, 2013 read with Rule 9 of Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014 and companies (Appointment and Remuneration of Managerial Personnel) Amendment Rules, 2020, following companies are required to obtain ‘Secretarial Audit Report’ from independent practicing company secretary in FORM- MR-3

“Explanation :- For the purposes of this sub-rule, it is hereby clarified that the paid up share capital, turnover, or outstanding loans or borrowings as the case may be, existing on the last date of latest audited financial statement shall be taken into account.”

Vide the Companies (Appointment and Remuneration of Managerial Personnel) Amendment Rules, 2020, the following clause was inserted to widen the scope of section 204 of companies Act, 13:

⇒ Every company having outstanding loans or borrowings from banks or public financial institutions of rupees one hundred crore or more.

The above clause has been made effective from 01 /04/2020.

Therefore, even the private companies, meeting the criteria of outstanding loans and borrowings of Rs. 100 cr. or more will be required to annex secretarial audit report with the board report.

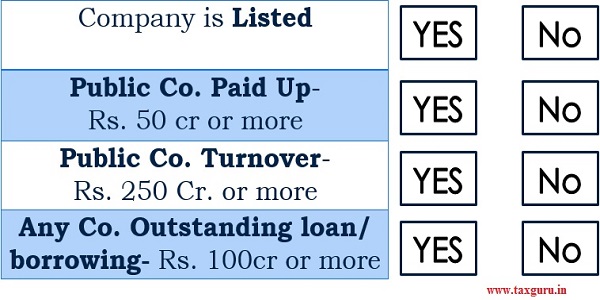

Ascertainment as to whether the Secretarial Audit is applicable on a particular company or not has to be made by checking below mentioned parameters: If answer to any of the above criteria is YES then the company is required to obtain secretarial audit report.

If answer to any of the above criteria is YES then the company is required to obtain secretarial audit report.

Note:

i. Deemed Public Company: A private company which is a subsidiary of a public company is called deemed public company and the provisions of section 204 will be applicable on such public company.

ii. Turnover: means the gross amount of revenue recognised in the profit and loss account from the sale, supply, or distribution of goods or on account of services rendered, or both, by a company during a financial year.

iii. The thresholds specified in section 204 shall be required to be checked throughout the year.

Hence, the secretarial audit report shall be required to be annexed with the Board report, if any time during the year (in respect of which board report is prepared):

(i) Any security of the company has remained listed on any recognised stock exchange; or

(ii) Public company had turnover of Rs. 250 crores or more or had paid up share capital of Rs. 50 crores or more.

(iii) Company had outstanding loans and borrowings of Rs. 100 crore or more

Benefits of secretarial audit

The trends of operating a business are changing swiftly and with that new rules, regulations, etc. are being enacted regularly. Hence, there exists a significant possibility of non-compliance, which may result into severe penalties and will increase the reputational and compliance risks.

Secretarial audit plays a crucial role to reduce the risk of non-compliance by independent examination of the non-financial records to ensure that the legal and procedural requirements are duly complied with. Thereby, secretarial audit will reduce the compliance, legal and reputational risk faced by an organization and will also save legal costs. The process of secretarial audit would act as a tool for good governance, if independence and diligence of the examiner (PCS) is maintained.

Apart from the organization itself, the secretarial audit provides benefits to other stakeholders as well, like:

Promoters: Gives them assurance that the management is complying with the applicable laws and the owners are not exposed to unintended risks.

Regulators: Reduces their burden of ensuring compliance, helps to prevent scams and frauds which can cause huge loss.

Investors: Informs them about the compliance practice of the organization and assists them in taking informed decisions

Independent/ Non-Executive Directors: comforts them that appropriate mechanisms are in place to ensure compliance.

Other Stakeholders: like Financial Institutions, Banks, Creditors and Consumers can measure the law abiding nature of company’s management and thus take a right decision with respect to their involvement with the company business

APPOINTMENT OF SECRETARIAL AUDITOR

As per Rule 8 of the Companies (Meetings of Board and its powers) Rules, 2014, Secretarial Auditor is required to be appointed by means of resolution passed at a duly convened Board meeting

The resolution for appointment shall be filed with Registrar of Companies within 30 days in MGT-14.

It is advisable to appoint Secretarial Auditor at beginning of the financial year as secretarial audit requires checking of compliances on a continuous basis.

As a good practice, the Secretarial Auditor should submit a report to the Board at the end of each quarter as to the compliances of the company

Scope of Secretarial audit

The Secretarial auditor needs to examine and report the compliance of the following:

- The Companies Act, 2013 and the rules made thereunder;

- The Securities Contracts (Regulation) Act, 1956 (‘SCRA’) and the rules made thereunder;

- The Depositories Act, 1996 and the Regulations and Bye-laws framed thereunder;

- Foreign Exchange Management Act, 1999 and the rules and regulations made thereunder to the extent of Foreign Direct Investment, Overseas Direct Investment and External Commercial Borrowings;

- Regulations and Guidelines prescribed under the Securities and Exchange Board of India Act, 1992

- Other laws as applicable on the company.

Secretarial Audit Report also requires reporting on whether-

Reporting of Fraud

Reporting of Fraud

Secretarial Auditor needs to report the fraud if in the course of performance of his duties as auditor has reason to believe that an offence involving fraud is being committed or has been committed against the Company by its officers/employees. (in accordance with section 143(12 & 14))

Compliance Reports

Ceiling on number of Annual Secretarial compliance report

Recently, the ICIS Council has issued a clarification with regard to ceiling on number of Reports to be issued by PCS.

Accordingly, ceiling on number of Annual Secretarial Compliance Reports to be issued by PCS is 5 reports individually/ per partner in each financial year w.e.f. April 1, 2020 and an additional limit of 5 Secretarial Compliance Reports individually/ per partner in case the Unit has been Peer Reviewed.

Further, in view of the foregoing, the said clarification has also provided for the following:

(a) Secretarial Audit/ Annual Secretarial Compliance Report of the following companies shall be undertaken only by peer reviewed PCS:

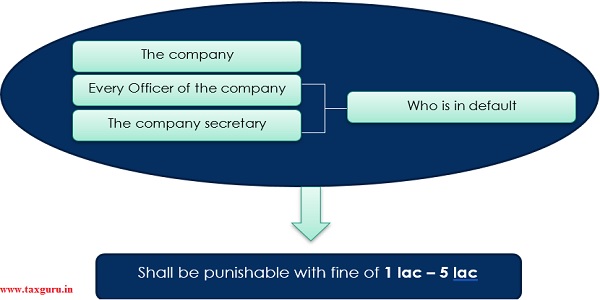

Penalty

Penalty

If a company or any officer of the company or the company secretary in practice, contravenes the provisions of section 204, then,