Introduction: On the 25th of October, 2023, the Chamber of Tax Consultants sent a formal representation to Smt. Nirmala Sitharaman, the Hon’ble Finance Minister of India, and Shri Nitin Gupta, Chairman of the Central Board of Direct Taxes. The representation pertains to a pressing matter concerning the relaxation of specific requirements in new Forms 10B and 10BB, and an extension of the due date for filing these forms. This article delves into the details of the representation and the underlying issues.

Detailed Analysis: The Chamber of Tax Consultants, founded in 1926, is an esteemed non-profit organization representing tax practitioners across India, including Advocates, Chartered Accountants, and Tax Practitioners. They have a history of advocating for crucial issues within the tax landscape and have previously addressed various government authorities.

In their earlier representation dated 11th September, 2023, they successfully urged for an extension of due dates for filing Form 10B, Form 10BB, and ITR-7. These extensions were granted, providing relief to taxpayers.

The Central Board of Direct Taxes further alleviated the situation by issuing Circular No. 17 dated 9th October, 2023, which relaxed certain requirements in Form 10B and Form 10BB, a decision greatly appreciated by the Chamber of Tax Consultants.

However, the representation doesn’t end here. The Chamber now seeks additional concessions, primarily due to the extensive details required in the new Forms 10B and 10BB, which are causing difficulties for auditors and charitable trusts. The issues include:

1. Extensive project details (Clause 15)

2. Comprehensive information on tax-deducted receipts (Clause 19)

3. Detailed data on donations (Clause 23)

4. Application of income specifics (Clause 31)

5. Income taxable under Section 115BBI (Clause 33)

6. Application of income from different sources (Clause 37)

7. Details of transactions referred to in Sec. 13(2) (Clause 42)

8. Details of specified violations (Clause 43)

9. Details about contravention of tax provisions (Clauses 46 to 49)

These requirements are cumbersome and impractical for many charitable trusts and institutions, as the necessary data is often not readily available.

Moreover, the Chamber of Tax Consultants highlights that the utility provided by the department is currently under revision, causing delays in finalizing reports. This software update impacts both auditors and taxpayers, further underscoring the need for an extension.

Therefore, the Chamber respectfully requests an additional month’s extension for filing Form 10B, Form 10BB, and ITR-7. The proposed due dates for compliance are as follows:

- Form 10B and Form 10BB: 30th November 2023

- Filing ITR 7: 31st December 2023

Another request involves relaxation in the disclosure of details about relatives of trustees, seniors, founders, and concerns in which they have substantial interest. While Circular No. 17 already relaxes requirements for donors’ relatives, the Chamber suggests extending this concession to relatives of settlors, trustees, founders, and concerns of substantial interest. This would ease the burden on auditors and align with the practicality of such disclosures.

Conclusion: The Chamber of Tax Consultants’ representation addresses the challenges faced by taxpayers and auditors in light of extensive reporting requirements and software revisions. Their request for an extension of the due dates and relaxation of certain details is grounded in practicality and aims to ensure a smoother tax filing process for all parties involved. The Chamber eagerly awaits a positive response from the authorities, hoping for a more manageable tax compliance environment.

*****

Chamber of Tax Consultants

25th October, 2023

To,

Smt. Nirmala Sitharaman,

Hon’ble Finance Minister of India

North Block,

New Delhi —110 001

To,

Shri Nitin Gupta

Chairman

Central Board of Direct Taxes, North Block,

New Delhi —110 001

Respected Madam Sir,

Sub : Representation for relaxation of certain requirements in new Forms 10B and Form 10BB and for further extension of due date for filing these Forms

The Chamber of Tax Consultants, established in 1926, is one of the oldest non-profit organizations of tax practitioners, having Advocates, Chartered Accountants and Tax Practitioners as its members spread across Pan India. Many senior tax professionals who regularly appear before ‘ITAT, High Courts and the Supreme Court are its Past Presidents. It has from time to time made various representations to different Government Authorities drawing their attention to pressing issues.

Vide our earlier representation dated 11th September, 2023, we had urged Your Honours for extension of due dates for filing Form 103, Form 10BB and ITR-7. You have been kind enough to address the same positively and extend the due dates of filing Form 10B and Form 10BB to 31st October. 2023 and the due date for filing ITR-7 to 30th November, 2023. Further. the Central Board of Direct Taxes has issued a circular, being Circular No. 17 dated 9th October, 2023. Vide this circular, the CBDT has relaxed certain requirements of Form No. 10B and Form 10BB. We would like to express our sincere thanks to you for the extension of time and also for relaxation of certain requirements which were difficult to comply.

In continuation of our earlier request, we would like to make further request to Your Honours as under:

Extensive details required for Form 10B and Form 10BB

We respectfully submit that the new Forms 103 and IOBB still has difficulties due to extensive details which are required to be filled in for the above Forms. Some of the details required are not there even in the Income-tax Returns and as such these are additional details to be provided by the auditor and the trusts.

Some of such details in relation to Form 1013, where the auditors and the charitable trusts are haling genuine difficulties are bent¢ listed hereunder for Your kind perusal

i) Clause 15 requires various details for each of the project undertaken by the trust

ii) Clause 19 requires extensive details of receipts by the trust where tax has been deducted under specified sections.

iii) Clause 23 of the Form requires the details of donations including cash donations, donation received from other trust: other donations and donation received in kind, anonymous donations etc. The details required are azain very voluminous

iv) Clause 31 of the Form requires extensive details about application of income including, bifurcation of expenses into electronic mode and other than electronic mode, amount not actually paid during the previous year: amount to be disallowed as application of funds etc.

v) Clause 33 requires details of Income taxable under Section 115BBI

vi) Clause 37 requires details of application of income out of different sources. This is also required to be bifurcated between application made through electronic mode and other than electronic mode.

vii) Clause 42 requires details of transactions referred to in Sec. 13(2). There are eight sub-clauses in this clause and the auditor is also required to report about the unreasonableness of the transactions. This is becoming extremely difficult since most of the auditee has not maintained documents to prole the reasonableness.

viii) Clause 43 requires details of specified violation. The auditees are not able to provide such details with in the available time.

ix) Clauses 46 to 49 of the Form requires details about contravention of the provisions of section 269SS, section 269ST, section 269T and also the provisions of TDS and ICS.

As such, you gill appreciate that the details called for in the new Form 10B is much extensive and it is having lot of practical difficulties since many of the details are not readily available with the charitable trusts • institutions. Some of the above difficulties are also common for the purpose of filing new Form 10BB.

Utilities provided are under revision

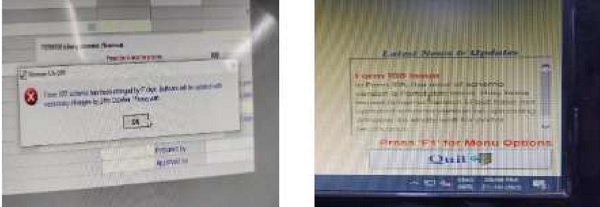

Further, we would also like to bring your kind attention on the fact that the utility provided by the department is under revision. The Schema for Form 10B has been changed very recently and the software from the private software vendors are under revision to incorporate the changes in the Schema. We are attaching a screen shots for the same, as taken on 22rd October, 2023 for your ready reference :

Request for further extension of time to furnish the Form 10B and Form 10BB

Considering the fact that the details required are extensive as explained above and also the fact that the schema version has been amended recently, which results in unintended delay in finalising the reports, we respectfully submit that it is absolutely difficult for the auditors to complete the above audits with the required diligence in the short time available.

We, therefore, request Your Honours to kindly grant further extension of a month for filing the Form 10B and Form 10BB and also the ITR-7 as a consequence to the same. We request for the following due dates of compliance to ensure proper filing of the forms :

| Form / Return | Extended Due Date for A Y 2023-24 | Extension Requested |

| Form 10B and Form 10BB | 31st October 2023 | 30th November 2023 |

| Filling ITR 7 | 30m November 2023 | 31st December, 2023 |

Request for relaxation of certain requirements in relation to details about relatives of the trustees / seniors / founders and the concerns in which such persons has substantial interest

As per the Circular No. 17 dated 9th October, 2023, the CBDT has relaxed certain requirements in relation to the information to be provided for relatives of the donors to the trusts. The circular provides that the information needs to be given only in case of relatives of donors who have given contribution of more than Rs. 50,000/- during the year and it further provides that such details may be given only if the same is available.

While the above circular is certainly a welcome relaxation, we respectfully submit that the circular relaxes the requirements only in relation to the relatives of donors and the concerns where the donors have substantial interest. We respectfully submit that it will be desirable to allow similar concession in relation to the relatives of the settlors / trustees and founders of such trust and also the concerns in which the seniors trustees and founds have substantial interest. This is necessary considering the fact that it is humanly impemsible for the auditor to confirm the correctness of the list of such relatives and concern& We also request you to kindly appreciate that as long as no amount has been spent by the trusts for the benefits of such relatives / concerns, there is no violation of the provisions of the law and therefore, calling for such details will not be having any material relevance.

We hope Your Honours will consider both our requests positively.

Thanking you,

Yours sincerely,

For The Chamber of Tax Consultants

Sd/-

Haresh P. Kenia

President

sd/-

Ketan L. Vajani

Chairman

Law & Representation Committee