Navigating the intricacies of Show Cause Notices (SCN) under the Goods and Services Tax (GST) regime is crucial for businesses. This presentation delves into the redressal of issues related to SCNs, encompassing procedures, key judgments, and the implications of SCN issuance.

Redressal of issues on Show Cause Notice (SCN) under GST

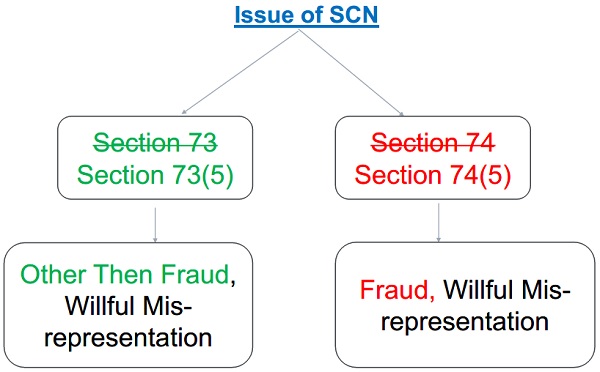

Procedure as per Rule 142(1A) to Issue SCN u/s 73/74

Important Judgement

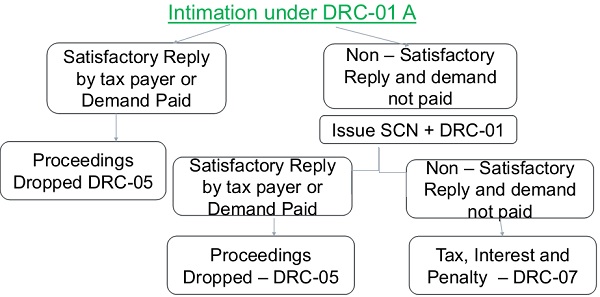

Agrometal Vendibles Private Limited vs State of Gujarat (Gujarat High Court) 6919/2022 held that “the department needs to correct itself not only as regards their understanding of the entire procedure, but even the contents of the Forms are incorrect. The intention of the proper officer was to give an intimation in accordance with sub-section (5) of Section 74 and therefore, the intimation should have been in the Form GST DRC – 01A and not Form GST DRC – 01.Therefore, DRC-01 issued by the department is set aside.”

Reasons for issuing of SCN

❑ Tax Short Paid as per GSTR 1 & GSTR 9/9C

❑ Tax Short Paid as per GSTR 1 & GSTR 9/9C

❑ Difference between the tax liability as per GSTR 1 & E-way Bills

❑ Excess ITC Claimed as per GSTR 2A and GSTR 3B

❑ Exempt Supply – Common ITC – Rule 42 & Rule 43

❑ Claim of ITC in respect of supplies from taxpayers whose registrations have been cancelled retrospectively.

Reasons for issuing of SCN

❑ ITC received after Cut off Date

❑ Ineligible ITC u/s 17(5)

❑ Mismatch in HSN Codes

❑ GSTR – 3B not filed by the supplier

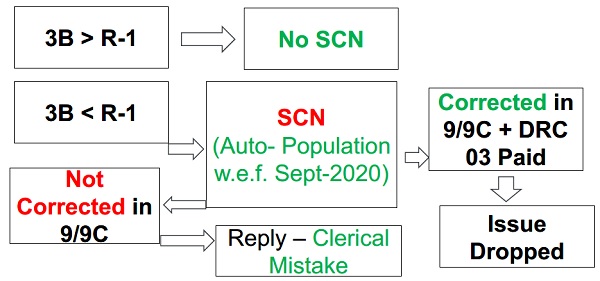

Tax Short paid as reported in GSTR 1 & GSTR 3B

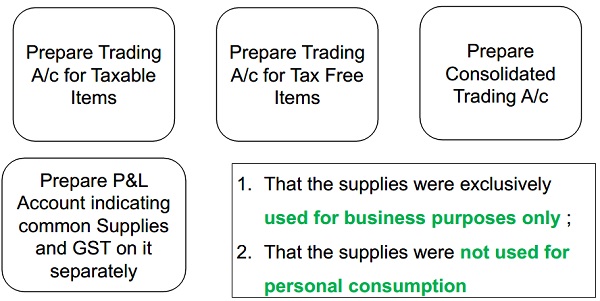

Exempt Supply – Common ITC – Rule 42 & Rule 43

Difference between the tax liability as per GSTR 1 & E-way Bills

| Financial Year |

|

E-way Bill Applicability | |

| 2017-18 | NO | ||

| 2018-19 | YES | ||

| 2019-20 | YES |

Note :- E-way Bill was applicable w.e.f. 01.04.2018 for Interstate Movement of Goods

(Press Release dated March 10, 2018)

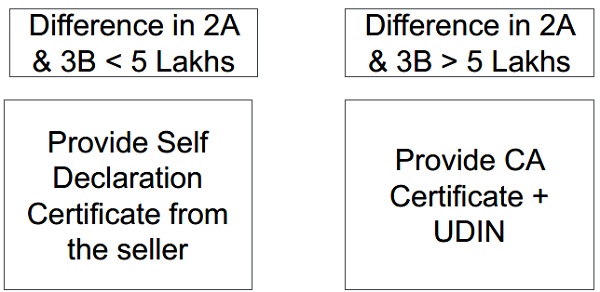

Excess ITC Claimed as per GSTR 2A and GSTR 3B

Excess ITC Claimed as per GSTR 2A and GSTR 3B

The Hon’ble Supreme Court in the matter of Union of India vs Bharti Airtel (Civil Appeal No. 6520 of 2021) held that “GSTR-2A is mere a facilitator and the recipient is required to avail the ITC on the basis of self assessment as GSTR-2A cannot be presumed to be accurate and complete.”

Diya Agencies vs State Tax Officer arising out of W.P.(C). 29769 of 2023, the Hon’ble Kerela High Court held that “ITC cannot be denied to the recipient solely on the ground that transactions are not reflected in GSTR-2A.”

Claim of ITC from Cancelled Dealers

Case – 1 : Where Tax payer voluntarily cancelled his GSTIN

Case – 2 : Where Tax Payer GSTIN was cancelled suo-moto from Current Date

Case – 3 : Where Tax Payer GSTIN was cancelled retrospectively

Case – 4 : Where Tax Payer GSTIN was cancelled but was active after issue of SCN

Case – 1 : Where Tax payer voluntarily cancelled his GSTIN

Case – 2 : Where Tax Payer GSTIN was cancelled suo- moto from Current Date

Case – 3 : Where Tax Payer GSTIN was cancelled retrospectively

Sun Craft Energy Pvt Ltd – Supreme Court “a major relief to purchasers and dealers, held that Input Tax Credit is not to be denied to Purchaser for fault of Seller if purchaser meets all conditions of Section 16(2)”

Gargo Traders vs Joint Commissioner of Commercial Taxes arising out of W.P.C. 1009 of 2022, the Hon’ble Calcutta High Court held that “a recipient of goods/services cannot be denied ITC if supplier becomes non-existent or their registration was cancelled retrospectively.”

Section 16 (2) – Conditions for claiming Input Tax Credit

a) Possession of Tax Invoice, debit note

b) Received the goods or services

c) Tax was paid to Government either in Cash or by utilizing ITC

d) Furnished the return under section 39

Important Judgements

Retrospective Effect of Cancellation of GST Registration not mentioned in SCN: Delhi High Court Orders to Cancel GST Registration Prospectively : Aditya Polymers vs Commissioner of Delhi GST 2023 TAXSCAN (HC) 699

Retrospective Cancellation of Registration of Purchasing Dealer does not affect Right of Selling dealer for Deduction: Asha Oil Traders – Rajasthan High Court 2022 TAXSCAN (HC) 194

Case – 4 : Where Tax Payer GSTIN was cancelled but was active after issue of SCN

Give the screenshot that GSTIN is active

| Time Limit for Completion of Issue Notice for Sec 73 (9) | ||

| Financial Year |

|

Last Date to Issue Notice |

| 2017-18 | 31st December, 2023 | |

| 2018-19 | 31st March, 2024 | |

| 2019-20 | 30th June, 2024 | |

Section – 73 : For passing an order under Section-73, Officer should issue notice at-least 3 months prior of issuing order.

Section – 74 : For passing an order under Section-74, Officer should issue notice at-least 6 months prior of issuing order.

Important Instructions

> Whether Interest charged by the department is payable as mentioned in DRC-01 in cases where the demand has been paid through Electronic Credit Ledger ?

No interest is payable – CBEC-20/01/08/2019 – GST dated 18.09.2020

As per above Instruction, interest is payable only on part of net cash tax liability.

Contents of Show Cause Notice (SCN)

– Document Identification Number (DIN) or RFN ,

– Complete Information about discrepancy,

– Discrepancy should be specific and not vague and general,

– quantify the amount of tax of such discrepancies,

– Discrepancies should be parameter wise along with detail including worksheets, supporting documents,

– required to scrutinize all the returns and a single compiled notice may be issued for full Financial Year under consideration.

Modes of Sending Notice and Orders

| Financial Year | Manual | Online |

| 2017-18 | X | √ |

| 2018-19 | X | √ |

| 2019-20 onwards | X | √ |

Important Instructions

> Instruction No. 04/2023-GST dated 13th December, 2023 : All Notices and orders under Section 52, 62, 63, 64, 73, 74, 75, 76, 122, 123, 124, 125, 127, 129, 130 must be uploaded on the portal.

– Summary order must be uploaded on the portal,

– Non Uploading of Summary of such Notice or order electronically on portal is in clear violation of GST Rules.

Important Judgements

Cancellation of GST Registration with Retrospective Effect Cannot be Ground to Deny ITC from Supplier to Purchaser : Gargo Traders vs Joint Commissioner GST Calcutta High Court 2023 TAXSCAN (HC) 957

Marketing Private Limited vs State Of U.P. 2022 TAXSCAN (HC) 273 The Allahabad High Court has held that the GST registration cannot be canceled merely for the reason that a firm is described as “bogus”.

Gujarat High Court refused the show-cause notices in form GST DRC-01 holding that it had been issued without expensing a personal hearing to the taxpayer

> Hitech Sweet Water Technologies Pvt. Ltd VS State of Gujarat C/SCA/14347/2022

Show Cause Notice should be in a particular format

> Metal Forging vs Union of India – 2002 (11) TMI 90- Supreme Court

> Gorkha Security Services vs Govt. of NCT Delhi – 2014 (8) TMI 1081- Supreme Court

> No adverse order could be passed against the petitioner without informing the petitioner of reasons for the same and affording him an opportunity to respond to the same : Roxy Enterprises High Court Of Delhi W.P.(C) 7023/2023

> Form GSTR-2A is only a facilitator for taking an informed decision while doing self-assessment : Kishore Projects Private Limited In The High Court Of Gujarat At Ahmedabad Special Civil Application No. 25604 of 2022

Judgements on Vague and Cryptic Notices

“Any shortfall in providing a reasonable opportunity for the defendant to respond can render the notice, and any consequent proceedings, invalid in law.”

> Sidhi Vinayak Enterprises Vs. The State of Jharkhand W.P.C. 745/2021.

Author Bio

very useful indeed.

very useful