Case Law Details

Aathi Hotel Vs Assistant Commissioner (ST) (FAC) (Madras High Court)

No interest and penalty to be imposed if credit is merely availed but not utilised | Section 73 & 74 Interest will be attracted only if wrong/excess ITC availed & utilized

The Hon’ble Madras High Court in Aathi Hotel v. Assistant Commissioner (ST) (FAC) [W.P.No.3474 of 2021 W.M.P.Nos.3980 & 3982 of 2021 dated December 08, 2021] has held that, the interest is to be attracted only where credit is not only availed but also utilised for discharging tax liabilities and if there is an attempt to wrongly avail the credit and utilise the same then the tax liability would arise.

Facts:

M/s. Aathi Hotel (“the Petitioner”) is an hotelier and had purchased certain capital goods in connection with the business. The Petitioner had filed Form GST TRAN-1 and claimed a transitional credit i.e. Input Tax Credit (“ITC”) of INR 3,86,271, of VAT paid on capital goods purchased for hotel business, with a view to set off future tax liability of its furniture business, which was actually not available to the Petitioner. The transitional credit availed by the Petitioner was never utilized.

In this regard, a Show Cause Notice (“SCN”) was issued to the Petitioner followed by summary Show Cause Notice (“Summary SCN”), for which, the Petitioner replied and admitted the mistake of availing the credit and reversed the transitional credit in the GST returns.

Consequently, the Revenue Department (“the Respondent”) passed an order (“the Impugned Order”) under Section 74 of the Central Goods and Services Tax Act, 2017 (“the CGST Act”), levying interest and imposing penalty on the Petitioner.

Being aggrieved, the Petitioner has challenged the Impugned Order.

Issue:

Whether the Petitioner is liable to pay interest and penalty for availment of ITC and not utilised?

Held:

The Hon’ble Madras High Court in W.P.No.3474 of 2021 W.M.P.Nos.3980 & 3982 of 2021 dated December 08, 2021 held as under:

- Observed that there is no record to show that the Petitioner had started such business in sale of furniture, yet the Petitioner had wrongly attempted to transition a credit of hoping that in case of future tax liability, the Petitioner can use the same against the tax liability. Thus, the intention of the Petitioner was not bona-fide.

- Noted that, the Petitioner admitted the mistake and accordingly reversed the ITC in the returns filed for the month of January 2019-20 in Form GSTR-3B. Though an improper attempt was made by the Petitioner to transition the ITC, the Petitioner had not utilized the same and had also reversed the same within a prescribed period under Section 73 of the CGST Act.

- Stated that, before levying penalty or interest, a proper excise was required to be made by the Respondent under Section 74(10) after ascertaining whether the credit was wrongly availed and wrongly utilised. Though, proceedings can be initiated under Section 73(1) and Section 74(1) of the CGST Act for mere wrong availing of ITC followed by imposition of interest penalty but it is only attracted where such ITC is not only availed but also utilised for discharging the tax liability. The proper method would have been to levy penalty under Section 122 of the CGST Act.

- Partly quashed the Impugned Order and set aside the liability of interest and penalty.

- Held that, since there was an attempt to wrongly avail the ITC and utilise the same, when the tax liability would have arisen, the Petitioner is liable to a token penalty of INR 10,000.

Our Comments:

It is to be noted that, proceedings in case where the ITC is merely availed and not utilised for payment of tax, would certainly be arbitrary and restricting the freedom to carry on trade without any justification and would be in violation of Articles 14, 19 and 301 of the Constitution of India.

Further, Section 50(3) of the CGST Act has been substituted retrospectively from July 01, 2017 vide the Finance Act, 2022, so as to provide for levy of interest on ITC wrongly availed and utilised against payment of output liabilities, which would come into force on the date as appointed by way of a notification.

As per the above amendment, the levy of interest would not be applicable in case of the ITC is merely availed and retained in the electronic credit ledger. This amendment is also in line with the general principle of interest being compensatory in nature as mere availment of credit is just a book entry and there is no actual loss to the revenue, whereas, there is a loss to the revenue only when the ineligible credit is utilized towards payment of tax.

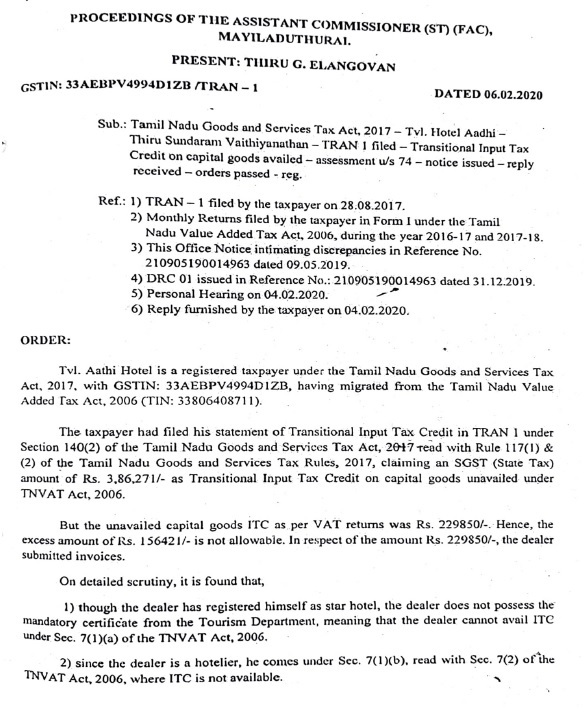

FULL TEXT OF THE JUDGMENT/ORDER of MADRAS HIGH COURT

The petitioner had challenged the impugned order dated 06.02.2020, which reads as under:-

____

2. It is the case of the petitioner that though the petitioner had filed TRAN-1 and claimed a credit of Rs.3,86,271/-, the aforesaid credit was never utilized and therefore even though the petitioner had failed to reply to the Show Cause Notice dated 09.05.2019 followed by a summary Show Cause Notice dated 31.12.2019, the question of levying interest and imposing penalty on the petitioner under the provisions of Tamil Nadu Goods and Services Tax Act, 2017 does not arise inasmuch as the entire transitional credit of Rs.3,86,271/- was reversed by the petitioner in the monthly returns for the month of January 2020 for the Assessment Year 2019-2020.

3. The learned counsel for the petitioner submits that Section 74 of the Tamil Nadu Goods and Services Tax Act, 2017 will get attracted only where there is a wrong utilization of credit availed. In this connection, the learned counsel for the petitioner has referred to Section 50 (3) of the Act. It is submitted that interest under Section 50 (3) of the Act will apply only in the case of a person who makes undue or excess claim of Input Tax Credit under sub-section 10 of Section 42 or undue or excess reduction in output tax liability under sub-section 10 of Section 43 in which case, interest shall be paid on such undue or excess claim or on such undue or excess reduction/deduction as the case may be, at such rate not exceeding 24 percentage as may be notified by the Government on the recommendations of the GST Council.

4. The learned counsel for the petitioner further submits that Section 42 (10) of the Tamil Nadu Goods and Services Tax Act, 2017 is not attracted in the facts and circumstances of the case, as the petitioner has never utilized the credit which was attempted for transition by filing TRAN-1. He submits that sub-section 10 to Section 42 will apply when the amount reduced from the output tax liability in contravention of the provisions of sub-section 7 which has to be added to the output tax liability of the recipient in his return for the month in which contravention takes place and such recipient shall be liable to pay tax/interest on the amount so added at the rate specified under sub-section 3 of Section 50 of the Tamil Nadu Goods and Services Tax Act, 2017.

5. The learned counsel for the petitioner further submits that Section 42 (7) will not apply as Section 47 (2) applies to the situation where will apply, in the case of a recipient. Section 42(7) of the Act reads as under:-

“Section 42. Matching, reversal and reclaim of

input tax credit-

(7). The recipient shall be eligible to reduce, from his output tax liability, the amount added under sub-Section (5), if the supplier declares the details of the invoice or debit note in his valid return within the time specified in sub-Section (9)

6. The learned counsel for the petitioner has also referred to decision of the Hon’ble Division Bench of the Patna High Court in the case of Commercial Steel Engineering Corporation Vs. State of Bihar, [2019] 28 GSTL 579 (Patna). A specific reference was made to Paras 29 and 35 & 36 which reads as under:-

“29. I have reproduced the relevant provisions of the ‘BGST Act’ which finds mention in the discussion held for ready reference. The legislative intent present in these provisions is eloquent and I am in no confusion to hold that be it a charge of wrong availment or utilization, each is a positive act and it is only when such act is substantiated that it makes the dealer concerned, liable for recovery of such amount of tax as availed from the input tax credit or utilized by him but in each of the two circumstances, the tax available at the credit of the dealer concerned must have been brought into use by him thus, reducing the credit balance. A plain reading of Section 73 would confirm that it is only on such availment or utilization of credit to reduce tax liability, which is recoverable under section 73(1) read alongside the other provisions present thereunder. In fact the position is made even more clear by reading the said provision alongside sub-section (5), (7), (8), (9) to (11).

30. ……

31. ……

32. ……

33. ……

34. ……

35. The legislative intent reflected from a purposeful reading of the provisions underlying section 140 alongside the provisions of section 73 and Rules 117 and 121 is that even a wrongly reflected transitional credit in an electronic ledger on its own is not sufficient to draw penal proceedings until the same or any portion thereof, is put to use so as to become recoverable.

36. This important aspect of the matter has eluded the wisdom of the respondent no.3 while passing the order. In fact it is on a complete misappreciation of legal position which lies at the foundation of the demand raised by the impugned order whereby the credit amount reflected in the credit ledger to the tune of Rs.42,73,869.00 has been treated as an outstanding tax liability against the petitioner to order for its recovery together with interest and penalty even when the electronic credit ledger status at Annexure 7 confirms to a credit in favour of the petitioner i.e. a negative tax liability.”

7. Opposing the prayer, the learned Additional Government Pleader for the respondent submits that the petitioner has an alternate remedy under Section 107 of the Tamil Nadu Goods and Services Act, 2017 and therefore this writ petition is liable to be dismissed.

8. The learned Additional Government Pleader for the respondent submits that the petitioner has an alternate remedy before the Appellate Commissioner and therefore the writ petition is liable to be dismissed. The learned Additional Government Pleader for the respondent further submits that the petitioner was neither entitled to Input Tax Credit under the provisions of the erstwhile Tamil Nadu Value Added Tax Act, 2006 nor entitled to transition in the credit under the provisions of Tamil Nadu Goods and Services Tax Act, 2017 and therefore submits even on merits the petitioner is liable to pay interest and penalty for availing the transitional credit wrongly.

9. The learned Additional Government Pleader for the respondent further submits that the petitioner has admitted that the petitioner was not registered as a dealer of furniture products under the TNVAT Act, 2006 and therefore the attempt of the petitioner to avail credit and transition the same shows that the petitioner’s intention was not bonafide but was to wrongly utilize the input tax credit which was not available to the petitioner.

10. That apart, it is submitted that the petitioner had un-availed credit for a sum of Rs.2,29,8501- whereas the petitioner transitioned a credit of Rs.3,86,2711- with a view to wrongly utilize the same.

11. The learned Additional Government Pleader for the respondent further submits that the interest is consequential and the penalty is also consequential in terms of the Section 74 of the TNGST Act, 2017 and therefore prays for the dismissal of the writ petition.

12. Heard the learned counsel for the petitioner and the learned Additional Government Pleader for the respondents and perused the impugned order and the decision of the Hon’ble Patna High Court referred to supra.

13. The undisputed facts of the case are that the petitioner is a hotelier and had purchased certain capital goods in connection with the business. Since GST was being implemented, the petitioner appears to have availed input tax credit paid on the capital goods which were purchased in connection with the hotel business with a view to set off the tax liability on the furniture business which the petitioner intended to start.

14. There are no record to show that the petitioner had started such business in sale of furniture. What is evident is that the petitioner had wrongly attempted to transitioned a credit of Rs.3,86,271/- hoping that in case of future tax liability, the petitioner can use the same against the tax liability. Thus, the intention of the petitioner was not bonafide.

15. After Show Cause Notice was issued to the petitioner on 09.05.2019, the petitioner replied and admitted the mistake by a reply dated 04.02.2020. The petitioner also reversed the transitional credit in the returns filed for the month of January 2019-20 in Form GSTR-3B under Rule 61(5) of the TNGST Rules, 2017. There are no records to show utilization of such credit.

16. Thus, the facts on record indicates that though an improper attempt was made by the petitioner to transition the aforesaid credit. The petitioner had however not utilized the same and had also reversed the same on 10.02.2020 after a Show Cause Notice were issued within a period prescribed under Section 73 of TNGST Act, 2017 by invoking Section 74 of the TNGST Act, 2017. However, the Show Cause Notice does not invoke the ingredients to justify the invocation of Section 74 of

17. Be that as it may, if the Show Cause Notice issued to the petitioner on 09.05.2019 is to be construed as a notice under Section 74 of the TNGST Act, 2017, the Show Cause Notice should have specifically invoked the ingredients of Section 74(1) of the TNGST Act, 2017. However, the said notice merely states that due to the unavailability of documents to prove admissibility of the ITC, Assessment under Section 74 is proceeded. Thus, the Show Cause Notice dated 31.12.2019 does not meet the requirements of Section 74(9) of the TNGST Act, 2017.

18. The Hon’ble Supreme Court in Union of India Vs. Ind-Swift Laboratories Limited [2011] 4 SCC 635 while construing the provisions of erstwhile Cenvat Credit Rules 2002, held that wrong filing of credit rule attracts interest under the Provisions of the Cenvat Credit Rules 2002 read with Central Excise Act, 1944. There the credit was availed and the benefit of refund was claimed. The case was attempted to be settled after payment of the amount ITC availed utilized before the settlement commission which circled interest at 10% per annum from the due dte as per Section 11 AB of the Central Excise Act, 1944. In paragraph 17 the Court held as under:-

“17. We have very carefully read the impugned judgment and order of the High Court. The High Court proceeded by reading it down to mean that where CENVAT credit has been taken and utilized wrongly, interest should be payable from the date the CENVAT credit has been utilized wrongly for according to the High Court interest cannot be claimed simply for the reason that the CENVAT credit has been wrongly taken as such availment by itself does not create any liability of payment of excise duty. Therefore, High Court on a conjoint reading of Section 11AB of the Act and Rules 3 & 4 of the Credit Rules proceeded to hold that interest cannot be claimed from the date of wrong availment of CENVAT credit and that the interest would be payable from the date CENVAT credit is wrongly utilized. In our considered opinion, the High Court misread and misinterpreted the aforesaid Rule 14 and wrongly read it down without properly appreciating the scope and limitation thereof. A statutory provision is generally read down in order to save the said provision from being declared unconstitutional or illegal. Rule 14 specifically provides that where CENVAT credit has been taken or utilized wrongly or has been erroneously refunded, the same along with interest would be recovered from the manufacturer or the provider of the output service. The issue is as to whether the aforesaid word “Or” appearing in Rule 14, twice, could be read as “AND” by way of reading it down as has been done by the High Court. If the aforesaid provision is read as a whole we find no reason to read the word “OR” in between the expressions ‘taken’ or ‘utilized wrongly’ or ‘has been erroneously refunded’ as the word “AND”. On the happening of any of the three aforesaid circumstances such credit becomes recoverable along with interest”

19. The ratio in the above case is to be distinguished on facts as in the present case although credit was wrongly attempted to be transitioned, it was never utilized. Further before levying penalty or interest, a proper excise was required to be made by a proper officer under Section 74(10) after ascertaining whether the credit was wrongly availed and wrongly utilised. Though under Sections 73(1) and 74(1) of the Act, proceedings can be initiated for mere wrong availing of Input Tax Credit followed by imposition of interest penalty either under Section 73 or under Section 74 they stand attracted only where such credit was not only availed but also utilised for discharging the tax liability. The proper method would have been to levy penalty under Section 122 of TNGST Act, 2017.

20. Considering the above, I am inclined to hold that the petitioner is not liable to penalty imposed. At the same time, since there was an attempt to wrongly avail credits and utilise the same as and when the tax liability would have arisen, the petitioner is held liable to a token penalty. Considering the gravity of the mistake committed by the petitioner, a penalty Rs.10,000/- is imposed on the petitioner. The impugned order stands partly quashed.

21. Accordingly, this writ petition stands partly allowed in terms of the above observations. No costs. Consequently, connected miscellaneous petitions are closed.

*****

(Author can be reached at info@a2ztaxcorp.com)

Author Bio

sir like your guide if Cenvat credit could,t be filed but credited and avialed in GSTR-3 B.after SC Jud. reversed .can GST ask for interest for the period from 1.7.2017.where as CENVAT IS ENETILEMENT FROM ACCRUAL Date 1.7.2017.

m 9999001345

IGST tax wrongly availed CGST AND SGST, Next year 3B revised ITC CSGT AND SGST then claim IGST interest applicable section 50(1)

Very nicely written 👍👍