The National Financial Reporting Authority (NFRA) has issued Order No. 001/2024, dated 3rd Jan, 2024, addressing a case of professional misconduct under section 132(4)(c) of the Companies Act, 2013. The order pertains to CA Pawan Jain, a member of ICAI, and M/s Kumar Jain & Associates, involving their issuance of reports under section 80 JJAA of the Income Tax Act for the financial years 2018-19, 2019-20, and 2020-21 concerning Quess Corp Ltd. NFRA’s investigations reveal lapses in due diligence and information verification, leading to a monetary penalty of Rs 50 Lakhs imposed on CA Pawan Jain. This analysis delves into the executive summary, background, identified lapses, charges, and the sanctions imposed by NFRA, shedding light on the gravity of the professional misconduct.

Government of India

National Financial Reporting Authority

*****

7th – 8th Floor, Hindustan Times House,

Kasturba Gandhi Marg, New Delhi

Order No. 001/2024 Dated: 03rd Jan, 2024

In the matter of CA Pawan Jain u/s 132 (4) (c) of the Companies Act, 2013.

1. This order disposes of the Show Cause Notice (‘SCN’ hereafter) no. NF- 23/23/2022 dated 21.06.2023 issued to M/s Kumar Jain & Associates (ICAI1 Firm Registration No: 016717S) and CA Pawan Jain (ICAI membership No: 228026), who is a member of ICAI and issued reports u/s 80 JJAA of the Income Tax Act for the financial years 2018-19, 2019-20, and 2020-21 in the matter of Quess Corp Ltd. (‘Quess’ hereafter). CA Pawan Jain is hereafter referred to as ‘the CA’ in this order.

2. This Order is divided into the following sections:

A. Executive Summary

B. Introduction & Background

C. Lapses in issue of reports

D. Finding on the Articles of Charges of Professional Misconduct by the Firm and CA

E. Penalty & Sanctions

A. EXECUTIVE SUMMARY

3. In August 2022 the Director General of Income Tax (Investigation), Bengaluru (IT department) shared information about claim of deduction under section 80 JJAA of Income Tax Act totalling Rs 1135.41 crores by Quess based on form 10 DA issued by two chartered accountants for Financial Years 2016-17, 2017-18, 2018-19, 2019-20 & 2020-21. NFRA Suo motu initiated action under Section 132(4) of the Companies Act, 2013 (‘Act’ hereafter) to look into the professional conduct of the chartered accountants and their firms involved in the said certification.

4. NFRA’s investigations inter alia revealed that the CA failed to exercise due diligence and obtain sufficient information before issuing reports under the Income Tax Act. The CA failed to apply the necessary checks, e.g., (a) verify reorganization of business with various parties; (b) exclude employees whose EPS2 contribution was paid by the Government; (c) correctly report the number of additional employees during FY 2020-21; (d) verify that payment of additional employee cost was made by account payee cheque/draft/electronic means; and (e) verify salary limit of Rs 25000 per month for new employees, etc.

5. Based on investigation and proceedings under section 132 (4) of the Companies Act 2013 and after giving the CA an opportunity to present their case, NFRA found the CA, who issued reports under Income Tax Act to Quess Corp Ltd, guilty of professional misconduct and imposes through this Order a monetary penalty of Rs fifty (50) Lakhs which take effect from a period of 30 days from issuance of this Order.

B. INTRODUCTION & BACKGROUND

6. NFRA is a statutory authority set up under Section 132 of the Companies Act 2013 (Act hereafter) to monitor implementation of the auditing and accounting standards and oversee the quality of service of the professions associated with ensuring compliance with such standards. NFRA is empowered under Section 132 (4) of the Act to investigate professional misconduct or other misconduct of individual members or firms of chartered accountants associated with prescribed classes of companies3 and sanction them where such misconduct is proved.

7. The Chartered Accountant Firms, Engagement Partners (EP) and the Engagement team that issues reports/certificates are bound by the duties and responsibilities prescribed in the standards on quality control and the Code of Ethics, the violation of which may constitutes professional misconduct, and is punishable with penalty prescribed under Section 132 (4) of the Act.

8. In August 2022 the Director General of Income Tax (Investigation), Bengaluru (Income Tax department) shared information about irregularities in deduction of Rs.113 5 .41 crores claimed by Quess under section 80 JJAA of the Income Tax Act, based on form 10 DA issued by two chartered accountants for. Financial Years 2016-17, 2017-18, 2018-19, 2019-20 & 2020-21. The irregularities were reinforced by the special audit commissioned by the Income Tax Department.

Quess Corp Limited being a listed company falls within the jurisdiction of NFRA in terms of Rule 3 of NFRA Rules 2018. It is engaged in the business of providing services in Workforce Management, Operating Asset Management and Global Technology Solutions. CA Pawan Jain, partner of M/s Kumar Jain & Associates, has signed the reports in form 1 ODA, which formed the basis of Quess claiming deduction under section 80JJAA of the Income Tax Act for FY 2018-19, 2019-20 and 2020-21.

9. NFRA Suo motu initiated proceedings under section 132(4) of the Act and on 23.09.2022 the CA was advised to submit the working files relating to the deduction claimed by Quess. The CA submitted the Files on 29.09.2022 and 11.10.2022. Based on their examination, NFRA, after observing prima facie professional misconduct, issued a Show Cause Notice (‘SCN’ hereafter) dated 21.06.2023 under section 132(4) of the Act, for (a) failure to exercise due diligence and being grossly negligent in the conduct of professional duties, and (b) failure to obtain an appropriate information necessary for expression of an opinion or its exceptions to negate the expression of an opinion. All of these constituted professional misconducts.

10. The CA sought extension of 7 days for replying, which was allowed. Vide email dated 28.07.2023 he submitted the reply to SCN. A personal hearing was also scheduled for 2 1.08.2023, but CA Pawan Jain sought extension of four weeks’ time. On 18.08.2023, NFRA rescheduled the personal hearing for 04.09.2023 . Vide mail dated 30.08.2023, CA Pawan Jain intimated that due to ongoing health challenges, he was not able to secure the services of a legal representative and requested to consider his reply dated 28.07.2023 as final submission. He stated that he had done certification of Form 1 ODA based on detailed review of documents, management discussion, process controls in place, understanding of the entity’s business and to the best of his professional judgement. He further stated that he might have erred in his professional judgement as highlighted in the SCN but it was not due to negligence in his professional duty, but possibly due to interpretation of the relevant regulations and guidance note. He requested that a lenient view be taken, considering the small size of his Firm and the impact on his professional career. This Order is based on examination of the facts of the case, charges in the SCN and written replies of CA Pawan Jain.

C. LAPSES IN ISSUE OF REPORTS

11. It is important to have a look at relevant Statutory provisions of the Income Tax Act and details of reports issued by the CA in this matter.

Section 80 JJAA of the Income Tax Act provides for deduction of an amount equal to thirty per cent of additional employee cost incurred in the course of such business in the previous year4, for three assessment years including the assessment year relevant to the previous year in which such employment is provided. Rule 19 AB of the Income Tax Rules provides that the report of an accountant, which is required to be furnished by the assessee along with the return of income under clause (c) of sub-section (2) of section 80JJAA, shall be in Form No. lODA- notified and amended from time to time. Form 10 DA is a report to be issued by a practicing chartered accountant based on which the deductions are claimed from taxable income by the company reported upon. The report should give details of the:

a) number of employees as on the last day of the immediately preceding year,

b) number of employees as on the last day of the previous year,

c) number of employees employed during the previous year,

d) number of additional employees, the emoluments of whom is eligible for deduction under section 80JJAA,

e) total amount of emoluments paid or payable to additional employee entitled for deduction u/s 80JJAA,

f) the amount of deduction eligible u/s 80JJAA in respect of payments for the emoluments paid or payable to the additional employee.

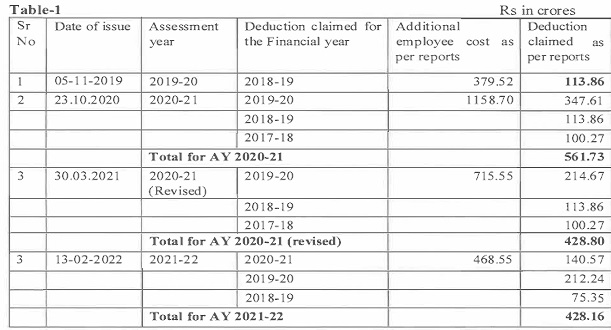

12. CA Pawan Jain had issued 4 reports in Form 10 DA based on which Quess had claimed deduction of Rs. 970.82 crores from its taxable income, the details of which are as under in Table 1:

One of the basic preconditions to this deduction is that the business should not be formed due to the splitting up, reconstruction or reorganization of any business. Subsection 2 of section 80JJAA is quoted below:

“80JJAA(2) : No deduction under sub-section (1) shall be allowed,-

(a) if the business is formed by splitting up, or the reconstruction, of an existing business:

Provided that nothing contained in this clause shall apply in respect of a business which is formed as a result of re-establishment, reconstruction or revival by the assessee of the business in the circumstances and within the period specified in section 33B;

(b) if the business is acquired by the assessee by way of transfer from any other person or as a result of any business reorganization;

(c) unless the assessee funishes along with the return of income the report of the accountant, as defined in the Explanation to section 288 giving such particulars in the report as may be prescribed”.

I. Failure to verify reorganization of business with various parties

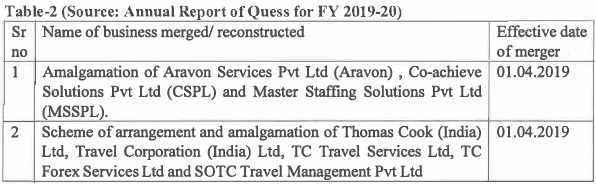

13. The Financial Statements of Quess for FY 2018-19 & 2019-20 (publicly available documents) contain information about the following mergers and amalgamation during the relevant periods.

Table-2 (Source: Annual Report of Quess for FY 2019-20)

The CA was required to obtain evidence of mergers or amalgamations that took place in Quess and the number of employees brought in therefrom before issuing the report in Form 10 DA. The working file for 2019-20 shows that the CA did not obtain such information from Quess. Accordingly, the CA was charged with failure to obtain sufficient & appropriate evidence and failure to exercise due diligence & professional skepticism before issuing the report in Form 10 DA in 2019-20.

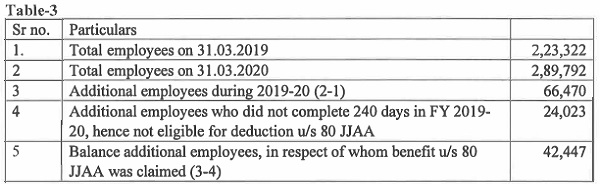

14. While denying the charge, CA Pawan Jain replied that he had verified these transactions (mergers/acquisitions/ amalgamations/ acquisitions), and Quess had not claimed any deduction in respect of additional employees of these entities, though employees of Aravon and MSSPL were part of the closing head count. This is contradictory to the working paper where MSSPL is not included in the head count. The Audit File does not contain any evidence in support of CA Pawan Jain’s statement that Quess had not claimed any deduction in respect of Aravon & MSSPL even though they were included in the head count. On the contrary, Table 3 shows that deduction had been claimed for the employees of Aravon & MSSPL. Table 3 shows that of the 66,470 additional employees in FY 2019-20, benefit under section 80 JJAA was claimed for 42,447 employees, excluding 24,023 employees who had not completed 240 days. As the employees of Aravon & MSSPL had completed more than 240 days (Aravon & MSSPL were merged with effect from 01.04.2019), it is obvious that the number of employees for whom the benefit was claimed included those of Aravon & MSSPL.

15. CA Pawan Jain had relied on para 1 and 2 of Management Representation Letter (MRL) dated 30.03.2021, which stated that “1. Business of the company is not formed by splitting up or the reconstruction of an existing business. 2. Business is not acquired by the company by way of transfer from any other person or as a result of any business reorganization”. The factual position is that eight companies were acquired during the period as mentioned in para 13 above. CA Pawan Jain did not obtain evidence on this matter, but simply relied on this MRL.

16. The above clearly prove the charge that CA Pawan Jain failed to obtain sufficient & appropriate evidence and failed to exercise due diligence & professional skepticism before issuing report in Form 10 DA in 2019-20.

II. Failure to exclude employees whose contribution was paid by the Government

17. Sub section 2 of section 80 JJAA of the IT Act, proscribes the deduction on account of employees, for whom the ‘entire contribution’ was paid by the Government under the Employees’ Pension Scheme under EPF&MP Act5.

18. While issuing reports in form 10 DA for FY 2018-19 & 2019-20, the CA did not exclude the number of employees in respect of whom Quess was already getting benefit of EPS under Pradhan Mantri Rojgar Protsaahan Yojana (PMRPY) scheme. Quess admitted to this incorrect claim in its Management Representation Letter (MRL) issued for FY 2020-21, intimating the CA that they had wrongly claimed deduction during FY 2018-19 & FY 2019-20. Accordingly, while claiming benefit in the Form 10 DA for FY 2020-2 1, the employee cost of such employees was reduced by Rs 128.35 crores for FY 2018-19 & Rs 8.09 crores for FY 2019- 20. The CA was charged with failure to obtain necessary information about such payments by the government & failure to perform any procedure in FY 2018-19 & FY 2019-20 to verify whether GOI was paying EPS contribution in respect of employees, whose employee cost was included while calculating and certifying the eligible employee costs for deduction.

19. The CA stated that “he was aware that certain ‘additional employees’ employed during the respective FY 2018-19 and FY 2019-20 were covered under the Scheme notified by the Govt. under the Employees Provident Fund and Miscellaneous Provisions Act 1952 ……… .

The samples selected for FY 2018-19 included those employees covered under the PMRPY Scheme but were qualifying as ‘additional employees’ as the contribution had not been paid by the Govt for the entire period ……. “.

He stated that the deduction u/s 80 JJAA was claimed on employees excluding those for whom the Government had paid the ‘entire contribution’, and in the case of M/s Quess Corp only a part of the contribution was paid by the Govt. for the employees, for whom the deduction was claimed. He referred to Annexure 2 of his reply as proof that he had verified on a sample basis.

20. On perusal of his reply along with Annexure -2 to his reply, containing a list of 7 employees with details of month wise PMRPY receipt, we find that in the initial one or two months of employment of new employees, the respective columns reflecting amount of PMRPY receipt from government are blank. This is because of the time lag in reimbursement of money by the Government as salary/wages are paid on the last day of the month or first week of next month and thereafter the claim is submitted to the Government. After processing the claim, the government- reimburses the money to the claimant. Section 80 JJAA does not use the words ‘entire period’. Therefore, in case “entire contribution” has been paid by the Government for a specific period, then also the Taxpayer is not entitled for deduction u/s 80 JJAA for that specific period. We note that the words ‘entire contribution’ used in sub section 2 of section 80 JJAA of the Income Tax Act means entire contribution payable under Employee Pension Scheme (EPS). As per EPS, 8.3 3% is paid by the employer and 1.16% is paid by the Central Government. However, to incentivize employment generation, under PMRPY scheme, the employer share is also paid by the Central Government. Therefore, the words ‘entire contribution’ refers to both 8.33% paid by employer and 1.16% paid by the Central Government. The CA has construed the words ‘entire contribution’ as ‘entire period’ which is far-fetched. The month wise statement submitted by the CA along with reply to SCN is an attempt to rationalize his negligence as such month wise details of PMRPY benefits received by Quess, are neither available in the Working Files nor is there any analysis of conclusion about “entire period” recorded in the Working Files.

21. On the basis of the above analysis, we conclude that professional skepticism was not exercised by CA Pawan Jain even while knowing that Quess was getting benefit of PMRPY in respect of additional employees. This, coupled with the admission by Quess of the mistake in the claim and its subsequent discontinuance and revision of the Form 10 DA by the CA himself proves that the CA was not diligent in issuing the said report dated 05.11.2019 for FY 2018- 19 and report dated 23.10.2020 for FY 2019-20, which was revised on 30.03.2021. This proves the charge against the CA.

III. Lapses in reporting additional employees during FY 2020-21

22. As per explanation to section 80 JJAA, additional employee cost shall be nil if there is no increase in the number of employees from the total number of employees employed as on the last day of the preceding year. Further, a proviso was inserted to explanation (ii) of subsection 2 of the section 80 JJAA by the Finance Act 2018 which reads as follows: “Provided further that where an employee is employed during the previous year for a period of less than two hundred and forty days or one hundred and fifty days, as the case may be, but is employed for a period of two hundred and forty days or one hundred and fifty days, as the case may be, in the immediately succeeding year, he shall be deemed to have been employed in the succeeding year and the provisions of this section shall apply accordingly”. Such employees are called as ‘spill over employees’ hereafter.

23. The total number of employees in Quess, as mentioned earlier, was 2,89,792 as on 31/3/2020 and 2, 70,596 as on 31/03/21 indicating a reduction of 19,196 in the total number of employees during FY 2020-21. However, the CA reported that Quess was eligible for deduction of Rs 140.57 crores u/s 80 JJAA in respect of 24,023 spillover employees of 2019-20. Therefore, even after considering 24,023 spillover employees, additional employees should have been considered as 4,827 (24,023-19,196).

24. The response of CA Pawan Jain was that Quess was eligible for deduction in respect of whole of 24,023 spill over employees without any adjustment due to the provisions of the second proviso to explanation (ii) of sub-section 2 of the section 80 JJAA.

25. We note that increase in the actual number of employees is fundamental to section 80 JJAA as is evident from:-

(a) Explanation (i) to said section that the additional employee cost shall be Nil if “there is no increase in the number of employees from the total number of employees employed as on the last day of the preceding year” ;

(b) Explanation (ii) to said section that “additional employee means an employee who has been employed during the previous year and whose employment has the effect of increasing the total number of employees employed by the employer as on the last day of the preceding year ….”. Explanation (ii) goes on to further list out those who will not qualify for new employees even if their employment has the effect of increasing the total number of employees. These new employees shall not be those drawing emoluments above Rs 25,000 per month; those whose entire contribution to EPS is met by the government; those employed for less than 240 days in the relevant FY; and those who do not participate in a recognized provident fund.

The second proviso to this explanation (ii) which the CA is relying on, merely states that when a new employee is employed for less than 240 days in one FY but is employed for 240 days in the subsequent FY, then he will be deemed to have been employed in the subsequent year and the provisions of the section shall apply. This does not automatically entitle spill over candidates and their eligibility will have to be evaluated in terms of all the provisions of section 80 JJAA of the Income Tax Act.

26. It is evident from the above analysis that there was an increase of only 4,827 number of employees during FY 2020-21 whereas the CA had certified deduction for 24,023 employees. Further, there is no analysis in the Working File about the increase in the number of employees on 31.03.2021 after considering spill over employees of the preceding year. In view of the explicit provision regarding the increase in the actual number of employees cited above, we find that the reply of the CA is not satisfactory.

IV. Failure to verify payment of additional employee cost by account payee cheque/draft/electronic means

27. As per explanation to section 80JJAA, additional employee cost shall be nil if emoluments are paid otherwise than by an account payee cheque or account payee bank draft or by use of electronic clearing system through a bank account. The CA was charged with failure to verify whether additional employee cost was paid through prescribed mode of payment during FY 2018-19, FY 2019-20 & 2020-21. The CA simply relied on MRL from Quess intimating that the additional employee cost was paid through prescribed mode of payment. The CA was charged with failure to obtain any evidence and failure to exercise due diligence & professional skepticism in this matter.

28. The CA replied that Quess makes salary payment in bulk and it is impossible to check payment to each and every additional employee; that he had relied on the Internal Financial Controls (IFC) framework in Quess and statutory auditors report on IFC; that the Quess payroll software is designed to function with minimal manual intervention; and that only minimal cash balance was maintained by Quess.

29. This reply is not supported by any evidence in the Working Files. The CA has not verified even a single case, to ascertain that salary was paid to an “additional employee” by way of an account payee cheque or account payee bank draft or by use of electronic clearing system through a bank account. Therefore, the basic requirement of the section enabling the company to claim the deduction was not verified by the CA while issuing the reports to enable claims under section 80 JJAA of the Income Tax Act. This constitutes gross negligence on the part of the CA.

V. Failure to verify salary limit of Rs 25,000 per month for new employees

30. The explanation (ii) to section 80 JJAA of lncome Tax Act states that “”additional employee” means an employee who has been employed during the previous year and whose employment has the effect of increasing the total number of employees employed by the employer as on the last day of the preceding year, but does not include

(a) an employee whose total emoluments are more than twenty-five thousand rupees per month;”

The section clearly mandates the exclusion of employees having total emoluments of more than Rs. 25,000/- per month. Accordingly, the CA was required to verify, inter alia, the employment contract (appointment letter) issued to new employees and verify payment records for determining total emoluments, before certifying the same in Form 10 DA. Examination of the Working Files shows that he did not verify even a single employee’s appointment letter or cross check the total emoluments received by him. The CA simply accepted the salary data provided by Quess and did not verify whether Quess had split the total emoluments into salary, allowances and reimbursable expenses, so as to keep the figure of salary below Rs 25,000 per month, in order to avail the deduction during FY 2018-19, FY 2019-20 & 2020-21.

31. The CA has replied that he relied on the salary data extracted from the Salary Master of the company having detailed breakup of various components of the salary. He further contended that there are several checks, controls & balances in place to ensure that there is no breach in the salary master software with very less manual intervention; that he had relied on the Internal Financial Controls (IFC) framework in Quess and statutory auditor’s report on IFC; that samples verified by him had no adverse findings, therefore, he had no reason to believe that there was manipulation in emoluments paid to employees. The CA further added that the impugned condition of Rs. 25,000 per month given under section 80JJAA should be read as a figure derived from an annualized condition and therefore if payment of emoluments in a particular month of the year breaches the limit of Rs. 25,000, it does not disentitle the concerned employee/s from definition of additional employees, if the emoluments paid to those employees does not exceed the annualized upper limit of Rs. 3,00,000. To substantiate his argument, the CA has referred to the case of Gujarat Co-operative Milk Marketing Federation Ltd (Gujarat Milk). (2020) 424 ITR 247 (Guj). On perusal, we find that this case is not relevant as Hon’ble High Court of Gujarat had set aside the aqditional tax levied by the Income Tax Department/Income Tax Appellate Tribunal; and the matter regarding calculation of monthly contribution per student was not commented upon by the Hon’ble High Court. In this case monthly contribution per student was calculated by the assessing officer based on annual contribution made by Gujarat Milk to Anandalaya Education Society, which imparts education to children of Gujarat Milk’s employees. Further, the CA referred to the case of Delhi Public School (DPS) (2012) 247 CTR 308 (P&H). On perusal of this case, we find that the facts of this case are not relevant as they pertain to deductibility of Rs 1,000/- per month (taken as Rs 12,000 per year) from the cost incurred by the employer for free education provided to the children of DPS’s employees; and the method of calculation was not commented upon by the Hon’ble High Court of Punjab and Haryana. Hence both the cases relied upon are not relevant to the facts of this case, as the Income Tax law is specific in its requirement for assessee to avail of the deduction under section 80JJAA.

32. The salary contract would be the appropriate document to peruse as it would give the breakup of pay, allowances and eligible reimbursements. All of this is necessary for determining whether the emoluments of the ‘additional employees’ are within the permissible threshold. The CA has given no reply in respect of verification of the employment contract (appointment letter) issued to new employees. The Working Files do not have evidence that (a) salary data were extracted from the Salary Master software of the company; and (b) controls testing done by the CA. Further, reliance on Internal Financial Control (IFC) and statutory auditors report in respect of employee benefit expenses is out of context as splitting of total emoluments into salary and reimbursable expenses may not have any impact on IFC and statutory auditors report. As a diligent professional, the CA was required to perform appropriate procedure to rule out the possibility of bifurcation of total emoluments to ensure that entire emoluments are considered while verifying this limit of Rs 25,000/-, which was not done. This point is corroborated from the analysis done by the Income Tax Department that Quess maintains the data of payments made to employees in two registers. The first register is ‘SALARY PAY REGISTER’ that includes the heads ‘gross salary’, all allowances, reimbursements etc., and second register is ‘OTHER INCOME REGISTER’ maintained as excel sheet that includes the remittances, incentives etc., paid to employees. The amount in other income register was not included by the company in total emoluments paid to employees for the purpose of claiming deduction u/s 80JJAA of lncome Tax Act 1961. However, there was no mention of ‘OTHER INCOME REGISTER’ in the Working Files submitted by CA. This shows a lack of due diligence on the part of CA. Therefore, we do not find the reply of the CA satisfactory.

33. From the paras I to V above, it has been established that CA Pawan Jain failed to obtain sufficient appropriate evidence and failed to exercise due diligence & professional skepticism before issuing report in Form 10 DA. He did not verify the basic conditions i.e., (a) excluding the additional employees of merged/amalgamated business; (b) excluding additional employees whose EPS contribution was paid by the Government; (c) whether there was increase in the total number of employees; (d) whether additional employee cost was paid by account payee cheque/draft/electronic means; and (e) whether total emoluments of additional employee was not more than Rs 25000 per month.

34. In addition to the above charges, there are many other conditionalities under section 80JJAA, which are required to be checked by the CA who certifies eligibility of the amount of Income Tax deduction to be claimed by the assessee company. These relate to ascertaining whether the new employees participated in a recognized Provident fund, whether there was no rehiring of old employees, and whether additional employees were employed for not less than 240 days. Besides these, there were deficiencies in sample testing done by the CA. The CA was charged with non-verification of the same. While denying all of these charges, the CA claimed that he had looked into these matters. As stated earlier, none of these are evidenced in the working file and therefore, we are unable to accept his defense.

D. Findings on the Articles of Charges of Professional Misconduct

35. The Income Tax Act, requires the accountant (in this case CA Pawan Jain) to provide a report/certificate in form 10 DA, to “certify” certain numbers based on which Quess would claim specific tax benefits. The certification requires utmost professional skepticism, due diligence and sufficient & appropriate evidence to ensure that the certificate is true and correct. However, as explained in the above paras, CA Pawan Jain has failed to exercise due diligence in ensuring the presence of the basic qualifying criteria to qualify for the tax benefit and obtaining sufficient appropriate evidence to support his certification. Thus, he was negligent in the conduct of his professional duties by not adhering to the scope of the work undertaken by him. As per sectioni 32(4) of the Companies Act, “Professional or other misconduct” shall have the same meaning assigned to it under section 22 of The Chartered Accountants Act 1949. Thus, failure of CA Pawan Jain to exercise due diligence and failure to obtain sufficient appropriate evidence resulted in the following professional misconducts within the meaning of Section 132 (4) of the Companies Act, 2013:

a) Failure to exercise due diligence in the conduct of professional duties (clause 7 of part-I of second schedule of The Chartered Accountants Act 1949),

This charge is proved that the CA Pawan Jain failed to exercise due diligence in the conduct of professional duties as explained in Section – C- I to V above.

b) Failure to obtain sufficient information which is necessary for expression of an opinion or its exceptions are sufficiently material to negate the expression of an opinion.(clause 8 of part-I of second schedule of The Chartered Accountants Act 1949).

This charge is proved as CA Pawan Jain failed to obtain sufficient information which was necessary to ensure that the report issued by him in Form 10 DA is true and correct as explained in Section – C – I to V above.

E. PENALTY & SANCTIONS

36. Section 132(4) of the Companies Act, 2013 provides for penalties in a case where professional misconduct is proved. The seriousness with which proved cases of professional misconduct are viewed is evident from the fact that a minimum punishment is laid down by the law.

37. The reports issued in form 10 DA under section 80 JJAA of the Income Tax Act have significant implication for Government Revenue. The Income Tax Act has trusted chartered accountants by giving them authority to certify certain claims of taxpayers. The chartered accountants have the responsibility to ensure that the amount of deduction certified in these reports are correct. They are required to exercise due diligence while performing such work so that the trust of the Government remains in the profession.

38. This Order has detailed the lapses by the CA in issuance of report/certificate in form 10 DA on the basis of which Quess claimed deduction u/s 80 JJAA of the Income Tax Act, 1961 of Rs. 113.86 crore, Rs.428.80 crore and Rs.428.16 crore during FY 2018-19, 2019-20 and 2020- 21 respectively. Thus, the work of the CA has major implications for revenue.

39. We find that CA Pawan Jain failed to exercise due diligence in the conduct of professional duties while certifying the information in form 10 DA based on examination of the relevant records. It has been proved that before issuing the reports, the CA did not obtain sufficient appropriate evidence with regard to compliance of conditions stipulated in section 80 JJAA for claiming deduction in respect of new employees.

40. Section 132(4)(c) of the Companies Act 2013 provides that National Financial Reporting Authority shall, where professional or other misconduct is proved, have the power to make order for

(A) imposing penalty of— (I) not less than one lakh rupees, but which may extend to five times of the fees received, in case of individuals; and (II) not less than ten lakh rupees, but which may extend to ten times of the fees received, in case of firms;

(B) debarring the member or the firm from—(1) being appointed as an auditor or internal auditor or undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate; or (11) performing any valuation as provided under section 247, for a minimum period of six months or such higher period not exceeding ten years as may be determined by the National Financial Reporting Authority.

41. As per information furnished by CA Pawan Jain, total remuneration and share of profit received by CA Pawan Jain is Rs Rs Rs and Rs during FY 2018-19, 2019-20, 2020-21 and 2021-22 respectively.

42. Considering the proved professional misconduct and keeping in mind the nature of violations, their impact on revenue and deterrence against future professional misconduct, we, in exercise of powers under Section 132(4)(c) of the Companies Act, 2013, hereby impose a monetary penalty of Rs fifty (50) lakhs only upon CA Pawan Jain.

43. This order will be effective after 30 days from the date of issue of this order.

(Dr Ajay Bhushan Prasad Pandey)

Chairperson

(Dr Praveen Kumar Tiwari)

Full-Time Member

(Smita hingran)

Full-Time Member

Authorized for issue by the National Financial Reporting Authority.

Date: 03rd January 2024

Place: New Delhi

(Vidhu Sood)

Secretary

Notes :

1. The Institute of Chartered Accountants of India.

2. EPS – Employees’ Pension Scheme

3. Rule 3 of the National Financial Reporting Authority Rules 2018 prescribes classes of companies and bodies corporate coming under its purview.

4. Previous year is corresponding financial year.

5. The Employees’ Provident Funds and Miscellaneous Provisions Act, 1952.