One of the main objective of GST was to eradicate cascading effect of taxes which existed under excise, VAT and service tax.

Under GST input tax credit can be claimed irrespective of place of supplier, thus making accessibility for sales and purchase of goods easier.

Amendment in Section 16

Eligibility and Conditions for taking Input Tax Credit

Budgetary Amendment (Effective date to be notified)

Section 16 (1)……

(2) Notwithstanding anything contained in this section, no registered person shall be entitled to the credit of any input tax in respect of any supply of goods or services or both to him unless, ––

(a) he is in possession of a tax invoice or debit note issued by a supplier registered under this Act, or such other tax paying documents as may be prescribed;

(aa) the details of the invoice or debit note referred to in clause (a) has been furnished by the supplier in the statement of outward supplies and such details have been communicated to the recipient of such invoice or debit note in the manner specified under section 37;”.

SECTION 16(1)

Every registered person shall,

subject to such conditions and restrictions as may be prescribed and in the manner specified in section 49,

be entitled to take credit of input tax charged on any supply of goods or services or both to him

which are used or intended to be used

in the course or furtherance of his business

and the said amount shall be credited to the electronic credit ledger of such person.

Section 2(94) of the CGST Act, 2017 – “registered person” means a person who is registered

under section 25 but does not include a person having a Unique Identity Number

Section 2(62) of the CGST Act, 2017 – “input tax” in relation to a registered person, means the CGST, SGST, IGST or UTGST charged on any supply of goods or services or both made to him and includes-

(a) the IGST charged on import of goods;

(b) the tax payable under reverse charge mechanism but does not include the tax paid under the composition levy.

Section 2(19) of the CGST Act, 2017 “capital goods” means goods, the value of which is capitalised in the books of account of the person claiming the input tax credit and which are used or intended to be used in the course or furtherance of business;

Intend means to have in one’s mind as a purpose or a goal. It is therefore a state of mind which can never be proved as a fact but can only be inferred from the facts which are proved.

Case Law: SAIL v. CCE (1996) 4 SCC 163

Facts: SAIL’s Rourkela plant manufactures fertilizers for which raw naphtha is used. Raw naphtha was, at the relevant time, excisable at a concessional rate of duty. The concessional rate of duty was admissible provided that such raw naphtha is intended for use in the manufacture of fertilizer. Because of supervening circumstances, namely, the low, uncertain and fluctuating availability of power, the reformed gas produced from naphtha during the interim stage of manufacture had to be vented out and was not used in the manufacturing of fertilizer.

Decision: The expression “intended for use” as occurring in the exemption notification would mean that the raw naphtha was ‘intended for use’ in the manufacture of fertilizer and not that it was actually used for the same. The benefit of the exemption notification is, therefore, available to SAIL in regard to the raw naphtha that it utilized in its plant for the manufacture of fertilizer but which, for reasons over which it had no control, did not, in fact, result in the manufacture of fertilizer but had, at the interim stage of reformed gas, to be vented out.

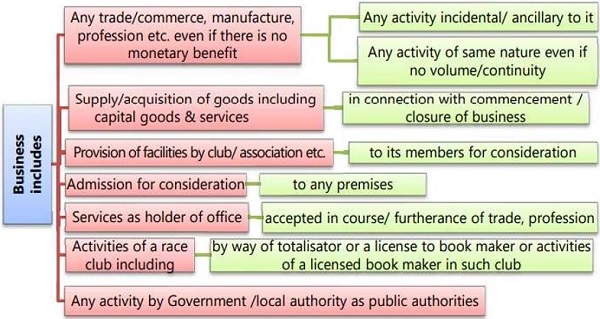

SECTION 16(1) IN THE COURSE OF FURTHERANCE OF BUSINESS CERTAIN CASE LAWS

State of Tamil Nadu Vs Burmah Shell Oil Storage and Distributing Co. of India Ltd. And Anr.; AIR 1973 SC 1045 Where the primary business of the Petitioner was trading in oil and oil related products it was held that periodic selling of scrap, unserviceable oil drums, old furniture, etc. was an activity ancillary and incidental to its business.

Hindustan Zinc Limited Vs. Commercial Tax Officer 1990 WLN (UC) 220 Where the main business of the Petitioner was manufacture and dealing of non-ferrous items, it was held sale of tender forms was an activity which was ancillary and connected to its business

United India Insurance Co. Ltd. Vs. Commissioner of Commercial Taxes, Bangalore and Anr. 1986 (2) KarLJ107 The petitioner was carrying its business in General Insurance and was selling used goods received against settlement of claim. The activity of selling used goods was held to be ancillary to its main business.

Citi Bank Vs. Commissioner of Sales

Tax 2016 IAD (Delhi) 581 The petitioner was engaged in banking business and in certain cases would recover dues from the defaulters, by auctioning of assets of the defaulters. The activity of selling of assets hypothecated to the bank was held to be incidental to its business.

Basic Conditions for Claiming Input Tax Credit (ITC)

The following requisites are mandatory for claiming input tax credit under GST

- One must be registered under GST Law

- A tax invoice or debit note issued by the registered supplier showing the tax amount

- Goods or services must have been received

- Supplier should have filed returns and paid such tax thereon to the government

- Where goods are received in parts or in instalments, ITC maybe claimed on receipt of last lot or instalment.

- Where input tax credit is included in the cost of capital goods and depreciation on such tax is claimed, no input tax credit is allowed.

- Input tax credit will not be allowed if the same has not been claimed within the prescribed time limit.

REQUIRED DOCUMENTS FOR CLAIMING ITC

A registered dealer can claim input tax credit on the basis of following documents

1. A tax invoice issued by registered supplier

2. A debit note issued in respect of earlier issued tax invoice by the registered supplier.

3. An invoice issued by the recipient of goods or services who has paid tax under reverse charge mechanism

4. A bill of entry or similar document in case of imports.

5. An invoice or credit note issued by an Input Service Distributor.

REVERSAL OF INPUT TAX CREDIT

Input tax credit may be reversed under certain circumstances as mentioned below –

- Failure to pay supplier within 180 days from the date of invoice.

- Goods and services whether inputs or capital goods used for personal purpose.

- Goods and services utilized for producing or supplying exempted goods or services.

- Sale of capital goods or plant and machinery on which input tax credit was claimed.

- Credit note issued by input service distributor.

- Supplies ineligible under section 17(5) of the Act.

- Transition from registered regular dealer to composite dealer

Where input tax credit (ITC) is reversed,

The amount reversed may be added to output tax liability in the month in which it is reversed,

Interest shall be paid from the date of availing credit till the date when the amount is reversed and paid

No time limit shall be applicable for reclaiming the reversed credit.

How To Avail Credit Where Tax Has Been Paid Under Reverse Charge Mechanism (RCM)

Where tax has been paid under reverse charge basis, input tax credit may be availed in the same month in which the payment is made, provided the following condition is satisfied –

(1) Liability has been discharged through cash

(2) Goods or service has been used for business purpose

(3) Self-invoicing is done on such purchases as no tax invoice can be issued by unregistered supplier

Time limit for claiming Input Tax Credit (ITC)

Input tax credit can be claimed against an invoice/ debit note or credit note before the end of the following dates, whichever is earlier –

1. Due date of GST return filing

for the month of September of the next financial year

2. Date of filing annual return for that financial year. For the FY 17-18, period to be claimed ITC was extended to March 2019.

However, if no credit has been claimed till filing return of March 2019, any such credit will lapse and cannot be claimed even through GSTR 9 annual return.

Thus, it can be understood that no Input tax credit can be claimed through GSTR 9 annual return if the same is not claimed through other GST returns.

Special Circumstances in which ITC may be claimed

As per section 18 of the CGST Act, input tax credit may be claimed in certain special circumstances –

Availability of input tax credit in case of compulsory registration.

Availability of input tax credit in case of voluntary registration

Availability of input tax credit when the registered person ceases to be applicable for composition scheme.

Availability of input tax credit in case exempted supplies become taxable

Availability of input tax credit in case of change in constitution

Ineligible Input tax credit or items where ITC is not allowed

Purchase of motor vehicles or conveyances. However, there are certain exceptions to it.

Any expense including insurance of motor vehicles or conveyances mentioned above.

ITC on food, beverages, outdoor catering services, beauty treatment, health services, cosmetic and plastic surgery

Sale of membership of health and fitness centre, clubs

ITC on rent a cab, life insurance, health insurance

Travel benefits extended to employees

ITC on works contract services availed for construction of immovable property, including goods and services used for construction for immovable property (except plant and machinery).

ITC on purchases by registered person opting for composition scheme.

Goods or services used for personal consumption

ITC on goods stolen, lost, destroyed, written off or given as free samples.

ITC on tax paid due fraud cases.

SET OFF CREDIT OF ITC

From 1st July 2019, GSTN portal has been updated with new system of ITC utilisation. ITC can be utilised in the manner described below.

- IGST credit should be fully utilised first.

- In case of CGST liability, CGST credit is to utilised first and then IGST credit. However, one must take into consideration that no IGST credit is pending

- In case of SGST liability, SGST credit is to utilised first and then IGST credit. However, one must take into consideration that no IGST credit is pending

- CGST credit cannot be utilised against setting off SGST liability and vice versa, SGST credit cannot be utilised to set off CGST liability.

- The main aim while setting off input tax credit against tax liability is to have minimum tax pay-out after complying with all provisions of the act.

Time limit for claiming ITC under GST

GSTIN has specified a time-limit to claim the Input Tax Credit.

As per Section 16(4) of the CGST Act 2017, taxpayers can claim any pending ITCs for any particular month, till the September of the subsequent year or while filing the annual return GSTR-9 for the financial year in which the Input Tax Credit has been availed.

Any pending ITC post this period will collapse & you will not be allowed to utilize it in any way to release any tax liabilities.

However, it is recommended to claim the ITC in real-time that is to claim ITC on a monthly basis via form GSTR-2B Reconciliation & GSTR-3B.

The ITC claiming time limit must be kept in mind by the accountants especially while dealing with complex transactions such as Imports & SEZ transactions.

Refund of Input tax credit under GST

Refund of Input Tax Credit under GST comes in three forms, that is there are three cases under which a taxpayer can claim the refund of the ITC in their electronic credit/cash ledger

Following are the three cases under which taxpayers can claim the refund of ITC-

Refund of unutilized Input Tax Credit (ITC) on account of Exports without the payment of integrated tax.

Refund of unutilized input tax credit (ITC) on account of goods or services supplied to SEZ Unit/ SEZ Developers without the payment of integrated taxes.Refund of unutilized ITC on account of accumulation due to the inverted tax structure, where the input tax is more than outward tax liabilities.

Input tax credit rules under GST

There are a few rules & conditions that taxpayers need to keep in mind while claiming ITC under GST.

We have simplified them & broken them down for you in a list below-

180 Days Rule

The buyer of the goods who is claiming the ITC must make the complete payment to the supplier within 180 days from the date of supply in order to claim ITC . If the buyer fails to do so, then their credit availed will be added to their outward tax liability.

Time Limit of claiming ITC

ITC can be claimed by the taxpayer EITHER till the GSTR filing of September of the subsequent year OR in the annual return filing of form GSTR-9

Possession of Documents

The taxpayer who is willing to take ITC must possess the invoices & other supporting documents with him, such as Credit & Debit Notes

Receiving the Goods

The receiver of the goods & services must have received the same within 180 days from the date of the invoice.

Provisional ITC under GST

As per the 10% Provisional ITC rule, if your supplier fails to furnish the invoices in their GSTR-1 & it does not appear in your GSTR-2A you will not be able to claim full ITC on such transactions.

Instead, you will be eligible only for an additional 10% of the actual ITC mentioned in your GSTR-2A.

ITC on Capital Goods

You cannot claim ITC on the capital goods if you have already claimed depreciation on the same. You can opt for either of the two but not both.

Goods Received in Instalments

In case you are receiving the goods in lots or instalments, then you will only be eligible for ITC when the last & final instalment is received by you.

ITC on Debit Notes

Customers can claim ITC based on Debit Notes created against an Invoice.

ITC, in case of Credit Note Generation

Using a Credit Note, the supplier can reduce their tax liabilities.

In this case, the recipient will have to reverse the ITC that they have claimed as Credit Notes nullify the transactions.

ITC on Import of Goods

While claiming ITC on imports, you must furnish- The bill of entry & The IGST payment challan.

Deposition of Taxes to the government

You must ensure that the GST that you have paid to the supplier reaches to the Government vis GST returns.If the tax doesn’t reach the Government, you may not be able to claim full ITC of the same

Common Credit of ITC under GST

Common Credits can only be claimed in the following 2 cases-

- Effecting exempted and taxable supplies

- Business and non-business related activities

What is meant by ineligible ITC?

There are certain cases Where Input Tax Credit under GST Cannot Be Availed, this is called ineligible ITC under GST.

We have listed down the cases that are ineligible for claiming Input Tax Credit under GST, if taxpayers claim the credits of these items/services they can be liable –

- ITC on purchase of Motor vehicles and conveyances (for personal use, and for motor vehicles with seating capacity up to 13 persons, purchase of aircraft & vessels)

- No ITC on account of detention, seizure, and release of goods and conveyances in transit. (Section 129)

- General insurance, servicing, repairs, and maintenance of vehicles & vessels

- Vessels & Aircraft, however, there are a few exceptions where ITC is allowed for the same.

- Supply of food, beverages, club memberships, beauty treatment, surgery, etc for personal use or office parties

- No ITC allowed on payment of late fees, penalties, interests, etc.

- No ITC on tax paid on account of confiscation of goods or conveyances and levy of penalty (section 130)

- ITC availed by means of a fraud or scam under section 74 of the CGST Act 2017.

- Goods & Services purchased for exempted supplies.

- Membership of a club, Gym, Beauty club, health, and fitness center

- Life & Health insurance

- Travel for personal or business purposes, vacations, holidays, etc. where LTA is provided to the employees (unless obligated

- Free Samples, gifts, lost stolen and destroyed goods

- Working Contract (for construction of properties)

- Leasing, Renting, Hiring Vehicles for other than specified purposes.

- Construction of immovable property for personal use

- Purchase from Composition Scheme

- Good & Services received by a Non-resident

- Goods & Services for Personal Consumption.

Input tax credit on capital goods

There are four types of Capital Goods in businesses & here is how ITC works on them-

Capital Goods only for Personal Use: No ITC available

Capital Goods only for Exempted Sales: No ITC available

Capital Goods only for Normal Taxable Sales- ITC available per usual

Capital Goods for both personal/ exempted AND for Normal Sales:

Calculate proportionate ITC depending on the ratio in which the goods are used for personal & business purposes.

Note- ITC can only be claimed on Capital Goods, when depreciation has not been claimed on them. Meaning you can either claim ITC or depreciation on Capital Goods.

Credit Reversal of input tax credit under GST

Payment the supplier within 180 days from issue of invoice

Inputs and capital goods must not be used for personal purposes

Inputs and capital goods must not be used for providing exempt supplies

Credit Notes issued by seller to ISD (Input service distributor)

When the reversed ITC is less than required

This reversed ITC needs to be furnished in the recipients GSTR-2. Additionally, the reversed ITC will add up to the total outward data.

Note- ITC can be declared in Table 11(2) of Form GSTR-2

Note- the recipient will have to pay these reverse charges & their taxes for the ITC availed earlier

Input Tax Credit in case of Imports

Under the GST Regime, the input tax credit of IGST and GST Compensation Cess is available to the importer. However, the input tax credit of Basic Customs Duty (BCD) would not be available.

In order to avail ITC of IGST and GST Compensation Cess, an importer has to mandatorily declare GST Registration number (GSTIN) in the Bill of Entry.

The Customs EDI system would be inter-connected with the GST portal for the validation of ITC. Bill of entry in the non-edi locations would be digitized and used for validation of input tax credit provided by the GST portal.

AMENDMENTS AND IMPORTANT JUDGEMENTS ON ITC UNDER GST

> Rule 36(4) (inserted vide N.N. 49/2019-CT) provided statutory backing to the most disputed CGST Rules.

> This provision would give force to entries appearing in GSTR 2A/ 2B as a valid proof of supply.

> To put end to litigation, regarding Legal sanctity of Rule 36(4) which was challenged being ultra vires the Act in various Writ Petitions.

> To overcome in a way to pre-GST legal jurisprudence that supports the view that as long as the purchasing dealer has taken all the steps required for being eligible for ITC, he could not be expected to keep track of whether the selling dealer has in fact deposited the tax collected with the government or has lawfully adjusted it against his output tax liability .

> To overcome Fake Invoicing issues, when read in conjunction with other Amendments pertaining Suspension of GSTN in case of mismatch of ITC in returns as per GSTR 2A/2B and blocking on non filing of GSTR 1.

-

- The proposed amendment although giving force to Rule 36(4), but somewhere challenging the leverage of Additional 5% as provided by the Rule.

- Asking the impossible: – The above provision leads to controls the action of supplier by the recipient, thereby overruling the past decisions like Arise India. Ltd (Delhi HC), Kay Kay Industries(SC), On Quest Merchandising India Pvt. Ltd. (DHC), Gheru Lal Bal Chand(P&H) where it was held to be unreasonable.

- The amendment being prospective in nature, the validity of Rule 36(4) prior to its insertion is highly disputed.

Important judicial pronouncement on input tax credit from 2019

Held: –

Where assessee filed refund claims under provisions of section 54(3) and Competent Authority issued on assessee deficiency memo under Form GST RFD03 pointing out several deficiencies, assessee was entitled to re-credit of refund amount on basis of Form GST RFD-03 issued by Competent Authority in its Electronic Credit Ledger

Issue:-

Whether credit is available on input tax paid on lease rent during pre-operative period for the leasehold land on which the resort is being constructed to be used for furtherance of business, when the same is capitalized and treated as capital expenditure

Held: –

The Appellant acquired land from the WBHIDCL on lease paying an upfront amount as premium and a yearly lease rental @10% onthe premium with an escalation clause from the third year of lease. The premium paid by the Appellant is exempted under Sl. No. 41 (SAC 9972) of Notification No. 12/2017-CT(Rate) dated 28.06.2017, as amended vide Notification No. 32/2017-CT (Rate) dated 13.10.2017 and Notification No. 23/2018-CT (Rate) dated 20.09.2018. Whereas lease rental paid by the Appellant is taxable under SI. No. 16 (iii) (SAC 9972) of Notification No. 11/2017- CT(Rate) dated 28.06.2017, as amended vide Notification No. 1/2018-CT (Rate) dated 25.01.2018. Lease premium and lease rental both are parts of the project cost, the former being one-time fixed amount and the latter being a variable cost. Both lease premium and lease rental are classified under SAC 9972 being Real Estate Services. As the lease premium paid by the Appellant is exempted under Sl. No. 41 of the Rate Notification under GST Act on satisfaction of stipulated criteria the question of availing input tax credit does not arise. So the moot question is whether input tax credit on lease rental paid is available in the pre-operative period. It transpires from the above discussion that the Appellant is constructing the Eco Resort on his own account in course of furtherance of its business of providing hospitality service, for which one of the input service availed is lease rental service. The ambit of the blocked credit as per clause (d) of sub-section (5) of section 17 is broad as it includes such goods or services or both when used in the course of furtherance of business. So clause (d) of sub-section (5) of section 17 restricts the Appellant from availing input tax credit on lease rental paid.

44. Section 16 – “Eligibility and Conditions for taking Input Tax Credit”

In Re: Assistant Commissioner, CGST & CX (2018) 69 GST 783 Appeal Case No. 05/WBAAAR/APPEAL/2018 Decided On: 27.09.2018

Issue:-

(a) whether the transfer of goods (optical lenses and frames for spectacles and accessories) from Head Office in West Bengal to its branches in other states, can be done at cost price, by applying the Second Proviso to Rule 28 of CGST Rules, 2017 (instead of 90% o MRP as required under the First Proviso to Rule 28 of CGST Rules, 2017, and

(b) what is meant by the expression “where the recipient is eligible for full input tax credit” as used in the Second Proviso to Rule 28 of CGST Rules, 2017.

Held:-

From a plain reading of law laid down under section 16 of the GST Act, it is clear that, inter alia, input tax credit is available only when the recipient is in possession of a tax or debit note issued by the supplier registered under the GST Act, and in case of a supply between distinct and/or related persons, as between Head Office and Branches, the value declared in the invoice shall be deemed to be the open market value of the goods or services supplied. It is therefore clear that if the value declared in such invoice is zero no input tax credit is available to the recipient. It is seen that the question raised by M/s. GKB Lens Pvt. Ltd. was correctly answered by the Authority of Advance Ruling. However, it may be clarified that no input tax credit is available to the recipient of goods/service if the value declared by the supplier in the invoice/debit note is zero. In the facts and circumstances discussed above the Ruling of the West Bengal Authority of Advance Ruling is modified to the extent that at the end of the second paragraph of the said ruling the following sentence will be added: “No input tax credit, however, would be available for supply of goods/services at Zero Value.”

Nagaur Mukundgarh Highways (P.) Ltd., In re [2019] 103 taxmann.com 212 (AAAR-Rajasthan) Order No. RAJ/AAAR/06/2018-19 February 12, 2019

Held:-

Where Government of Rajasthan has awarded to applicant a works contract for construction of road on DBOT basis and State Government has also awarded work of Operation and Maintenance (O & M) of said road for a period of 10 years, only 50 per cent ITC of GST paid on Input and Input service used in construction phase and full ITC of GST paid on inputs and input services used in O&M phase is available to appellant subject to provisions of section 17(5)

49. Section 17 – “Apportionment of Credit and Blocked Credits”

Facts:-

It is an undisputed fact that the activity of letting out the units of the shopping mall attracts CGST and OGST on the amount of rent received by the petitioner No.1 because the activity of letting out the Units in the said Mall amounts to supply of service under the GGST Act/OGST Act. The petitioner No.1 having accumulated input Credit of GST amounting to Rs 34,40,18,028/-(Rupees thirty four crores forty lacs eighteen thousand twenty eight only) in respect of purchases of inputs in the form of goods and services is desirous of availing of the credit of input tax charged on the purchase/supply of goods and services which are consumed and used in the construction of the said shopping mall in order to utilise the said input credits to discharge and pay the CGST and OGST payable on the rentals received by the petitioner no. 1 from , the tenants of the said shopping mall and approached the revenue authorities in this regard. However, the petitioner no. 1 was advised to deposit the CGST and OGST collected without taking input credit in view of restrictions placed as per Section 17(5)(d) and was warned of penal consequences if it did not do so.

Held:-

The very purpose of the Act is to make the uniform provision for levy collection of tax, intra state supply of goods and services both central or State and to prevent multi taxation. Therefore, the contention which has been raised by the learned counsel for the petitioners keeping in mind the provisions of Section 16 (1)(2) where restriction has been put forward by the legislation for claiming eligibility for input credit has been described in Section 16(1) and the benefit of apportionment is subject to Section 17(1) and (2). While considering the provisions of Section 17(5)(d), the narrow construction of interpretation put forward by the Department is frustrating the very objective of the Act, inasmuch as the petitioner in that case has to pay huge amount without any basis. Further, the petitioner would have paid GST if it disposed of the property after the completion certificate is granted and in case the property is sold prior to completion certificate, he would not be required to pay GST. But here he is retaining the property and is not using for his own purpose but he is letting out the property on which he is covered under the GST, but still he has to pay huge amount of GST, to which he is not liable.

In that view, of the matter, in our considered opinion the provision of Section 17(5)(d) is to be read down and the narrow restriction as imposed, reading of the provision by the Department, is not required to be accepted, inasmuch as keeping in mind the language used in [1999] 2 SCC 361 (supra), the very purpose of the credit is to give benefit to the assessee. In that view of the matter, if the assessee is required to pay GST on the rental income arising out of the investment on which he has paid GST, it is required to have the input credit on the GST, which is required to pay under Section 17(5)(d) of the CGST Act.

2021 (3) TMI 1020 – [MADRAS] M/S. D.Y. BEATHEL ENTERPRISES

Input Tax Credit (ITC) – Liability of tax on petitioners – petitioners believes that the tax had already been5remitted to the Government by their sellers – petitioners could not furnish any proof for the payment of tax –

HELD THAT: –

- The assessee must have received the goods and the tax charged in respect of its supply, must have been actually paid to the Government either in cash or through utilization of input tax credit, admissible in respect of the said supply –

- if the tax had not reached the kitty of the Government, then the liability may have to be eventually borne by one party, either the seller or the buyer.

- In the case on hand, the respondent does not appear to have taken any recovery action against the seller / Charles and his wife Shanthi, on the present transactions.

When it has come out that the seller has collected tax from the purchasing dealers, the omission on the part of the seller to remit the tax in question must have been viewed very seriously and strict action ought to have been initiated against him.

- That apart in the enquiry in question, the Person who supplied / sold the goods, ought to have been examined. They should have been confronted. – This is all the more necessary, because the respondent has taken a stand that the petitioners have not even received the goods and had availed input tax credits on the strength of generated invoices. The matters are remitted back to the file of the respondent – petition allowed by way of remand.

*******

Author Name: M.S. VIJAYAKUMAR

Qualification: M.COM. B. ED.M.B.A.M. PHIL.HDNC.,

OCCUPATION: ASSISTANT COMMISSIONER GST (RETD.)

Location: MADURAI TAMILNADU Author can be reached in 9442022874; 8838052001; mail4rvijay@gmail.com sva_vijay@yahoo.com

The author has more than 30 years of Experience in the state commercial/GST department The author is interested in giving lectures on taxation, management, accounting AND other motivational areas. Wrote articles in a e-journal published from Hyderabad. Delivered lectures on Tamilnadu General Sales Tax Act CST Act Entertainment Tax ACT VAT ACT. Master trainer on GST and delivered lectures on GST in all areas to Officers and gave lectures on GST in various Arts and Science Colleges in tamilnadu. He is also a part time faculty in the Department of Management Studies/Commerce in Madurai Kamaraj University since 1998.have attended various GST webinars, zoom meeting conducted by various NIRC’s voice of CA, and different forums.

Author Bio

Informative Article well Explained

.Thanks

Excellent Article. Thanks for Sharing.