SEBI Consultation Paper

Designing a Framework for Enhanced Market Borrowings by large Corporates

1. Budget Announcement and its objective

1.1. Government of India in the Union Budget of 2018-19, made the following announcement:

“SEBI will also consider mandating, beginning with large Corporates, to meet about one-fourth of their financing needs from the debt market.”

1.2. A series of steps have been taken, over time, by Government in consultation with Regulators, to develop and deepen the bond market. At the same time, however, concerns have been raised about the ability of banks to finance increasing borrowing needs of the corporates, especially as the investment cycle has shown an upward tick. Accordingly, the said budget announcement may be seen as a step in the direction of the larger goal of not only to reduce reliance on banks to finance corporates but also to develop a liquid and vibrant corporate bond market.

2. Evolving a framework for operationalising the intent of budget announcement

2.1. Evolving a framework for operationalising the extant budget announcement may require identification of the meaning and scope of the terms “large corporates”, “financing needs” and “mandate”, which have been used therein. The same are discussed as under:

a) Identifying large corporates and their financing needs: The intention of the budget announcement is to nudge corporates (who have borrowing needs) to access the bond market. Accordingly, a large corporate could be one who;

i. has a certain threshold of outstanding borrowings;

ii. has a reasonable credit rating;

iii. intends to finance itself with long-term borrowings (i.e. borrowings above 1 year);and

iv. has listed its securities on the stock exchange.

b) What constitutes mandate: Given the current stage of development of bond market in India, any mandatory requirement would need to be light-touch in nature and would also need to provide enough leeway to the identified corporates to meet the mandatory requirement from the bond market.

3. Current market structure and inference drawn therefrom

3.1. Some of the measures that have been taken for the development of bond market includes: mandatory reporting requirement of OTC trades in bonds and dissemination of the data in public domain, setting up of dedicated debt segment on exchanges, uniformity in market conventions, electronic bidding platform for private placement, consolidation of debt ISINs etc. These measures have resulted in an uptick in the share of bond market to total corporate credit. The budget announcement, as above, is a further step towards deepening the bond market.

3.2. Before, however, arriving at the granular level details of the operational framework underpinning the Budget announcement, it is important to understand the bond market micro-structure and the lessons that can be learnt for framing the operational framework.

Bank Financing Vs. Bond Financing:

3.3. Chart1 below shows the percentage share of bank and bond financing to corporate sector over a period of 5 years. As is seen, the share of bond market in comparison to bank financing has seen a steady growth. Further, FY 2016-17 was a watershed year when share of bond market financing overtook that of bank financing.

Chart 1 – Percentage share of bank borrowing and bond borrowing in corporate

credit

Source: CARE Ratings, SEBI

Credit rating profile of issuers:

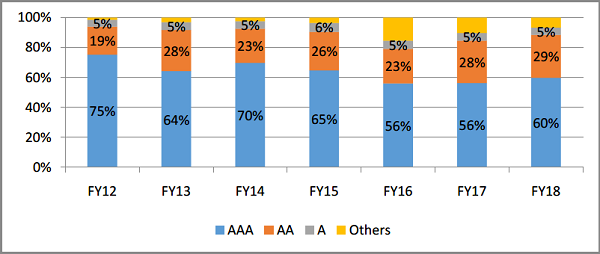

3.4. If we catalogue the primary issuances of listed corporate bonds, across multiple years, in different rating buckets, it is seen that the majority of the issuances is skewed towards credit rating of “AA” and above. Chart 2 below represents the bonds issued in different rating categories.

Chart 2: Proportion of corporate bonds issuances in different rating categories

Source: CRISIL

3.5. As can be seen from the chart above, around 90% of the issuances happen in credit rating bucket of “AA or above”.

3.6. One of the primary reasons for a high concentration of issuance in paper rated “AA and above” is because institutional investors, who are the largest investors in bond market, invest primarily in highly rated paper. With a view to address this issue, the budget of 2018-19 has made the following announcement:

“Corporate debt securities rated ‘BBB‘ or equivalent are investment grade. In India, most regulators permit debt securities with the ‘AA‘ rating only as eligible for investment. It is now time to move from ‘AA‘ to ‘A‘ grade ratings. The Government and concerned Regulators will take necessary action.”

3.7. The operationlisation of this budget announcement is likely to facilitate even lower rated borrowers (borrowers rated between AA – and A) to raise funds from the bond market.

3.8. Apart from the above, the rating profile of corporates could be further augmented by providing credit enhancement facilities. This is especially relevant for companies in the infrastructure sector as generally they have a lower rating. With a view to improve the credit rating of infrastructure companies, the Union Budget of 2016-17 had made an announcement regarding credit enhancement/guarantee to the debt securities issued by such infrastructure companies. Once this announcement is operationalized, it would help infrastructure companies to further access institutional funding from the bond market.

Issuers and issuance types:

3.9. An analysis of issuers and issuances is shown in Charts 3 and 4 below.

Chart 3 – Issuer wise breakup of bond issuances

Source: CRISIL

Chart 4 – Manner of issuance of Listed Corporate Debt Securities

Source: SEBI

3.10. As per the above charts, corporate bond issuance is done primarily through private placement route. Further, almost 60-70% of the total issues are done by financial sector entities and the private sector non-financial entities constitutes only around 20 % of the total issuances.

3.11. A deeper examination of the reasons for the above trend reveals that financial sector companies, including NBFCs doing private placement, have been exempted from the requirement of maintenance of Debenture Redemption Reserve (DRR), while all issuances by non-financial entities and entities doing public issue are required to set aside a part of their profits (equivalent to 25 % of the value of outstanding debentures) as DRR. Further, such companies have to investatleast an amount equivalent to 15% of the debentures maturing during the year in bank deposits, government securities, etc. Such an earmarking of funds imposes an opportunity cost on the issuer.

3.12. As the requirement of DRR maintenance imposes a significant cost on public issue of bonds and on bonds issued on private placement basis by non-financial corporates, and given that issue of protection of bond investors, in cases of default, has been significantly addressed by the enactment and operationalisation of Insolvency and Bankruptcy Code (IBC), it is felt that if the requirement of DRR is dispensed with, it will naturally facilitate more corporates to access the bond market for their financing needs.

RBI Policy framework on Large Exposures

3.13. With a view to address concentration risk in the banking system, RBI has come out with a policy framework on banks’ large exposures.

3.14. The framework involves mandating enhanced provisioning norms for banks’ exposure to large borrowers. These enhanced provisioning norms have come into effect from the FY 2018-19 and shall be applicable on incremental lending made to borrowers with Aggregate Sanctioned Credit Limit (ASCL) of INR 25,000 crores in FY 2017-18. Further, the ASCL limit for application of the extant norms will be gradually reduced and it will be INR 10,000 crores beginning FY 2019-20. These measures are expected to result in corporates further accessing the bond market but the impact of these measures is yet to be assessed.

Implementation of IBC:

3.15. The coming into force of IBC in 2016 has addressed the default risk of bonds to a large extent as the bond holders have been kept on higher priority than even Government dues in the liquidation waterfall. It is expected that, in the medium term, this would facilitate deepening of bond market. As per Bank of International Settlement (BIS) data, implementation of bankruptcy reforms have significant impact on deepening of bond market in countries which have implemented such reforms. For example, the corporate bond as a percentage of GDP increased from 12.7 % to 26.3 % in Brazil, 8.1 % to 13.1 % for Russia, 18.8 % to 33.4 % in China and 68.4 % to 106.8 % for U.K. over the 5 year period from the year of reform. For India, at present, the share of corporate bond to GDP is approximately 17 % and if the trend is the same as that seen in other countries, then it can safely be presumed that the bond market to GDP should move from the current 17 % to at least 22 – 23 % by 2022-23, just on account of successful implementation of IBC.

3.16. From the above bond market micro-structure, the following can be inferred –

a) The share of bond market in comparison to bank financing has shown an upward trend and currently both these modes have almost an equal share. It is expected that the share of bond market would get further accentuated in coming years.

b) A large proportion of issuances happen in the credit rating bucket of “AA and above”.

c) Most of the bond issuances are privately placed with financial sector companies accounting for a major share of such placements.

d) Dispensing the DRR requirement for non-financial entities and entities doing public issue could facilitate more such companies to access the bond market.

e) The budget announcements regarding shifting to the credit rating bucket of “A and above” and regarding credit enhancement / guarantee to the debt securities issued by infrastructure companies, once operationalized, could give additional boost to the bond market.

3.17. As for the headwinds which may impact the growth of bond markets, it may be noted that during the last year, as a result of various factors (including global factors), there has been a hardening of G-Sec yield by almost 120-130 bps. Evolving global scenarios, depreciation of Rupee, etc could add further uncertainty to the level and direction of the long term yields. This could impact the appetite of borrowers to access the bond market.

4. Proposal

Considering the above, the regulatory intent would be to operationalize the budget announcement in a manner which provides for a light touch framework and at the same time provides an appropriate timeframe to the market for smooth transition to the new framework. Accordingly, following is proposed:

4.1. Applicability of framework – The framework shall be applicable to any corporate (except for scheduled commercial banks), which as on March 31stof an year:

a) has an outstanding long term borrowing of Rs 100 crores or above; and

b) has a credit rating of “AA and above”;and

c) intends to finance itself with long-term borrowings (i.e. borrowings above 1 year); and

d) its securities (specified securities or debt securities or non-convertible redeemable preference share) listed in terms of Chapter IV, V or VI of SEBI(Listing Obligations and Disclosure Requirements) Regulations, 2015.

A corporate fulfilling the above criteria will be considered as a large corporate under this framework.

Subsequent to implementation of budget announcement and after making an assessment of the capacity of the bond market to absorb even lower rated issues, a view would be taken on reducing the threshold of rating in the extant framework, from “AA” to “A”.

4.2. Definition of borrowing: The word “long term borrowing” shall mean borrowings which have original maturity period of 1 year or above. Further, the same shall exclude external commercial borrowings and inter-corporate borrowings between a parent and subsidiaries.

4.3. Implementation Schedule: The framework is proposed to be implemented with effect from April 01, 2019 and the large corporate, which has been identified in terms of criteria as mentioned at para 4.1 above, shall raise 25% of its borrowings (incremental) for the following year through bond market. For e.g. a large corporate identified on March 31, 2019 shall borrow atleast 25% of its borrowings (incremental) made in F.Y. 2019-20 through bond market. Discussions with market participants and analysis of data reveals that the incremental shifting of corporate borrowing to bond market (as a result of this mandatory requirement), on a yearly basis, would be in the range of 5 to 10 % of the total bond issuances during a year. It is expected that this requirement may not be onerous on the corporates, given that implementation of IBC could result in further deepening of bond market by at least 5 % of GDP as brought out in para 3.15 above Also, the implementation of other related budget announcements and the proposed dispensing with the DRR requirement would give additional fillip to this initiative.

4.4. Compliance framework: The framework proposes a staggered compliance mechanism, details of which are as under:

a) Large corporate, covered under the framework shall inform the stock exchanges of the same;

b) A “comply or explain” approach would be applicable for the initial two years of implementation. Thus, in case of non-fulfillment of the requirement of market borrowing, reasons for the same shall be disclosed as part of the “continuous disclosure requirements”;

c) From third year of implementation i.e. F.Y. 2021-22, the requirement of bond borrowings shall be tested for a contiguous block of two years i.e. F.Y. 2021 22 and 2022-23 will be treated as one block and the requirement of 25% borrowing through bond market shall need to be complied for the sum of incremental borrowings made across the period of the block. Further, at the end of block if there is any deficiency in the requisite bond borrowing, a monetary penalty in the range of 0.2% to 0.3% of the shortfall shall be levied.

d) Subsequent compliance will be tested for each such block of two years i.e. FY 2023-24 and 2024-25, F.Y. 2025-26 and 2026-27, etc. in the manner identified above.

5. Public comments

Public comments are invited on the proposed framework given at Para 4 above. The comments, may be sent by email or through post, latest by August 13, 2018, in the following format:

| Details of Responder | |

| Name1/Organization:

1if responding in personal capacity |

|

| Contact number: | |

| Email address: | |

| Comments on the proposals as mentioned at Para 4 of | the consultation paper | ||

| Sr. No. | Para No. | Comment/proposed change | Rationale |

While sending email kindly ensure the subject is “Consultation Paper on designing a framework for enhanced market borrowings by large corporates”

Postal Address: Email Address:

Ms. Richa G. Agarwal bonds@sebi.gov.in

Deputy General Manager

Department of Debt and Hybrid Securities

Securities and Exchange Board of India

SEBI Bhavan

C4-A, G Block

Bandra Kurla Complex

Mumbai – 400 051

Issued on : July 20, 2018