Summary: The Reserve Bank of India’s Monetary Policy Committee (MPC) has decided to maintain the policy repo rate at 6.50% following its meeting from August 6 to 8, 2024. This decision aims to balance the goal of controlling inflation while fostering economic growth. The standing deposit facility rate remains at 6.25%, and the marginal standing facility rate and the Bank Rate are both at 6.75%. The MPC emphasized a continued withdrawal of accommodation to gradually align inflation with the 4% target, while also supporting economic growth. Global economic conditions show resilience with moderated inflation in major economies, though financial markets remain volatile. Domestically, economic activity is robust, supported by strong industrial output, growing private investment, and improving rural demand due to favorable monsoon conditions. Despite a rise in headline inflation to 5.1% in June 2024, driven mainly by food prices, core inflation remains moderate. The RBI projects a real GDP growth of 7.2% for 2024-25, with inflation expected to average 4.5% for the year. The MPC’s focus remains on maintaining price stability while ensuring steady economic growth. The next MPC meeting is scheduled for October 7-9, 2024.

Reserve Bank of India

Date: Aug 08, 2024

Monetary Policy Statement, 2024-25 Resolution of the Monetary Policy Committee (MPC) August 6 to 8, 2024

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (August 8, 2024) decided to:

- Keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 6.50 per cent.

Consequently, the standing deposit facility (SDF) rate remains unchanged at 6.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent.

- The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

Assessment and Outlook

2. The global economic outlook remains resilient although with some moderation in pace. Inflation is retreating in major economies but services price inflation persists. International prices of food, energy and base metals have eased since the last policy meeting. With varying growth-inflation prospects, central banks are diverging in their policy paths. This is creating volatility in financial markets. Amidst recent global sell offs in equities, the dollar index has weakened, sovereign bond yields have eased sharply and gold prices have soared to record highs.

3. Domestic economic activity continues to sustain its momentum. After a weak and delayed start, the cumulative southwest monsoon rainfall has picked up with improving spatial spread. By August 7, 2024, it was 7 per cent above the long period average. This has supported kharif sowing, with total area sown as on August 2, being 2.9 per cent higher than a year ago. Industrial output registered an expansion of 5.9 per cent (y-o-y) in May 2024. Core industries rose by 4.0 per cent in June, against 6.4 per cent in May. Other high frequency indicators released during June-July 2024 indicate expansion of services sector activity, ongoing revival of private consumption, and signs of pickup in private investment activity. Merchandise exports, non-oil non-gold imports, services exports and imports expanded during April-June.

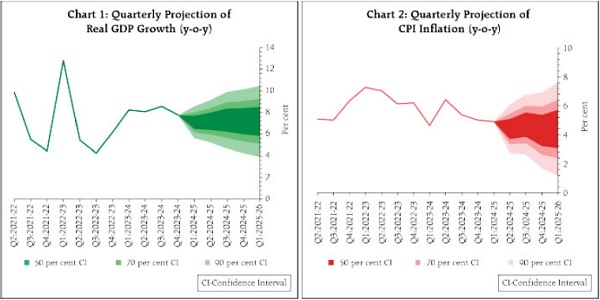

4. Going forward, the Indian Meteorological Department’s (IMD) projection of above normal southwest monsoon and healthy kharif sowing will support improving rural demand. The sustained momentum in manufacturing and services suggests steady urban demand. High frequency indicators of investment activity as evident in strong expansion in steel consumption, high capacity utilisation, healthy balance sheets of banks and corporates, and the Government’s continued thrust on infrastructure spending, point to a robust outlook. Improving world trade prospects could support external demand. Headwinds from geopolitical tensions, volatility in international commodity prices and geoeconomic fragmentation, however, pose risks to the outlook. Taking all these factors into consideration, real GDP growth for 2024-25 is projected at 7.2 per cent with Q1 at 7.1 per cent; Q2 at 7.2 per cent; Q3 at 7.3 per cent; and Q4 at 7.2 per cent. Real GDP growth for Q1:2025-26 is projected at 7.2 per cent (Chart 1). The risks are evenly balanced.

5. Headline inflation increased to 5.1 per cent in June 2024 after remaining steady at 4.8 per cent during April-May 2024. Worsening of food inflation pressures – driven primarily by a sharp increase in prices of vegetables, pulses and edible oils along with a pick-up in inflation across cereals, milk, fruits and prepared meals – pushed up headline inflation. The fuel group remained in deflation, reflecting the cumulative impact of the sharp cuts in LPG price in August 2023 and March 2024. Core (CPI excluding food and fuel) inflation at 3.1 per cent in May-June touched a new low in the current CPI series, with core services inflation also at its lowest in the series.

6. Headline inflation has moderated from its peak but unevenly. Looking ahead, food price momentum has remained elevated in July. In Q2:2024-25, though favourable base effects are large, the sharper uptick in price momentum relative to earlier expectations is likely to result in a shallower softening of CPI headline inflation. Inflation is expected to edge up in Q3 as favourable base effects taper off. The steady progress in monsoon, pick-up in kharif sowing, adequate buffer stocks of foodgrains and easing global food prices are positives for containing food price pressures. Adverse climate events remain an upside risk to food inflation. Crude oil prices continue to be volatile on demand concerns and geopolitical tensions. The revision in mobile tariff rates is likely to lead to an increase in core inflation. Manufacturing, services and infrastructure firms surveyed by the Reserve Bank expect a pickup in selling prices in the second half of this year. Households’ inflation expectations have also gone up and consumer confidence has weakened. Assuming a normal monsoon, CPI inflation for 2024-25 is projected at 4.5 per cent with Q2 at 4.4 per cent; Q3 at 4.7 per cent; and Q4 at 4.3 per cent. CPI inflation for Q1:2025-26 is projected at 4.4 per cent (Chart 2). The risks are evenly balanced.

7. The MPC expects domestic growth to hold up on the strength of investment demand, steady urban consumption and rising rural consumption. Risks from volatile and elevated food prices remain high, which may adversely impact inflation expectations and result in spillovers to core inflation. There are also indications of core inflation bottoming out. Accordingly, the MPC decided to remain watchful on how these forces play out, going forward. The MPC stays resolute in its commitment to aligning inflation to the 4 per cent target on a durable basis. In these circumstances, the MPC decided to keep the policy repo rate unchanged at 6.50 per cent in this meeting. The MPC reiterates the need to continue with the disinflationary stance, until a durable alignment of the headline CPI inflation with the target is achieved. Enduring price stability sets strong foundations for a sustained period of high growth. Hence the MPC also considers it appropriate to continue with the disinflationary stance of withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth.

8. Dr. Shashanka Bhide, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to keep the policy repo rate unchanged at 6.50 per cent. Dr. Ashima Goyal and Prof. Jayanth R. Varma voted to reduce the policy repo rate by 25 basis points.

9. Dr. Shashanka Bhide, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth. Dr. Ashima Goyal and Prof. Jayanth R. Varma voted for a change in stance to neutral.

10. The minutes of the MPC’s meeting will be published on August 22, 2024.

11. The next meeting of the MPC is scheduled during October 7 to 9, 2024.

(Puneet Pancholy)

Chief General Manager

Press Release: 2024-2025/850

Governor’s Statement: August 8, 2024

This was the 50th meeting of the Monetary Policy Committee (MPC) since its inception in September 2016.1 The flexible inflation targeting (FIT) framework will soon complete eight years of its functioning. The framework has worked well in maintaining macroeconomic stability even during times of extreme stress. Its embedded flexibility has withstood the pandemic-related stress, the spillovers from the war in Ukraine and the continuing geopolitical crisis. Today, while India’s growth remains strong, inflation is broadly on a declining trajectory. Strong macroeconomic fundamentals have led to greater confidence in India’s prospects.

Decisions and Deliberations of the Monetary Policy Committee (MPC)

2. The Monetary Policy Committee (MPC) met on 6th, 7th and 8th August 2024. After a detailed assessment of the evolving macroeconomic and financial conditions and the outlook, it decided by a 4 to 2 majority to keep the policy repo rate unchanged at 6.50 per cent. Consequently, the standing deposit facility (SDF) rate remains at 6.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent. The MPC also decided by a majority of 4 out of 6 members to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth.

3. I shall now briefly set out the rationale for these decisions. Headline inflation, after remaining steady at 4.8 per cent during April and May 2024, increased to 5.1 per cent in June 2024, primarily driven by the food component, which remains stubborn.2 Core inflation (CPI excluding food and fuel) moderated, while the fuel group remained in deflation.3 The expected moderation in headline inflation during the second quarter of 2024-25 on account of favourable base effects is likely to reverse in the third quarter. Domestic growth, however, is holding up well on the back of steady urban consumption and improving rural consumption, coupled with strong investment demand.

4. Amidst this confluence of factors, the MPC judged that it is important for monetary policy to stay the course while maintaining a close vigil on the inflation trajectory and the risks thereof. Resilient and steady growth in GDP enables monetary policy to focus unambiguously on inflation. It must continue to be disinflationary and resolute in its commitment to aligning inflation to the target of 4.0 per cent on a durable basis. Accordingly, the MPC decided to keep the policy repo rate unchanged at 6.50 per cent in this meeting. The commitment of monetary policy to ensure price stability would strengthen the foundations for a sustained period of high growth. Hence, the MPC reiterated the need to continue with the disinflationary stance of withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth.

Assessment of Growth and Inflation

Global Growth

5. Global economic outlook exhibits steady though uneven expansion.4 Manufacturing is indicating slowdown, while services activity is holding up.5 Notwithstanding sticky services prices, inflation is receding grudgingly across major economies. With varying outlook for growth and inflation across countries, monetary policy is showing signs of divergence across jurisdictions. Several central banks are cautiously moving towards policy pivots through forward guidance and rate cuts; at the same time, there has been tightening by a few central banks.6 Global financial markets are exhibiting volatility. Bond yields and the dollar index have softened since the last meeting.

6. While the near-term outlook looks positive, there are significant challenges to medium-term global growth outlook. Demographic shifts, climate change, geopolitical tensions and fragmentations, rising public debt and new technologies, such as artificial intelligence, pose new sets of challenges. A coherent policy approach in which monetary policy is complemented by other policies to manage the policy trade-offs will be crucial to deal with such multiple challenges.

Domestic Growth

7. Domestic economic activity continues to be resilient. On the supply side, steady progress in south-west monsoon,7 higher cumulative kharif sowing,8 and improving reservoir levels9 augur well for the kharif output. The likelihood of La Niña conditions developing during the second half of the monsoon season is likely to have a bearing on agricultural production in 2024-25.10

8. Manufacturing activity continues to gain ground on the back of improving domestic demand. The index of industrial production (IIP) growth accelerated in May 2024. Purchasing managers’ index (PMI) for manufacturing at 58.1 in July remained elevated. Services sector maintained buoyancy as evidenced by the available high frequency indicators.11 PMI services stood strong at 60.3 in July 2024, and is above 60 for seven consecutive months, indicating robust expansion.

9. On the demand side, household consumption is supported by a turnaround in rural demand12 and steady discretionary spending in urban areas.13 Fixed investment activity remained buoyant,14 amid government’s continued thrust on capex15 and other policy support.16 Private corporate investment is gaining steam17 on the back of expansion in bank credit.18 Merchandise exports expanded in June, although at a slower pace. Expansion in non-oil-non-gold imports accelerated reflecting resilience of domestic demand.19 Services exports recorded double digit growth in May 2024 before moderating in June.20

10. Looking ahead, improved agricultural activity brightens the prospects of rural consumption, while sustained buoyancy in services activity would support urban consumption. The healthy balance sheets of banks and corporates; thrust on capex by the government; and visible signs of pick up in private investment would drive fixed investment activity. Improving prospects of global trade are expected to aid external demand.21 The spillovers from protracted geopolitical tensions, volatility in international financial markets and geoeconomic fragmentation, however, pose risks on the downside. Taking all these factors into consideration, real GDP growth for 2024-25 is projected at 7.2 per cent, with Q1 at 7.1 per cent; Q2 at 7.2 per cent; Q3 at 7.3 per cent; and Q4 at 7.2 per cent. Real GDP growth for Q1:2025-26 is projected at 7.2 per cent. The risks are evenly balanced. It may be seen that we have slightly moderated the growth projection for Q1 of the current year in relation to the June 2024 projection. This is primarily due to updated information on certain high frequency indicators which show lower than anticipated corporate profitability, general government expenditure and core industries output.22

Inflation

11. Headline CPI inflation edged up to 5.1 per cent in June 2024 due to higher-than-expected food inflation. Fuel remained in deflation for the tenth consecutive month. Core inflation moderated to a historic low in May and June.23

12. Food inflation, with a weight of around 46 per cent in the CPI basket, contributed to more than 75 per cent of headline inflation in May and June.24 Vegetable prices increased sharply and contributed about 35 per cent to inflation in June.25 High inflation pressures persisted across other major food items also.26 On the other hand, the softening in core inflation continues to be broad-based, with core services inflation touching a new low in the current CPI series during May-June 2024.27

13. The high food price momentum is likely to have continued in July.28 Large favourable base effects may, however, push headline inflation downwards in July.29 The impact of the revision in milk prices30 and mobile tariffs needs to be watched.31

14. A degree of relief in food inflation is expected from the pick-up in the south-west monsoon and healthy progress in sowing. Buffer stocks of cereals continue to be above the norms. Global food prices showed signs of easing in July, after registering increases since March 2024.32 Assuming a normal monsoon, and taking into account the 4.9 per cent inflation print in Q1, CPI inflation for 2024-25 is projected at 4.5 per cent, with Q2 at 4.4 per cent; Q3 at 4.7 per cent; and Q4 at 4.3 per cent.33 CPI inflation for Q1:2025-26 is projected at 4.4 per cent. The risks are evenly balanced.

What do these Inflation and Growth Conditions mean for Monetary Policy?

15. As I stated earlier, continuing food price shocks slowed the process of disinflation in Q1:2024-25. There is also considerable divergence between headline and core inflation.34 This has brought to the fore the issue of how much importance should the MPC give to food inflation. Let me dwell upon this in some detail.

16. First and foremost is the fact that our target is the headline inflation wherein food inflation has a weight of about 46 per cent. With this high share of food in the consumption basket, food inflation pressures cannot be ignored. Further, the public at large understands inflation more in terms of food inflation than the other components of headline inflation. Therefore, we cannot and should not become complacent merely because core inflation has fallen considerably.

17. Second and equally important is the reality that high food inflation adversely affects household inflation expectations, which have a significant impact on future trajectory of inflation. Household inflation expectations, after witnessing a moderating trend between May 2022 and September 2023, have edged up on the back of high food inflation since November 2023.35 Persistently high food inflation and unanchored inflation expectations – if they materialise – could lead to spillovers to core inflation through pick-up in wages on cost-of-living considerations. This, in turn, could be passed on by firms in the form of higher prices for services as well as goods, especially in a scenario of strong aggregate demand. Third, these behavioural changes can then result in overall inflation becoming sticky, even after food inflation recedes.

18. The MPC may look through high food inflation if it is transitory; but in an environment of persisting high food inflation, as we are experiencing now, the MPC cannot afford to do so. It has to remain vigilant to prevent spillovers or second round effects from persistent food inflation and preserve the gains made so far in monetary policy credibility.

Liquidity and Financial Market Conditions

19. System liquidity transited from deficit in June to surplus conditions in July.36 In tune with the changing liquidity conditions, the Reserve Bank conducted two-way operations under the LAF37 to ensure that the inter-bank overnight rate remained closely aligned to the policy repo rate.38

20. Mirroring the liquidity dynamics, the weighted average call rate (WACR), on an average, remained close to the middle of the LAF corridor.39 Across the term money market segment, the yields on certificates of deposit (CDs) and 3-month treasury bills (T-bills) eased, while the yields on commercial papers (CPs) remained stable.40 The 10-year G-Sec yield softened in June-July and in August so far.41 The term premium has remained steady in recent months.42 Transmission in the credit market remains ongoing.43

21. Going forward, the Reserve Bank will continue to be nimble and flexible in its liquidity management operations keeping in view the evolving liquidity conditions to ensure that money market interest rates evolve in an orderly manner.

22. During 2024-25 (up to August 7), the Indian rupee (INR) remained largely range-bound.44 The lower volatility of the INR bears testimony to India’s macroeconomic and financial stability, and an improving external sector outlook.

23. In the last few days, global financial markets have seen turmoil on concerns of growth slowdown in a major economy, flare up in geopolitical tensions in the Middle East and the unwinding of the carry trade. These developments have implications for emerging market economies. In this context, it would be important for market participants to keep in mind the strength of India’s macroeconomic fundamentals, which remain robust. India has built strong buffers that impart resilience to the domestic economy from such global spillovers. The Reserve Bank remains committed to ensure orderly evolution of financial markets in its regulatory domain.

Financial Stability

24. The Indian financial system remains resilient and is gaining strength from broader macroeconomic stability. Its well-capitalised and unclogged balance sheet is reflective of higher risk absorption capacity.45 The NBFC sector and the Urban Cooperative Banks also continue to show improvements.46

25. Even in such stable financial sector conditions, the emphasis cannot shift away from proactive identification of potential risks and challenges, if any. In the current context, there are four issues which I would like to highlight. First, it is observed that alternative investment avenues are becoming more attractive to retail customers and banks are facing challenges on the funding front with bank deposits trailing loan growth. As a result, banks are taking greater recourse to short-term non-retail deposits and other instruments of liability to meet the incremental credit demand. This, as I emphasised elsewhere, may potentially expose the banking system to structural liquidity issues. Banks may, therefore, focus more on mobilisation of household financial savings through innovative products and service offerings and by leveraging fully on their vast branch network.

26. Second, it is observed that the sectors in which pre-emptive regulatory measures were announced by the Reserve Bank in November last year have shown moderation in credit growth.47 However, certain segments of personal loans continue to witness high growth.48 Excess leverage through retail loans, mostly for consumption purposes, needs careful monitoring from macro-prudential point of view. It calls for careful assessment and calibration of underwriting standards, as may be required, as well as post-sanction monitoring of such loans.

27. The third issue that is attracting our attention is home equity loans, or top-up housing loans as they are called in India, which have been growing at a brisk pace. Banks and NBFCs have also been offering top-up loans on other collateralised loans like gold loans. It is noticed that the regulatory prescriptions relating to loan to value (LTV) ratio, risk weights and monitoring of end use of funds are not being strictly adhered to by certain entities. I repeat certain entities. Such practices may lead to loaned funds being deployed in unproductive segments or for speculative purposes. Banks and NBFCs would, therefore, be well-advised to review such practices and take remedial action.

28. Fourth, recently there was an unprecedented IT outage globally, which affected businesses in many countries. The outage demonstrated how a minor technical change, if it goes haywire, can wreak havoc on a global scale. It also showed the fast-growing dependence on big-techs and third-party technology solution providers. In this background, it is necessary that banks and financial institutions build appropriate risk management frameworks in their IT, Cyber security and third-party outsourcing arrangements to maintain operational resilience. The Reserve Bank has time and again emphasised the importance of robust business continuity plans (BCP) to deal with such incidents.

External Sector

29. India’s current account deficit (CAD) moderated to 0.7 per cent of GDP in 2023-24 from 2.0 per cent of GDP in 2022-23 due to a lower trade deficit and robust services and remittances receipts. In Q1:2024-25, merchandise trade deficit widened as imports grew faster than exports. Buoyancy in services exports49 and strong remittance receipts are expected to keep CAD within sustainable level in Q1:2024-25. We expect CAD to remain eminently manageable during the current financial year.

30. On the external financing side, foreign portfolio investors turned net buyers in the domestic market from June 2024 with net inflows of US$ 9.7 billion during June-August (till August 6) after witnessing outflows of US$ 4.2 billion in April and May. Foreign direct investment (FDI) flows picked up in 2024-25 as gross FDI rose by more than 20 per cent during April-May 2024, while net FDI flows doubled during this period compared to the corresponding period of the previous year.50 External commercial borrowings moderated during April-June 2024-25, while non-resident deposits recorded higher net inflows during April-May compared to the previous year.51 India’s foreign exchange reserves reached a historical high of US$ 675 billion as of August 2, 2024.52 Overall, India’s external sector remains resilient as key indicators continue to improve.53 We remain confident of meeting our external financing requirements comfortably.

Additional Measures

31. I shall now announce certain additional measures.

Public Repository of Digital Lending Apps

32. The Reserve Bank has taken several measures54 for the orderly development of the digital lending ecosystem in India. As a further measure in this direction and to address the problems arising from unauthorised digital lending apps (DLAs), the Reserve Bank proposes to create a public repository of DLAs deployed by its regulated entities. The regulated entities (REs) will report and update information about their DLAs in this repository. This measure will help the consumers to identify the unauthorised lending apps.

Frequency of Reporting of Credit Information to Credit Information Companies

33. The availability of accurate credit information is vital for both lenders and borrowers. At present, lenders are required to report credit information to credit information companies (CICs) on a monthly basis or at such shorter intervals as may be agreed between the lenders and the CICs. It is proposed to increase the frequency of reporting of credit information to a fortnightly basis or at shorter intervals. Consequently, borrowers will benefit from faster updation of their credit information, especially when they repay their loans. The lenders, on their part, will be able to make better risk assessment of borrowers.

Enhancing Transaction Limit for Tax Payments through UPI

34. Currently, the transaction limit for UPI is ₹1 lakh except for certain category of payments which have higher transaction limits. It has now been decided to enhance the limit for tax payments through UPI from ₹1 lakh to ₹5 lakh per transaction. This will further ease tax payments by consumers through UPI.

Introduction of ‘Delegated Payments’ through UPI

35. It is proposed to introduce a facility of “Delegated Payments” in UPI. This would enable an individual (primary user) to allow another individual (secondary user) to make UPI transactions up to a limit from the primary user’s bank account without the need for the secondary user to have a separate bank account linked to UPI. This will further deepen the reach and usage of digital payments.

Continuous Clearing of Cheques

36. At present, cheque clearing through Cheque Truncation System (CTS) operates in a batch processing mode and has a clearing cycle of up to two working days. It is proposed to reduce the clearing cycle by introducing continuous clearing with ‘on-realisation-settlement’ in CTS. This means that cheques will be cleared within a few hours on the day of presentation. This will speed up cheque payments and benefit both the payer and the payee.

Conclusion

37. Under the current monetary policy setting, inflation and growth are evolving in a balanced manner and overall macroeconomic conditions are stable. Growth remains resilient, inflation has been trending downward and we have made progress in achieving price stability; but we have more distance to cover. The progress towards our goal of price stability has been uneven due to large and persistent supply side shocks, especially in food items. We, therefore, need to remain vigilant to ensure that inflation moves sustainably towards the target, while supporting growth. This approach would be net positive for sustained high growth.

38. We recognise the challenges along the way, but we have to be patient to finish the job at hand. In the current context, the following words of Mahatma Gandhi are highly relevant: “The slightest error of judgment, a hasty action or a hasty word may put back the hands of the clock of progress. Policies have, therefore, to be cautiously evolved…”55

Thank you. Namaskar.

(Puneet Pancholy)

Chief General Manager

Press Release: 2024-2025/851

1 On June 27, 2016, the Finance Act 2016 institutionalising inflation targeting framework through amendments to the RBI Act, 1934, came into effect. On the same day, Government notified Procedure for Selection of Members of the MPC and terms and conditions of their appointment Rules, 2016 as well as the factors constituting failure to achieve inflation target. On August 5, 2016, the inflation target was notified by the Government. On September 29, 2016, the government notified constitution of the first MPC which met for the first-time during October 3-4, 2016.

2 CPI food inflation at 8.4 per cent in June firmed up from 7.9 per cent in May driven primarily by a sharp increase in prices of vegetables and edible oils along with a pick-up in inflation across cereals, milk, fruits and prepared meals. CPI food inflation averaged 8.0 per cent since November 2023.

3 Core (CPI excluding food and fuel) inflation at 3.1 per cent during May-June 2024, touched a new low in the current CPI series. Fuel group continued to remain in deflation, reflecting the cumulative impact of the sharp cut in LPG price in August 2023 and March 2024.

4 The International Monetary Fund (IMF) in its latest World Economic Outlook (WEO) update released on July 16, 2024, maintained the global growth forecast for 2024 at 3.2 per cent (retained as in the April 2024 WEO) and revised up the growth forecast by 10 basis points (bps) to 3.3 per cent for 2025.

5 Global manufacturing PMI moved into contraction in July 2024 at 49.7 from 50.8 in June. Global services remained in expansion with PMI at 53.3 In July as compared to 53.1 in June.

6 Since the last MPC meeting, the UK, Canada, Switzerland and Czech Republic, among advanced economies (AEs) and China, Chile, Columbia, Hungary, Romania and Sri Lanka among emerging market economies (EMEs) have cut their policy rates. Japan and Russia, on the other hand, raised their benchmark rates.

7 After the pause from June 12, the Southwest Monsoon (SWM) picked up pace since June 28 and covered the entire country six days before the normal date (July 08). During the current SWM season so far (June 1- August 7), the cumulative rainfall has been 7 per cent above the Long Period Average (LPA), compared to 2 per cent above LPA during the corresponding period last year.

8 The total area sown under kharif crops at 904.6 lakh hectares was 2.9 per cent higher than a year ago as on August 2, 2024. The area under paddy, pulses, coarse cereals, oilseeds and sugarcane remained higher over last year, while it decreased under cotton.

9 At the all-India level, the water storage level in 150 major reservoirs stood at 51 per cent of total capacity as of August 1, 2024. The water storage, as percentage of total capacity, surpassed the decadal average.

10 Rainfall progress, however, needs to be cautiously watched as the La Niña events are also often associated with excess rainfall, which could lead to flooding and waterlogging and impact crop harvest in some regions.

11 E-way bills increased by 16.3 per cent in June 2024, GST revenues at Rs. 1.82 lakh crore rose by 10.3 per cent and toll collections expanded by 9.4 per cent during July. Domestic air cargo and port cargo posted a healthy growth of 10.3 per cent 6.8 per cent, respectively, in June 2024. Aggregate bank credit posted a growth of 15.1 per cent as on July 26, 2024.

12 Consumer non-durables rose by 2.3 per cent in May 2024, while two-wheeler sales expanded by 21.3 per cent in June. The demand under Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) declined by 21.7 per cent in June 2024 and 19.4 per cent in July, reflecting improvement in farm sector employment. Tractor sales registered a turnaround by recording 3.6 per cent growth in June.

13 Consumer durables posted a growth of 12.3 per cent in May 2024, and sales of passenger vehicles increased by 4.9 per cent in June. Domestic air passengers rose by 6.9 per cent in June 2024 and 6.0 per cent in July, on the back of a very high base as it increased by 19.2 per cent in June 2023 and 26.3 per cent in July 2023.

14 Steel consumption rose sharply by 14.6 per cent in July 2024. Cement production increased modestly by 1.9 per cent in June 2024. Imports of capital goods expanded by 11.6 per cent during June 2024, while capital goods production increased by 2.5 per cent in May 2024.

15 Capital expenditure as per the Budget Estimates (BE) for 2024-25 increased to ₹11.1 lakh crore (3.4 per cent of GDP), an increase of 17.1 per cent over ₹9.5 lakh crore in the provisional accounts (PA) of 2023-24 and 11.0 per cent over ₹10.0 lakh crore in BE 2023-24.

16 Government schemes such as Production Linked Incentive (PLI) scheme, Pradhan Mantri Awas Yojana (PMAY) [expanded to construct 3 crore additional houses] and Pradhan Mantri Gram Sadak Yojana (PMGSY) [launching of phase IV] would provide impetus to capital formation.

17 Capacity utilisation in manufacturing sector at 76.8 per cent in Q4:2023-24 is the highest in 11 years.

18 For the fortnight ending July 26, 2024, bank credit expanded by 15.1 per cent year-on-year. Bank credit to food processing, textiles, chemicals, base metal, and engineering goods increased y-o-y by 10.8 per cent, 6.2 per cent, 11.7 per cent, 11.7 per cent, and 8.8 per cent respectively in June 2024. Among infrastructure sectors, bank credit expanded by 3.3 per cent, 8.8 per cent and 7.0 per cent, respectively, in power, roads, and telecommunication during June 2024.

19 India’s merchandise exports expanded by 2.5 per cent (y-o-y) to US$ 35.2 billion, and imports registered an expansion of 5.0 per cent to US$ 56.2 billion in June 2024. Merchandise trade deficit stood at US$ 21.0 billion in June 2024 as compared with US$ 19.2 billion in June 2023.

20 While services exports grew by 3.7 per cent, services imports contracted by 3.8 per cent, in June 2024.

21 According to the IMF World Economic Outlook (July 2024 update), global trade volume (goods and services) is expected to grow by 3.1 per cent in 2024 as compared with a growth of 0.8 per cent in 2023. According to the World Trade Organisation, global merchandise trade volume is expected to grow by 2.6 per cent in 2024 as against a contraction of 1.2 per cent in 2023.

22 The results of 483 listed private manufacturing companies available so far indicate that their gross profits grew by a modest 4.7 per cent in Q1: 2024-25 as against 7.0 per cent in Q4:2023-24. Capital expenditure of central and state governments contracted by 35.0 per cent and 22.1 per cent, respectively, during Q1:2024-25. Revenue expenditure net of interest payments and subsidies of central and state governments contracted by 1.5 per cent and 0.2 per cent, respectively, during the quarter. Index of eight core industries expanded by 4.0 per cent year-on-year (y-o-y) in June 2024 compared to 6.4 per cent in May 2024.

23 Headline inflation which was at 4.8 per cent in April-May increased to 5.1 per cent in June. Food inflation surged to 8.4 per cent in June from 7.9 per cent in April-May. Deflation in fuel is (-) 3.7 per cent in June. CPI excluding food and fuel moderated from in 3.2 per cent in April to 3.1 per cent in May-June 2024, a new low in the current CPI series.

24 Contribution of food to headline inflation increased from 74.7 per cent in April to 75.2 per cent in May and 76.3 per cent in June. The contribution of food was 44.8 per cent in June 2023.

25 CPI tomatoes increased by 48.7 per cent (m-o-m) in June, CPI onion by 24.2 per cent (m-o-m) and potatoes by 12.2 per cent (m-o-m), resulting in a year-on-year inflation of 29.3 per cent for vegetables. Overall, vegetables with a weight of 6.0 per cent in CPI basket contributed 34.9 per cent to inflation in June.

26 Cereals inflation increased to 8.8 per cent in June from 8.6 per cent in April. Fruit inflation increased to 7.2 per cent in June from 5.2 per cent April. Pulses inflation at 16.1 per cent in June, recorded 13 consecutive months in double digits.

27 In CPI excluding food and fuel, core goods inflation was at 3.5 per cent in June compared to 3.6 per cent in April. Core services inflation moderated to 2.7 per cent In June from 2.8 per cent in April.

28 High frequency food price data from Department of Consumer Affairs (DCA) points to a month on month increase in tomato prices by 62.1 per cent in July, onion prices by 22.6 per cent and potato prices by 18.0 per cent. Prices of key pulses also increased in the range of 0.4 to 4.3 per cent in July.

29 CPI headline inflation would experience a favourable base effect of 2.9 percentage points in July.

30 Milk has a high weight of 6.4 per cent in CPI basket. Milk prices have been increased by Rs.2 per litre in early June 2024 by a few major dairies.

31 Mobile tariffs were increased in range of 10-22 per cent by the major companies in early July.

32 The FAO food price index, after registering an increase during March-June 2024, declined in July, with a month-over-month change of (-) 0.18 per cent.

33 Food inflation pressures could see a significant abatement in Q4:2024-25 as the good run of the monsoon may continue to progress during the rest of the season. La Nina conditions may lead to higher moisture content conducive for a good rabi sowing. Good reservoir level would also further ease risk to food production.

34 The divergence between headline and core inflation increased to 2 percentage points in June 2024 from 1.6 percentage points in April and 0.3 percentage points a year ago.

35 The 3-month and 1-year ahead household inflation expectations declined by 170 bps and 120 bps, respectively between May 2022 and September 2023. Food inflation averaged around 8 per cent during November 2023-June 2024. Since November 2023, the decline in inflation expectations has halted. 3-month and one year ahead inflations rose by 20 bps each in the July 2024 round of the survey over the previous survey round (May 2024).

36 System liquidity, as measured by the net position under the liquidity adjustment facility (net LAF) was, on an average, in deficit of about ₹0.45 lakh crore during June but turned into surplus of about ₹1.1 lakh crore during July. Thereafter, it continued to be in surplus of about ₹2.7 lakh crore in August (up to August 6). The transition from surplus in early June to deficit conditions during the latter half of the month was on account of liquidity leakage from the banking system due to advance tax payments and goods and services tax (GST) related outflows. With the increase in government spending at the month-end, system liquidity again turned into surplus beginning June 28.

37 Liquidity Adjustment Facility.

38 As liquidity conditions tightened, the Reserve Bank injected liquidity through variable rate repo (VRR) operations during the second half of June but mopped up surplus liquidity through variable rate reverse repo (VRRR) auctions as liquidity conditions eased in July. During June 10-28, one main and 4 fine-tuning VRR auctions (3 to 6 days maturity) injected liquidity cumulatively amounting to ₹3.5 lakh crore, while 2 main and 23 fine-tuning VRRR operations (1 to 7 days maturity) absorbed liquidity to the extent of ₹7.1 lakh crore during July-August (up to August 6). A 3-day VRR auction was conducted instead of the main 14-day operation on June 28 as liquidity conditions were expected to improve imminently with the usual increase in government spending at the month end.

39 The standing deposit facility (SDF) rate at 6.25 per cent (25 bps below the repo rate) and the marginal standing facility (MSF) rate at 6.75 per cent (25 bps above the repo rate) provide a corridor around the repo rate at 6.50 per cent. The weighted average call rate (WACR) averaged 6.54 per cent during June – August (up to August 6) as against 6.58 per cent during April – May. Rates in the collateralised segment – the triparty and market repo rates – although relatively softer, moved in tandem with the WACR.

40 Average yields on CDs and T-bills moderated from 7.34 per cent and 6.90 per cent, respectively, in April-May to 7.13 per cent and 6.76 per cent, respectively, during June – August (up to August 6), while that on CPs marginally increased from 7.75 per cent to 7.76 per cent during the same period.

41 The 10-year G-Sec yield averaged 6.97 per cent during June – August (up to August 6) as compared to 7.08 per cent during April – May 2024.

42 The term premium is calculated as the difference between the yield on 10-year G-Sec and 91-day T Bills. On an average, the term premium was 22 bps during June-August (up to August 6) as compared to 18 bps during April-May.

43 In response to the cumulative policy repo rate hike of 250 bps since May 2022, the weighted average lending rates (WALRs) on fresh and outstanding rupee loans of SCBs have increased by 181 bps and 119 bps, respectively, during May 2022 to June 2024, while the weighted average domestic term deposit rate (WADTDR) on fresh and outstanding deposits of SCBs increased by 243 bps and 188 bps, respectively, during the same period. With credit growth outpacing deposit growth, banks have raised their term deposit rates in addition to mobilising funds through higher issuances of CDs. In 2024-25 (up to July), CD issuances amounted to ₹3.2 lakh crore as compared to ₹1.9 lakh crore in the corresponding period of 2023-24.

44 On a financial year basis (up to August 7), the Indian rupee (INR) registered lower depreciation (-0.7 per cent) against the US dollar as compared to the depreciation of some of its emerging market peers like Mexican peso, Brazilian real, Argentine peso, Turkish lira, Philippine peso, Vietnamese dong and Indonesian rupiah. During 2024-25 (up to August 7), the INR was the least volatile (in terms of coefficient of variation) amongst peer EME currencies, including – Chinese yuan, Vietnamese dong, Indonesian rupiah, Thailand baht and Turkish lira.

45 The capital-to-risk-weighted assets ratio (CRAR) and the common equity tier 1 (CET1) ratio of scheduled commercial banks (SCBs) at 16.8 per cent and 13.9 per cent, respectively, at end-March 2024 are well above the regulatory thresholds. On the other hand, SCBs’ gross non-performing assets (GNPA) and net non-performing assets (NNPA) ratios have dipped to 2.8 per cent and 0.6 per cent, respectively, at end-March 2024. Resultantly, the SCBs ratio of NNPAs with total equity has dipped to an all-time low of 4.1 per cent in March 2024 from the peak of 43.9 per cent in March 2018. The macro stress tests done by the Reserve Bank also reveal that the banking sector will continue to remain resilient even under stress scenarios (Financial Stability Report, June 2024).

46 Non-Banking Financial Companies (NBFCs) remain healthy, with CRAR at 26.6 per cent, GNPA ratio at 4.0 per cent and Return on Assets (RoA) at 3.3 per cent at end-March 2024. Excluding NBFCs under resolution, the GNPA ratio for NBFCs is below 3 per cent. The capital position of UCBs has been continuously improving in the post-pandemic period [CRAR was 17.5 per cent as on March 31, 2024].

47 The Reserve Bank increased risk weights on unsecured consumer credit and bank credit to NBFCs on November 16, 2023 to pre-empt build-up of any potential risk in these segments. Consequently, the total consumer loan growth in the sectors where risk weights were increased moderated from 23.3 per cent in November 2023 to 13.9 per cent in June 2024. In parallel, bank credit to NBFCs declined from 18.5 per cent to 8.2 per cent during the same period.

48 Credit growth in unsecured personal loans such as ‘credit card outstanding’ though declining, remained high at 23.3 per cent in June 2024 as compared to 34.2 per cent in November 2023.

49 As per provisional figures, India’s services exports grew by 10.4 per cent during April-June 2024-25, while services imports rose by 6.5 per cent during the same period. Net services exports grew by 15.4 per cent during the same period.

50 Gross foreign direct investment (FDI) flows rose sharply by 22.8 per cent to US$ 15.2 billion in April-May 2024-25 from US$ 12.3 billion during the same period a year ago. Net FDI flows increased twofold to US$ 7.1 billion in April-May 2024-25 from US$ 3.4 billion a year ago due to lower repatriation.

51 External commercial borrowings to India moderated to US$ 1.8 billion during April-June 2024-25 as compared with an inflow of US$ 5.7 billion a year ago. Non-resident deposits recorded a higher net inflow of US$ 2.7 billion in April-May 2024-25 than US$ 0.6 billion a year ago.

52 As on August 2, 2024, India’s foreign exchange reserves stood at US$ 674.92 billion.

53 India’s CAD/GDP ratio moderated to 0.7 per cent in 2023-24 from 2.0 per cent during 2022-23. India’s external debt to GDP ratio declined to 18.7 per cent at end-March 2024 from 19.0 per cent at end-March 2023. The net International Investment position to GDP ratio improved from (-) 11.3 per cent to (-) 10.3 per cent during the same period.

54 These include the guidelines on digital lending and first loss default guarantee issued in September 2022 and June 2023 respectively.

55 Mahatma Gandhi, Collected Works, Vol. 67 and Harijan, August 17, 1935.

Statement on Developmental and Regulatory Policies

This Statement sets out various developmental and regulatory policy measures relating to (i) Regulations; and (ii) Payment Systems.

I. Regulations

1. Public Repository of Digital Lending Apps

Guidelines on Digital Lending addressing protection of customers interest, data privacy, concerns on interest rates and recovery practices, mis-selling, etc. were issued on September 02, 2022. However, media reports have highlighted continued presence of unscrupulous players in digital lending who falsely claim their association with RBI regulated entities (REs). Accordingly, to aid the customers in verifying the claim of Digital Lending App’s (DLAs) association with REs, Reserve Bank is creating a public repository of DLAs deployed by the REs which will be available on RBI’s website. The repository will be based on data submitted by the REs (without any intervention by RBI) directly to the repository and will get updated as and when the REs report the details, i.e., addition of new DLAs or deletion of any existing DLA. Detailed instructions in this regard shall be issued shortly.

2. Frequency of Reporting of Credit Information to Credit Information Companies

At present credit institutions (CIs) are required to report the credit information of their borrowers to credit information companies (CICs) at monthly or such shorter intervals as mutually agreed between the CI and CIC. With a view to provide a more up-to-date picture of a borrower’s indebtedness, it has been decided to increase the frequency of reporting of credit information to CICs from monthly intervals to fortnightly basis or at such shorter intervals as mutually agreed between the CI and CIC. The fortnightly reporting frequency would ensure that credit information reports provided by CICs reflect a more recent information. This will be beneficial to both borrowers and lenders (CIs). Borrowers will have the benefit of faster updation of information, especially when they have repaid the loans. Lenders will be able to make better risk assessment of borrowers and also reduce the risk of over-leveraging by borrowers. Necessary instructions will be issued shortly.

II. Payment Systems

3. Enhancing Transaction Limits for Tax Payments through UPI

UPI has become the most-preferred mode of payments, due to its seamless features. Currently, the transaction limit for UPI is capped at ₹1 lakh. Based on the various use-cases, the Reserve Bank has periodically reviewed and enhanced the limits for a few categories like capital markets, IPO subscriptions, loan collections, insurance, medical and educational services etc.

As direct and indirect tax payments are common, regular and high value, it has been decided to enhance the limit for tax payments through UPI from ₹1 lakh to ₹5 lakh per transaction. Necessary instructions will be issued separately.

4. Introduction of Delegated Payments through UPI

The Unified Payments Interface (UPI) has a very large user base of 424 million individuals. There is, however, potential for further expansion of the user base.

It is proposed to introduce “Delegated Payments” in UPI. “Delegated Payments” would allow an individual (primary user) to set a UPI transaction limit for another individual (secondary user) on the primary user’s bank account. This product is expected to add to the reach and usage of digital payments across the country. Detailed instructions will be issued shortly.

5. Continuous Clearing of Cheques under Cheque Truncation System (CTS)

Cheque Truncation System (CTS) currently processes cheques with a clearing cycle of up to two working days. To improve the efficiency of cheque clearing and reduce settlement risk for participants, and to enhance customer experience, it is proposed to transition CTS from the current approach of batch processing to continuous clearing with ‘on-realisation-settlement’. Cheques will be scanned, presented, and passed in a few hours and on a continuous basis during business hours. The clearing cycle will reduce from the present T+1 days to a few hours. Detailed guidelines in this regard shall be issued shortly.

(Puneet Pancholy)

Chief General Manager

Press Release: 2024-2025/852