CA Nitul Mehta

Introduction:

ADR’S, GDR’S: These are commonly known as Depository Receipts (‘DR’), a negotiable security issued outside India by a depository bank (‘DB’), on behalf of the Indian company, which reflects the local rupee denominated equity shares of the company held as deposit by a custodian bank (‘CB’) in India. These DR’s were bought out as an option for Indian companies to get an access to overseas capital markets.

Fundamentally, new doors were opened for non-residents who wished to invest in Indian capital markets and concurrently have liquidity and minimum procedural requirements. These doors were opened in 1993 vide amendment in Master Circular on Foreign investment n India (‘Circular’) under Foreign Exchange Regulation Act (‘FERA Act’) presently know as Foreign Exchange Management Act (‘FEMA’) . These DR are listed on various stock exchanges and freely tradable on such stock exchanges , DR’s issued on American stock exchanges are termed as American Depository receipts (‘ADRs’) and which are listed on other stock exchanges are named as Global depositor y receipts (‘GDRs’). Concurrently the Indian companies can also raise monies overseas without attracting so many Laws of such country from which the monies are raised.

Implications under FEMA:

Since, ADR’s and GDRs being one of the way of directly subscribing to capital of Indian Companies by non-residents, subscribing to DR’s is termed under Foreign Direct Investment (‘FDI’), and accordingly sectoral caps apply on issue of these DR .

The companies which are eligible to issue shares to nonresident within the sectoral cap of FDI are eligible to issue DR s and on other side of the coin person/entities who are not eligible to invest in capital markets or who have been refrained from Indian capital markets are not eligible to invest in ADRs and GDR’s.

There is also a window kept open for residents of India to hold DR s overseas by surrendering shares to the company and holding foreign exchange on sale of those DR’s in a foreign currency (Domestic) account.

Further a two way limited fungubility option is available where a non-resident can give a advice note to his SEBI Broker/ DP/and Authorized Dealer category-I in Inda and get his DR’s converted in to shares which are then readily listed on stock exchange with some pricing restrictions and on a other side already converted DR’s in to shares can again be reconverted into DRs fol l wing the samproce ure and they automatically get listed on overseas stock exchange.

Further, from the companies prospective there is no bar on end use of the proceeds of ADR/GDR and till the date company brings such proceeds in to India it can be invested in a very restrictive fashion such as Fixed deposits, government securities etc.

To understand the taxation of DR’s let’s first understand the scheme of ADR’s and GDR ’s:

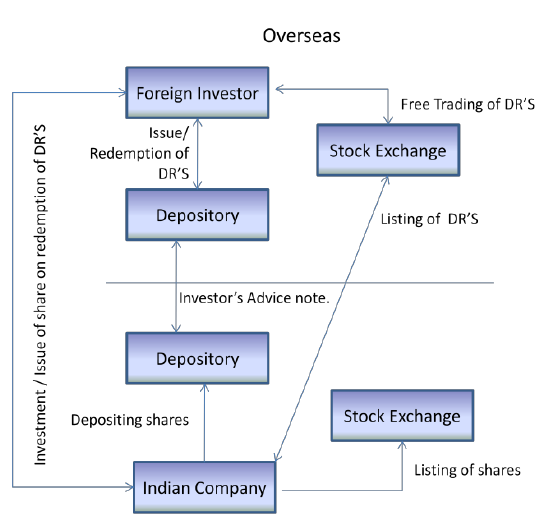

Similar to issue of shares in India by the company, while going for an Initial Public Offer or Further Public Offer, or listing a Stock Option plan overseas, company engages a overseas depository participant who acts as a custodian of DR’s, this is done in consultation of Lead Merchant Banker here in India who also acts for/or helps the company in appointing a custodian in India to hold shares on behalf of DR holder.

A schematic presentation of the above arrangement is showed below.

Now let’s evaluate the options under which a non-resident investor can divest his investment in the Indian company without crossing the line under FEMA:

1. Transfer of DR’s to another Non-Resident:Under FEMA and Exchange control Manual issued by Reserve Bank of India (‘RBI’), a non-resident can freely transfer DR’s to another non-resident via sale or gift.

2. Transfer of DR’s to a Resident of India: As per legislation mentioned in option 1 a non-resident is allowed to gift any security to a resident in India. However, options available with Resident to subsequently dispose off the DR s are not clear under FEMA. Further the wordings under the circular suggests that Non –residents has only two options

in India after acquiring the DR’s, one is to get it converted into shares and sell it immediately without any further procedural requirements and the other is to redeem the DR’s overseas and send a advice to DP in India to get the shares transferred in his name.

3. Get DR’s converted to shares and then sell them on Indian stock exchange.

There is no specific restriction on this option other than some pricing regulations and procedural requirements to be fulfilled like certificate from accountant for payment of taxes, no objection certificate from Income Tax department etc.

In the above back drop now let’s understand the provisions of Income Tax Act 1961 (‘Act’)

Taxation of income from any overseas securities issued by Indian companies including DR’s is dealt specifically under section 115AC (for other than employees of issuing company) and 115ACA (for employees of issuing company).

Section 115ACA is amply clear which taxes dividends other than those covered under section 115-O of the act on DR’s under the hands of the resident employees @ 10%. Further income in way of long-term capital gains on transfer of those DR s are taxed at a concessional rate of 10%.

Section 115AC similarly taxes the income from DR’s to a nonresident at a concessional rate of 10%. The non-Resident, further need not file his return of income if he has only income

covered under this section taxable in India and appropriate TDS has been deducted on the said income. Further since the DR is just a change in nomenclature of shares any transfer/ surrender of DR during a course of amalgamation/demerger under section 47 should not attract the term ‘Transfer’.

Situs of DR’s:

As it can be inferred from the definition of DR as explained above which can also be seen from Fig 1.1 above, that DR is issued by the overseas DP and is also redeemed through them only, hence, one can argue that the Situs of DR is outside India. However, applying a look-at approach as ruled by the apex court and also viewing it from the eyes of ‘Substance over form’, Non-resident is ultimately holding share capital in Indian company and holding of shares instead of DR is just a change in nomenclature and only for convenience of liquidity and hassle free investment process.

Moreover the value of DR though traded on overseas stock exchanges is ultimately derived from the share value of that company in India. Concurrently, recent amendment in the Act wherein any capital asset whose substantial value is derived from assets situated in India is to be deemed as situated in India, in spite of the fact that DR is situated overseas the amendment extends the reach of section 9 of Act and deems DR to be situated in India. Though a stand can be taken that value of DR overseas on stock exchanges depends on demand and supply relationship on that exchange, the value of those DR substantially depends on what is the price of the underlying asset i.e. of shares in India or at Indian stock exchanges. Hence from the above it is impermissible to argue that Situs of DR is not in India. This is also seconded by intention of the government by taxing the transfer of DR as capital gains under 11 5AC and 11 5ACA respectively.

Once the Situs of DR is concluded to be in India let us evaluate the tax liability on various options under FEMA as discussed as above.

1. Transfer of DR’s to another Non-Resident:

Under this option as discussed earlier non-resident transfers the DR to another non-resident overseas in foreign exchange, this prima facie gets taxed under section 11 5AC of the Act. However, due to specific exemption given under section 47 of the Act the same is not treated as transfer and not liable to capital gain tax in India.

Though the ultimate purpose of going under this route is not clear from a resident’s prospective, since the exemption available under section 47 as taken under option 1 is not available here, since this is not a transfer made to non-resident, this transfer will squarely fall under section 115AC and will be taxed accordingly depending on whether it is short term capital gains or long term capital gains.

However, if the transfer is in the form of gift, this could have implications on the part of resident as receiver of gift under section 56 and accordingly will be taxed to resident as ‘Income from other sources’.

3. Get DR’s converted to shares and then sell them on Indian stock exchange:This being the most complicated option, since there are two stages of transfers being done, one when the DR are converted into equity shares and other when the equity shares are actually sold. Let us deal this stage wise:Stage I: At this stage DR are converted into equity shares either to still hold them or to sell them off immediately. irrespective of above since DR and equity shares are two separate financial instruments with separate voting rights under companies Act, separate set of risks involved, separate returns expected from them, issuing authority also being different, and most importantly transfer of DR is kept open for taxation under section 115AC of the Act. From the foregoing it would not be wrong to say that surrendering of DR in order to get shares in lieu of it is taxable in India

Further, the scheme of ‘Issue of Foreign currency convertible bonds and ordinary shares (Through Depository Receipt Mechanism) 1993 states that value of shares acquired or say cost of acquisition of shares obtained by surrendering the DR’s will be the market value of those shares as on the date of such shares getting credited to his D-mat account or getting the purchase note from the respective stock broker which ever is earlier, moreover the period of holding of those shares is also to be reckoned from the date of those shares getting credited to one’s account and not from the date from which DR’s were held, from which is amply clear that stage I and II are separate taxable events.

Further, one more view is also possible that exchange of DR for equity is just moving from one class of deemed equity to another class of equity with new/separate rights which is similar to exchanging A class of equity for B class of equity which may still fall under the term ‘Transfer’and capital gains may attract accordingly.

It is also pertinent to note that one of the clauses of section 47 mentions ”any transfer by way of conversion of (bonds) or debentures, debenture stock, or deposit certificates in any form, of a company in to shares or debentures of that company” will not attract the provisions of section 45 i.e. charging section of capital gains under the Act.

Few questions that arise from the above clause are, does the deposit certificate as mentioned above include DR, prima facie it does not look like because the relationship between lender and borrower which exists generally in a transaction of deposit is missing here, and an extremely aggressive stand would also not fall within the four walls of ‘Deposit certificates’. Another question that arise is, specific exemption for transfer of DR between Non-resident to Non-Resident is provided in the Act and, also specific provision to exclude conversion of bonds mentioned under section 115AC, (the same section where taxation of DR is mentioned), in to equity shares is been provided but there is no specific provision to exempt exchange of DR with equity from capital gains. Hence it can be safely be concluded that exchange of DR with equity is a taxable event.

The cost of acquisition taken for the above shares as discussed in the preceding paragraphs can also be treated as sale value for the DR’s surrendered/ transferred/exchanged. Further one can also argue that getting equity by surrendering DR is not a transfer, but the definition of transfer is wide enough to include exchange of assets which in this case is of DR for equity shares, which via intermediataries ultimately happens between the company and share holder/DP holder.

To conclude stage I, the exchange being taxable and the computation of gain is done by taking sale value as mentioned in the above paragraph and cost of acquisition as actual cost incurred to acquire DR.

Stage 2: At this stage since the DR are converted in to equity shares and are listed on Indian stock exchanges, there is no ambiguity as to the Situs of the shares and depending on which type of capital gain is earned i.e. Long term which will be exempt under section 10(38) or Short term which will be taxed at a special concessional rate of 15%.

Further the mode of computation is also not complex since the cost of acquisition is derived as mentioned in the scheme as discussed above and sale value will be the net sale consideration received by selling the shares.

Effects on Two Way Fungubility option:

As discussed earlier RBI has given a limited option of getting converted DR into shares by non-resident and reconverting equity shares to DR up to a extent to which they were converted from those DR directly through SEBI registered stock broker and Authorized Dealer category-I. If the above interpretation of taxability is adopted, every time the DR is converted in to shares and vice-versa there would arise a tax liability on capital gain.

Conclusion:

To conclude, the most tax savvy way of disposing off DR’s for a non-resident is to sell it to another non-resident, which also serves the purpose of Indian Government since it helps to postpone shelling of foreign exchange due to aggressive taxation on DR’s.