Case Law Details

Barapur Gramodyog Vikas Samiti Vs ITO (ITAT Delhi)

The AO while completing the assessment noticed that the assessee claimed exemption u/s 10(23B) of the Act as the assessee was engaged in the business of production, sale, etc. of Khadi and Products of Village Industries. The AO was of the view that in view of proviso to section 10(23B) of the Act Khadi and Village Industries Commission has to grant the approval for not more than three assessment years beginning with the assessment year next following the financial year in which exemption was granted. Therefore, AO was of the opinion that in the present case approval was granted for more than three assessment years and the condition for claiming exemption u/s 10(23B) was not fulfilled and accordingly, he denied the exemption claimed by the assessee u/s 10(23B) of the Act.

ITAT observed that certificate issued by Khadi & Village Industries Commission clearly show that it relates to the period from 11.06.2012 to 31.03.2016 and followed by the letter issued by the Commission to the ITO, Bijnore, Uttar Pradesh clearly shows that the assessee is entitled to claim exemption u/s 10(23B) of the Act. The reason for denying the exemption by the AO is that the Commission has given certificate to the assessee for more than three years. It is pertinent to note that the time period for which the certificate has to be granted is not within the control of the assessee. In any case it is only a technical violation for which the assessee could not be penalized by denying the exemption otherwise allowable to the assessee. Thus, I hold that the assessee is entitled for exemption u/s 10(23B) of the Act. Accordingly, the Assessing Officer is directed to allow the claim for exemption u/s 10(23B) as claimed by the assessee.

FULL TEXT OF THE ORDER OF ITAT DELHI

This appeal is filed by the Assessee against the order of the Ld. CIT(Appeals)-(NFAC), Delhi dated 16.09.2021 for the AY 201617. The assessee filed written submissions on 10.05.2022 as the Counsel for the assessee is admitted in hospital and he is unable to attend the hearing and, therefore, requested to decide the appeal on the basis of written submissions or adjourn the matter for two months. The appeal of the assessee is disposed off based on the written submission furnished by the assessee.

2. The assessee in its appeal raised the following grounds: –

1. “That the AO has misinterpret the certificate of registration of society which was for five years and ignore the exemption certificate u/s 10(23B) which was only for AY 2016-17. Hence, order passed by AO having bundle of mistake suo moto which can be rectify u/s 154, which is not done by AO hence assessment made by AO is arbitrary, unjust and not according to law and Ld. CIT(A) confirmed the addition ignore the relevant facts and also bad in law.

2. That the exemption certificate given by Khadi and Gram Industry Commission, Mumbai u/s 10(23B) is crystal clear. The AO has misinterpret with the registration of society which is for five years and it is nothing to do with exemption 10(23B) of I.T. Act. Therefore, addition made by AO and confirmed by CIT(A) against the facts and law.

3. That Ld. CIT(A) has committed error in para 5.3 that exemption certificate is available for the FY 2016-17 i.e. AY 2017-18. However, exemption certificate was for the AY 201617.

4. That the assessee has right to add, delete or modify any grounds of appeal during the proceedings.

3. The AO while completing the assessment noticed that the assessee claimed exemption u/s 10(23B) of the Act as the assessee was engaged in the business of production, sale, etc. of Khadi and Products of Village Industries. The AO was of the view that in view of proviso to section 10(23B) of the Act Khadi and Village Industries Commission has to grant the approval for not more than three assessment years beginning with the assessment year next following the financial year in which exemption was granted. Therefore, AO was of the opinion that in the present case approval was granted for more than three assessment years and the condition for claiming exemption u/s 10(23B) was not fulfilled and accordingly, he denied the exemption claimed by the assessee u/s 10(23B) of the Act.

4. On appeal the Ld. CIT(Appeals) sustained the order of the AO in denying the exemption claimed by the assessee u/s 10(23B) observing that the certificate issued by the Khadi and Village Industries Commission was valid from 01.04.2016 to 31.03.2021 beginning from the FY 2016-17 relevant to AY 2017-18 onwards and, therefore, he held that assessee is not entitled to claim exemption for AY 2016-17.

5. The assessee in its written submissions stated as under:

“It is submitted that in the above case, the assessee is cooperative society registered under Society Registration Act, 21, 1860, the assessee further applied for exemption u/s 10(23B). The certificate of the society registration was already available at the time of hearing before the CIT(A) vide Letter No. DOM/Khadi/BGVS/2018-19 dated 05.02.2019 directly by the Khadi and Village Industries Commission, Divisional Office, Meerut.

The AO has not allowed ignored the certificate and not rely upon the documents already available to him and decide the case on the basis of registration of Society Act which is not absolutely correct because the assessee has already obtained certificate vide Regn. No. 1872/1981-82 from Khadi and Village Industries Commission. Therefore, for wants of certificate the assessee requests your honour to kindly accept the contention of the assessee. Here it is further mentioned that the assessee has applied more than five to six months before but due to the Government and Khadi and Village Industries Commission, the assessee could not file the certificate in time. Even, at the time of CIT(A) has decide the appeal he has not gone to the record which can be obtained by the AO in remand proceedings.

The assessee rely upon the Hon’ble Bombay High Court Judgment in the case of Mahila Griha Udyog Lijjat Papad vs. Deputy Directory of Income Tax (Exemption)-1(1), (2012) 20 taxmann.com 643 (Bom.), in which Hon’ble Bombay High Court held as under:

Section 10(23B), read with section 147, of the Income Tax Act, 1961 – Khadi and Village Industries, Institution for Development of – Assessment year 2004-05 – Assessee was a registered trust which had been granted exemption under section 10(23B) from AY 1975-76 onwards – It had been approved by Commissioner, Khadi and Village Industries Commission which had not been revoked till date – Assessee filed its return along with income and expenditure account and balance sheet declaring total sales of Rs.288.47 crores and income of Rs.6.54 crores – Assessing Officer passed order of assessment on 29.12.2006 accepting claim of assessee to benefit of exemption under section 10(23B) after being duly satisfied that assesse had fulfilled requisite conditions – Subsequently on 21.03.2011 Assessing Officer issued notice under section 148 seeking to reopen assessment on ground that books of account filed with return indicated that activities carried on by assessee did not cover any public charity but were commercial activities; besides assessee failed to provide details of expenditure incurred to achieve approved objects – Whether since entire basis for reopening assessment was income and expenditure account and balance sheet filed along with return of income, it was to be held that primary requirements of proviso to section 147 for reopening an assessment beyond a period of four years, had not been fulfilled – Held, yes – Whether line of enquiry which Assessing Officer sought to pursue in regard to expenditure incurred by assessee was extraneous to purpose of section 10(23B), as section 10(23B) only requires that an institution must exist solely for purpose of developing Khadi and Village Industries – Held, yes – Whether in view of above and further in view of fact that Assessing Officer had completely ignored objections which were filed by assessee, it was to be held that reopening of assessment was purely based upon a change of opinion by Assessing Officer and could not be permitted in law – Held, yes (In favour of assessee).”

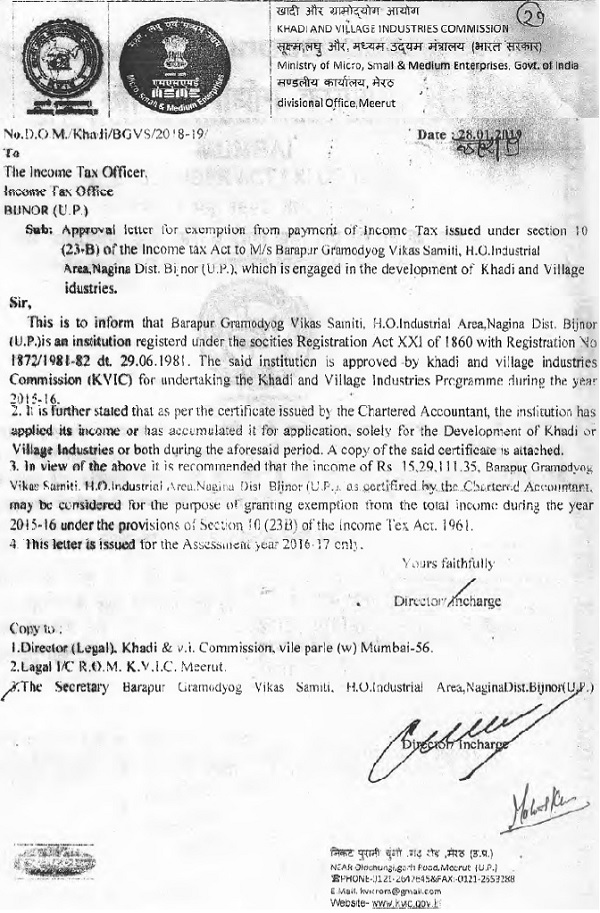

6. Apart from the above submissions, the assessee in its Paper Book enclosed copy of certificate issued by Khadi and Village Industries Commission, Mumbai recognizing the assessee for granting rebate and other financial benefits from 11.06.2012 to 31.03.2016 (vide certificate no. 3854/2013-14). This certificate was ignored by the Ld. Commissioner (Appeals) while adjudicating the appeal of the assessee. It is further noticed that the certificate which the Ld. CIT(Appeals) referred to in his order is the certificate issued for the period from 01.04.2016 to 31.03.2021 i.e. for AY 2017-18 onwards which is also placed on record before me. Relying on this certificate the Ld. CIT(A) held that the assessee is not entitled for exemption u/s 10(23B) of the Act which is misplaced. As a matter of fact Khadi and Village Industries Commission had issued certificate to the assessee from 11.06.2012 to 31.03.2016 and the assessee is entitled to claim exemption u/s 10(23B) for the AY 2016-17. Further the Khadi and Village Industries Commission, Divisional Officer, Meerut had also written a letter dated 28.01.2019 to the Assessing Officer the ITO, Bijnore (U.P.) to consider the assessee for granting exemption u/s 10(23B) for the AY 2016-17. The contents of the letter are as under: –

7. Therefore, the certificate issued by Khadi & Village Industries Commission clearly show that it relates to the period from 11.06.2012 to 31.03.2016 and followed by the letter issued by the Commission to the ITO, Bijnore, Uttar Pradesh clearly shows that the assessee is entitled to claim exemption u/s 10(23B) of the Act. The reason for denying the exemption by the AO is that the Commission has given certificate to the assessee for more than three years. It is pertinent to note that the time period for which the certificate has to be granted is not within the control of the assessee. In any case it is only a technical violation for which the assessee could not be penalized by denying the exemption otherwise allowable to the assessee. Thus, I hold that the assessee is entitled for exemption u/s 10(23B) of the Act. Accordingly, the Assessing Officer is directed to allow the claim for exemption u/s 10(23B) as claimed by the assessee.

8. In the result, the appeal of the assessee is allowed.

Order pronounced in the open court on 27/05/2022