Income Tax Demand U/s 143 (1) of Income Tax Act, 1961 – Possible Reasons

Yesterday, the dream day for all professionals, when at last clients has provided their details for Tax Audits and my entire professional colleague has rendered their best services to the nation and their clients. With the completion of this ITR Filing season, now Income Tax Department is processing our Filed ITR’s and starts sending intimation U/s 143 (1) of Income Tax Act, 1961.

After successful verification of our ITR, an income tax return has been sent for Processing U/s 143 (1) of Income Tax Act, 1961. Under Section 143 (1), AO can complete the assessment without passing regular assessment order. Basically, the Income-tax department accepts your ITR on a self-declaration basis except for cases that are selected for Scrutiny assessment. Our Filed ITR are processed U/s 143 (1) and an intimation letter is issued after successful verification of our filed ITR.

During this season, I have received many queries from my circle, related to the issuance of Demand U/s 143 (1) of Income Tax Act, 1961. Now, I am trying to elaborate on some reason which may attract demand U/s 143 (1)

1. TDS Credit Mismatch: When we file our ITR, it is mandatory, that we must check our Form 26 AS and TDS details reflected in it. Sometimes, it is observed that we have Form 16/16 A in hand but credit is not reflected in our Form 26AS. Income Tax Department allows credit, which is reflected in Form 26AS.

2. Quoting wrong TAN Number: This is the error commonly done when we file our ITR on the last day. In a Hurry, we quote the wrong TDS number of Deductor, due to which TDS detail does not match with details available with the Income Tax department, which may lead to Demand.

3. Under Reporting of Income: Now, the income tax department is focusing on the maximum utilization of technology and information available with them from outside sources. Like, information received from banks related to Interest on deposits, which you have not considered while filing ITR. File processing your Income Tax Return, the department will add this income to your account which creates demand.

4. Salary from 2 or More Employers: This error is mainly observed in the case of Salaried Class ITR. Sometimes, an employee works with 2 or more employers but at the time of ITR Filing, they do not disclose complete details of their previous employer. If any information is available with the department to your hidden salary details, this will be added to your taxable income.

5. Excess Deduction Claim: This error is commonly done by the assessee, who files their ITR by themselves because they are not fully aware of Income Tax Provision and claims excess deductions in comparison to their permissible limit.

6. Software Utility Error: This error comes in an exceptional situation when Software utility malfunctions. Recently, a case comes to us, in which software calculated wrong Tax liability and ITR is also submitted and processed, due to which demand is generated U/s 143 (1) of Income Tax Act.

7. Disallowance under Tax Audit Report: Sometimes, our Tax Auditor disallowed some expenses which are not admissible as per Income Tax Law and they report such disallowance in their Tax Audit Report. If assesses does not consider these disallowances while filing their ITR, then this may lead to demand.

Above are commonly observed error which invites demand U/s 143 (1) of Income Tax Act, 1961

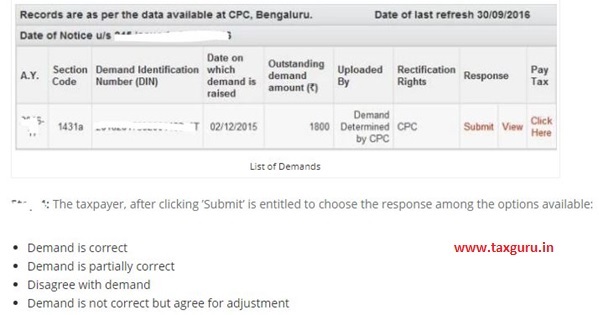

If we received any demand intimation, then we have to respond to this intimation within 30 days. In case, no response is received within 30 days, it is assumed that you have accepted that demand.

Caution: While replying to such demands (Acceptance, Denying Demand), it is advised to go through the provision of the Income Tax Act or Consultant Professional/ Tax Expert. Because, sometimes it is observed that, wrong replying to notice may lead to Scrutiny Notice.

This article is for the purpose of information and shall not be treated as a solicitation in any manner and for any other purpose whatsoever. It shall not be used as a legal opinion and not be used for rendering any professional advice. This article is written on the basis of the author’s personal experience and provision applicable as on the date of writing of this article. Adequate attention has been given to avoid any clerical/arithmetical error, however; if it still persists kindly intimate us to avoid such error for the benefits of other readers.

The Author can be reached at mail –shivsharma786@gmail.com and Mobile/Whatsapp – 9911303737/ 9716118384

Author Bio

Sir i submitted 10e form but the it department not consider this .

Credit mismatch is the biggest problem and we, the assessees, are penalised for someone else’s fault. Inspite of Delhi High Court Orders the CBDT appears to be bent upon collection and not genuine difficulty of the assessee. Some rectification and claim process needs to be put in place

The 143(1) processing authorities, since ignorance of the fact that any addition to the returned income and consequent demand in tax should be sufficiently informed pre-hand to the assessee. If only when the riposte is not prima-facie acceptable to the assessing authorities by virue of the provisions of the Income-tax Act, then the demand is raisible. Otherwise the intimation u sec. 143(1) is bad in law

if it is an amount compared to total tax pay it and forget about it

2. Once I made a minor mistake in the TAN of the deductor while copying from 26AS but amount is correct. Hope income tax itself rectify the TAN as they can see mky26AS. Perhaps in the pre-filled return the details are automatically copied from 26AS though I have to check.

some clarity what data is automatically copied in the pre-filled form?