After the passage of more than 2 Years of GST Implementation, now GST Department becomes active in relation to GST Defaulters and starts cancelling GST Registration of GST Defaulters which may be in form GST Return Defaulters, GST Bogus Dealers issuing Fake GST Invoices etc. In Today’s article, we will discuss GST Cancellation and Revocation Process and activities which lead to GST Registration termination and steps to be taken, if your GST Registration is cancelled, and you want to continue same GST Number for your business activities.

Process of GST Cancellation is governed by Sec-29 of CGST Act, 2017. GST Cancellation may be suo motto by GST Officer or against in response to an application filed by GST Registered person. GST registration may be cancelled in the following situations:

- The business has been discontinued (reason may be the death of the proprietor, transfer of business in form amalgamation, demerger)

- Change in constitution of business

- GST Registered person is not mandatorily, liable to get registered under GST, (reason may be turnover of business goes below the threshold limit)

- When GST Registered person contravenes the provisions of the Act

- When GST Registered person does not file his GST Return

- When GST Registration has been obtained by means of fraud, willful misstatement or suppression of facts

- When a person takes Voluntary GST Registration and after registered under GST, does not commence business within 6 months from the date of GST Registration, then GST Officer has the power to cancel the GST Registration

As per Rule 20 of Central GST Rules, 2017, if GST registered person wants to cancel its GST voluntarily, then he has to File GST cancellation request in FORM GST REG-16 and has to provide required details correctly. Providing inaccurate figure/detail may lead to rejection of your cancellation request.

Note: As per Section 29 (3) of CGST Act, 2017, cancellation of GST Registration shall not affect the liabilities arising before the date of GST Cancellation. Due care must be given that; the registered person is wholly responsible for all acts done before GST Cancellation even if GST Cancellation order determines zero liability.

When GST Officer has reason to believe that the registration of a person is liable to be cancelled under section 29, then he shall issue a show-cause notice in Form GST REG -17

The registered person has to submit his reply within the prescribed time period in Form REG -18

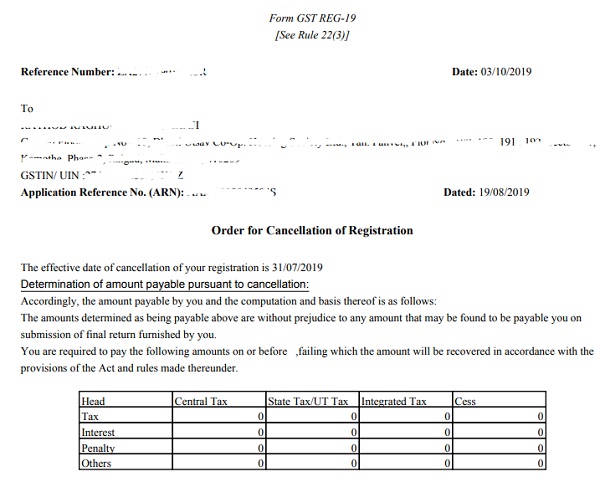

If the GST Officer is not satisfied by the reason of registered person as replied in Form REG -18 in relation to Show cause notice of GST Cancellation, then he will issue GST Cancellation order on Form GST REG-19 and if officer is satisfied by reply submitted by registered person then he shall drop the proceedings and pass an order in Form GST REG-20.

When GST Registration has been cancelled by GST Officer in response to the application filed by a registered person, and the registered person wants to start its GST Registration again, then he has to apply for fresh GST Registration.

However, if GST Registration of any registered dealer is cancelled by GST officer on his own motion, the registered person has the option to apply for Revocation of Cancellation of registration, which is governed by Sec-30 of CGST Act, 2017. If we want, Revocation of cancellation of registration, then we have to submit our application in FORM GST REG-21 to GST Officer within 30 days from the date of service of the cancellation order.

Note: No application for revocation shall be filed, if the registration has been cancelled for the failure of the registered person to furnish returns unless such returns are furnished and any taxes due have been paid.

After the receipt of Revocation Request, in Form GST REG-21, if the officer is satisfied by the reason/ grounds for revocation of GST Registration, then he shall revoke the cancellation of registration in FORM GST REG-22

And if the reply submitted by registered person is not satisfactory, the GST Officer may pass an order for rejection of application for revocation of cancellation and pass order in FORM GST REG-22, here it is to be noted that, GST Officer has to issue a show cause notice in FORM GST REG-23, to the applicant, asking the reason, why the application submitted for revocation under sub-rule (1) of Rule 23 of Central GST Rules 2017 should not be rejected and the applicant shall furnish his reply in Form GST REG-24.

Caution: If you are a GST Registered person dealing properly and having stock in hand and by any mistake (due to unawareness of GST law) your GST number is cancelled, it is suggested that before proceeding towards submitting any reply to GST Officer, please make sure that, you must have adequate knowledge of GST law, or consult GST Expert, because nowadays, GST Department is very strict in GST Cancellation and Revocation Process, a wrong reply may cancel your GST Number which may be harsh to the registered person according to its Stock holding and its GST liability on his stock in hand.

This article is for the purpose of information and shall not be treated as a solicitation in any manner and for any other purpose whatsoever. It shall not be used as a legal opinion and not be used for rendering any professional advice. This article is written on the basis of the author’s personal experience and provision applicable as on date of writing of this article. Adequate attention has been given to avoid any clerical/arithmetical error, however; if it still persists kindly intimate us to avoid such error for the benefits of other readers.

The Author “CA. Shiv Kumar Sharma” can be reached at mail –shivsharma786@gmail.com and Mobile/Whatsapp – 9911303737/ 9716118384

Author Bio

Hi sir,

GST number got cancelled under suo-moto on October 2020..(this registration not revoked)

And taken fresh registration on Jan 2021.

But from October to December made sales in old GST number…

My doubt is how to file that sales made under GST from October to December

sir,

Sir

my revocation of cancellation application has been rejected what should i do & what’s the further process

Thanking you

Dear Sir

In this case you can file Appeal against this Rejection Order

If still you have any Query, then you can contact us at – 9911303737/ 9716118384

Regards

CA. Shiv Kumar Sharma

My gst is cancelled I filled and apply for revocation through online

But not reopen the gst

Any other solutions for that ??

REG 21 Filed on 11/05/2021 ,but not yet received any reply,how many days will wait

i want to cancel my gst registration i have also filed the request its been a month but there is no revert back from the officers. What am i suppose to do

Dear sir my gst registration has been canceled from my side in 2019 because my business is not growing but I want to start my own business with gst number you tell me sir how to start revocation my gst number

I received Cancelation order dated 17/12/2020 for my company’s GST No, after that I filled GSTR3B and GSTR1 with due dates of on or before 17/12/2020. But I’m still not able to fill the application for Revocation of cancellation. Need help

My GST number is Cancelled suo-moto due to not filing return from February 2019.what Can i do for starting again my gst number there were no transaction in company

DEAR SIR,

IF GST NUMMBER SUSPENDED THAN WHAT IS THE PROCEDURE AND IT IS NOT CANCELLED IT IS SUSPENDED BY DEPARTMENT DUE TO NOT FILED RETURN FOR 15 MOTNHS

My GST number is Cancelled suo-moto due to not filing return from February 2019.what Can i do for starting again my gst number

Hello

Last return we filed of our client is November,2019, but couldn’t file GSTR3B return as GST number got cancelled suo-moto. We also reply on GST portal to officer but officer not appropriate of reply. Please let us know what we give response to GST officer.

Hello Sir,

Last return we filed of our client is November,2019, but couldn’t file GSTR3B return as GST number got cancelled suo-moto. We also reply on GST portal to officer but officer not appropriate of reply. Please let us know what we give response to GST officer.

Last return we filed of our client is November,2019, but couldn’t file GSTR3B return as GST number got cancelled suo-moto. We also reply on GST portal to officer but officer not appropriate of reply. Please let us know what we give response to GST officer.

For any type of issue relating to revocation of cancelled GSTIN or getting a fresh one please contact on 7717768987.

At your service/support 24*7

Hello

Last return we filed of our company is of April’2018, We have paid GST for FY 2018-19 but couldn’t file GSTR 3B return as GST number got Cancelled.

Please let us know what can I do to reactivate GST number.

I had migrated from VAT to GST. Since I did not have any business, I surrendered my temporary registration on 23/12/2017 and got acknowledgement from Dept. I was not aware I had to submit Nil Returns.

Now I wish to restart my business. When I applied against the same PAN card it is not possible.

Please advise me.

Sir, for one of my client gst number is cancelled on 19/04/2020 with effect from 01.07.2017. On 19.02.2020 officer has issued show cause notice by giving reply time on 26.02.2020. this SCN is issued on gst portal nd no physical copy is received at registered address nd never any call is made. Only on portal SCN is posted. Assessee did not notice it’s Portal nd time limit is expired nd in lockdown period cancellation order is passed with restropective effect from 01.07.2017.

Reason for cancellation mentioned in SCN is purchase from bogus firm during fy 16-17.

Please note in fy 16-17 vat was applicable not gst. Gst was implemented from July 17. If department has noticed any bogus purchase for vat period then provision of vat will be applicable nd his assessment in vat upto fy 16-17 is complete. Section 29(2) is applicable for default in gst compliance.

We had filed revocation application by mentioning the same reason that bogus purchase noticed by department is related to pre gst regime , then gst number must not be cancelled. If any action is required to be taken for bogus purchase related to vat period then vat assessment is required to be reopened.

Sir I had not received any reply for revocation application till date. We had filed application for revocation within 30 days nd reply is not received.

Sir one more thing on SCN no din no is mentioned. Nd no din is mentioned on cancellation order only ref no is mentioned which start with like this ZA …….

Sir please advise us what I should do to start this number and tell whether can officer cancel the gst number with restropective effect for default of pre gst regime i.e vat period. Please guide me.

My GST registration cancelled before 8th month causes for return not filed .In this circumstances how do I revoke my GST Registration?

Pls. Serve me online version in my said E-mail I’d.

Sir I have filled all my pending returns with the applicable late fees and applied for revocation of cancellation but still my application was cancelled , can you please help me with this

We registerd our gst on 2017. Only 2 months returns filed. Got cancelled on nov 2019. What we gave bills in this cancelled

Gst. What to do next. Hoe to revoke the cancelled gst. Late fees is more than 3 lakhs. We are not in a situation to pay this huge amount what to do??

Tax officer has cancelled my GSTIN with effect from 20.11.2019. when I go to apply for revocation on 01.06.2020 it show a massage that please file all pending return by 01.06.2020. it means 30 days period over. Can I file all pending return and still can apply fore revocation even after 30 days. Please suggest I m in trouble

Sir, in gst side the revocation option not be shown in my account….

Sir my GST no is cancelled and i have applied for revocation after 30 days officer has rejected my application for revocation. thereafter as per press release till 30th june one time opportunity is given in which we can revoke even when 30 days are over however when i am applying for revocation again it is showing that i have already applied for revocation and it is rejected by officer please suggest the course of action.

Dear Sir,

I have filed all the pending returns up to the date of cancellation order and application for revocation is also filed. Now since there is a lockdown in the country I’m not able to visit the tax authorities and produce before them the application for revocation, subsequent to which only I will be able to ask them revoke the blocked account so that I can continue with the billings, My question to you is “ Is there any way out, like deemed approval of revocation or can I place this revocation application and continue with the Invoicing, will it hold valid?

Dear Sir, What should we Write in Reason for Revocation of Cancellation

if within 30 days the application is not accepted by the officer can the number be stated by applying to a higher officer?

How can I activate my Cancelled GST number after 30 days?

sir we applied volunterly for cancellation of my gstin and approved by the tax officer. now our gstin is stands in cancelled status. how we revoke my gstin. please clarify

sir we applied volunterly for cancellation of my gstin and approved by the tax officer. now our gstin is stands in cancelled status. how we revoke my gstin. please clarify

we filed cancellation of my gstin by voluntery and accepted the tax officer and my gstin now stands in cancelled status. how we revoke my gstin

Tax officer has cancelled my GSTIN with effect from 22.11.2019. when I go to apply for revocation on 24.12.2019 it show a massage that please file all pending return by 24.12.2019. it means 30 days period over. Can I file all pending return and still can apply fore revocation even after 30 days. Please suggest I m in trouble

sir my gst registration cancel 15/07/2019 appeal time limit postion clear

I am not able to find any link for the application of the revocation of cancellation of the registration. Please help

Sir

my revocation of cancellation application has been rejected what shud i do & what’s the further process

Thanking you

govt. should erode late fees on all gstr -3b,and other return so that the dealers should file their return easily without any burden