In Indirect Taxes Regime tax/duty was charged on various taxable events like manufacture, sale, rendering of service, purchase, entry into a territory of State etc. This have been done away in GST with in favour of just one taxable event i.e. ‘Supply‘. The taxable event in GST is supply of goods or services or both. The constitution defines “goods and services tax” as any tax on supply of goods, or services or both except taxes on the supply of the alcoholic liquor for human consumption. As per Article 246A of the Constitution confers concurrent powers to both, Parliament and State Legislatures to make laws with respect to GST i.e. Central Tax (CGST) and State Tax (SGST) or Union Territory Tax (UTGST). However, clause 2 of Article 246A read with Article 269A provides exclusive power to the Parliament to legislate with respect to inter-State trade or commerce i.e. integrated tax (IGST).

As per Section 7 of CGST Act Scope of supply

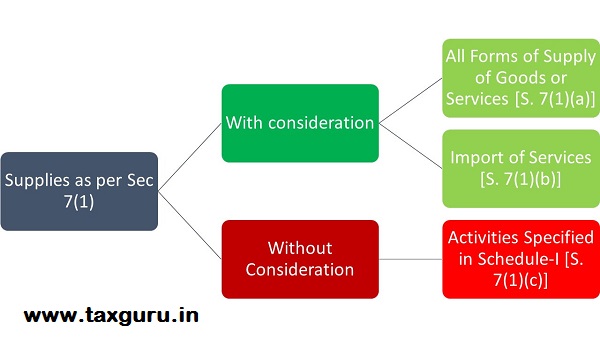

(1) For the purposes of this Act, the expression “supply” includes––

(a) all forms of supply of goods or services or both such as sale, transfer, barter, exchange, licence, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business;

(b) import of services for a consideration whether or not in the course or furtherance of business;

(c) the activities specified in Schedule I, made or agreed to be made without a consideration; and

(d) the activities to be treated as supply of goods or supply of services as referred to in Schedule II.

(2) Notwithstanding anything contained in sub-section (1), ––

(a) activities or transactions specified in Schedule III; or

(b) such activities or transactions undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities, as may be notified by the Government on the recommendations of the Council, shall be treated neither as a supply of goods nor a supply of services.

(3) Subject to the provisions of sub-sections (1) and (2), the Government may, on the recommendations of the Council, specify, by notification, the transactions that are to be treated as—

(a) a supply of goods and not as a supply of services; or

(b) a supply of services and not as a supply of goods.

The term, “supply” has been inclusively defined in the Act.

Further Section 7(1) includes Supplies both Supply of Goods/Services with consideration and without consideration.

When we summarize the whole Section, it is as follows:

I would like to discuss some relevant case laws for further understanding:

- “Additional Bonus” towards early payments (in case of Del Credere Agent) is not in nature of “Supply”. – K.K. Polymers (AAR – Rajasthan)

- “e-Procurement Transaction Fee” collected on behalf of government department is not liable as this amounts to services rendered by State Government. – Andhra Pradesh Technology Services Ltd. (AAR – Andhra Pradesh)

- Where funds are provided by the Government under contract for construction of road, the funds provided in the form of grants are entitled for exemption under Notification No. 12/2017 – Central Tax (Rate). – NFPC Ltd. (AAR – Uttarakhand)

- Where cheques have been dishonoured and “Cheque Dishonour Fees” is recovered by “Electricity Distributor” company such cheque dishonour fees will be considered as “Supply” and hence leviable to GST. – TP Ajmer Distribution Ltd. (AAAR – Rajasthan)

- Amount received by tenant towards alternate accommodation or delayed possession of new premises would be treated as “Supply” and therefore, GST would be leviable on such amount. – Zaver Shankarlal Bhanushali (AAR – Maharashtra)

Therefore, for a supply to attract GST the supply must be taxable. Taxable supply has been broadly defined and means any supply of goods or services or both which is leviable to tax under the Act. Exemptions may be provided to the specified goods or services or to a specified category of persons / entities making supply.

Also, for a supply to attract GST the place of supply should be in whole of India. The place of supply of any goods or services is determined based on Sections 10, 11, 12 and 13 of IGST Act 2017.

Author Bio