The e-way bill is an essential compliance mechanism under the Goods and Services Tax (GST) regime in India. It ensures seamless movement of goods and prevents tax evasion. This article provides a detailed overview of intra-state e-way bill requirements for tax professionals, including threshold limits, exemptions, notifications, and other relevant details.

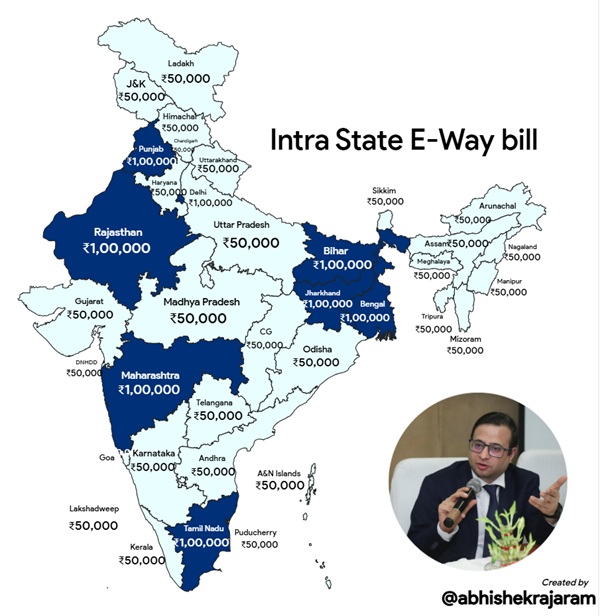

Threshold Limits for E-Way Bill Generation

Consignment Value Above INR 1,00,000:

E-way bills are mandatory for goods exceeding INR 1,00,000 in value in the following states:

- Bihar

- Delhi

- Maharashtra

- Jharkhand

- Tamil Nadu

- West Bengal

- Punjab

- Rajasthan (Threshold limit of INR 2,00,000 for intra-city movements)

Consignment Value Above INR 50,000:

The following states require e-way bills for goods valued above INR 50,000:

- Andhra Pradesh

- Gujarat

- Karnataka

- Madhya Pradesh (No limit for intra-district movement | All goods of any value for intra-district movement)

- Telangana

- Uttar Pradesh, among others.

Not Required:

Goa: E-way bills are not mandatory for the intra-state movement of goods.

General Exemptions from E-Way Bill Requirements

1. Goods with Low Value: Consignments valued below INR 2,000 within the same city or town are exempt from e-way bill requirements.

2. Specific Exempt Goods: Goods such as alcoholic liquor for human consumption, petroleum products, and goods exempted from GST.

3. Customs Supervised Movements: Transit cargo to/from Nepal or Bhutan and goods under customs supervision.

Relevant Notifications and Circulars

State Notifications

Rajasthan:

• Notification F.17 (131-Pt.-II)ACCT/GST/2017/6672 dated 30.03.2021.

• Notification F.17 (131-Pt.-II)ACCT/GST/2017/7713 dated 24.02.2022.

Madhya Pradesh:

• Notification FA 3-08-2018-–-V (18) dated 23.03.2022.

CBIC Circulars

Circular No. 49/23/2018-GST dated 21.06.2018: Provides guidance on detention and confiscation for partial consignment issues.

Circular No. 160/16/2021-GST dated 20.09.2021: Clarifies the requirement of carrying physical copies of invoices during goods transportation.

Additional Compliance Notes

1. Electronic Generation: E-way bills must be generated electronically on the GST portal.

2. Documentation Requirements: The transporter must carry the invoice or bill of supply along with a copy of the e-way bill.

3. Penalties for Non-Compliance: Non-compliance can lead to penalties, detention of goods, and seizure of vehicles.

Key Takeaways for Tax Professionals

- State-Specific Rules: Ensure familiarity with state-specific e-way bill thresholds and exemptions to avoid inadvertent non-compliance.

- Documentation Readiness: Educate clients on maintaining accurate invoices and supporting documents during the transportation of goods.

- Proactive Monitoring: Regularly track updates to notifications and circulars issued by state governments and CBIC.

By adhering to these guidelines, tax professionals can assist businesses in ensuring seamless operations and compliance with GST regulations. For further details or clarification, always refer to the latest notifications and circulars issued by the respective authorities.

Source:- Creating graphic for using IIP Maps

Author Bio