The Ministry of Corporate Affairs (MCA) has taken action against Herox Private Limited for violations under Section 90 of the Companies Act, 2013. The Registrar of Companies (RoC), NCT of Delhi & Haryana, has issued a detailed order of penalty following a thorough investigation and adjudication process.

Herox Private Limited, incorporated on November 21, 2020, with CIN U80902DL2020PTC373493, operates with a significant financial footprint. As of the financial year 2022-23, the company reported a paid-up capital of INR 13,179,850, revenue from operations of INR 1,700,823,480, other income of INR 325,167,490, and a profit of INR 761,596,037. The company also has several shareholders, including significant stakeholders like Bahadur Chand Investments Pvt Ltd and Survam Partners LLP.

Proceedings and Notices

Notice Under Section 206(1)

On February 7, 2024, the RoC issued a notice under Section 206(1) of the Companies Act, 2013, to ascertain the compliance of Herox Pvt Ltd with Section 90 and related rules. The notice sought details on:

- Filing of Form BEN-2 as required under Section 90(4).

- Actions taken to identify Significant Beneficial Owners (SBOs) as per Section 90(4A).

- Compliance with issuing BEN-4 notices.

- Applications moved to the NCLT under Section 90(7).

Company’s Response

Herox Pvt Ltd responded on February 26, 2024, confirming receipt of declarations from beneficial owners in Form BEN-1 and maintaining the register in BEN-3. However, the company admitted that it had not issued BEN-4 notices nor filed applications to the NCLT.

Show Cause Notice and Hearing

Due to the non-filing of Form BEN-2, a show cause notice was issued on March 27, 2024. The company responded on April 24, 2024, admitting delays in filing BEN-2 forms and requesting leniency under Section 446B due to its status as a startup. A hearing was conducted on May 20, 2024, where authorized representatives of the company reiterated their compliance efforts and submitted proof of declarations received from SBOs.

Findings and Adjudication

Determination of Default

The investigation revealed that while Herox Pvt Ltd received declarations from SBOs in a timely manner, it failed to file the necessary e-forms (BEN-2) as required under Section 90(4). This delay constitutes a clear violation of Section 90(11).

Liability of Officers

Both directors, Akshay Munjal (Whole-Time Director) and Suman Kant Munjal, were found liable under Section 2(60) for their roles in the company’s failure to comply with Section 90(4). Their knowledge and participation in company proceedings without objecting to the non-compliance made them accountable.

Relevant Legal Provisions

- Section 90 of the Companies Act, 2013: Mandates declarations from SBOs and filing of returns.

- Section 454(1): Empowers the RoC to impose penalties for violations.

- Section 446B: Provides for lesser penalties for startup companies.

Final Order

As The company did not take any measure to file the e-form BEN-2 in terms of section 90(4) of the Act despite receiving notices in BEN-1 from the SBOs. It was only after the initiation of the proceedings that the relevant e-forms were filed. Thus, there is clearly a “failure” to file in terms of section 90(11) on the part of the company and its officers, which is being reckoned in terms of the three filings of BEN-2 made by the company. In view of the same MCA imposes total Penalty of Rs. 9 Lakh on Company and its directors.

*****

GOVERNMENT OF INDIA

MINISTRY OF CORPORATE AFFAIRS,

OFFICE OF REGISTRAR OF COMPANIES,

NCT OF DELHI & HARYANA

4TH FLOOR, IFCI TOWER, 61, NEHRU

PLACE, NEW DELHI -110019

ORDER OF PENALTY FOR VIOLATION UNDER SECTION 90 OF THE COMPANIES ACT, 2013 IN THE MATTER OF HEROX PRIVATE LIMITED (CIN: U80902DL2020PTC373493) (SRN: 100090505)

1. Appointment of Adjudicating Officer:

Ministry of Corporate Affairs vide its Gazette Notification No. A-42011/112/2014-Ad.II, dated 24.03.2015 appointed Registrar of Companies Adjudicating Officer in exercise of the powers conferred by section 454(1) of the Companies Act, 2013 (hereinafter known as as Penalties) Rules, 2014 (hereinafter known as “Rules”) the provisions of this Act.

2. Company: –

Whereas HEROX PRIVATE LIMITED (hereinafter known as “company” or “subject company”) having CIN U80902DL2020PTC373 93 is a Private Limited Company registered on 21.11.2020 with this office having registered office address at Plot No 2, Lado Sarai Institutional Area, New Delhi -110030. The financial & other details of the subject company for immediately preceding F.Y 2022-23 as available on MCA-21 portal is stated as under:

| S. No. | Particulars | Details |

| 1. | Paid up capital (INR in Thousands) | 1,31,79,850 |

| 2. | a. Revenue from operation (INR in Thousands) | 17,00,82,348 |

| b. Other Income (INR in Thousands) | 3,25,16,749 | |

| c. Profit for the Period (INR in Thousands) | 76,15,96,037 | |

| 3. | Whether company has a Holding Company? | YES |

| 4. | Whether company has a Subsidiary Company? | YES |

| 5. | Whether company registered under Section 8 of the Act? | No |

| 6. | Whether company registered under any other special Act? | No |

(i) LIST OF SHAREHOLDERS AS ON MARCH 31, 2023

| S.no | Shareholder’s Name | Types of shares | No of shares |

| 1 | Suman Kant Munjal |

Equity | 5,000 |

| 2 | Akshay Munjal | Equity | 5,000 |

| 3 | Bahadur Chand Investments Private Limited |

Equity | 5,94,059 (45%) |

| 4 | Survam Partners LLP | Equity | 2,98,019 (22%) |

| 5 | Pawan Munjal Family Trust | Equity | 1,65,675 (12%) |

| 6 | Brij Mohan Lal Om Prakash | Equity | 2,50,232 |

| Total | 13,17,985 |

(ii) Directorship:

| DIN/PAN | Name | Nation | Date of

appointment |

Current Designation |

| 00002803 | Suman Kant Munjal | India | 21.11.2020 | Director |

| 01347846 | Akshay Munjal | India | 21.11.2020 | Whole time director |

3. The details of the proceedings:

A. Issuance of a notice under section 206(1)

A notice was issued to the subject company under section 206(1) of the Act on 07.02.2024 to ascertain compliance of section 90 of the Act and rules made thereunder. The notice was issued for broadly ascertaining the following compliances:

i. Whether the company had filed form BEN-2 in terms of section 90(4) of the Act. If yes, provide a copy of the s me. If no, provide reasons with supporting documents.

ii. Provide details of all the actions taken by the company to identify its Significant Beneficial Owner in terms of section 90(4A) of the Act.

iii. Did the company comply with the mandatory compliance of issuing a BEN-4 notice as required in rule 2A (2) of the Companies (Significant Beneficial Owners) Rules, 2018. If no, provide re sons.

iv. Provide the details of the application moved by the company to the NCLT in terms of section 90(7) of the Act.

B. Reply submitted by the company:

In response to the above notice a reply was received on 26.02.2024 from the company, wherein it was inter alia stated as under:

i. The company has received the declaration pursuant to sub-section (1) of Section 90 of the Act from the Beneficial Owners in the Form BEN-1 at the time of creation of interest in the company. The copies of the form BEN-1 along with the register maintained by the company in BEN-3 are enclosed herewith.

ii. The company has not issued any notice in BEN-4.

iii. Since there was no notice issued by the company in Form BEN-4, there was no application moved to the NCLT in terms 7 of Section 90(7) of the Act r/w rule 7 of the Companies (Significant Beneficial Owners) Rules 2018.

iv. Survam Partners LLP is a shareholder of the company holding 22% of shares in the company as on 31.03.2023.

v. M/s. Pa wan Munjal Family Trust is a private discretionary trust.

vi. The Company is registered as a Startup Company vide DPIIT Registration Certificate No. DIPP79604. A copy of the registration certificate is enclosed. Accordingly, as per the provisions of Section 446B of the Companies Act, 2013, your good self is hereby requested to provide the company with an opportunity to rectify any non-compliance, if any, in the subject matter by waiving off any penalties.

C. Show Cause Notice issued under section 90 of the Act:

In light of the above and since no form BEN-2 was filed by the company, a show cause notice was issued to the subject company dated 27.03.2024 wherein it was asked to show cause as to why action under Section 90 of the Act should not be initiated against it. The Company submitted its reply on 24.04.2024 which inter-alia states as under:-

i. company has received the required declarations pursuant to sub section (1) of section 90 of the Act from all the beneficiaries/ owners in form BEN-1 at the time of creation/modification of their respective interest in the company. Therefore, partners of Survam Partners LLP, Trustees/Beneficiaries of Pawan Munjal Family trust and partners of BMOP have not violated the provisions of sub-section (1) of section 90 of the Companies Act, 2013.

ii. The company couldn’t file BEN-2 due to inadvertent reasons and therefore has initiated the process of filing form BEN-2 to comply with the provisions of the Act and Companies (Significant Beneficial Owners) Rules 2018.

iii. It is further submitted that the company is registered as a Startup Company vide DPIIT Registration Certificate No. DIPP79604. Accordingly, as per the provisions of Section 4468 of the Companies Act, 2013, your good self is hereby prayed to provide the company with an opportunity to rectify the non-compliance by way of filing applicable BEN-2 and waive off any penalties on the company and its officer.

D. Providing an opportunity of being heard to the company

I. The reply dated 24.04.2024 as furnished by the company was perused and accordingly, a hearing was scheduled on 20th May 2024. Mr. Sushil Kumar Singh, CA and Mr. Kundan Agrawal, CS, authorized representatives of the Company and SBOs appeared for hearing and submitted as under:

(a) Company have filed 3 BEN-2 e-forms for declaration of 11 SBOs in relation to the company. They have submitted that in all cases, the SBOs had given the declaration to the Company in a timely manner but there was a delay on the part of the company to file BEN-2, which may be condoned.

(b) In addition, they have submitted beneficial that on account of changes in the beneficial ownership they have additionally filed 57 more BEN-2 forms to reflect the changes in beneficial ownership from time to time, which reflects the compliant nature of the company

(c) Further, considering the importance of the compliance of section 90, of the company/group has deputed an individual who is professionally qualified to oversee the compliances

II. The authorized representatives were as asked to submit proof of receipt of declarations in BEN-1 by the SBOs.

III. The proof of physical receipt of the declaration was submitted by the company.

IV. Following persons have been declared as SBOs by the company in the three eforms BEN-2 filed by it on 03.05.2024:

| SI. No. |

Name of the SBO |

| 1. | Pawan Munjal |

| 2. | Aniesha Munjal |

| 3. | Annuvrat Munjal |

| 4. | Supria Munjal |

| 5. | Vasudha Dinodia |

| 6. | Suman Kant Munjal |

| 7. | Renuka Munjal |

| 8. | Ujjwal Munjal |

| 9. | Akshay Munjal |

| 10. | Vidur Munjal |

| 11. | Renu Munjal |

4. Determination of default

I. Section 90(11) of the Act categorically penalizes the failure on the part of the company to disclose the declarations received from the SBOs. In this case, the company in its reply has shown that it has received the declarations from different SBOs on 27.01.2021, 24.03.2021 and 29.04.2022 in compliance with section 90(1). However, the company did not take any measure to file the relevant e-form in terms of section 90(4) of the Act. It was only after the initiation of the proceedings that the relevant e-forms were filed. Thus, there is clearly a “failure” to file in terms of section 90(11) on the part of the company and its officers.

II. It is seen that both the directors of the company namely Shri Akshay Munjal [whole-time director] and Shri Suman Kant Munjal are also SBOs in relation to the company. Under section 2(60), the whole-time director would get covered as an officer in default. As far as the other director is concerned, he is also an SBO in relation to the company, and it is the case of the company that he had filed his declaration as per section 90(1) in time with the company. Now, section 2(60)(vi) which reads as follows, arrays the following person as an officer in default:

every director, in respect of a contravention of any of the provisions of this Act, who is aware of such contravention by virtue of the receipt by him of any proceedings of the Board or participation in such proceedings without objecting to the same, or where such contravention had taken place with his consent or connivance

III. Thus, even though Shri Suman Kant Munjal is not a whole-time director of the company, since he had submitted his declaration under section 90(1) to the company stating himself to be an SBO, it is presumed that he had knowledge about the requirement of filing this information with the registry under section 90(4). Thus, in this particular case, even Shri Suman Kant Munjal is liable for the violation under section 90(11) of the Act.

5. The relevant provisions for adjudication

Section 90 – Register of significant beneficial owners in a company are as follows:

(1) Every individual, who acting alone or together, or through one or more persons or trust, including a trust and persons resident outside India, holds beneficial interests, of not less than twenty-five per cent. or such other percentage as may be prescribed, in shares of a company or the right to exercise, or the actual exercising of significant influence or control as defined in clause (27) of section 2, over the company (herein referred to as “significant beneficial owner”, shall make a declaration to the company, specifying the nature of his interest and other particulars in such manner and within such period of acquisition of the beneficial interest or rights and any change thereof, as may be prescribed:

(2) Every company shall maintain a register of the interest declared by individuals under sub-section (1) and changes therein which shall include the name of individual, his date of birth, address, details of ownership in the company and such other details as may be prescribed.

(4) Every company shall file a return of significant beneficial owners of the company and changes therein with the Registrar containing names, addresses and other details as may be prescribed within such time, in such form and manner as may be prescribed.

(4A) Every company shall take necessary steps to identify an individual who is a significant beneficial owner in relation to company and require him to comply with the provisions of this section.

(5) A company shall give notice, in the prescribed manner, to any person (whether or not a member of the company) whom the company knows or has reasonable cause to believe-

(a) to be a significant beneficial owner of the company.

(b) to be having knowledge of the identity bf a significant beneficial owner or another person likely to have such knowledge; or

(c) to have been a significant beneficial Owner of the company at any time during the three years immediately preceding the date on which the notice is issued,

and who is not registered as a significant beneficial owner with the company as required under this section.

(10) If any person fails to make a declaration as required under sub-section (1), he shall be liable to a penalty of fifty thousand rupees and in case of continuing failure, with a further penalty of one thousand rupees for each day after the first during which such failure continues, subject to a maximum of two lakh rupees.]

(11) If a company, required to maintain register under sub-section (2) and file the information under sub-section (4) or required to take necessary steps under sub-section (4A), fails to do so or denies inspection as provided therein, the company shall be liable to a penalty of one lakh rupees and in case of continuing failure, with a further penalty of five hundred rupees for each day, after the first during which such failure continues, subject to a maximum of five lakh rupees and every officer of the company who is in default shall be liable to a penalty of twenty-five thousand rupees and in case of continuing failure, with a further penalty of two hundred rupees for each day, after the first during which such failure continues, subject to a maximum of one lakh rupees.

(12) If any person wilfully furnishes any false or incorrect information or suppresses any material information of which he is aware in the declaration made under this section, he shall be liable to action under section 447.

Section 446B of the Act:

446B. Lesser penalties for certain companies.–Notwithstanding anything contained in this Act, if penalty is payable for non-compliance of any of the provisions of this Act by a One Person Company, small company, start-up company or Producer Company, or by any of its officer in default, or any other person in respect of such company, then such company, its officer in default or any other person, as the case may be, shall be liable to a penalty which shall not be more than one-half of the penalty specified in such provisions subject to a maximum of two lakh rupees in case of a company and one lakh rupees in case of an officer who is in default or any other person, as the case may be.

The relevant provision Companies (Significant Beneficial Owners) Rules, 2018:

Rule 3

3. Declaration of significant beneficial ownership in shares under section 90.-

(1) Every significant beneficial owner shall file a declaration in Form No. BEN-1 to the company in which he holds the significant beneficial ownership on the date of commencement of these rules within ninety days from such commencement and within thirty days in case of any change in his significant beneficial ownership.

(2) Every individual, who, after the commencement of these rules, acquires significant beneficial ownership in a company, shall file a declaration in Form No. BEN-1 to the company, within thirty days of acquiring such significant beneficial ownership or in case of any change in such ownership.

Rule 4

4. Return of significant beneficial owners in shares-

Where any declaration under rule 3 is received by the company, it shall file a return in Form No. BEN-2 with the Registrar in respect of such declaration, within a period of thirty days from the date of receipt of declaration by it, along with the fees as prescribed in Companies (Registration offices and fees) Rule, 2014.

6. Adjudication of penalty: –

i. The company did not take any measure to file the e-form BEN-2 in terms of section 90(4) of the Act despite receiving notices in BEN-1 from the SBOs. It was only after the initiation of the proceedings that the relevant e-forms were filed. Thus, there is clearly a “failure” to file in terms of section 90(11) on the part of the company and its officers, which is being reckoned in terms of the three filings of BEN-2 made by the company.

ii. The subject company is a startup company. Hence, the benefit of section 446B would be applicable.

iii. Now in exercise of the powers conferred vide Notification dated 24th March 2015, and having considered the reply submitted and hearings held in the matter, I do hereby impose the penalty on the company and its officers in default as follows:

TABLE I

| Violation section and penal provision |

Period of default (in day) | Penalty imposed on | Calculation of penalty amount 90(11) as per section (In Rs.) | Penalty imposed as per Section 446B (In Rs) |

| A | B | C | D | E |

| Section 90(4) r/w rule 4 of the SBO Rule, 2018.

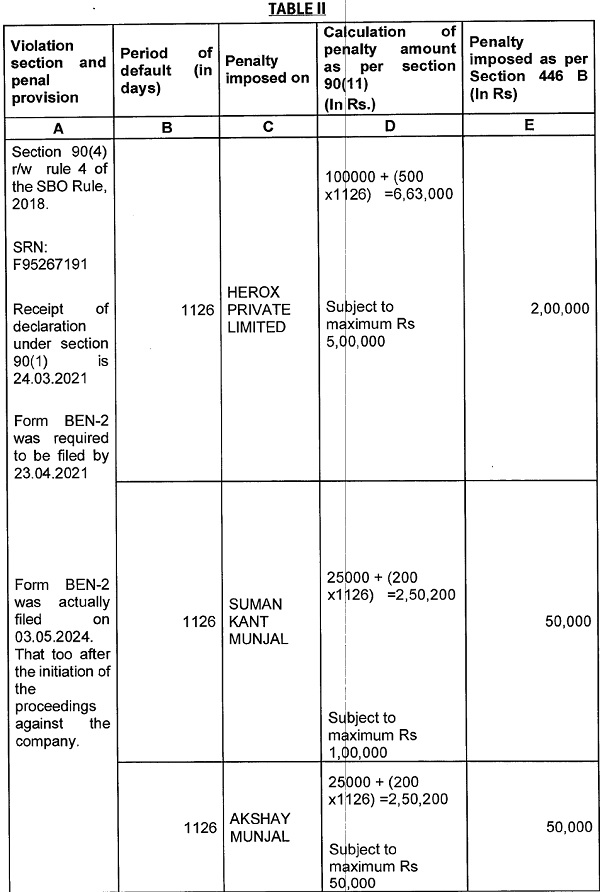

SRN: F95265161 Receipt of declaration under section 90(1) is 27.01.2021 Form BEN-2 was required to be filed by 26.02.2021 Form BEN-2 was actually filed on 03.05.2024. That too after the initiation of the proceedings against the company. |

1162 | HEROX PRIVATE LIMITED | 100000 + (500×1162) =6,81,000

Subject to maximum Rs 5,00,000 |

2,00,000 |

| 1162 | SUMAN KANT MUNJAL | 25000 + 200 x1162=2,57,400

Subject to |

50,000 | |

| 1162 | AKSHAY MUNJAL | 25000 + 200 x1162 =2,57,400

Subject to |

50,000 |

TABLE III

| Violation section and penal provision | Period of default (in days) | Penalty imposed on | Calculation of penalty amount as per section 90(11) (In Rs.) | Penalty imposed as per Section 446 B (In Rs) |

| A | B | C | D | E |

| SRN:

F95288544 Receipt of declaration under section 90(1) is 29.04.2022 Form BEN-2 was required to be filed by 28.05.2022 Form BEN-2 was actually filed on 05.05.2024. That too after the initiation of the proceedings against the company. |

708

|

HEROX PRIVATE LIMITED |

100000+(500×708) = 4,54,000

Subject to |

2,00,000 |

| 708 | SUMAN KANT MUNJAL | 25000+(200x 708) = 1,66,600

Subject to |

50,000 | |

| 708 | AKSHAY MUNJAL | 25000+(200x 708) = 1,66,600

Subject to |

50,000 | |

a. Names of parties as mentioned in Table I, II and III above are hereby directed to pay the penalty amount as per column no. ‘E’ therein, in each case.

b. The said amount of penalty shall be paid through online by using the website www.mca.gov.in (Misc. head) in favor of “Pay & Accounts Officer, Ministry of Corporate Affairs, New Delhi within 90 days of receipt of this order, and intimate this office with proof of penalty paid.

c. Appeal against this order may be filed with the Regional Director (NR), Ministry of Corporate Affairs, B-2 Wing , 2nd Floor, Paryavaran Bhawan, CGO Complex, Lodhi Road, New Delhi-110003 within a period of sixty days from the date of receipt of this order, in Form ADJ [available on Ministry website www.mca.gov.in] setting forth the grounds of appeal and shall be accompanied by a certified copy of the order. [Section 454(5) & 454(6) of the Act read with Companies (Adjudicating of Penalties) Rules, 2014].

d. Your attention is also invited to section 454(8) of the Act in the event of non-compliance of this order.

(Pranay Chaturvedi, ICLS)

Registrar of Companies

NCT of Delhi & Haryana

No. ROC/D/Adj/Order/Section 90/Herox/2757

Date : 09/07/2024

To,

HEROX PRIVATE LIMITED

Plot No 2, Lado Sarai Institutional Area,

New Delhi-110030.

2. SUMAN KANT MUNJAL

K-5 Lane W12 Western Avenue, Sainik Farms,

New Delhi-110062.

3. AKSHAY MUNJAL

K-5, W-12, Western Avenue, Sainik Farms Khanpur,

New Delhi-110062.

Copy to:

The Regional Director (NR), Ministry of Corporate Affairs, B-2 Wing, 2nd Floor, Pt. Deendayal Upadhyay Bhawan, CGO Complex, Lodhi Road, New Delhi-110003.