Granting of loans, giving guarantees or providing securities are transactions that are routinely take place in the course of business of a company though such transactions expose the company to a certain level of risk. Section 185 covers such transactions which are between a company and a director or a person in whom the director is interested. Author has tried to make an analysis of the Section 185 of the Companies Act, 2013 with practical aspects.

Section 185 of the Companies Act, 2013 is divided into four parts. In the first part, sub section (1) imposes a complete bar for granting loans to, providing guarantee or security for the loans taken by certain persons. In the second part, sub-section (2) permits certain transactions subject to certain exceptions and exemptions. In the third part in sub-section (3), certain exemptions are given and in the fourth part in sub-section (4), consequences of contraventions of provisions of section 185 are given. For the proper understanding of the spirit behind section 185, it is pertinent to refer to their bare text along with detailed analysis of each provision.

| Legal text of sub-section (1) of Section 185

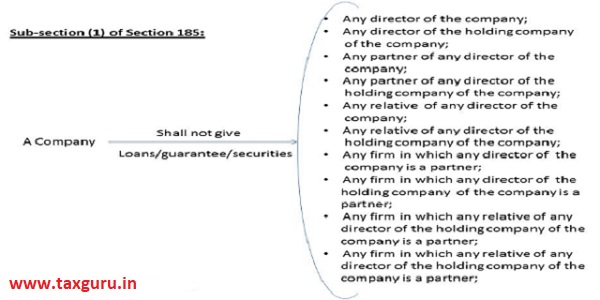

No company shall, directly or indirectly, advance any loan, including any loan represented by a book debt to, or give any guarantee or provide any security in connection with any loan taken by,— (a) any director of company, or of a company which is its holding company or any partner or relative of any such director; or (b) any firm in which any such director or relative is a partner. |

Page Contents

Analysis of sub-section (1) of Section 185:

> As discussed above, sub-section (1) is a prohibitory part of section 185 of the Companies Act, 2013 which provides that a company shall not advance any loan, including any loan represented by a book debt or give any guarantee or provide any security in connection with any loan to any director of the company or of holding companies or partner or relative of any such director or any firm in which any such director or relative is a partner.

> The term relative has been defined under Section 2(76) relative’’, with reference to any person, means anyone who is related to another, if— (i) they are members of a Hindu Undivided Family; (ii) they are husband and wife; or (iii) one person is related to the other in such manner as may be prescribed;

Rule 4 of Companies(Specifications and definition details) Rules, 2014 provides that a person shall deemed to be relative of another, if he or she is related to another in the following manner, namely:-

(1) Father including step-father.

(2) Mother including step-mother.

(3) Son including the step-son.

(4) Son’s wife.

(5) Daughter’s husband.

(6) Brother including the step-brother.

(7) Sister including step-sister.

> The ambit of the section is very wide and it applicable on every company, both private and public companies, it covers all types of companies. The word Company has been defined under section 2(20) of Companies Act, 2013 as “a company incorporated under this act or under any previous Companies Act”. However, it is pertinent to mention that body corporate are not covered under the section thereby meaning that foreign companies may grant loan or provide security and guarantee to its Directors without attracting any penal consequences of section 185.

Lets understand this with more clarity with the help of following illustration: ABC is a body corporate incorporated under the laws of America and having its branch office in India, ABC wants to grant loan of rupees 50 crores to its Indian director. Under the present case ABC can grant loan to the proposed Indian director since it is not a company falling within the definition of section 2(20) of Companies Act, 2013 (Assumption: ABC is not falling under section 379 of Companies Act, 2013). Section 379 provides for the circumstances under which a Foreign Company is deemed to be a company incorporated in India.

> The law maker has used the word directly or indirectly, it is imperative to understand the meaning and scope indirect loan. In the absence of definition of indirect loan in Companies Act and in General Clause Act, the same has been interpreted in light of dictionary meaning and judicial pronouncements. Indirect loan can refer to any loan in which the lender does not have a direct relationship with the borrower. Indirect loans can be obtained through a third party with the help of an intermediary (Black’s Law Dictionary).

> In Dr. Fredie Ardeshir Mehta V. Union of India [1991] 70 Comp. Cas. 210 ( Bom.), the term Indirect used in the Section 185 (section 295 of Companies Act, 1956) is interpreted as “When Section 185 refers to indirect loan to director, what it means is that the company shall not give a loan to a director through the agency of one or more intermediaries.” The word “indirectly” used in Sec. 185 cannot be read as converting what is not a loan into a loan. Therefore, the company shall not lend through intermediary to the persons who are otherwise related with the lending company.

> Further in view of the serious implications in the event of violation of the provisions of section 185 it is absolutely necessary to understand the precise and concise meaning of word “loan” and “Advances”. Loan has not been defined under Companies Act, 2013. Therefore we have to rely on the dictionary meaning of the term “Loan” and judicial clarification in this regard.

> In “Pennwalt India Ltd. v. RoC” MANU/MH/0006/1987, the Hon’ble High Court of Bombay has held that to ascertain whether a transaction is a loan or not, surrounding circumstances, relationship and character of the transaction and the manner in which parties treated the transactions will have to be considered. Therefore, with reference to each transaction with Directors and other person in whom the Directors are interested, the nature of transactions has to be studied, in case they relates to book debts.

> The Hon’ble Supreme Court in the case of Shree Ram Mills Ltd Vs. Commissioner of Excess Profit Tax, MANU/SC/0054/1954 = AIR 1953 SC 485has defined the word “Loan” in the following words:-

“At bottom this is a question of fact. Of course, money so left, could by a proper agreement between the parties, be converted into a loan, but in the absence of an agreement mere inaction on the part of the managing agents cannot convert the money due to them, and not withdrawn, into a loan. A loan imports a positive act of lending coupled with an acceptance by the other side of the money as a loan.”

> The Calcutta High Court in the case of Saradindu Sekhar Banerjee vs. Lalit Mohan MANU/WB/0045/1941, AIR 1941 Cal. 538 Every loan is a debt but every debt is not a loan.

> The Hon’ble Madras High Court in the case of Mohammed Abdul Kadir Rowther vs. S. Muthia Chettiar MANU/TN/0424/1959held that advance means literally a payment beforehand. In certain cases, it may be a loan but it cannot be said that a sum paid by way of advance is necessarily a loan.

> The Hon’ble Privy Council in the case of Raja of Venkatagiri vs. Krishnayya Rao Bahadur MANU/PR/0017/1948: AIR 1948 PC 150 at p. 155, has observed that ordinarily advance does not connote any idea of repayment, hence loan is completely different from an advance as is understood in the common parlance in the sense of payment of money beforehand and which is likely to become due at some future time.

> In London Financial Association vs. Kelk L.R. (1884) 26 Ch. D. 107, it was observed, that the words-‘advancing’ and ‘lending’ each have a different significance, the money might be ‘advanced’ without being ‘lent’.

> Whether section 185 is talking about loan or advance or both?

Section 185(1) of the Companies Act, 2013 inter-alia provides that no company shall, directly or indirectly, advance any loan, including any loan represented by a book debt, to any of its directors or to any other person in whom the director is interested or give any guarantee or provide any security in connection with any loan taken by him or such other person.

Here words “advance any loan” are used, it is not used as “advance or loan/advance and loan”, and hence the word “advance any loan shall be read together and word advance is a verb and loan is a noun, accordingly “advance any loan” means to give any loan This section is not at all include the words ‘Advance’ as noun which means paying something in advance before it is actually due.

It is pertinent to refer to the case of Pennwalt India Ltd. v. RoC , wherein the Hon’ble High Court of Bombay has held that to ascertain whether a transaction is a loan or not, surrounding circumstances, relationship and character of the transaction and the manner in which parties treated the transactions will have to be considered. Hence, with reference to each transaction with Directors and other person in whom the Directors are interested; the nature of transactions has to be studied.

> Guarantee has been covered; however, letter of comfort is not covered by section 185. Comfort letters (also called letters of awareness, letters of support, letters of responsibility and letters of patronage) are a hybrid between a guarantee and making no commitments at all. Comfort letters are often given by a parent company to a lender in relation to a credit facility being granted by the lender to the parent’s subsidiary. They are usually used where the issuer is unable or unwilling to give a guarantee, but wishes to give some comfort to the lender. The purpose is to give some comfort to the recipient of the letter by specifying certain moral or legal consequences or commitments.

| Legal text of sub-section (2) of Section 185

A company may advance any loan including any loan represented by a book debt, or give any guarantee or provide any security in connection with any loan taken by any person in whom any of the director of the company is interested, subject to the condition that— (a) a special resolution is passed by the company in general meeting: Provided that the explanatory statement to the notice for the relevant general meeting shall disclose the full particulars of the loans given, or guarantee given or security provided and the purpose for which the loan or guarantee or security is proposed to be utilised by the recipient of the loan or guarantee or security and any other relevant fact; and (b) the loans are utilised by the borrowing company for its principal business activities. Explanation.—For the purposes of this sub-section, the expression “any person in whom any of the director of the company is interested” means— (a) any private company of which any such director is a director or member; (b) any body corporate at a general meeting of which not less than twenty-five per cent. of the total voting power may be exercised or controlled by any such director, or by two or more such directors, together; or (c) any body corporate, the Board of directors, managing director or manager, whereof is accustomed to act in accordance with the directions or instructions of the Board, or of any director or directors, of the lending company. |

Analysis of sub-section (2) of Section 185:

> Unlike sub-section (1), sub-section (2) is restrictive part of the section 185 of the Companies Act, 2013. This sub-section introduces restrictions and certain compliance requirements only before a company proceeds to advancing loans to, or providing guarantee or securities for the loans taken by person in whom any of the director of the company is interested.

> This sub-section is relaxed comparative to the provision prior to Companies (amendment) Act, 2017 where in there was absolute prohibition for giving loan or providing security or guarantee to the persons in whom director is interested.

> Sub-section (2) permits the company to advance loan and to provide security and guarantee to the persons in whom directors is interested subject to passing of:

(i) Special resolution, and

(ii) Utilization of loan by the borrowing company in its principal business activities.

> Section 102 of the Companies Act, 2013 requires an explanatory statement to be annexed to notice of a general meeting when the general meeting is going to transact any item of any item of business that is special business within the meaning of clause (b) of sub-section (2) of section 102. Similarly, section 185 (2) specifically states that explanatory statement to the notice for the relevant general meeting shall disclose to the members of the company who are being called upon by the Board of Directors to approve a proposal by a special resolution, the precise purpose why the proposal requires approval of members. The responsibility surely falls on the Board of Directors. Impliedly the Board should be able to justify the proposal and show what commercial advantage would accrue to the company if the company proceeds to advance the loan or provide the guarantee or security. The facts must be disclosed in the explanatory statement for the members to take an informed decision and grant the requisite approval by way of a special resolution.

> Clause (b) of sub-section (2) of section 185 of the companies Act, 2013 makes it very clear that borrowing company (recipient) utilizes such loan for its principal activities only.

> The term controlled is defined in clause (27) of section as control” shall include the right to appoint majority of the directors or to control the management or policy decisions exercisable by a person or persons acting individually or in concert, directly or indirectly, including by virtue of their shareholding or management rights or shareholders agreements or voting agreements or in any other manner.

> The meaning of person in whom director is interested has been defined under the explanation to sub-section (2) where in the borrower must be either

a private company or a body corporate.

> No doubt the term “Body Corporate” includes limited liability partnership (LLPs). However clause (b) of the explanation under sub-section (2) is directly connected to voting powers in a general meeting, in case of LLP incorporated under the Limited Liability Partnership Act, 2008, there may not be any general meeting at all. In this context, it could be taken as meeting of partners. We found no reason why LLP should not be covered here and earn the wrath of section 185.

| Legal text of sub-section (3) of Section 185

Nothing contained in sub-sections (1) and (2) shall apply to— (a) the giving of any loan to a managing or whole-time director— (i) as a part of the conditions of service extended by the company to all its employees; or (ii) pursuant to any scheme approved by the members by a special resolution; or (b) a company which in the ordinary course of its business provides loans or gives guarantees or securities for the due repayment of any loan and in respect of such loans an interest is charged at a rate not less than the rate of prevailing yield of one year, three years, five years or ten years Government security closest to the tenor of the loan; or (c) any loan made by a holding company to its wholly owned subsidiary company or any guarantee given or security provided by a holding company in respect of any loan made to its wholly owned subsidiary company; or (d) any guarantee given or security provided by a holding company in respect of loan made by any bank or financial institution to its subsidiary company: Provided that the loans made under clauses (c) and (d) are utilised by the subsidiary company for its principal business activities. |

Analysis of sub-section (3) of Section 185:

> Sub-section (3) opens with the words “nothing contained in sub-section in sub-section (1) and (2) shall apply” meaning thereby the prohibition contained in sub-section (1) nor the conditions prescribed in sub-section (2) will apply to certain specified transactions

> It is pertinent to mention w.r.t. clause (a) that the exemption is given only to managing and whole time directors; thereby meaning that loan to part-time directors is absolutely prohibited. However loan to part time directors is permissible under section 186(2) upto the limits mentioned therein without approval of members in general meeting. In this clause, exemption is given only if company provides LOAN to its directors, in other words providing guarantee or security is not permitted. Further the exemption is only available when loan is given by company to its directors thereby meaning that loan by subsidiary company to the directors of holding company is not exempted. Further the loan must be given as a part of condition of service eg: housing loan, education loan, marriage loan etc. if the loan is not covered under terms of employment then company may pass board resolution, amend the service condition accordingly.

> Clause (b) of sub-section (3) of section 185 is for those companies which in their ordinary course of business provides loans or gives guarantee or securities for due repayment of any loan. Obviously, such a company will be either a non-banking financial company (NBFCs) or a bank.

> Clause (c) of sub-section (3) of section 185, exempts from the applicability of sub-section (1) and (2) to any loan made by a holding company to its wholly owned subsidiary company or any guarantee given or securities provided by a holding company in respect of any loan made to its wholly owned subsidiary company. One of the conditions is that the recipient of the loan or guarantee or security must be a wholly owned subsidiary. The other condition is that the loans must be utilised by the subsidiary company for its principal business activities only.

> Clause (d) of sub-section (3) of section 185 grants exemption from the prohibition contained in sub-section (1) as well as from the restriction contained in sub-section (2) to any guarantee given or security provided by a holding company in respect of loan made by any bank or financial institution to its subsidiary company. It is to be noted that this clause does not talk about wholly owned subsidiary companies.

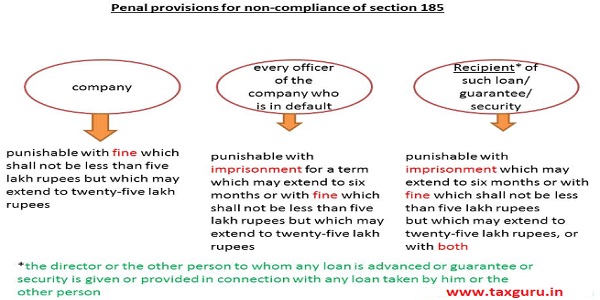

Sub-section (4) of Section 185: Penal provisions for non-compliance of section 185

What may be the planning for sec 185?

What may be the planning for sec 185?

(1) Convert both Lender co & receiver co to LLP or

(2) Convert other co (to whom loan is given) to public Ltd to enjoy 25% limit or

(3) Rearrange shareholding pattern & directorship pattern:

a) Appoint new directors in lender Co, who personally neither hold any share in other co nor are directors in other co. If their relatives holds shares or are directors than there is no problem or

b) One can gift shares to other relative to rearrange shareholding pattern.

Section 462 of the Act empowers Central Government to grant exemption to any class or classes of companies from the applicability of any of the provisions of the Act or to apply any provision with such modifications as the Central Government may deem fit. In this reference, MCA has exempted Government companies, Private companies, Nidhi companies and specified IFSI Public companies. Readers of this article are advised to go through such notifications before applying the provisions of section 185.

(Any query and suggestion kindly contact the author at: sandy673711@gmail.com or +918077133617)

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness, and resliability of the information provided, I assume no responsibility, therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not professional advice and is subject to change without notice. I assume no responsibility for the consequences of the use of such information.

Author Bio

Excellent Article.