Key points of provisions of Section 135 of Companies Act, 2013 [(Corporate Social Responsibility (CSR)]

1. Provisions of this section is applicable to all companies having turnover of Rs. 1000 crore or more or Net profit of Rs. 5 crore or more or Net worth of Rs. 500 crore or more in immediately preceding financial year.

2. The company shall constitute a committee called Corporate Social Responsibility Committee, however if the total amount to spent by company does not exceeds Rupees 50 lakhs then constitution of the Corporate Social Responsibility Committee shall not be applicable.

3. The companys pends, in every financial year, at least two per cent of the average net profits of the company made during the three immediately preceding financial years. If, company has not completed 3 years from its incorporation, then for the purpose of calculation of average net profit, the profit immediately preceding financial year shall be considered.

Note: Net profit shall be calculated in accordance with provisions of section 198 of the Companies act, 2013.

4. The preference should be given to the local area and areas around it where it operates for spending the amount earmarked for CSR activity.

5. A company may undertake the implementation of CSR projects through the following methods:-

- Undertaking CSR activities by company itself

- Section 8 company/ registered public trust / registered society, registered under section 12A and 80 G of the Income Tax Act, 1961, established by the company, either singly or along with any other company

- Section 8 company/ registered trust/ registered society, established by the Central Government or State Government

- any entity established under an Act of Parliament or a State legislature

- Section 8 company/ registered public trust/ registered society, registered under section 12A and 80G of the Income Tax Act, 1961, and having an established track record of at least three years in undertaking similar activities.

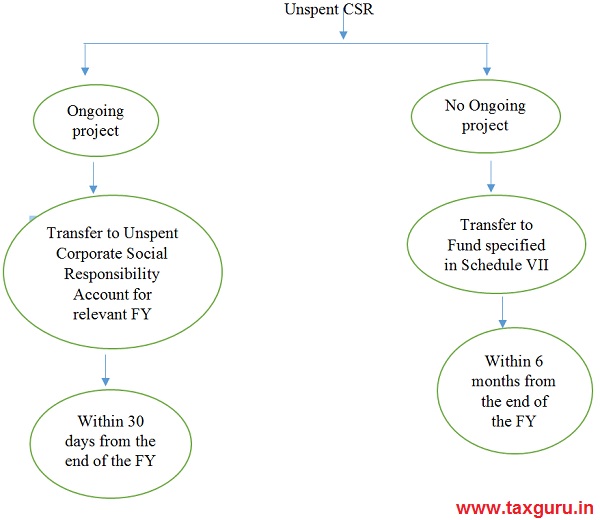

6. As per the provisions of section 135 (5) of the Companies Act 2013, if company fails to spent the amount (at least two per cent of the average net profits), then Board shall disclose the fact along with reason for not spending the same in its report and unless the unspent amount shall be transfer to a fund specified in Schedule VII, within a period of six months from of the expiry of the financial year, if it relates to ongoing project.

Note: As per The Companies (CSR Policy) Rules, 2014 (‘CSR Rules’) ‘Ongoing Project’ means a multi-year project undertaken by a company in fulfilment of its CSR obligations, having timelines not exceeding three years excluding the financial year in which it was commenced, and shall include such project that was initially not approved as a multi-year project but whose duration has been extended beyond one year by the board based on reasonable justification.

7. Any amount remaining unspent as per the provisions of Section 135(5) of the Companies Act, 2013, pursuant to any ongoing project, shall be transferred within a period of thirty days from the end of the financial year to a special account to be opened by the company in that behalf for that financial year in any scheduled bank to be called the Unspent Corporate Social Responsibility Account and such amount shall be spent by the company as per is CSR policy with in period of 3 financial years from the date of such transfer and failing which company shall within a period of 30 days from the end of the third financial year transfer such amount to a fund as specified in Schedule VII.

The para 6 and 7 can be understand with help of following flow chart:-

8. If, company spends more than the amount as it requires to spend as per the provisions of this section then such excess amount may set off against the requirement to spend under sub-section (5) of section 135 up to immediately succeeding three financial years subject to the conditions that:-

- The excess amount available for set-off shall not include the surplus arising out of the CSR activities, if any, in pursuance of sub-rule (2) of the Companies (Corporate Social Responsibility Policy) Rules, 2014.

- The Board of the company shall pass a resolution to that effect.

9. If a company is in default in complying with the provisions of sub-section (5) or sub-section (6), the company shall be liable to a penalty of twice the amount required to be transferred by the company to the Fund specified in Schedule VII or the Unspent Corporate Social Responsibility Account, as the case may be, or one crore rupees, whichever is less, and every officer of the company who is in default shall be liable to a penalty of one-tenth of the amount required to be transferred by the company to such Fund specified in Schedule VII, or the Unspent Corporate Social Responsibility Account, as the case may be, or two lakh rupees, whichever is less.

10. Activities which may be included by companies in their Corporate Social Responsibility Policies Activities relating to:-

i. Eradicating hunger, poverty and malnutrition, [“promoting health care including preventive health care”] and sanitation [including contribution to the Swach Bharat Kosh set-up by the Central Government for the promotion of sanitation] and making available safe drinking water.

ii. Promoting education, including special education and employment enhancing vocation skills especially among children, women, elderly and the differently abled and livelihood enhancement projects.

iii. Promoting gender equality, empowering women, setting up homes and hostels for women and orphans; setting up old age homes, day care centres and such other facilities for senior citizens and measures for reducing inequalities faced by socially and economically backward groups.

iv. Ensuring environmental sustainability, ecological balance, protection of flora and fauna, animal welfare, agroforestry, conservation of natural resources and maintaining quality of soil, air and water [including contribution to the Clean Ganga Fund set-up by the Central Government for rejuvenation of river Ganga].

v. Protection of national heritage, art and culture including restoration of buildings and sites of historical importance and works of art; setting up public libraries; promotion and development of traditional art and handicrafts;

vi. Measures for the benefit of armed forces veterans, war widows and their dependents, [Central Armed Police Forces (CAPF) and Central Para Military Forces (CPMF) veterans, and their dependents including widows];

vii. Training to promote rural sports, nationally recognised sports, Paralympic sports and Olympic sports

viii. Contribution to the prime minister’s national relief fund [or Prime Minister’s Citizen Assistance and Relief in Emergency Situations Fund (PM CARES Fund)] or any other fund set up by the central govt. for socio economic development and relief and welfare of the schedule caste, tribes, other backward classes, minorities and women;

(a) Contribution to incubators or research and development projects in the field of science, technology, engineering and medicine, funded by the Central Government or State Government or Public Sector Undertaking or any agency of the Central Government or State Government; and

(b) Contributions to public funded Universities; Indian Institute of Technology (IITs); National Laboratories and autonomous bodies established under Department of Atomic Energy (DAE); Department of Biotechnology (DBT); Department of Science and Technology (DST); Department of Pharmaceuticals; Ministry of Ayurveda, Yoga and Naturopathy, Unani, Siddha and Homoeopathy (AYUSH); Ministry of Electronics and Information Technology and other bodies, namely Defense Research and Development Organisation (DRDO); Indian Council of Agricultural Research (ICAR); Indian Council of Medical Research (ICMR) and Council of Scientific and Industrial Research (CSIR), engaged in conducting research in science, technology, engineering and medicine aimed at promoting Sustainable Development Goals (SDGs).]

x. Rural development projects

xi. Slum area development.

Explanation.- For the purposes of this item, the term `slum area’ shall mean any area declared as such by the Central Government or any State Government or any other competent authority under any law for the time being in force.

xii. Disaster management, including relief, rehabilitation and reconstruction activities, it includes spending of CSR Funds for COVID-19 is eligible CSR activity.

xiii. If any ex-gratia payment is made to temporary / casual workers/ daily wage workers over and above the disbursement of wages, specifically for the purpose of fighting COVID 19, the same shall be admissible towards CSR expenditure as a onetime exception provided there is an explicit declaration to that effect by the Board of the company, which is duly certified by the statutory auditor.

11. Activities would not qualify as CSR Expenditure:-

- The CSR projects or programs or activities that benefit only the employees of the company and their families shall not be considered as CSR activities in accordance with section 135 of the Act.

- One-off events such as marathons/ awards/ charitable contribution/ advertisement/sponsorships of TV programmes etc. would not be qualified as part of CSR expenditure.

- Expenses incurred by companies for the fulfilment of any Act/ Statute of regulations (such as Labour Laws, Land Acquisition Act etc.) would not count as CSR expenditure under the Companies Act.

- Contribution of any amount directly or indirectly to any political party shall not be considered as a CSR activity.

- Activities undertaken by the company in pursuance of its normal course of business.

- ‘Chief Minister’s Relief Fund’ or ‘State Relief Fund for COVID-19’ is not included in Schedule VII of the Companies Act, 2013 and therefore any contribution to such funds shall not qualify as admissible CSR expenditure.

- Payment of salary/ wages to employees and workers during the lockdown period (including imposition of other social distancing requirements) shall not qualify as admissible CSR expenditure.

- Payment of wages to temporary or casual or daily wage workers during the lockdown period shall not count towards CSR expenditure.

- Medical camp exclusive for the unskilled labour hired by the company shall not be permitted as a CSR activity.

Author Bio

हमारी एनजीओ पिछले छे साल से सामाजिक कार्य कर रही है लेकिन सिएसआर फंडीग नही मिल पाई ! कृपया सहयोग किजीए यही आपसे प्रार्थना

अच्छे तरह से काम करणेवाले एनजीओ को सिएसआर फंडीग मिलना जरूरी है!