Evolution of Listing Compliance framework : Analysis of Amendments to the Listing Regulations, SEBI Circulars & Notifications & Stock Exchange directives as applicable for Equity Listed Companies

The landscape of listing compliance underwent a change for the better with introduction of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (“Listing Regulations”) which was notified on 2nd September, 2015 and made effective from 1st December, 2015. It brought a consolidated legislation into force and repealed the Listing Agreement along with innumerable circulars/notifications issued thereunder.

With the advent of time and experience gained in implementing the Listing Regulations by the Stock Exchanges and the SEBI, the SEBI has come out with several amendments to the Listing Regulations and issued several Circulars and Notifications which have further changed/streamlined the regulatory & compliance landscape.

Further, the recommendations of the Uday Kotak Committee on Corporate Governance notified by SEBI vide the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) (Amendment) Regulations, 2018 dated May 9, 2018 has raised several action points which require active consideration and decision by the management of listed entities for its implementation, documentation and appropriate disclosures, inter-alia, in the Annual Report for the Financial Year 2018-19 onwards.

Consequentially, sole reading of the Listing Regulations as it stands today may be insufficient in understanding the current compliance framework of an Equity Listed entity in its totality, unless they are correlated with the Circulars and Notifications issued by SEBI and directives issued by the Stock Exchanges.

The Author has compiled, analyzed and summarized the relevant amendments to the Listing Regulations, several Circulars and Notifications issued by SEBI and directives issued by the Stock Exchanges with the actions to be taken in order to give the readers a comprehensive view of the regulatory requirements.

(Note: All Regulations mentioned hereunder pertain to Listing Regulations only unless mentioned otherwise)

1) SEBI Circular No. CIR/CFD/CMD/4/2015 dated 9th September, 2015 – Disclosure under Regulation 30 of LODR – Continuous disclosure requirements for listed entities.

Companies must refer to this Circular in addition to Regulation 30 and Schedule III of the Listing Regulations for the details to be covered while disclosure of material events/information under Regulation 30 of the Listing Regulations is being made – Insufficiency in this respect is usually followed by query/warning from stock exchanges.

2) The SEBI (LODR) (Amendment) Regulations, 2015 vide notification no. SEBI/LAD-NRO/GN / 2015-16/27 dated December 22, 2015

Requirement of providing Business Responsibility Report as part of the Annual Report has been extended to Top 500 listed entities based on market capitalization from Top 100 earlier. Companies other than Top 500 may voluntarily comply.

3) SEBI FAQs dated 19th, 21st & 29th January, 2016 on Listing Regulations Key takeaways:

a) Criteria under both Companies Act, 2013 and applicable AS to be considered for determining Associate Company and Related Party – if either is fulfilled, such entity to be classified as Associate Company and Related Party.

b) Certificate of compliance under Regulation 17(8) may be signed by officials (Managing Director/Wholetime Director) holding powers, duties, responsibilities of CEO/CFO irrespective of designation.

c) Related parties to abstain from voting on material RPTs whether party to the particular transaction or not. (As per latest version of Reg. 23(4) a Related party, can now vote against, but not in favour of a resolution for approval of a material RPT)

d) Director of a listed entity can be member of upto 10 committees and chairman of upto 5 committees in other listed companies /unlisted public companies put together.

e) Listed Holding company has to make disclosure under Regulation 30(9) of events or information with respect to subsidiaries which are material for the listed entity though its listed subsidiary company may have made disclosure to stock exchange in its own right.

f) Company’s policy for determination of material subsidiary can have stricter criteria than Listing Regulations, i.e. Income or Net Worth exceeding 20% of consolidated figures.

g) Listed company having subsidiary to be submit two sets of Form A/Form B for financial results (should be read as Statement of Impact of Audit Qualification/ Declaration of unmodified audit opinion)

h) Agreements with media companies or their associates, which are not in the ordinary course of business are only to be disseminated on company’s website under Regulation 46(2)(n).

i) Requirement to update change in website within 2 days of change pertains to content uploaded in terms of Regulation 46.

j) “Working day” shall mean working day of the stock exchange where the securities of the company are listed.

k) Policy for Preservation of documents pertain to documents which are maintained under “securities laws” defined under Regulation 2(1)(zf) i.e. the SEBI Act, the Securities Contracts (Regulation) Act, 1956, the Depositories Act, 1996, and the provisions of the Companies Act, 1956 and Companies Act, 2013, and the rules, regulations, circulars or guidelines made thereunder.

l) Disclosure under Regulation 30 on acquisition of 5% or more shares/voting rights in a company includes acquisition of both listed and unlisted companies.

4) The SEBI (LODR) (Amendment) Regulations, 2016 vide notification no. SEBI/LAD-NRO/GN/ 2016-17/001 dated May 25, 2016

Amendments in brief:

a) In Regulation 33, i.e. Financial Results, Form A (for audit report with unmodified opinion) or Form B (for audit report with modified opinion) has been done away with;

Statement of Impact of Audit Qualification introduced for companies with Audit Report with modified opinion. For Audit Reports with unmodified opinion, listed entities are required to furnish a declaration to that effect to the Stock Exchange(s) while publishing the annual audited financial results.

b) Regulation 33(7) – omitted – which earlier read “The listed entity shall on the direction issued by the Board, carry out the necessary steps, for rectification of modified opinion and/or submission of revised pro-forma financial results, in the manner specified in Schedule VIII.”

c) Annual Report shall include Statement on Impact of Audit Qualifications as stipulated in regulation 33(3)(d), if applicable.

d) Cumulative impact of Audit qualification on earning per share, total expenditure, total liabilities or any other financial item(s) which may be impacted to be disclosed.

e) Management of listed entity has option to explain its views on audit qualifications to be included in Statement on Impact of Audit Qualification.

f) If management is unable to quantify impact of audit qualification, then estimate of impact to be prepared and reviewed by auditor, if estimate not possible, then provide reason which is to be reviewed by auditor.

g) Deletion of Schedule VIII (Manner of reviewing Form B accompanying audited financial results).

5) The SEBI (LODR) (Second Amendment) Regulations, 2016 vide notification no. SEBI/ LAD-NRO/GN/2016-17/008 dated July 08, 2016

Amendments in brief: Introduction of Dividend Distribution Policy – to be formulated by Top 500 listed entities based on market capitalization to be calculated as of 31st March of every financial year which shall be disclosed in their annual reports and on their websites. Other than Top 500 listed entities may comply voluntarily.

6) The SEBI (LODR) (Third Amendment) Regulations, 2016 vide notification no. SEBI/LAD-NRO/GN/2016-17/025 dated January 4, 2017.

Amendments in brief:

a) Ambit of Regulation 26 extended to Employees, KMPs and Promoters – Heading changed from “Obligations with respect to directors and senior management” to “Obligations with respect to employees including senior management, key managerial persons, directors and promoters”

b) Addition of sub-regulation (6) to Regulation 26 which states –

“No employee including key managerial personnel or director or promoter of a listed entity shall enter into any agreement for himself or on behalf of any other person, with any shareholder or any other third party with regard to compensation or profit sharing in connection with dealings in the securities of such listed entity, unless prior approval for the same has been obtained from the Board of Directors as well as public shareholders by way of an ordinary resolution:

Provided that such agreement, if any, whether subsisting or expired, entered during the preceding three years from the date of coming into force of this sub-regulation, shall be disclosed to the stock exchanges for public dissemination:

Provided further that subsisting agreement, if any, as on the date of coming into force of this sub-regulation shall be placed for approval before the Board of Directors in the forthcoming Board meeting:

Provided further that if the Board of Directors approve such agreement, the same shall be placed before the public shareholders for approval by way of an ordinary resolution in the forthcoming general meeting:

Provided further that all interested persons involved in the transaction covered under the agreement shall abstain from voting in the general meeting.

Explanation – For the purposes of this sub-regulation, ‘interested person’ shall mean any person holding voting rights in the listed entity and who is in any manner, whether directly or indirectly, interested in an agreement or proposed agreement, entered into or to be entered into by such a person or by any employee or key managerial personnel or director or promoter of such listed entity with any shareholder or any other third party with respect to compensation or profit sharing in connection with the securities of such listed entity.”

7) SEBI Circular No. SEBI/HO/CFD/CIR/P/2017/004 dated January 5, 2017 – Guidance note on Board Evaluation: The Guidance crystallizes the Board Evaluation criteria, procedure and removes ambiguities.

8) The SEBI (LODR) (Amendment) Regulations, 2017 vide notification no. SEBI/LAD/NRO/ GN/ 2016-17/029 dated February 15, 2017

Amendment in brief – Requirement of No Objection letter from stock exchanges before filing of draft scheme relaxed for schemes solely for merger of a wholly owned subsidiary with its holding company done away with. However, that such draft scheme shall be filed with the stock exchanges for the purpose of disclosures.

9) SEBI Circular No. SEBI/HO/OIAE/IGRD/CIR/P/2018/58 dated March 26, 2018 on “Investor grievance redress mechanism – new policy measures”

The Circular states that SEBI has received inputs from listed companies and intermediaries that investor grievances can be resolved faster if the grievance been taken up directly with the entity at the first instance.

Accordingly, with effect from August 01, 2018, aggrieved investors may use SCORES platform to submit the grievance directly to companies / intermediaries and the complaint shall be forwarded to the entity for resolution. The entity is required to redress the grievance within 30 days, failing which the complaint shall be registered in SCORES. In case, the listed company or registered intermediary fails to redress the complaint to the investor’s satisfaction, the investor may file a complaint in SCORES.

An Investor may lodge a complaint on SCORES within limitation period of 3 years from the date of cause of complaint, where –

- Investor has approached the listed company or registered intermediary for redressal

- The company or intermediary rejected the complaint, or

- Complainant does not receive any communication from Company or Intermediary, or

- Complainant is not satisfied with the reply given or redressal action taken.

10) SEBI Circular No. SEBI/HO/MIRSD/DOP1 /CIR/P/2018/73 dated 20th April, 2018 titled: “Strengthening the Guidelines and Raising Industry standards for RTA, Issuer Companies and Banker to an Issue”

This Circular is intended to remove lack of clarity and establish a framework in matters of payment of Dividends/Interests/Redemptions, Handling/Maintenance/Update of Records, Transfer of Securities, Due Diligence and introduces Internal Audit of RTAs. Though applicability extends to activities in the domain of RTAs and Bankers, the onus of compliance with the Circular is on the listed entity.

STEPS TO BE TAKEN

| 1. | Maintenance of documents/ records for 8 years |

| 2. | Listed co. to monitor activities of RTA and ensure compliance with this Circular |

| Payment of Dividend/ Interest/ Redemption | |

| 3. | Dividend Master File to contain specified particulars as per Para I (1) of Circular. Dividend Master to be maintained by Bank and reconciled by RTA & Issuer. |

| 4. | RTA to update Bank A/c. details of shareholders if not available or changed. Cancelled cheque with shareholder name or bank attested account statement/ passbook to be sought. |

| 5. | Unpaid dividend to be paid by electronic means as first preference. In case of failure or rejection or unavailability of IFSC/ MICR code, physical instrument to be issued. |

| 6. | Instrument lying unpaid beyond validity of the instrument to be cancelled and amount should revert back to bank a/c. of the Co. Banks should also provide unpaid instrument details along with reconciliation data. |

| 7. | Revalidation requests by RTA to Bank to contain specified details and RTA to maintain record of revalidation/ re-issue requests. |

| 8. | Issuer Co., RTA & Bank to ensure that Bank provides Paid-Unpaid details as follows –

a) Fortnightly till initial validity of instrument b) Quarterly till transfer of unpaid dividend to IEPF Reconciliation data provided by Bank to contain details of all DDs/ new instruments issued/ electronic instruction in lieu of original dividend. RTA to reconcile the same and inform Issuer/ Bank of any discrepancy. Reconciliation files provided by Bank to be maintained by Co./RTA/Bank for 8 years. |

| 9. | Linking detail of rejection of electronic remittance, instrument undelivered, instrument expired, subsequent payment and status of payment to payment record of each Folio by RTA and RTA shall keep audit trail in its system. |

| Transfer, Transmission, Correction of Errors etc. | |

| 10. | Folio once allotted to a shareholder should not be re-allotted including ceased folios, i.e. folios having nil balance. |

| 11. | History of all transactions in a Folio (e.g. Securities held, certificates issued, dividend/ interest/ redemption) to be linked to each folio. |

| 12. | RTA to maintain Certificate Printing Register/ Records containing – Date of printing / issue, Folio No., Name in which printed, Certificate No., Distinctive Nos., Old Certificate No. (in case of reprinting), Reason of printing etc. |

| 13. | RTA to follow “Maker-Checker” system in all activities and have mechanism to check unauthorized transaction and record shall be maintained. |

| 14. | RTA and Cos. to ensure that all updation in folio records are only through front end modules and maintain system logs having complete details of any change. [Applicable w.e.f 90 days after Circular date] |

| 15. | RTA to take Company’s prior approval for correction of errors in same manner as is taken in case of transfer/ transmission. |

| 16. | RTA to provide SOFT COPY of MEMBER DATA with details of Name, Address, Folio No., No. of Shares, Distinctive Nos., Certificate Nos. etc. and transaction in physical Folios during the period, under their certification on QUARTERLY basis.

This record is to be maintained by RTA and Listed Company, independently and permanently. |

| 17. | Returns/ documents filed with Registrar of Companies relating to Company’s securities processed and compiled by RTA to be shared with Company and preserved by Company. |

| 18. | RTA & Co. to frame written policy and maintain strict control over stationery (blank certificates, dividend warrants etc.) and periodical verification of the same. Reconciliation report on the same to be maintained by Co. & RTA. |

| 19. | Bonus shares to holders of physical shares can be issued in physical form only. |

| 20. | RTA & Listed Company to take special efforts to collect copy of PAN and Bank A/c. details of physical share-holders. In this regard RTA to –

|

| 21. | ENHANCED DUE DILIGENCE to be exercised for the following cases –

|

| 22. | In order to exercise due diligence Issuer Company and RTA shall call for –

|

| 23. | RTA to maintain register of documents and records destroyed with specified details as per Para II (15) of the Circular, i.e. Description of the records and documents destroyed, Name of authority authorising the destruction, Date of authorization of destruction, Destroyed in whose presence (with signature) and Date of destruction. Its authenticity shall be verified during internal audit of the RTA. |

| Compulsory Internal Audit of RTAs | |

| 24. | Mandatory internal audit of RTA’s on Annual basis by independent and qualified CA/ CS/ CMA/ CISA not having any conflict of interest.

The audit firm, to be eligible, is required to have minimum experience of 3 years in financial sector and can be appointed for a maximum term of 5 years with cooling off period of 2 years. Scope of the Audit to cover all issues concerning functioning of RTAs including Investor Grievance Redressal Mechanism and Compliance with requirements of SEBI Act, Rules and Regulations made thereunder. |

| 25. | Internal Audit Report shall be considered by the Board of Directors/ Partners/ Proprietor of the RTA and RTA to take steps to rectify the deficiencies. RTA shall within next 1 month send Action Taken Report to the Issuer Company in the format specified in the Circular, preserving a copy with itself.

Audit Report shall be preserved by the RTA and shared by RTA with Issuer Co., within 3 months from end of FY. The Audit observations along with ATR is required to be placed before the Board of the Issuer Company and the Issuer Company shall satisfy itself regarding adequacy of the corrective measure taken by RTA or ask the RTA to take more stringent measures. |

11) SEBI Circular No. IMD/FPIC/CIR/P/2018/61 dated April 05, 2018 titled “Monitoring of Foreign Investment limits in listed Indian companies”

This circular requires listed entities to appoint any one of NSDL or CDSL as the Designated Depository for the purpose of monitoring of foreign exchange limits in listed companies for with a view to assist companies comply with the Sectoral Caps on FPI/NRI holding laid down by FEMA. In case of breach of applicable limits the acquirer (foreign investor) is required to offload the excess investment beyond the permissible limit within 5 trading days.

12) SEBI Circular No. SEBI/HO/CFD/CMD/CIR/P/2018/77 dated May 3, 2018 titled “Non-compliance with certain provisions of the SEBI (LODR) Regulations, 2015 and the Standard Operating Procedure for suspension and revocation of trading of specified securities”(Read with NSE/BSE’s Guidance note and Curve out policy drawn in consultation with SEBI)

Critical features of the Circular –

- Supersedes earlier circulars dated 30/11/15 and 26/10/16 issued in the matter.

- Applicable for compliances periods ending on 30th September, 2018 and thereafter. (First instance of non-compliance will be calculated effective 30/09/2018 whereas QE 30/06/2018 will be considered for calculating consecutive non-compliance)

- Compulsory for Stock exchanges to take action for non-compliance with LODR and follow the SOP for suspension of trading in securities of the entity / moving to ‘Z’ Category – trade for trade basis.

- Compulsory for Depositories to freeze entire shareholding of Promoter/ Promoter Group of the non-compliant entity and all other securities in the Demat A/c.

- Action taken by Stock Exchanges i.e. fine/ freeze, suspension of trading to be disclosed on stock exchange website – information becomes public.

- Action taken by Stock Exchanges to be placed before Board of Directors and submit comments of the Board to stock exchanges.

- Listed entities are mandated to bring this circular to the knowledge of the Promoter/ Promoter Group.

- BSE and NSE to coordinate keep each other in loop + action by one SE to trigger another SE.

- For continuing non-compliances/ non-payment of fines, stock exchanges shall initiate compulsory delisting process 6 months after suspension of trading.

Penalties for violation of the Listing Regulations –

a) 6(1) – Non-appointment of qualified CS as Compliance Officer – Rs.1000/-/Day.

b) 7(1) – Non-appointment of share transfer agent – Rs.1000/-/Day.

c) 13(1)/ 13(3) – Failure to ensure adequate steps for expeditious redressal of investor complaints / Non-submission of statement of investor complaints – Rs.1000/-/Day.

d) 17(1) – Non-compliance in composition of Board of Directors incl. appointment of woman Director – Rs.5000/-/Day.

e) 18(1) – Non-compliance in composition of Audit Committee – Rs.2000/-/Day.

f) 19(1)/(2) – Non-compliance in composition of NRC – Rs.2000/-/Day.

g) 20(2) – Non-compliance in composition of SRC – Rs.2000/-/Day.

h) 21(2) – Non-compliance in composition of Risk Management Committee – Rs.2000/-/ Day.

i) 27(2) – Non-submission of CG Report within due date – Rs.2000/-/ Day.

j) 29(2)/(3) – Prior intimation of Board Meetings – Rs.10,000/-/ Instance.

k) 31 – Non-submission of Shareholding Pattern within due date – Rs.2000/-/ Day.

l) 32(1) – Non-submission of deviation/ variation in utilization of issue proceeds-Rs.1000/- /Day.

m) 33 – Non-submission of Financial Results within due date – Rs.5000/-/Day.

n) 34 – Non-submission of ANNUAL REPORT within due date – Rs.2000/-/Day. (N.B.: As per amended Reg. 34, Annual Report has to be submitted to stock exchange on or before commencement of dispatch to shareholders)

o) 39(3) – Non-submission of intimation of Loss of Shares/ Issue of Duplicate Shares within 2 days – Rs.1000/-/Day. (As per directive of NSE, proof of date of information about loss/ issue of duplicate to be attached with letter)

p) 42(2)/(3)/(4)/(5) – Record Date/ Book Closure/ Dividend declaration related compliances – Rs.10,000/- per instance of non-compliance.

q) 44(3) – Non-submission of Voting Results within 48 Hours of AGM/ EGM/ Postal Ballot/ Court convened Meetings – Rs.10,000/- per instance of non-compliance.

r) 46 – Website compliances – Upto 4 Warning Letters/ FY and Rs.10,000/- per fineper Warning Letter beyond. [As per amended Reg. 46 – details prescribed under the said Reg. is to be provided under a separate section in Co.’s website – Aggregation of information under a separate appropriate heading may be required]

[N.B.: Above to be kept in consideration at all times, BSE & NSE has started imposing fines and uploading list of non-compliant companies in its website]

UDAY KOTAK COMMITTEE RECOMMENDATIONS

13) The SEBI (LODR) (Amendment) Regulations, 2018 vide notification SEBI/LAD-NRO/GN/2018/10 dated May 9, 2018

Amendments effective April 1, 2019 onwards –

a)Reg. 2(zb) – Person or entity belonging to Promoter or Promoter Group and holding 20% or more shareholding deemed to be “related party”.

b)Reg. New Reg.17A – Maximum number of directorships and Reg.24A – Secretarial Audit introduced.

c)Reg. 16(c) – Material subsidiary – threshold reduced from 20% to 10% of consolidated income or net worth.

d)Reg. 16(d) – Definition of ‘senior management’ means officers/ personnel who are members of core management team and to specifically include CS and CFO; excludes CEO/ MD/ WTD/ Manager (including CEO/ Manager if they are not part of the Board)

e) Reg. 17(1)(a) – Top 500 companies as on 31/03/18 to have 1 woman ID by 01/04/19 and top 1000 as on 31/03/19 by 01/04/20.

f) Reg. 17(1)(c) – New – Board to have minimum 6 directors (top 1000 by 01.04.19, top 2000 by 01.04.20).

g) Reg. 17(1A) – New – No listed entity shall appoint a person or continue the directorship of any person as a non-executive director who has attained the age of seventy five years unless a special resolution is passed to that effect, in which case the explanatory statement annexed to the notice for such motion shall indicate the justification for appointing such a person.”

h) Reg. 17(1B) – New – With effect from April 1, 2020, the top 500 listed entities shall ensure that the Chairperson of the board of such listed entity shall – (a) be a non-executive director; (b) not be related to the Managing Director or the Chief Executive Officer as per the definition of the term “relative” defined under the Companies Act, 2013: Provided that this sub-regulation shall not be applicable to the listed entities which do not have any identifiable promoters as per the shareholding pattern filed with stock exchanges. Explanation – The top 500 entities shall be determined on the basis of market capitalisation, as at the end of the immediate previous financial year.”

i) Reg. 17(2A) – New – The quorum for every meeting of the board of directors of the top 1000 listed entities with effect from April 1, 2019 and of the top 2000 listed entities with effect from April 1, 2020 shall be one-third of its total strength or three directors, whichever is higher, including at least one independent director; VC participation allowed for quorum; [Corporate Governance Policy/ other document/ resolution mentioning quorum to be amended in line with the changed quorum requirement and such quorum to be ensured]

j) Reg. 17(6)(ca) – New – The approval of shareholders by special resolution shall be obtained every year, in which the annual remuneration payable to a single non-executive director exceeds fifty per cent of the total annual remuneration payable to all non-executive directors, giving details of the remuneration thereof;

k) Reg. 17(6)(e) – New – The fees or compensation payable to executive directors who are promotersor members of the promoter group, shall be subject to the approval of the shareholders by special resolution in general meeting, if- (i) the annual remuneration payable to such executive director exceeds rupees 5 crore or 2.5 per cent of the net profits of the listed entity, whichever is higher; or (ii) where there is more than one such director, the aggregate annual remuneration to such directors exceeds 5 per cent of the net profits of the listed entity: Provided that the approval of the shareholders under this provision shall be valid only till the expiry of the term of such director. Explanation: For the purposes of this clause, net profits shall be calculated as per section 198 of the Companies Act, 2013.

l) Reg. 17(10) – Evaluation of Independent Directors – The evaluation of independent directors shall be done by the entire board of directors which shall include – (a) performance of the directors; and (b) fulfillment of the independence criteria as specified in these regulations and their independence from the management: Provided that in the above evaluation, the directors who are subject to evaluation shall not participate.” [Evaluation checklist to be updated and minuting to be done in line with above change; N.B.: Board to confirm veracity of declaration of independence while taking the same on record in first BM]

m) Reg. 17(11) – New – Explanatory statement for each item of special business to be transacted at a general meeting shall clearly set forth recommendation of the board to shareholders on each of the specific items. [N.B.: A line on recommendation is to be kept in mind]

n) Reg. 17A – New – Maximum No. of directorship – (1) Max. 8 listed co. directorships wef 01/04/19 and Max. 7 listed co. directorships wef 01/04/20. Provided, not to at as ID in more than 7 listed cos. (2) WTD/MD of listed co. can serve as ID in Max. 3 listed equitylisted cos.

o) Reg. 19(2A) & 19(3A) – New – NRC’s quorum to be 2 or 1/3rdof members whichever greater, including atleast 1 Independent Director in attendance; NRC to meet atleast once in a year. [N.B.: Terms of reference of NRC to be amended before 01/04/19, minuted in NRC/BM, updated in Co. website and changed in Annual Report text.]

p) Reg. 20 – Stakeholders Relationship Committee to look into various aspects of interest of shareholders, debenture holders and other security holders (previously, it was “the mechanism of redressal of grievances”. SRC to be have minimum 3 directors with minimum 1 independent director as members. Chairman of SRC shall be present at AGMs to reply to sh. queries. SRC to meet atleast once in a year. [N.B.: Points to be ensured, terms of ref. if any to be amended, requirement of minimum meeting to be minuted in SRC, BM]

q) Reg. 21 – Risk management committee – shall meet atleast once in a year, cyber security to be specifically included in risk monitoring, applicability made to Top 500 from top 100.

r) Reg. 23 – Related party transactions– 23(1) – Policy on materiality of RPTs and dealing with RPTs, policy should include clear threshold limits duly approved by the Board and policy to be reviewed by the Board atleast once in 3 years and updated accordingly. [N.B.: RPT policy to be amended, minuted in ACM, BM and uploaded to Co. website. Based on these amendments]

s) Reg. 23(1A) – RPT – Transaction(s) involving payments to related party for brand usage or royalty (individual transaction/ aggregate in a fy) to be considered material if exceeds 2% of consolidated turnover as per last audited financial statements.

t) Reg. 23(4) – Voting in material RPT– A Related party, whether party to transaction or not, cannot vote to approve material RPT. Previously requirement was to abstain from voting, now RPs can vote against, but not in favour of a material RPT.

u) Reg. 23(7) – Voting in Non-material RPT– A Related party, whether party to transaction or not, cannot vote to approve RPT. Previously requirement was to abstain from voting, now RPs can vote against, but not in favour of a RPT.

v) Reg. 23(9) – New – Disclosure of RPTs (on consolidated basis) to stock exchanges and Co. website on half yearly basis w.e.f. HY ending after 01/04/19,within 30 days of publication of standalone or consolidated financial results. Format of disclosure to be as per relevant Accounting Standards for annual results.

w) Reg. 24(1) – Requirement of having atleast 1 independent director of the listed entity on the Board of unlisted material subsidiary whether incorporated in INDIA or NOT. [N.B.: Listed entity having foreign material subsidiary to comply].For this purpose material subsidiary to mean whose Income/ Networth exceeds 20% of consolidated Income/ NW (notwithstanding that in Reg. 16(1)(c) definition of “material subsidiary” threshold limit is 10% of consolidated Income/ NW.

x) Reg. 24(4) – deletion of word “material” in explanationto Reg. 24(4) – Management of unlisted material subsidiary to periodically notify Board of listed entity about significant transactions and arrangements. Here significant transaction or arrangement is which exceeds / like to exceed 10% of the total Revenues/ Expenses/ Assets/ Liabilities of the unlisted subsidiary.[N.B.: Listed entity having unlisted subsidiary to place significant transactions and arrangements of such subsidiary before BM].

y) Reg. 24A– New – Secretarial audit for listed entities and material unlisted subsidiaries of listed entities which are incorporated in India, w.e.f. year ended 31/03/19.

z) Reg. 25(8) – New – Declaration of independence by IDs to include that he is not aware of any circumstances or situation, which exist or may be reasonably anticipated, that could impair or impact his ability to discharge his duties with an objective independent judgment and without any external influence.

aa) Reg. 25(9) – New – Board to take on record declaration of independence by IDs after undertaking assessment of its veracity. [N.B.: minuting to be done accordingly].

bb) Reg. 33(3)(b) – Listed companies having subsidiaries to mandatorily submit consolidated financial results on quarterly/year-to-date basis. Requirement of intimating stock exchange as to whether standalone/consolidated results will be submitted etc. omitted.

cc) Reg. 33(3)(g) – New – Statement of Cash Flows to be submitted with Half yearly standalone/ consolidated financial results. Effective date: 01/04/19.

dd) Reg. 33(3)(h) – New – for the purpose of quarterly consolidated financial results at least 80% of each of consolidated revenue, assets and profits, be subject to audit/LR.

ee) Reg. 33(3)(i) – New – Financial results for the last quarter to disclose by way of a note, the aggregate effect of material adjustments made in the results of that quarter which pertain to earlier periods.

ff) Reg. 33(8) – New – “The statutory auditor of a listed entity shall undertake a limited review of the audit of all the entities/ companies whose accounts are to be consolidated with the listed entity as per AS 21 in accordance with guidelines issued by the Board on this matter.”

gg) Reg. 34(1) – Substituted – Annual Report for year ending 31.03.19 onwards to be filed with stock exchange on or before commencement of dispatch to shareholders. In case of changes, revised copy to be submitted within 48 hours of AGM.

hh) Reg. 36 – Documents/ Information – 36(1) – Soft copy of annual report to be sent to email address of shareholders registered with company/ depository.

ii) Reg. 36(4) – New – Disclosures to stock exchanges to be in XBRL mode and in machine readable/ searchable format. Except in case of statutorily required to make disclosure in non-searchable format e.g. scan copy of documents. [N.B.: Enforced w.e.f. 9/5/18 and being complied]

jj) Reg. 36(5) – New – Explanatory statement of AGM notice to contain PROPOSED FEE, terms of appointment, material change in fee compared to outgoing auditor, rationale for such change, BASIS OF RECOMMENDATION for appointment and credentials of STATUTORY AUDITORS proposed to be appointment.

kk) Reg. 44 – Meetings of shareholders and voting (New heading) – 44(5)/(6) – New – Top 100entities as of 31st March of every FY to hold AGMs within 5 months from closure of FY and provide one-way live telecast of AGM proceedings;

ll) Reg. 46 – Website compliance – Information under regulation 46 to be disseminated on company website under a separate section. [N.B.: Separate section to be created in website, named accordingly and information compiled there]

mm) New 46(2)(s) – Website – Separate audited financial statement of each subsidiary to be uploaded on website atleast 21 days before AGM. [N.B.: Companies having subsidiary to comply].

nn) Schedule II, Part C, No. 21 – New – Role & review of information by Audit Committee – Audit Committee to review utilization of loans/ advances/ investments by holding company into subsidiary exceeding Rs.100 Cr. or 10% of asset size of subsidiary (whichever lower) including existing loans/ advances/ investments existing as on date of coming into force of this provision. [N.B.: Companies having subsidiary to comply].

oo) Schedule II Part D Para A Clause No. 6 – New – Role of NRC – NRC to recommend to the board, all remuneration, in whatever form, payable to senior management. [N.B.: Point to be inserted in NRC policy and accordingly minuting in NRC and BM required, further same change to be carried out in Policy annexure in Annual Report and change on Co. website]

pp) Schedule II Part D Para B – Substituted – Role of SRC expanded as under –

(1) Resolving the grievances of the security holders of the listed entity including complaints related to transfer/transmission of shares, non-receipt of annual report, non-receipt of declared dividends, issue of new/duplicate certificates, general meetings etc.

(2) Review of measures taken for effective exercise of voting rights by shareholders.

(3) Review of adherence to the service standards adopted by the listed entity in respect of various services being rendered by the Registrar & Share Transfer Agent.

(4) Review of the various measures and initiatives taken by the listed entity for reducing the quantum of unclaimed dividends and ensuring timely receipt of dividend warrants/annual reports/statutory notices by the shareholders of the company.

[N.B.: Point to be inserted in SRC and accordingly minuting in SRC and BM required before 01/04/2018, further same change to be carried out in Annual Report wherever role of SRC appears, reporting of investor issues and steps taken before the NRC to be done and minuted accordingly]

qq) Schedule II Part E Para D – Discretionary corporate governance requirements – Separate post of Chairman and CEO which was optional – omitted w.e.f. 01/04/2020. [N.B.: Companies having same person as Chairman & CEO to comply accordingly]

rr) Schedule III – Disclosure under Regulation 30 – Additions – In case of resignation of Auditor detailed reasons for resignation as given by auditor shall be disclosed latest by 24 hours. In case of resignation of Independent Director, he has to give detailed reason and confirmation that there is no other material reason and the Company’s disclosure to stock exchanges to mention such detailed reason and confirmation of no other material reason for resignation. [N.B.: Becomes relevant in case of resignation of auditor or independent director]

ss) Schedule IV – In case of modified opinion of auditor the management of the listed entity to mandatorily make estimate which auditor shall review and report accordingly, however that, the management may be permitted to not provide estimate on matters on matters like going concerned or sub-judice matters, in which case, management shall give reasons and auditor shall review and report accordingly. [N.B.: Becomes relevant in case of modified audit opinion]

tt) Schedule V – Annual Report – Changes: [IMPORTANT FOR 2018-19 ANNUAL REPORT]

a. Part A – Related Party Disclosure

Disclosures of transactions of the listed entity with any person or entity belonging to the promoter/promoter group which hold(s) 10% or more shareholding in the listed entity, in the format prescribed in the relevant accounting standards for annual results.

b. Part B – Management Discussion and Analysis

Additional disclosure requirement vide insertion of 1(i) & (j) –

Details of significant changes (i.e. change of 25% or more as compared to the immediately previous financial year) in key financial ratios, along with detailed explanations therefor, including: (i) Debtors Turnover (ii) Inventory Turnover (iii) Interest Coverage Ratio (iv) Current Ratio (v) Debt Equity Ratio (vi) Operating Profit Margin (%) (vii) Net Profit Margin (%) or sector-specific equivalent ratios, as applicable.

(j) details of any change in Return on Net Worth as compared to the immediately previous financial year along with a detailed explanation thereof.

c. Part C – Corporate Governance Report

In Corporate Governance Report, the relevant portion on BOARD OF DIRECTORS will be required to contain the following additional points –

-

-

- Clause 2(c)– of other directorships and other Committee memberships –Names of the listed entities where the person is a director and the category of directorship is required to be mentioned, additionally.

- Clause 2(h)– New – A chart or a matrix setting out the skills/ expertise/ competence of the board of directors specifying the following: (i) With effect from the financial year ending March 31, 2019, the list of core skills/expertise/competencies identified by the board of directors as required in the context of its business(es) and sector(s) for it to function effectively and those actually available with the board; and (ii) With effect from the financial year ended March 31, 2020, the names of directors who have such skills / expertise / competence.

- Clause 2(i)– New – Confirmation that in the opinion of the board, the independent directors fulfill the conditions specified in these regulations and are independent of the management.

- Clause 2(j)– New – detailed reasons for the resignation of an independent director who resigns before the expiry of his tenure along with a confirmation by such director that there are no other material reasons other than those provided.

-

In Corporate Governance Report, the relevant portion on GENERAL SHAREHOLDER INFORMATION will be required to contain the following additional point –

-

- Clause 9(q)– New – list of all credit ratings obtained by the entity along with any revisions thereto during the relevant financial year, for all debt instruments of such entity or any fixed deposit programme or any scheme or proposal of the listed entity involving mobilization of funds, whether in India or abroad.

In Corporate Governance Report, the relevant portion on OTHER DISCLOSURES will be required to contain the following additional points –

-

- Clause 10(h)– New – Details of utilization of funds raised through preferential allotment or qualified institutions placement as specified under Regulation 32 (7A).

- Clause 10(i)– New – a certificate from a company secretary in practice that none of the directors on the board of the company have been debarred or disqualified from being appointed or continuing as directors of companies by the Board/Ministry of Corporate Affairs or any such statutory authority.

- Clause 10(j)– New – where the board had not accepted any recommendation of any committee of the board which is mandatorily required, in the relevant financial year, the same to be disclosed along with reasons thereof: Provided that the clause shall only apply where recommendation of / submission by the committee is required for the approval of the Board of Directors and shall not apply where prior approval of the relevant committee is required for undertaking any transaction under these Regulations.

- Clause 10(k)– New – total fees for all services paid by the listed entity and its subsidiaries, on a consolidated basis, to the statutory auditor and all entities in the network firm/network entity of which the statutory auditor is a part.

Amendments effective October 1, 2018 –

a) Reg. 16(b)(ii) – member of the promoter group of the listed entity cannot be independent director.

b) Reg. 16(b)(viii) – New reg. – Independent Director – who is not a non-ID on the Board of another company on the Board of which any non-ID of the listed entity is an ID.

c) Reg. 25(1) – No person shall be appointed or continue as an alternate director for an independent director w.e.f. 01/10/18.

d) Reg. 25(9) – New – Top 500 companies to take directors and officers liability insurance for all their independent directors for such quantum and such risks as may be determined by its board of directors.

e) Reg. 29(1)(f) – Prior intimation of BM to be given to stock exchange if Bonus issue is to be considered.Earlier exemption if bonus was a tabled item has been withdrawn by omitting the proviso w.e.f. 01.10.18. [N.B.: Matter to be kept in mind if there’s plan for giving Bonus]

f) Reg. New 46(2)(r) – Website – W.e.f. 01/10/18 all credit ratings obtained for all outstanding instruments, updated immediately as and when there is any revision in any of the ratings.

N.B.: List of Top 500/ 1000/ 2000 Companies based on Market Cap required for determining applicability of requirements:

NSE LINK – https://www.nseindia.com/corporates/content/compliance_info.htm

BSE LINK – https://www.bseindia.com/static/about/downloads.aspx

Based on recommendation of Uday Kotak Committee, SEBI issued LODR Amendment notification dated 9th May, 2018 which is summarized above. Further in this context,

14) SEBI also issued Circular No. SEBI/HO/CFD/CMD/CIR/P/2018/79 dated 10thMay, 2018 applicable to equity listed companies, which is summarized hereunder:

- Disclosure on Board Evaluation in Annual Report –

- Observations of board evaluation carried out for the year,

- Previous year’s observations and actions taken,

- Proposed actions based on current year observations

- Group governance unit – Where the listed entity has large number of unlisted subsidiary –

- Monitoring governance through Governance Committee comprising board members,

- Group governance policy established by the listed entity,

- Board to decide on setting up governance committee/ policy.

- Disclosure on Medium & Long term Strategy in Management Discussion and Analysis – subject however to competitive position; Articulation of clear set of long term metrics corresponding to long term strategy for measurement of progress.

15) May 30, 2018 by the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) (Second Amendment) Regulations, 2018 vide notification No. SEBI/LAD-NRO/GN/2018/13

Amendment – Schedule I – (1) the listed entity either directly or through the depositories or through their RTA, shall use ECS, direct credit, RTGS, NEFT etc for making payment of dividend/interest on securities issued/redemption or repayment amount.

System-driven Disclosures in Securities Market – SAST & PIT

16) SEBI Circular No. SEBI/HO/CFD/DCR1/CIR/P/2018/85 dated May 28, 2018 titled System-driven Disclosures in Securities Market (Latest Circular on the matter)

Circular dated 01/12/15

Implementation of 1st phase w.e.f. 01/01/2016 – wherein database of existing holding of promoters/ promoter group at ISIN level was built based on PAN and depositories tagged the demat a/c. of P/PG at ISIN level. Depositories provided RTAs with daily trade data of Demat A/c. of P/PG and RTA got physical holding data (if any) and assimilated them and reported to stock exchanges for dissemination. [Acquisition, Sale, Pledge]. In case of subsequent change in P/PG, Company has to inform Depository through RTA.

Circular dated 21/12/16

Streamlining of 1st phase – wherein Depositories to provide the data of transactions beyond threshold limits to stock exchanges directly for dissemination w.e.f. 01/01/2017.

Circular dated 28/05/18

Implementation of 2nd phase – w.e.f. 01/08/2018 – SAST-29(1)/(2) & PIT-7(2)

- SAST Reg. 29(1) – Acquisition of 5% or more of voting power by anyone to be informed by acquirer to TC & Stock Exchanges within 2 working days.

- SAST Reg. 29(2) – Intimation of acquisition/ disposal by person already holding 5% or more, if such change exceeds 2% of total shareholding/ voting rights to be informed by acquirer to TC & Stock Exchanges within 2 working days..

- PIT Reg. 7(2) – Promoter/ Employee/ Director to intimate acquisition/ disposal amounting to traded value exceeding Rs.10 Lacs over a calendar quarter, within 2 trading days of transaction. Company to further intimate SE within 2 trading days of receipt of information/ becoming aware. [N.B.: Disclosure of the incremental transactions after any disclosure under this sub-regulation, shall be made when the transactions effected after the prior disclosure cross the threshold, i.e. Rs.10 Lacs.]

- PIT Strategy:To build database of existing shareholding of all Directors/ Employees by Upload/ Removal of PAN of Directors and employees upto 2 levels below CEO in NSDL and CDSL portal latest by 2 days of appointment/ cessation for PAN based tracking of transactions of such persons. Designated depository chosen by the Company shall aggregate and process the data and send to SEs data identified to be disclosed on a daily basis. Discrepancy to be informed by Company to respective SE [N.B.: HR Department has to inform CS immediately on appointment and removal of employees upto 2 levels below CEO]

- SAST strategy:Depositories to share data with each other on daily basis pertaining to non-promoter shareholders holding more than 2%. Shareholding details of non-promoter shareholders holding more than 5% to be provided by depositories to stock exchanges on daily basis. SEs shall identify data required to be disseminated under SAST. [N.B.: Discrepancy to be informed by Company to respective SE]

Existing system of disclosure by concerned parties shall continue.

17) The SEBI (LODR) (Third Amendment) Regulations, 2018 vide notification No. SEBI/LAD-NRO/GN/2018/21 dated May 31, 2018.

Amendments intended to align LODR with Insolvency & Bankruptcy Code:

- 2(1)(na) – New definition – “Insolvency Code” means the Insolvency and Bankruptcy Code, 2016 [No. 31 of 2016]

- 15(2A) – New – Provisions of regulation 17 (Board of Directors) made not applicable during corporate insolvency resolution process however role and responsibilities of BoD as per reg. 17 to be fulfilled by IRP/RP in accordance with section 17 and 23 of insolvency code.

- 15(2B) – New – Provisions of regulation 18, 19, 20 and 21 (AC, NRC, SRC, RMC) made not applicable during corporate insolvency resolution process period however role and responsibilities of committees to be fulfilled by IRP/RP.

- New proviso to Reg. 23(4) – Restriction that no related party shall vote to approve material related party transaction not to apply in respect of a resolution plan approved u/s. 31 of the insolvency code subject to such event being disclosed to stock exchanges within 1 day of being approved.

- 24(5)/(6) amended to include approved resolution plan (intimated to stock exchanges within 1 day of approval) as a basis of disposing shares of material subsidiary to below 50% or cease to exercise control over it; and also selling/disposing/leasing assets 20% or more of the assets of material subsidiary during a financial year; These were earlier subject to prior special resolution or Court/ Tribunal order.

- Addition of Reg. 31A(9) – not being mentioned here since replaced and taken care of in LODR Sixth amendment dated 16/11/18.

- 37(7) – New – Conditions and compliances by listed companies as per reg. 37 and by Stock exchanges as per reg. 94 in cases of Scheme of Arrangement made inapplicable to a restructuring proposal approved as part of a resolution plan by the Tribunal under section 31 of the Insolvency Code, subject to the details being disclosed to the recognized stock exchanges within one day of the resolution plan being approved.

- Schedule III Part A – New Point No. 16(a) – (l) – 12 events in relation to the corporate insolvency resolution process (CIRP) of a listed corporate debtor under the Insolvency Code included which are to be disclosed under Regulation 30 without applying materiality test.

18) The SEBI (LODR) (Fourth Amendment) Regulations, 2018 vide notification No. SEBI/LAD-NRO/GN/2018/24 dated June 8, 2018.

Amendment in brief – Regulation 40 amended to the effect that except in case of transmission or transposition of securities, requests for effecting transfer of securities shall not be processed unless the securities are held in the dematerialized form with a depository. Omission of Schedule VII(A)(2). Effective date: 05/12/2018. Application extended till 01/04/2019 vide Notification dated 30/11/2018.

19) NSE Circular No.NSE/CML/2018/25 dated July 6, 2018 titled “Disclosure of Unpublished Price Sensitive Information by Listed Companies”

Background: Availability of Unpublished Price Sensitive Information (UPSI) with certain section of Company insiders & market intermediaries & market participants, instances of leakage of UPSI before crystallization of major events/contingent liabilities, finalization of quarterly financial results etc. and their public disclosure/dissemination.

Guidelines: In the above backdrop, the Circular advises listed companies to –

-

- Disclose provisional figures/amounts before crystallization/finalization of final figures/amounts, if there is likelihood of crystallization, so that information becomes generally available and UPSI is not misused.

- Above disclosure may be avoided in the interest of stakeholders (e.g. impending JV, Merger, Settlement of one out of many labour disputes, etc.) and listed company has to ensure confidentiality/non-leakage of such information.

- In case of observance of rumours in any media (including social media), the company should suo-motu make appropriate disclosure to stock exchanges without waiting for query.

- In case of inadvertent passage of UPSI to any third party, the company should suo-motu make appropriate disclosure to stock exchanges

20) The SEBI (LODR) (Fifth Amendment) Regulations, 2018 vide notification No. SEBI/LAD-NRO/GN/2018/30 dated September 6, 2018.

Amendments brought in for Security Receipt Listed Companies –

- New definitions etc. and replacement of symbols SEBI (Public Offer and Listing of Securitised Debt Instruments) Regulations, 2008 with SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008.

- New Chapter VIIIA – Obligations Of Listed Entity Which Has Listed Its Security Receipts

- New – Part E: Disclosre Of Events Or Information To Stock Exchanges: Security Receipts in Schedule III (Regulation 30)

21) SEBI Circular No. SEBI/HO/MIRSD/DOS3/CIR/P/2018/139 dated 6th November, 2018 titled Standardised norms for transfer of securities in physical mode – documentation procedure for physical transfers in case of :

- Non-availability of PAN of the transferor for transfer deeds executed prior to December 01, 2015: transfer deeds executed prior to notification of LODR may be registered with or without the PAN of the transferor as per the requirement of quoting PAN under the applicable Income Tax Rules.

- Mismatch of name in PAN card vis-à-vis name on share certificate/ transfer deed: transfer shall be registered on submission of any of the four following additional documents explaining the difference in names: Copy of Passport/ Legally recognized Marriage Certificate/ Gazette notification regarding change in name/ Aadhar Card.

- Major mismatch / Non-availability of transferor’s signature: Refer to Schedule VII Para (B)(2) and above circular for procedure to be followed.

22) SEBI Circular No. SEBI/HO/CFD/CMD1/CIR/P/2018/141 dated November 15, 2018 on DISCLOSURE REGARDING COMMODITY RISKS BY LISTED ENTITIES

- ALL Listed entities are required to make disclosure in Annual Report as part of its Corporate Governance Report details of commodity risks, foreign exchange risks and hedging activities in the prescribed format provided in the circular which is as under:

[N.B.: Risk management policy to take into account total exposure in commodities, commodity risks faced by the entity, hedged exposures etc., RM policy to undergo change, minuting in Audit Committee & Board meeting required, Annual Report 2018-19 onwards have to include details in given format – subject to materiality of exposure as per policy. Logically, in case exposures are non-material a statement in that regard should be mentioned]

23) The SEBI (LODR) (Sixth Amendment) Regulations, 2018 vide notification No. SEBI/LAD-NRO/GN/2018/47 dated November 16, 2018.

Amendment in brief:

- 2(1)(ia) – New definition – “fugitive economic offender” shall mean a person declared as a fugitive economic offender under section 12 of the Fugitive Economic Offenders Act, 2018.

- 31(4) – New – “All entities falling under promoter and promoter group shall be disclosed separately in the shareholding pattern appearing on the website of all stock exchanges having nationwide trading terminals where the specified securities of the entity are listed, in accordance with the formats specified by the Board.” [N.B.: Amendment applicable for shareholding pattern to be filed for the QE 31-12-2018 onwards, hence entities need to decide upon the same]

- Substitution of Reg. 31A – Conditions for re-classification of any person as promoter/ public. [Refer to notification for details] – Important to note that disclosure within 24 Hr. under Regulation 30 is required on receipt of request for reclassification from promoter.

- 102(2) & (3) – Inserted – Application to SEBI along with non-refundable fee of Rs.1 Lac for relaxation of strict enforcement of the regulations on certain grounds.

- Corporate Governance Report required to contain the following as per new Clause C(10)(l) to Schedule V

Disclosures in relation to the Sexual Harassment of Women at Workplace (Prevention, Prohibition and Redressal) Act, 2013:

a. number of complaints filed during the financial year

b. number of complaints disposed of during the financial year

c. number of complaints pending as on end of the financial year

[N.B.: Annual Report 2018-19 to cover this point]

- Changes in documents required for transmission of securities – Schedule VII(C)(2)(b) substituted. [B.: To be referred when dealing with transmission cases]

24) NSE directive dated 30th November, 2018 on compliance of Regulation 39(3) – Intimation of information on loss of share certificate and issue of duplicate share certificate

- Submission of hard copy of intimation under Regulation 39(3) not to be considered as compliance. Submission of intimation shall be only through NEAPS portal under dedicated tab.

- Copy of receipt of information of loss of share certificate/ issue of duplicate share certificate reflecting the date of receipt of such information by the Company to be attached with the intimation letter.

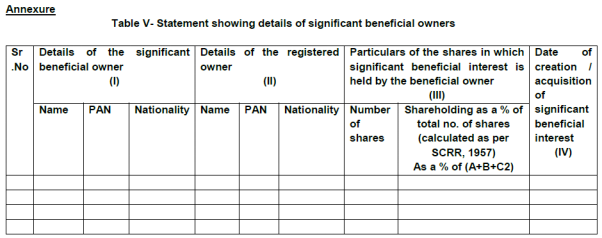

25) SEBI Circular No. SEBI/HO/CFD/CMD1/CIR/P/2018/149 dated December 7, 2018 on Disclosure of significant beneficial ownership in the shareholding pattern

Quarterly Shareholding Pattern w.e.f. QE March 31, 2019 to contain SBO details in given format:

Disclaimer: Disclaimer: Interpretation of the Author are his personal views and the same are being published in academic interests only. Readers are advised to refer to relevant provisions for compliance.

About the Author

Abhishek Seth is a Company Secretary & Masters in Economics from Calcutta University. He is currently associated with Albert David Ltd., Kolkata as Asstt. Company Secretary.

Abhishek Seth is a Company Secretary & Masters in Economics from Calcutta University. He is currently associated with Albert David Ltd., Kolkata as Asstt. Company Secretary.

Feedbacks are welcome at cs.abhishekseth@gmail.com.

Brilliant article