Summary: The Income Tax Department issues various notices, letters, and orders to individual taxpayers for compliance and assessment purposes. Intimations under Section 143(1) notify taxpayers about tax calculations after return processing. Defective return notices under Section 139(9) require rectification within 15 days. Section 245 notices inform taxpayers about adjustments of outstanding tax demands with refunds. Rectification orders under Section 154 address errors in tax assessments. Refund confirmation requests require taxpayer responses. Scrutiny notices under Section 143(2) initiate detailed assessments, while Section 142(1) notices request further details before assessments. Section 143(3) orders finalize assessments based on submissions. Section 119(2) orders allow exemptions and deductions under special circumstances. Best Judgment Assessments under Section 144 apply when taxpayers fail to file returns or respond to inquiries. Summons under Section 131 enable tax authorities to gather information. Section 133 empowers authorities to demand financial details. Section 148 notices investigate income escaping assessment, with time limits based on undisclosed income amounts. Section 156 demands tax payments, and Section 143(1)(a) communicates proposed return adjustments. Each notice requires timely responses to avoid penalties, reassessments, or legal actions.

Types of Notices/Letters/Orders issued by the Income Tax Department to the Individual Taxpayers

In the month of December 2024, the Income-tax Department released data relating to the Income-tax returns (ITR) filed. As per the date, for Financial Year (FY) 2023-24, 8.13 crore ITR were filed (including Revised Return) relating to Individual out of total ITR of 8.61 crore. Further, as per the data, for FY 2023-24, 7.63 crore Individuals filed ITR out of total ITR filed of 8.09 crore.

Category of Individuals are significant in proportion of the total Assessees filing ITR in India which will also significantly include Individuals having salary income as around 30% (appx.) of total employment works in service sector.

In this article, we will discuss few types of notices / letters / orders that can be issued by the Income-tax Department to the Individual taxpayers.

1. Intimation under section 143(1) of the Income-tax Act (the Act) – Intimation under section 143(1) of the Act is issued by the Income Tax Department after processing of your Income-tax return determining tax refund, tax payable or no demand / no refund. Intimation compares the details of the source of income, deductions, exemptions & tax relief claimed, tax payable & tax deducted provided in the ITR by the assessee and determined by the Income-tax Department.

Further, as per section 143 of the Act, an intimation is required to be sent within 9 months from the end of financial year in which return is filed. The acknowledgement of the return shall be deemed to be the intimation in a case where no sum is payable by, or refundable to, the assessee and where no adjustment has been made.

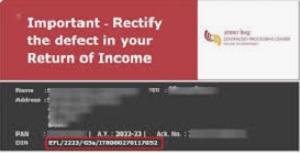

2. Defective return notice under section 139(9) of the Act – Defective notice return u/s 139(9) of the Act is issued by the Income Tax Department intimating the defect to the assessee and give him the opportunity to rectify the defect within the period of 15 days from the date of such intimation. In this case, the taxpayer either agree with the defect & file the revised ITR in response to the intimation or disagree with the defect & provide a response / comment in relation to the intimation issued.

Further, in case, the taxpayer has not provided any response or filed a revised ITR within the time allowed, the ITR shall be treated as invalid and the provisions of the Act shall apply as if the assessee has failed to furnish the ITR.

One of the major reasons for issue of defective return notice is mismatch in total receipts appearing in Form 26AS / Annual Tax Statement and total receipts offered to tax in the ITR filed.

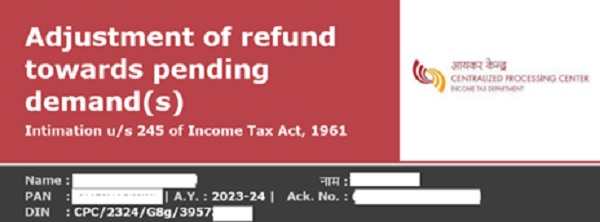

3. Adjustment of Demand notice under section 245 of the Act – As per section 245 of the Act, a notice / intimation for adjustment of demand for an Assessment Year (AY) or multiple AYs with refund due of the latest FY is issued by the Income Tax Department.

Further, in response to the notice, the taxpayer has to provide the response within 30 days from the date of notice issued – either agree with the demand & pay the said demand or disagree with the demand & provide the reason for disagree with demand. The reason for disagree with demand includes demand already paid, demand is incorrect, rectification or appeal is pending etc.

Further, without notice / intimation, the Income-Tax Department cannot adjust the demand with the refund determined & to be issued.

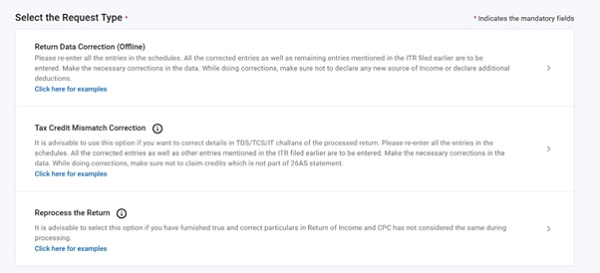

4. Rectification Order under section 154 of the Act – Rectification under section 154 of the Act can be filed online on the Income-tax portal as well as with jurisdictional Assessing Officer (when the rectification rights are transferred) if there is a mistake apparent from record to amend the intimation passed under section 143(1).

Further, no amendment under this section shall be made after the expiry of 4 years from the end of the financial year in which the order sought to be amended was passed. However, where an application for amendment under this section is made by the assessee to an income-tax authority, the authority shall pass an order, within a period of 6 months from the end of the month in which the application is received by it – making the amendment or refusing to allow the claim.

Following are the options available to file the rectification request online on Income-tax portal:

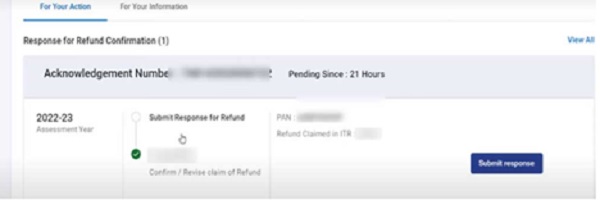

5. Response for Refund Confirmation – Intimation in the form of email is issued by the Income Tax Department in relation to “Response to Confirm or Revise Claim of Refund” in the income-tax return filed and the response to be filed within 30 days from the date of communication online on the Income-tax portal.

Further, in case of refund claimed in the income-tax return filed in not correct, then revised return can be filed in response to the notice or if the refund claimed is correct, then only response needs to be provided on the Income-tax portal.

6. Issue Letter – Issue letter is generally issued by the jurisdictional Assessing Officer in relation to various reasons including requesting to provide submission for outstanding tax demand appearing on the Income-tax portal or provide the supporting documents in relation to any grievance / rectification filed with the jurisdictional Assessing Officer.

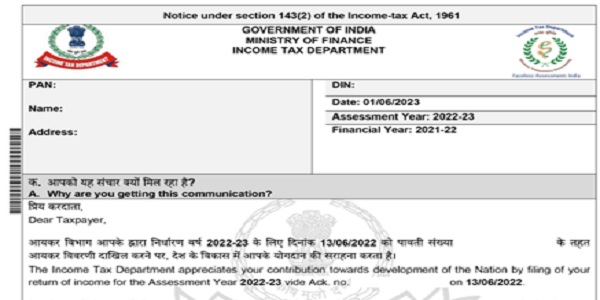

7. Scrutiny Assessment Notice under section 143(2) of the Act – Where a return has been furnished under section 139 or in response to the notice under section 142(1), the Assessing Officer or prescribed income-tax authority consider it necessary to ensure that the assessee has not understated the income or has not computed excessive loss or has not under-paid the tax in any manner, shall serve on the assessee a notice requiring him either to attend the office of Assessing Officer or to produce, or cause to be produced before the Assessing Officer any evidence on which the assessee may rely in support of the return.

Further, the scrutiny assessment can be limited relating to 1-2 issues or can be complete scrutiny requesting to provide complete documents for all type of income offered in the income-tax return etc.

Further, no notice under this section shall be served on the assessee after the expiry of 3 months from the end of the financial year in which the return is furnished.

8. Inquiry before Assessment Notice under section 142(1) of the Act – For the purpose of making an assessment, the Assessing Officer may serve notice on any person who has filed the return under section 139 or the time to file the return under section 139(1) has expired or detailed questionnaire subsequent to notice under section 143(2) requesting the assessee to provide specific details relating to issues raised in the notice issued under section 143(2), if it is limited scrutiny assessment or to provide complete details relating to bank statement, income details, TDS / TCS claimed, residential status, disallowances in tax audit report, deductions or exemptions claimed etc.

9. Assessment Order under section 143(3) of the Act – After going through the submissions provided by the assessee in response to notice issued under section 143(2) & section 142(1), the Assessing Officer shall in writing, make an assessment of total income or loss of the assessee and determine the sum payable by him or refund of any amount due to him on the basis of such assessment.

Further, as of February 2025, an order of Assessment may be made at any time before the expiry of 12 months from the end of the Assessment Year in which the income was first assessable.

Further, where a return is furnished in consequence of an order under section 119(2)(b), an order of assessment under section 143 may be made at any time before the expiry of 12 from the end of the financial year in which such return was furnished.

10. General or Special Order under section 119(2) of the Act – As per section 119(2), the Central Board of Direct Taxes (CBDT) may, if it considers it desirable or expedient so to do for avoiding genuine hardship in any case or class of cases, by general or special order, authorise any income-tax authority, not being a Joint Commissioner (Appeals) or a Commissioner (Appeals) to admit an application or claim for any exemption, deduction, refund or any other relief under this Act after the expiry of the period specified by or under this Act for making such application or claim and deal with the same on merits in accordance with law.

Further, CBDT vide its Circular No. 11/2024 dated October 1, 2024 authorises Income-tax Authorities to admit an application or claim for refund and carry forward of loss and set off thereof under section 119(2)(b) of the Income-tax Act.

11. Best Judgment Assessment under section 144 of the Act – If any person—

(a) fails to make the return required under section 139(1) and has not made a belated return under section 139(4) or a revised return under section 139(5) or an updated return under section 139(8A), or

(b) fails to comply with all the terms of a notice issued under section 142(1) or fails to comply with a direction issued under section 142(2A), or

(c) having made a return, fails to comply with all the terms of a notice issued under section 143(2),

the Assessing Officer, after taking into account all relevant material which the Assessing Officer has gathered, shall, after giving the assessee an opportunity of being heard, make the assessment of the total income or loss to the best of his judgment and determine the sum payable by the assessee on the basis of such assessment.

Provided that an opportunity shall by given by the Assessing Officer by serving a notice calling upon the assessee to show cause on a date and time specified in the notice that why the assessment should not be completed to the best of his judgment. However, no show cause notice to be issued where notice under section 142(1) has already been issued prior to Assessment under this section.

Further, where a return is furnished in consequence of an order under section 119(2)(b), an order of assessment under section 144 may be made at any time before the expiry of 12 from the end of the financial year in which such return was furnished.

12. Summon issued under section 131 of the Act – Section 131 grants following power to Assessing Officer, Deputy Commissioner (Appeals), Joint Commissioner, Joint Commissioner (Appeals), Commissioner (Appeals), Principal Chief Commissioner or Chief Commissioner or Principal Commissioner or Commissioner and the Dispute Resolution Panel:

(a) discovery and inspection;

(b) enforcing the attendance of any person, including any officer of a banking company and examining him on oath;

(c) compelling the production of books of account and other documents; and

(d) issuing commissions.

Section 131 gives power to Tax Authorities to issue summons or to force attendance of any person for being examined on oath or to compel production of books of account and other documents if any proceeding is pending.

As per section 131(1A), if the Principal Director General or Director General or Principal Director or Director or Joint Director or Assistant Director or Deputy Director, or the authorised officer under section 132, before he takes action under clauses (a) to (d) above, has reason to suspect that any income has been concealed, or is likely to be concealed, by any person or class of persons, within his jurisdiction, then, for the purposes of making any enquiry or investigation relating thereto, it shall be competent for him to exercise the powers provided in section 131 even if no proceeding is pending.

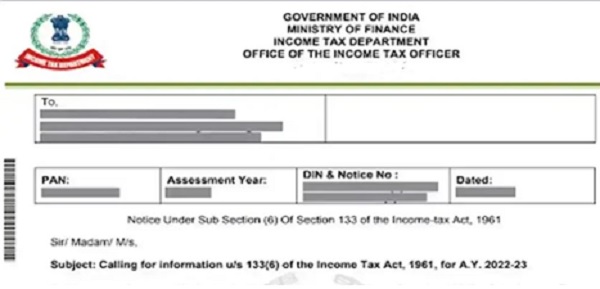

13. Power to call for Information under section 133 of the Act – As per section 133, the Assessing Officer, the Deputy Commissioner (Appeals), the Joint Commissioner or the Joint Commissioner (Appeals) or the Commissioner (Appeals) may require any class of persons including firm, Hindu Undivided Family (HUF), trustee, guardian, agent, any dealer, broker, banking company or any officer thereof any assessee to furnish the information as provided in the section and requested by the officer for the purpose of collection of financial or business related information.

Provided further that the power in respect of an inquiry, in a case where no proceeding is pending, shall not be exercised by any income-tax authority below the rank of Principal Director or Director or Principal Commissioner or Commissioner, other than the Joint Director or Deputy Director or Assistant Director, without the prior approval of the Principal Director or Director or, as the case may be, the Principal Commissioner or Commissioner.

14. Issuance of notice under section 148 of the Act where income has escaped assessment – The Assessing Officer shall, subject to the provisions of section 148A, issue a notice to the assessee, along with a copy of the order passed under 148A(3), requiring him to furnish, within such period as may be specified in the notice, not exceeding 3 months from the end of the month in which such notice is issued, a return of his income or income of any other person in respect of whom he is assessable under the Act during the previous year corresponding to the relevant assessment year.

Further, no notice shall be issued unless there is information with the Assessing Officer which suggests that the income chargeable to tax has escaped assessment in the case of the assessee for the relevant assessment year.

Further, following are the time limits to issue notice under section 148 & 148A (as of February 2025):

– No notice under section 148 shall be issued for the relevant Assessment Year—

(a) if 3 years and 3 months have elapsed from the end of the relevant assessment year, unless the case falls under clause (b);

(b) if 3 years and 3 months, but not more than 5 years and 3 months, have elapsed from the end of the relevant assessment year unless the Assessing Officer has in his possession books of account or other documents or evidence related to any asset or expenditure or transaction or entries which show that the income chargeable to tax, which has escaped assessment, amounts to or is likely to amount to INR 50 lakhs or more.

– No notice to show cause under section 148A shall be issued for the relevant Assessment Year—

(a) if 3 years have elapsed from the end of the relevant assessment year, unless the case falls under clause (b);

(b) if 3 years, but not more than 5 years, have elapsed from the end of the relevant assessment year unless the income chargeable to tax which has escaped assessment, as per the information with the Assessing Officer, amounts to or is likely to amount to INR 50 lakhs or more.

Further, no order of assessment, reassessment or recomputation shall be made under section 147 in relation to income escaping assessment after the expiry of 12 months from the end of the financial year in which the notice under section 148 was served.

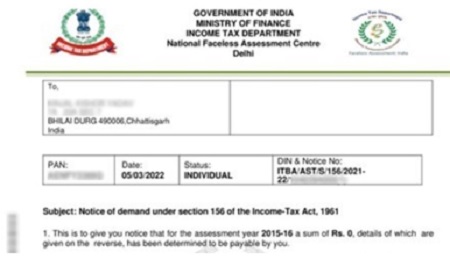

15. Notice of demand issued under section 156 of the Act – When any tax, interest, penalty, fine or any other sum is payable in consequence of any order passed under this Act, the Assessing Officer shall serve upon the assessee a notice of demand under section 156 in the prescribed form specifying the sum so payable. Generally, notice of demand is issued even if there is NIL demand is payable.

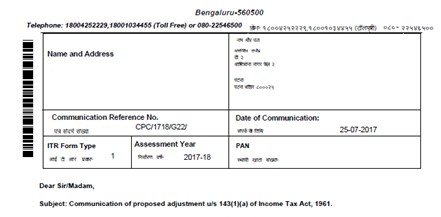

16. Communication of proposed adjustment under section 143(1)(a) of the Act – Where a return has been made under section 139, or in response to a notice under section 142(1), such return shall be processed in the following manner, namely:

(a) the total income or loss shall be computed after making the following adjustments, namely:

(i) any arithmetical error in the return;

(ii) an incorrect claim, if such incorrect claim is apparent from any information in the return;

(iii) disallowance of loss claimed, if return of the previous year for which set off of loss is claimed was furnished beyond the due date specified under section 139(1);

(iv) disallowance of expenditure or increase in income indicated in the audit report but not taken into account in computing the total income in the return;

(v) disallowance of deduction claimed under section 10AA or under any of the provisions of Chapter VI-A under the heading “C.—Deductions in respect of certain incomes”, if the return is furnished beyond the due date specified under section 139(1); or

(vi) addition of income appearing in Form 26AS or Form 16A or Form 16 which has not been included in computing the total income in the return

Provided that no such adjustments shall be made unless an intimation is given to the assessee of such adjustments either in writing or in electronic mode and if no response is received within 30 days of the issue of such intimation, such adjustments shall be made.

Provided also that no adjustment shall be made under sub-clause (vi) in relation to a return furnished for the assessment year commencing on or after the 1st day of April, 2018.

********

Author can be reach out for any queries at email ID – canavneetsingh1@gmail.com

Disclaimer: This article serves an educational purpose and should not be considered as professional advice. Consultation with a qualified individual is recommended before making any decisions based on the content provided. The author bears no responsibility for any actions taken based on this article.

Author Bio

u/s 148 no re-opening of accounts could be made after 5 years and 3 months from the end of the assessment year even when the escaping income in the form of assets is more than Rs.50 lakhs. Is it correct. Is it not 10 years from the end of the assessment year. Kindly clarify

No, as of February 2025, it is 5 years and 3 months. Budget 2025 proposals (if any) are not considered in the above article as it is not incorporated in the Income Tax Act.