Tax Audit Applicability for A.Y. 2020-21 under Section 44AB vis-à-vis Section 44AD / Section 44ADA of the Income Tax Act, 1961

We have attempted to provide a compendious view of Tax Audit Applicability for A.Y. 2020-21 under Section 44AB vis-à-vis Section 44AD / Section 44ADA of the Income Tax Act, 1961.

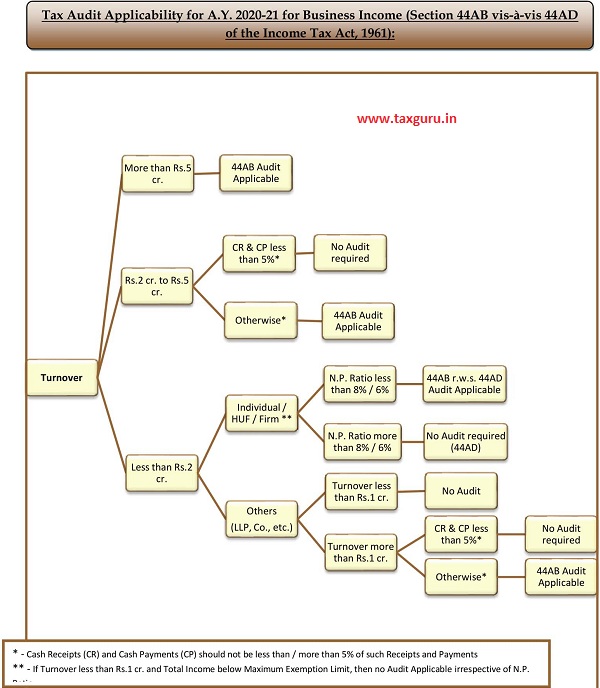

Tax Audit Applicability for A.Y. 2020-21 for Business Income (Section 44AB vis-à-vis 44AD of the Income Tax Act, 1961)

Tax Audit Applicability for A.Y. 2020-21 for Professional Income (Section 44AB vis-à-vis 44ADA of the Income Tax Act, 1961)

Disclaimer: This document is meant for the recipient for use as intended and not for circulation. The information contained herein is from the public domain, company published data or sources believed to be reliable. The information published is analyzed by the respective analyst publishing the report. The data contained herein doesn’t represent any view that is intended to influence any decision making by the person reading the content of this report. We do not guarantee the accuracy, adequacy or completeness of any Data in the Report and is not responsible for any errors or omissions or for the results obtained from the use of such Data.

Author Bio

A partnership firm doing consulting business (export of services) will it be classified under 44 AD?

A PARTNERSHIP FIRM TOTAL TURNOVER RS. 22 LAC AND NET PROFIT AFTER GIVEN INTEREST AND REMUNERATION IS ZERO.IS AUDIT IS REQURIED FOR THIS FIRM?

Ms. Khayati,

I am a marketing professional having income of Rs. 7 lakhs from consultancy in FY: 2019-20 and loss from Intraday Trading at stock market. What does turnover mean under this section? Do i have to go for audit? Pls clarify.

TAX AUDIT LIMIT FOR A CA. CONDUCT IS 60. IN THIS LIMIT AUDIT U/S 44AD IS NOT INCLUDED. WHAT IS THE T/O LIMIT U/S 44AD FOR THIS PURPOSE 1 OR 2 CRORES

As per my view, Requirement of audit (Range 1Cr-2Cr) will not be applicable under Section 44AB(e), because erstwhile requirement of getting books of account audited if profit is below 8%/6% has been removed. So even if it is loss or below, assessee can escape audit.

If turnover less then 5 cr. and CR and CP less then 5%. whether the assessee will opt for 44AD(presumptive) disclosing profit @6% for 95% turn over and 8% for 5% of turnover or is to file unaudited PL and BS showing even less profit. Pl. reply.

very fine and simple presentation of complex provision of section 44AD and 44ADA of income tax act 1961