When any person purchases an immovable property from a non-resident, TDS is required to be deducted on the amount of the capital gain (not on the sale proceeds) arising to such non-resident as per Section 195 of the Income Tax Act.

Section 195:

“(1) Any person responsible for paying to a non-resident, not being a company, or to a foreign company, any interest (not being interest referred to in section 194LB or section 194LC) or section 194LD or any other sum chargeable under the provisions of this Act (not being income chargeable under the head “Salaries”) shall, at the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by the issue of a cheque or draft or by any other mode, whichever is earlier, deduct income-tax thereon at the rates in force.

………

(2) Where the person responsible for paying any such sum chargeable under this Act (other than salary) to a non-resident considers that the whole of such sum would not be income chargeable in the case of the recipient, he may make an application in such form and manner to the Assessing Officer, to determine in such manner, as may be prescribed, the appropriate proportion of such sum so chargeable, and upon such determination, tax shall be deducted under sub-section (1) only on that proportion of the sum which is so chargeable.”

Please note that “resident but not ordinary resident” also falls under “resident” status for this purpose.

Applicable TDS rates on the purchase of property from NRI:

The Indian resident purchasing a property from Non-resident Indian is required to deduct TDS as follows:

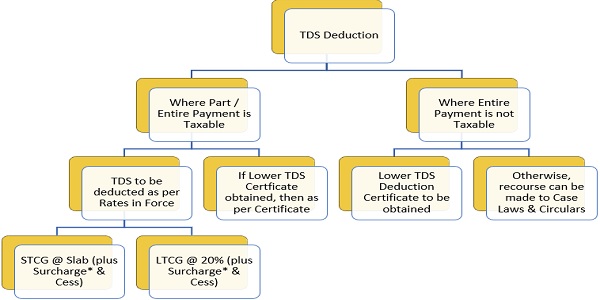

> TDS Deduction as per Rates in Force: TDS is to be deducted by the buyer as per provisions of Section 195:

> In case the property is held for more than two years, then there would be ‘Long Term Capital Gain’ and TDS would be deducted at the rate of 20% (plus Surcharge as applicable and Cess).

> In case the property is held for less than two years, then there would be ‘Short Term Capital Gain’ and TDS would be deducted at the applicable Income Tax Slab Rate (plus Surcharge as applicable and Cess).

> Lower TDS Deduction Provisions: The facility of lower TDS rate is also available in case of TDS deduction on the purchase of property from NRI:

> An Application in Form No. 13 needs to be made to the Jurisdictional Assessing Officer.

> The Assessing Officer shall issue a certificate of lower TDS deduction within a period of 30 days after considering the Income of the Payee (NRI).

> Based on the certificate of lower TDS deduction, the buyer of the property is required to deduct “such TDS” on “such Payment” within “such Date” as mentioned in the certificate.

> The Lower TDS Deduction Certificate shall be applicable only for the Amount mentioned in the Certificate and only for such Period (usually upto the end of the Financial Year) as per Certificate.

> Lower TDS is applicable only for Tax Rate – not for Surcharge Rate Some Points to note:

> OCI card holders can also avail the lower TDS benefit by filing in form 13.

> In case of Home Loan, TDS is to be deducted when payment is made to the Seller.

> TDS is to be deducted on token / advance payments as well depending on presence of lower deduction certificate.

Form No. 13: Application for Lower or Nil TDS Deduction:

An application for lower or no deduction of TDS is to be done in Form No. 13. The Central Board of Direct Taxes, vide Notification No. 8/2018 dated 31st December 2018, has provided the procedure for electronic filing of Form No. 13 online and generation of the certificate through TRACES.

Form 13 Online Filing & Generation:

1. Registration in the TRACES portal is mandatory. Consequently, if the taxpayer is not registered in TRACES, then, one needs to first obtain registration in TRACES. For registration in TRACES please follow the under mentioned steps:

i. Visit the site https://contents.tdscpc.gov.in/

ii. Click on Login and select Register as New User option;

iii. Select ‘Taxpayer’ from the drop-down list;

iv. After selecting Proceed, the registration form would be displayed;

v. Fill in the appropriate information and submit and the registration in TRACES would be done.

2. Login in TRACES and under ‘Statements / Form’ tab select ‘Request for Form 13’;

3. Form 13 would be displayed and appropriate details need to be filled up by the applicant; and

4. Once all the details are filled up and appropriate documents are uploaded, the applicant is required to submit the form

13 either by using Digital Signature or by using EVC.

Generation of Certificate:

After successful submission of an application in FORM 13 through TRACES by the applicant, on the basis of the information/details furnished in FORM 13, the application shall be forwarded to the appropriate TDS assessing officer.

After carrying out appropriate verification of information/details furnished in FORM 13, and on receipt of approval of the competent authority, the Assessing Officer would generate the certificate.

Since the certificate would be system generated, there will not be any requirement of the signature. The applicant, as well as the deductor, can download the generated certificate through their TRACES login.

Standard Requirements for making an Applicant u/s 197:

1. Name, PAN and Jurisdictional Assessing Officer details

2. Contact person (responsible for TDS) details

3. Income/Tax payment details:

i. Details of last three years income and projection for current year to be provided

ii. Tax payment details for last 3 years to be filled

iii. Details of tax already deducted / paid for current FY to be filled

iv. Details of demand outstanding before any Income Tax authority to be provided including details of AY, amount outstanding , section and current status(whether any stay granted)

v. Particulars of default as reported in column 27 of tax audit report (Form No. 3CD) for last three years to be provided. Reasons for the default and corrective action taken should also be mentioned

vi. Details of pending scrutiny assessment or penalty proceedings to be provided

vii. Details of receipt/utilization/accumulation for last 10 years to be provided if the applicant is a person referred to in Rule 28AB(1)

4. TAN details, if applicable

5. Details of Cumulative Tax likely to be foregone by issue of certificate:

i. Section of the Income Tax Act under which the receipt is liable for TDS

ii. Cumulative amount of projected receipt under this section

iii. No. of parties from whom the receipt is expected

iv. Normal Rate of TDS applicable as per Income Tax Act if no certificate is issued

v. Rate at which lower deduction certificate is requested for receipts covered under this section

vi. Tax Foregone

vii. Total Tax foregone as per certificate proposed

viii. Tax foregone as per certificate, if any issued earlier during Financial Year: to be filled if certificate for lower deduction issued earlier for the same financial year

ix. Cumulative tax foregone

6. Deductor wise details with respect to payments for which certificate is sought to be provided:

i. Name of the deductor from whom payment is expected

ii. TAN

iii. Current correspondence address of the deductor

iv. Email ID of the deductor

v. Expected receipt amount to be filled

vi. TDS Section under which receipt is covered

7. Documents to be submitted along with application:

i. ITR-V/Acknowledgement of filing Income Tax return for relevant financial years to be provided

ii. Computation of Income for relevant financial years

iii. Balance Sheet and Profit and Loss Account for relevant financial years with all Schedules/Annexures

iv. Audit report in Form-3CD/3CA-3CB/10B ( Whichever is applicable) for relevant financial years

v. Complete Chart showing all the payments made, the head of such expenses (e.g. contract payment, legal professional fees, etc.) and the section under which tax has been deducted by the applicant

vi. Copy of Purchase Agreement of said property

vii. Copy of MOU or Draft Agreement for Sale of property

viii. Working of LTCG

ix. Proof of Cost of improvement, if any

x. Payment details of new flat claiming deduction u/s 54 / 54F

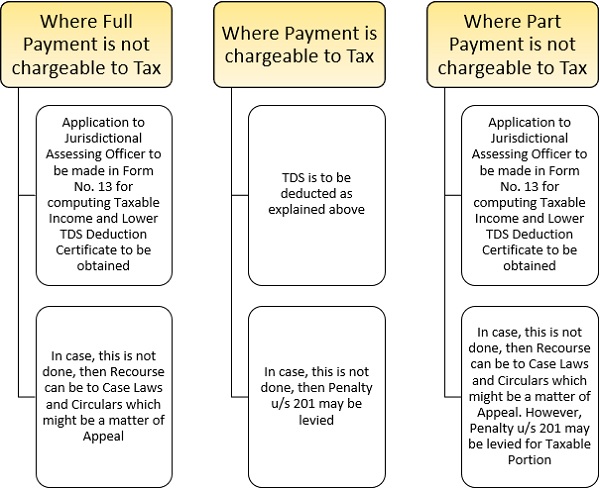

Various situations that can arise for the applicability of section 195 as under:

(a) In case of a bona fide belief by the payer that no part of the payment bears income character, it is not mandatory for him to undergo the procedure of section 195(2) before making any payment to a non-resident. However, if the Department is of the view that the payer ought to have deducted tax at source, it will have recourse under section 201 of the Act. Thus, here the interest of the Revenue is protected. In the proceedings under section 201, the Assessing Officer will determine the portion chargeable to tax according to the provisions of the Act and determine the tax payable by the payer. The Assessing Officer is bound to determine the income chargeable to tax in accordance with the provisions of the Act. In any case, the liability of the payer cannot exceed that of the payee and if the payer is dissatisfied with the order under section 201, he will have recourse to appeal against the said order. Thus, the interests of both the parties are protected.

(b) If the payer believes that whole of the payment is chargeable to tax and if he deducts and pays the tax, no problem arises.

(c) If the payer believes that only a part of the payment is chargeable to tax, he can apply under section 195(2) for deduction at appropriate rates and act accordingly. No interest is jeopardized.

(d) If the payer believes that a part of the payment is income chargeable to tax, and does not make an application under section 195(2), he will have to deduct tax from the entire payment. Thus, the interests of the Revenue stand protected.

(e) If the payer believes that the entire payment or a part of it is income chargeable to tax and fails to deduct tax at source, he will face all the consequences under the Act. The consequences can be the raising of demand under section 201, disallowance under section 40(a)(i), penalty, prosecution etc. The interests of the Revenue stand protected.

(f) If the payee wants to receive the payment without deduction of tax, he can apply for a certificate to that effect under section 195(3) and if he gets the certificate, no one is adversely affected.

(g) If the payee fails to get the certificate, he will have to receive payment net of tax. No interest is jeopardized.

Section 201 – Consequences of failure to deduct or pay:

“(1) Where any person, including the principal officer of a company,—

(a) who is required to deduct any sum in accordance with the provisions of this Act; or

(b) referred to in sub-section (1A) of section 192, being an employer, does not deduct, or does not pay, or after so deducting fails to pay, the whole or any part of the tax, as required by or under this Act, then, such person, shall, without prejudice to any other consequences which he may incur, be deemed to be an assessee in default in respect of such tax:

Provided that any person, including the principal officer of a company, who fails to deduct the whole or any part of the tax in accordance with the provisions of this Chapter on the sum paid to a payee* or on the sum credited to the account of a payee* shall not be deemed to be an assessee in default in respect of such tax if such payee*—

(i) has furnished his return of income under section 139;

(ii) has taken into account such sum for computing income in such return of income; and

(iii) has paid the tax due on the income declared by him in such return of income,

and the person furnishes a certificate** to this effect from an accountant in such form as may be prescribed:

Provided further that no penalty shall be charged under section 221 from such person, unless the Assessing Officer is satisfied that such person, without good and sufficient reasons, has failed to deduct and pay such tax.”

* – Substituted for “resident” by the Act No. 23 of 2019, w.e.f. 1-9-2019

** – Form 26A has been prescribed as per Rule 31ACB

The above Proviso clearly states that in case the conditions mentioned in it are satisfied, then the Assessee cannot be treated as an assessee in default for non-deduction of TDS. The Proviso was initially introduced w.r.t. to only Resident Payees. However, the same has been extended to all Payees by way of Amendment in Finance Act, 2019 w.e.f. 01-09-2019.

Even the recent judgement in the case of Shree Balaji Concepts [TS-393-ITAT-2022(PAN)], the Panaji ITAT held that the amended Section 201(1)-proviso is retrospective since it removes statutory anomaly over sum paid to NRs.

CBDT Instruction 2/2014 dated 26th February, 2014:

On getting references from field officers on the issue of deduction of tax at source under section 195 of the Income-tax Act, 1961 in the light of the decisions of the Supreme Court of India in the cases of GE India Technology (P.) Ltd. (supra) and Transmission Corpn. of AP Ltd. (supra) as also the decision of the Madras High Court in Chennai Metropolitan Water Supply and Sewerage Board (supra) with a request for clarification as to whether the tax is to be deducted under sub-section (1) of section 195 of the Act on the whole sum being remitted to a nonresident or only the portion representing the sum chargeable to tax, particularly if no application has been made undo sub-section (2) of section 195 of the Act to determine the sum the CBDT came out with Instruction No. 2/2014, dated 26-2-2014 wherein at para. 3 it has been clarified as under-

“The matter has been examined in the Board and, accordingly, in exercise of powers vested under section 119 of the Act, the Board hereby directs that in a case where the assessee fails to deduct tax under section 195 of the Act, the Assessing Officer shall determine the appropriate proportion of the sum chargeable to tax as mentioned in sub-section (1) of section 195 to ascertain the tax liability on which the deductor shall be deemed to be an assessee in default under section 201 of the Act, and the appropriate proportion of the sum will depend on the facts and circumstances of each case taking into account nature of remittances, income component therein or any other fact relevant to determine such appropriate proportion.”

RECOURSE TO CASE LAWS:

> Transmission Corporation of AP Ltd. vs. CIT (1999) 239 – ITR – 587 (SC):

Where the person responsible for deduction is fairly certain, then he can make his own determination:

“The Supreme Court has clearly laid down that where the person responsible for deduction is fairly certain then he can make his own determination. Moreover the argument of the assessee in the case before the Supreme Court was that section 195 contemplates tax deduction only for payments fully having character of income. The provision for determination of tax is a safeguard and this safeguard by way of workings can be furnished by a Chartered Accountant of the non-resident. As per provisions of Section 195(2) if still there is any doubt, with regard to appropriate proportion of such sum so chargeable to tax in the mind of the person making the payment of such sum to a non resident then such person may make an application to the Assessing Officer to determine by general or special order to determine the appropriate proportion with regard to tax deducted at source. The application can also be made under section 195(3) read with section 197 to the assessing officer by the recipient (payee) requesting the officer to issue necessary directions in this regard.”

> GE India Technology Centre (P) Ltd. vs. Commissioner of Income Tax & Anr. (2010) 44 DTR (SC) 201:

In case of a bona fide belief by the payer that no part of the payment bears income character, it is not mandatory for him to undergo the procedure of section 195(2) before making any payment to a non-resident:

“Supreme Court, overruling the decision of the Karnataka High Court in the case of CIT vs. Samsung Electronic Company Ltd. 320-ITR-209(Kar), has observed:

Most important expression in s. 195(1) consists of the words “chargeable under the provisions of the Act”—Payer is bound to deduct tax at source only if the sum paid is assessable to tax in India—A person paying interest or any other sum to a non-resident is not liable to deduct tax if such sum is not chargeable to tax under the IT Act—Sec. 195 also covers composite payments which have an element of income embedded or incorporated in them—Thus, where an amount is payable to a non-resident, the payer is under an obligation to deduct tax in respect of such composite payments—However, obligation to deduct tax is limited to the appropriate proportion of income which is chargeable under the Act—This obligation flows from the said words used in s. 195(1)—Sec. 195(2) pre-supposes that the person responsible for making the payment to the non-resident is in no doubt that tax is payable in respect of some part of the amount to be remitted but is not sure as to what should be the portion so taxable or the amount of tax to be deducted—In such a situation he is required to make an application to ITO(TDS) for determining the amount—It is only when these conditions are satisfied that the question of making an order under s. 195(2) arises – If the contention of the Department that the moment there is remittance the obligation to deduct tax arises is to be accepted, then the words “chargeable under the provisions of the Act” in S. 195(1) would stand obliterated – If the contention of the Department is accepted then the Department would be entitled to appropriate the moneys deposited by the payer even if it is not chargeable to tax because there is no provision in the Act whereby a payer can obtain refund—Sec. 237 r/w s. 199 implies that only the recipient of the sum can seek a refund – Thus, the interpretation of the Department leads to an absurd consequence—Entire basis of the Department’s contention is based on administrative convenience in support of its interpretation—There are adequate safeguards in the Act which would prevent revenue leakage.

The application (undertaking) for issuing of a certificate by the Income-tax Officer (Foreign Section) for NIL/less deduction can be made under section 195(2)[ refer circular no.10/2002 dated 09-10-2002 issued by CBDT] by the person responsible for making the payment along with the certificate of a Chartered Accountant specifying that the payment of sum does not attract tax or attracts tax at a lower rate based on the workings of the Chartered Accountant. In case of a bona fide belief by the payer that no part of the payment bears income character, it is not mandatory for him to undergo the procedure of section 195(2) before making any payment to a non-resident.

The application for NIL/less deduction can also be made by the payee (the recipient) to the Income-tax Officer (Foreign Section) in Form 13 with all necessary and relevant documents along with workings.

The Income-tax Officer (Foreign Section) on being satisfied with the correctness of the claim made by the applicant shall proceed to issue a certificate under section 195(3) of the Income-tax Act specifying the rate at which tax has to be withheld by the payer and remit it to the Income-tax department on behalf of the payee.”

> Van Oord ACZ India (P) Ltd. vs.CIT (2010)-3-taxmann.com 52 dated 15-03-2010 (DelhiHC):

Where in the Assessment Proceedings it is held that the sum received by NRI is not chargeable to tax, then the Payer is will not be treated as assessee-in-default:

“In case in the assessment proceedings relating to the non-resident recipient, if it is ultimately held that the sum received by the recipient was not chargeable to tax, the effect of that would be that there was no obligation on the assessee to deduct tax at source on the sum paid to the said non-resident and in that eventuality, the assessee will not be treated as assessee-in-default and would be absolved of any consequences for non deduction of tax at source.”

TDS will be applicable only if the payment is chargeable to income-tax either wholly or partly:

“The Special Bench has held that if the payer has a bonafide belief that no part of the payment has income character, then section 195(1) will not apply because section 195 will apply only if the payment is chargeable to income-tax either wholly or partly.”

> Income-tax Officer vs. Prasad Production Ltd. [2010] 003 ITR (Trib) 0058 (ITAT Chennai Special Bench)

Mangalore Refinery & Petrochemicals Ltd. vs. DDIT (113 ITD 85) (Mumbai ITAT):

The Assessee cannot be treated in default u/s 201 of the Act because it has applied u/s 195(2) of the IT Act before the AO, prior to remitting the Payment.

> Shree Balaji Concepts vs. ITO (Intnl. Taxation) [TS-393-ITAT-2022] [I.T.A. No. 73/PAN/2018] (Panaji ITAT):

Holds amended Sec.201(1)-proviso as retrospective since removes statutory anomaly over sum paid to NRs:

“Panaji ITAT allows Assessee’s appeal, holds amendment by Finance (No. 2) Act, 2019 extending the benefit contained in proviso to Section 201(1) for sum paid to non-resident to be applicable retrospectively; Thus holds that Assessee cannot be considered as assessee-in-default for failure to deduct tax at source under Section 195 in respect of purchase of immovable property from two nonresidents who disclosed the sale consideration in their respective returns; During AY 2012-13, Assessee-Firm purchased an immovable property from Mr. Elrice D’Souza and his wife for a consideration of Rs.10 Cr and did not deduct any tax at source while remitting the sum; Revenue held the Assessee as ‘assessee-in-default’ for not deducting tax under Section 195 and consequently raised demand of Rs.2.26 Cr under Section 201(1) and interest demand of Rs.1.22 Cr under Section 201(1A), which was confirmed by CIT(A); ITAT notes that the two sellers of the property have disclosed the consideration received from the Assessee in their respective return of income, considers Assessee’s contention that although proviso to Section 201(1) is applicable to resident-assessee as applicable on that particular date, the said beneficial relaxations allowed to the resident payees should also be considered and be applied to the non-residents as well, which is discriminatory in nature and should be equally applied to the non-residents; Notes that the legislature in its wisdom has thought about this discrimination and has vide the Finance (No. 2) Act, 2019 has extended the benefit of the proviso to Section 201(1) even to the non-residents, opines that “the said benefit has to be given retrospective effect, since, the said amendment has been brought into the statute only to remove the anomaly which was created in the statute and consequently any provision which has been inserted for removing any anomaly has to be given retrospective effect.”; Accepts Assessee’s reliance on SC ruling in Calcutta Export Company, Delhi HC ruling in Ansal Landmark Township, Mumbai ITAT ruling in Celltick Mobile and Bangalore ITAT ruling in Ananda Marakala; Accordingly, deletes demand of Rs. 2.26 Cr raised under Section 201(1); Further observes that the property purchase transaction was undertaken in Sep 2011 while the non-resident sellers’ filed their return of income in July 2012 and accordingly directs Revenue to recalculate interest under Section 201(1A) for the period Oct 7, 2011 (being due date of remittance of TDS for the month of Sept) to July 30, 2012 (being the date of filing of return).”

Concluding Remarks:

1. Before entering into Transaction:

- In our opinion, it is always advisable to make an application in Form 13 by the Payee (i.e. Seller) u/s 195(3) of the Act. The Payer may not be interested in making the Application, so it’s usually the Payee’s interest to make the application.

- Take TAN No.

2. At the time of Transaction:

- Prevention is always better than cure.

- Deduct TDS (along with applicable Surcharge and Cess) as per Lower TDS Certificate, if available, or else Deduct TDS as per Rates Applicable (on STCG / LTCG).

3. After the Transaction:

- Pay TDS u/s 195 within 7 days of next month of TDS Deduction

- File TDS Return in Form 27Q as per Due Date applicable for relevant quarter.

- In case TDS is not deducted and Lower Deduction Application is also not made, then recourse can be made to Instruction 2/2014 dated 26th February, 2014 and various case laws with regards to taxability of only income element in payments covered under section 195 of the Act.

- Protection provided by case laws and circulars should be resorted to only in case of bonafide ignorance and should not become a habit.

Amendments required:

Rather than filing of TDS Return in Form 27Q, a simpler Challan cum Return Statement like Form 26QB should be made available. This move will go away with unnecessary requirement of taking TAN No.

Author Bio