The Taxation Laws (Amendment) Ordinance, 2019 has been promulgated by President of India on 20th September, 2019 with a view to amend Income Tax Act, 1961 and Finance Act (No. 2), 2019.

The ordinance intends to provide impetus to the growth amidst the ostensible slowdown.

Highlights of the said ordinance include:

1. Reduction of corporate tax from 30% to 22%;

2. Reduction of minimum alternate tax rate from 18.5% to 15%;

3. Roll back of tax on buy back of shares wherein announcement of buy back was made prior to the budget date i.e. 5th July, 2019 and

4. Roll back of higher surcharge of 25% and 37% which was imposed by Finance Act, 2019 in the following cases:

a. Foreign Institutional Investors (FIIs) deriving income by way of capital gains from transfer of securities covered under section 115AD (1)(b);

b. Individuals, HUF, BOI, AOP and artificial judicial person deriving income by way of capital gains on transfer of equity shares or units of equity-oriented funds (covered u/s 111A and 112A).

The article focuses primarily on the first two points i.e. reduction of normal tax rate and reduction of minimum alternate tax rate in light of the afore-mentioned ordinance and circular no. 29/2019 issued by CBDT which clarifies the restrictions that need to be borne in mind prior to opting for concessional regime.

Article is structured as under:

A. Corporate tax rate under normal provisions of Income Tax Act, 2019 pre and post ordinance;

B. Case Specific analysis so as to decide whether or not to opt for new regime;

C. Generalization based on part B – Flow-chart to assist in decision making.

Before proceeding, Section 115BAA and Section 115BAB need to be briefly explained:

Section 115BAA: Option for companies to avail concessional tax rate of 22% (Effective Rate 25.17%) and also exemption from MAT provided they don’t avail certain exemptions and cannot avail set-off of loss going forward on account of those exemptions and in light of clarification of CBDT provided vide Circular no. 29/2019, they cannot avail MAT credit and brought forward loss on account of additional depreciation.

Section 115BAB: Option for manufacturing companies incorporated on or after 01/10/2019 to avail concessional tax rate of 15% (Effective Rate 17.16%) and exemption from MAT but subject to prescribed conditions regarding its formation in addition to conditions similar to those as stated in Section 115BAA.

In both the above cases, option once exercised cannot be subsequently withdrawn.

A. Corporate tax rate under normal provisions of Income Tax Act, 2019 pre and post ordinance

The following table shows computation of impact on effective tax rate ignoring minimum alternate tax (MAT) presuming that Option u/s 115 BAB (in case of domestic manufacturing company incorporated after 01/10/2019) or option u/s 115BAA (in case of domestic companies other than domestic manufacturing company incorporated after 01/10/2019) is exercised:

Comments:

- As can be seen from differences owing to amendment above, small companies with total income of up to Rs. 1 crore are least benefitted while the to be incorporated large manufacturing companies will be most benefitted.

- Also, most of profitable listed companies shall also be substantially benefitted as most of them would see reduction of nearly 9.8% in effective tax rate (excluding the cases where MAT applies.)

- It may be pertinent to note that under the concessional regime, surcharge is at a flat rate of 10% on the respective corporate tax of 22%/15% in case of Section 115BAA and Section 115BAB respectively. The said rate is then increased by Heath and Education Cess of 4% yielding effective tax rate of 25.17% and 17.16%.

B. Case Specific analysis so as to decide whether or not to opt for concessional regime

1. Domestic Mfg. Cos. incorporated between 01/03/2016 and 30/09/2019 and Domestic Cos. whose turnover or gross receipts for FY 2017-18 did not exceed Rs. 400 crore (Both the cases are clubbed as the implications are identical:

To assess whether or not to opt for the concessional regime, it is quintessential to identify whether the tax is likely to be paid under MAT regime or under normal provisions of income tax act.

Such identification is important as it would enable to decide whether MAT credit would be utilized or not.

Ascertainment of MAT utilization is critical as once the concessional regime is opted for, MAT credit would lapse.

For the cases as titled above, it can be observed if tax is likely to be paid under MAT provisions, company would be better off if it chooses to not opt for option under Section 115BAA because it would pay lower tax in the form of MAT otherwise.

In case if it doesn’t have MAT credit and its unlikely that tax would be payable as per MAT provisions going forward, then it can straight away opt for concessional regime.

However, case gets slightly complicated when it’s likely that tax would not be paid as per MAT and the company has unutilized MAT credit at its disposal.

In such a scenario, calculation needs to be made whether MAT credit will lead to reduction in liability greater than difference between normal provision and MAT provision. For example, MAT credit is substantial enough let’s say 12% of total income, in case of company in total income range of 1 crore to 10 crore where difference between MAT and normal tax rate is 11.13% as can be seen from table above. In this case, it would be advisable to defer the option of paying tax under concessional regime (Section 115BAA) by 1 year so that MAT credit is almost utilized and doesn’t lapse. Such strategic delay is suggested in the circular no. 29/2019 itself of CBDT.

Now, in the next year, MAT credit is as meagre as 0.87% (12% – 11.13%) of total income (assuming income remains constant) . In such scenario, it is advisable to opt for concessional regime straight away as in order to capitalize on 0.87% of available credit (leading to tax out go of 27.82% – 0.87% = 26.95%), the company would be better off instead to pay straight tax of 25.17%.

Similar analysis is done for remaining two cases as under:

2. Domestic Mfg. Cos. incorporated on or after 01/10/2019

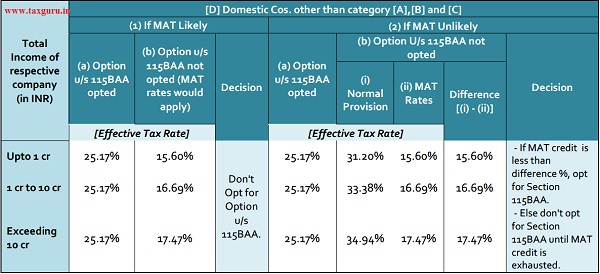

3. Domestic Companies other than afore-mentioned special cases:

Presumption:

Its noteworthy that flat surcharge @10% irrespective of level of income has been made applicable only for newly introduced section 115BAA and Section 115BAB.

The amendment is not clear as to this flat surcharge would be applicable to tax rate applicable for MAT rate as well.

For performing the above analysis, it has been presumed that flat surcharge would not apply to MAT rate and hence surcharge for MAT rate has been computed @7% for total income in the range of INR 1 crore to INR 10 crore and @12% for cases wherein total income exceeds INR 10 crore.

C. Generalization based on analysis done in part B- Flow-chart to assist in decision making

The following generalization can be deduced having analyzed the above 4 scenarios:

(Author Can be reached at email id for suggested correction: priyeshsjoshi@yahoo.com)

Also Read relevant Press Releases and Notifications