Seventh Proviso to Section 139(1)

Mandatory Furnishing of Return of Income by Certain Person – Finance Act 2019

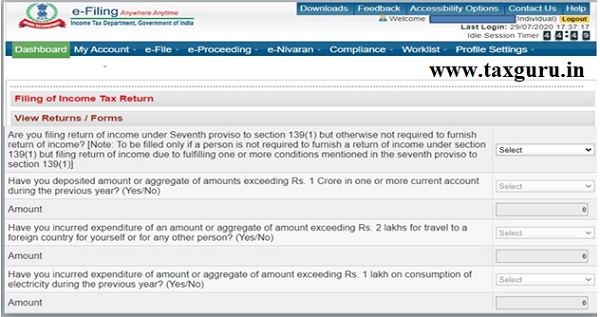

High Value Transactions-

Currently, a person (other than a company or a firm) is required to furnish the return of income only if his total income exceed the maximum amount not chargeable to tax, subject to certain excitations, Therefore, a person entering into certain high value transaction is not necessarily required to furnish his return of income, In order to ensure that persons who enter into certain high value transactions do furnish their return of income, section 139 has been amended with effect from April 1, 2020 (i.e., from the assessment year 2020-21 onward). A person (other than a company or a firm) shall be mandatorily required to file his return of income, if during the previous year, he-

a. Has deposited an amount (or aggregate of the amounts) exceeding Rs.1 crore in one or more current account maintained with a banking company or a co-operative bank; or

b. Has incurred expenditure of an amount (or aggregate of the amounts) exceeding Rs.2 lakh for himself, or any other person for travel to a foreign country; or

c. Has incurred expenditure of an amount (or aggregate of the amounts) exceeding Rs.1 lakh towards consumption of electricity; or

d. Fulfil such other prescribed conditions, as may be prescribed.

Persons claiming exemption under sections 54, 54B, etc.- Currently, a person claiming rollover benefit of exemption from capital gains tax on investment in specified assets like house, bonds, etc., is not required to furnish a return of income, if after claim of such rollover benefits, his total income is not more than the, exemption limit, In order to make furnishing of return compulsory for such persons, sixth proviso to section 139(1) has been amended with effect from Assessment year 2020-21 onwards.

Author Bio